🧠 Trading Logic

This strategy is a simple, fully mechanical system that separates its logic for long and short trades. Long positions are opened when there is no current long trade and the 12,5 Stochastic oscillator drops below 29, which is a classic oversold threshold. In other words, it looks to buy after short-term weakness, aiming to catch potential bounces. Each long trade is protected by a volatility-based stop loss set at 1.5 times the 13‑period Average True Range (ATR), and it targets a fixed 3.7% profit. Because of the oversold trigger and moderate profit target, the long side appears designed for relatively short‑term, mean‑reversion style entries rather than long trend-following moves.

On the short side, the logic is stricter and more trend-oriented. A short position is only opened when no short is already open and a faster 20‑period moving average (with smoothing 8) crosses below a slower 95‑period moving average (with smoothing 2), while the 12‑period RSI is above 70. This combination looks for overbought conditions (high RSI) that occur at the same time as a bearish moving average crossover, suggesting the strategy wants to sell into potential downside trend beginnings rather than random spikes. Short trades use a wider volatility stop at 2.3 times the 8‑period ATR and aim for a larger 8.3% profit. The asymmetry between the long and short sides—different entry logic, different ATR multipliers, and much larger profit targets on shorts—suggests the system is trying to exploit potentially bigger downside moves while keeping long trades more conservative and quicker.

Overall, this code reflects a hybrid approach: mean-reversion style entries on the long side, and trend-following / breakout style entries on the short side, with all exits managed by a mix of ATR-based stops and fixed percentage profit targets. It may be better suited to markets and timeframes where downside moves tend to be sharper and more extended than rallies, and where volatility-based risk management is preferred over fixed-point stops. Traders should be aware that the system never pyramids (cumulateorders is off), and it always waits for the current position to be flat before opening a new one on the same side, which keeps position management straightforward but may limit exposure in strongly trending environments.

📊 Performance Metrics

| Metric |

Value |

Metric |

Value |

| Score (SQN) | 1.30 | Sharpe Ratio | 1.05 |

| Profit Factor | 1.35 | Max Drawdown | 15.20% |

| Ulcer Index | 0.029 | Stability (R²) | 0.892 |

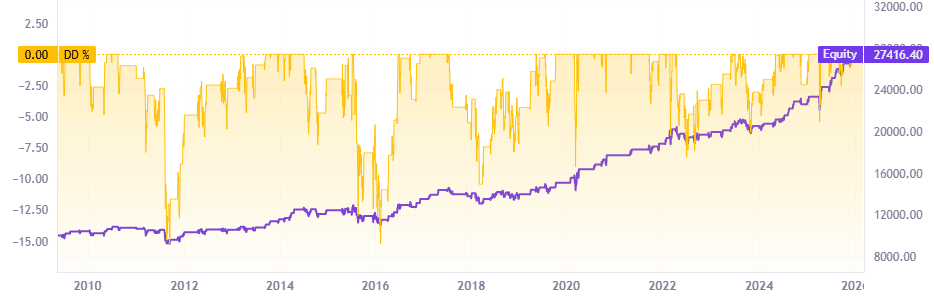

| Trades | 207 | PnL ($) | 17,416 |

| Time in Market | 27.30% | MC Score | 60.0 |

📈 Backtest Context

| Instrument | DAX P (^GDAXI) |

Timeframe | 1d |

| Period | 2010-01-13 → 2026-03-03 |

Seed | 217126686 |

📉 Equity Curve

⚠️ Community-generated strategy — please read before trading

This strategy was automatically generated by a community member using

ProRealQuant, a free tool for automated strategy generation on ProRealTime. It is shared purely for educational and discussion purposes.

Past backtest results do not guarantee future performance. Always conduct your own analysis, apply sound risk management, and never trade with capital you cannot afford to lose.

💻 ProBuilder Code

// Generated ProBuilder Strategy

// Auto-generated from ProRealQuant

DEFPARAM cumulateorders=false

DEFPARAM preloadbars = 200

// Long Entry Condition

BuyCondition = NOT LONGONMARKET AND Stochastic[12,5](close) < 29

// Short Entry Condition

SellCondition = NOT SHORTONMARKET AND (AVERAGE[20, 8](close) CROSSES UNDER AVERAGE[95, 2](close) AND RSI[12] > 70)

// Market Orders

IF BuyCondition AND NOT SellCondition THEN

BUY AT MARKET

// Stop Loss Exit

SET STOP LOSS (1.5 * AVERAGETRUERANGE[13])

// Take Profit Exit

SET TARGET %PROFIT (3.7)

ENDIF

IF SellCondition AND NOT BuyCondition THEN

SELLSHORT AT MARKET

// Stop Loss Exit

SET STOP LOSS (2.3 * AVERAGETRUERANGE[8])

// Take Profit Exit

SET TARGET %PROFIT (8.3)

ENDIF

💬 Join the discussion! Feel free to share your own backtest results on different instruments or timeframes, suggest improvements, propose forks or parameter variations — the community learns best together.

🔧 Generated with ProRealQuant — a free community tool for automated strategy generation and backtesting on ProRealTime. Try it yourself!