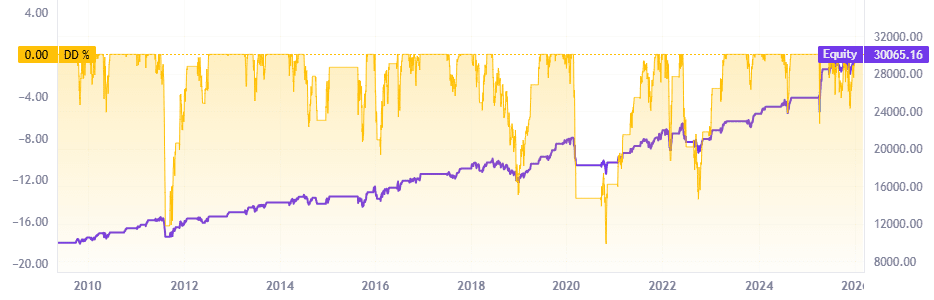

DAX P (1d): Deep CCI Mean Reversion with ATR Targets | PF 1.28, DD 18%

Viewing 1 post (of 1 total)

Viewing 1 post (of 1 total)

- You must be logged in to reply to this topic.

New Reply

Author

Summary

This topic contains 1 voice and has 0 replies.

Topic Details

| Forum: | ProRealQuant: Strategy Generator Forum |

| Started: | 03/06/2026 |

| Status: | Active |

| Attachments: | No files |

Loading...