User @Alessio posted a custom indicator on the italian forum, to tell Trending from Ranging markets (https://www.prorealcode.com/topic/indicatore-per-laterale-laterale-inclinato-trend/).

I liked it and wanted to give it a try on DAX, 1-hour TF, with Nicolas’trailing stop code on the 20-second TF. I decided to embed the indicator in the strategy, instead of CALLing it.

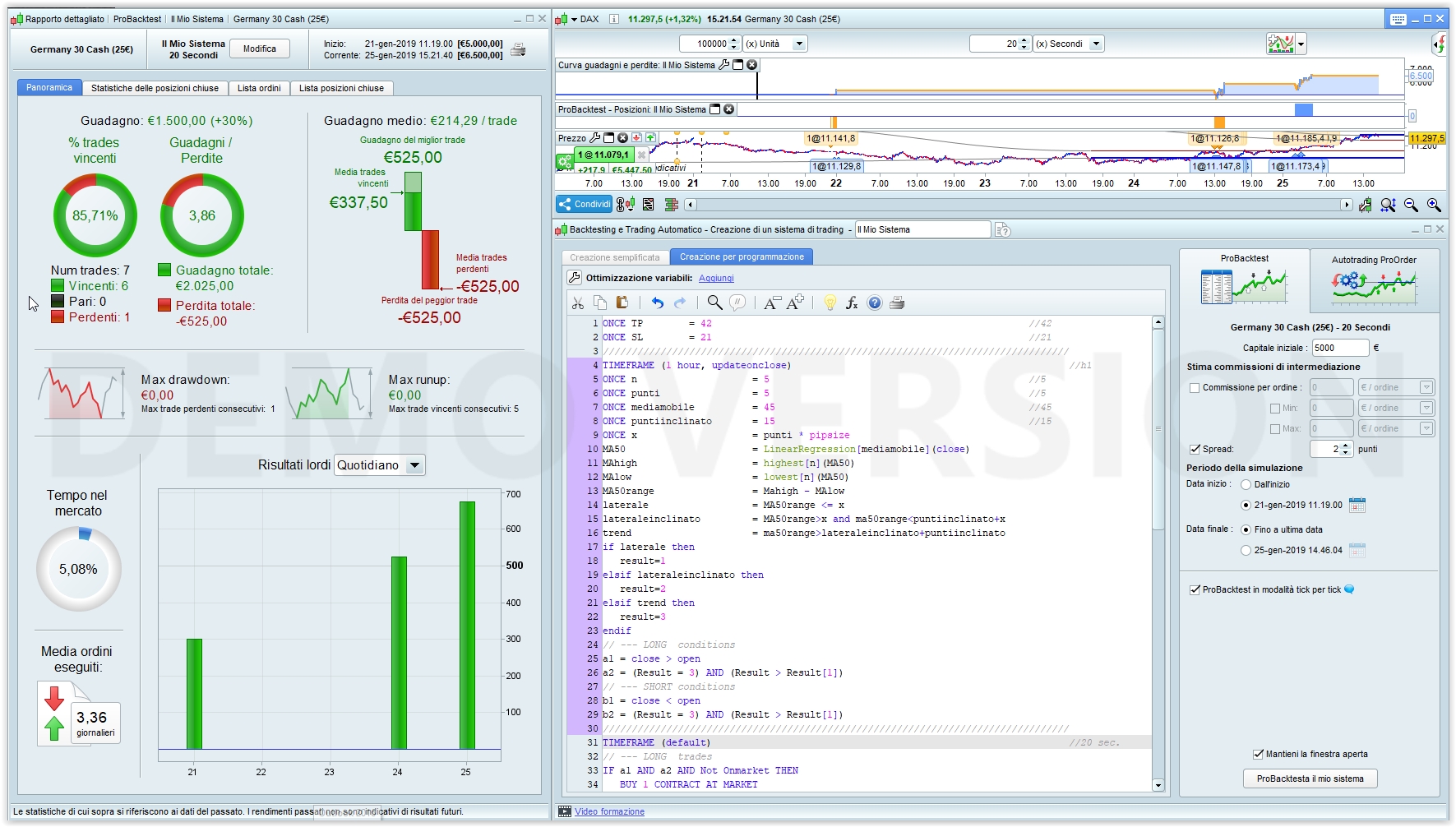

The indicators returns 1 for ranging market, 2 for sloping ranges and 3 for trending markets. I decided to enter a position (based on the direction of each candle) whenever it rises from 2 to 3.

Performance seems rewarding:

ONCE TP = 42 //42

ONCE SL = 21 //21

/////////////////////////////////////////////////////////////////////////////////

TIMEFRAME (1 hour, updateonclose) //h1

ONCE n = 5 //5

ONCE punti = 5 //5

ONCE mediamobile = 45 //45

ONCE puntiinclinato = 15 //15

ONCE x = punti * pipsize

MA50 = LinearRegression[mediamobile](close)

MAhigh = highest[n](MA50)

MAlow = lowest[n](MA50)

MA50range = Mahigh - MAlow

laterale = MA50range <= x

lateraleinclinato = MA50range>x and ma50range<puntiinclinato+x

trend = ma50range>lateraleinclinato+puntiinclinato

if laterale then

result=1

elsif lateraleinclinato then

result=2

elsif trend then

result=3

endif

// --- LONG conditions

a1 = close > open

a2 = (Result = 3) AND (Result > Result[1])

// --- SHORT conditions

b1 = close < open

b2 = (Result = 3) AND (Result > Result[1])

/////////////////////////////////////////////////////////////////////////////////

TIMEFRAME (default) //20 sec.

// --- LONG trades

IF a1 AND a2 AND Not Onmarket THEN

BUY 1 CONTRACT AT MARKET

ENDIF

// --- SHORT trades

IF b1 AND b2 AND Not Onmarket THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

//

SET TARGET pPROFIT TP

SET STOP pLOSS SL

//**************************************************************************

//trailing stop function

trailingstart = 10 //10 trailing will start @trailinstart points profit

trailingstep = 3 //3 trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

the trend phase, I thought only for the exit, nice trailing

Dear fellow traders,

First, thanks to robertogozzi for this very effective trailing stop. You can see from the screenshot very little difference between MFE and exit price.

I was impressed with the effectiveness of the indicator shared by Alessio on the Italian forum, so I called it “Da Vinci”. Thank you Alessio!

I’m stuck with an MTF issue. I’m testing this H1 System run on 5min chart, which I’m testing only on 2k for the example. I expect the signals to be taken on the 1 hour basis. However, some of the trades are taken outside of this rule. For example, on 4 Jan. 2022 at 12:15 the System took a Long trade, while there is no Signal on the H1 chart between 11 and 13 and the Signal is Short on the 5min chart.

Can you please help to fix this MTF issue?

Any suggestions how to this strategy? Your ideas or comments are welcome!

DEFPARAM CUMULATEORDERS= FALSE

DEFPARAM PreLoadBars = 2000

//////////////////////////////////////////////////////////////////////////////////////////////////////////////////

TIMEFRAME(60 MINUTES, UPDATEONCLOSE)

//////////////////////////////////////////////////////////////////////////////////////////////////////////////////

// Ehlers RMS

flen = 8//5//9//8//40 //fast length

slen = 21//26//21//60 //slow length

if barindex>slen then

a1= 5/flen

a2= 5/slen

PB = (a1 - a2) * close + (a2*(1 - a1) - a1 * (1 - a2))* close[1] + ((1 - a1) + (1 - a2))*(PB[1])- (1 - a1)* (1 - a2)*(PB[2])

RMSa = summation[50](PB*PB)

RMSplus = sqrt(RMSa/50)

RMSminus = -RMSplus

endif

IF PB > RMSminus and PB > PB[1] THEN

LongRMS=+1

ENDIF

IF PB < RMSplus and PB < PB[1] THEN

ShortRMS=-1

ENDIF

//////////////////////////////////////////////////////////////////////////////////////////////////////////////////

// Stochastics

StoK = Stochastic[8,1](close)

StoD = Average[3](Stochastic[8,1](close))

IF (StoK >= 20) and (StoK > StoD) and (StoK > StoK[1]) THEN

LongSto=+1

ENDIF

IF (StoK <= 80) and (StoK < StoD) and (StoK < StoK[1]) THEN

ShortSto=-1

ENDIF

//////////////////////////////////////////////////////////////////////////////////////////////////////////////////

// Vigor Index

PeriodRVI = 8 //5//12

diffRVI = close - open

ind1RVI = (diffRVI + 2*diffRVI[1] + 2*diffRVI[2] + diffRVI[3]) / 6

ind2RVI = (Range + 2*Range[1] + 2*Range[2] + Range[3]) / 6

condRVI = Summation[periodRVI](ind2RVI)

IF condRVI = 0 THEN

temp = 0.0001

ELSE

temp = condRVI

ENDIF

RVI = Summation[periodRVI](ind1RVI) / temp

RVIsig = (RVI + 2*RVI[1] + 2*RVI[2] + RVI[3]) / 6

IF (RVI > RVI[1]) and (RVI > RVIsig) THEN

LongRVI=+1

ENDIF

IF (RVI < RVI[1]) and (RVI < RVIsig) THEN

ShortRVI=-1

ENDIF

//////////////////////////////////////////////////////////////////////////////////////////////////////////////////

// Moving Average Crossing

PFast = 8//5

PSlow = 21//13

HullFast = HullAverage[PFast](close)

HullSlow = HullAverage[PSlow](close)

EndPFast = EndPointAverage[PFast](close)

EndPSlow = EndPointAverage[PSlow](close)

TSFast = TimeSeriesAverage[PFast](close)

TSSlow = TimeSeriesAverage[PSlow](close)

LRFast = LinearRegression[PFast](close)

LRSlow = LinearRegression[PSlow](close)

ZLEMAFast = ZLEMA[PFast](close)

ZLEMASlow = ZLEMA[PSlow](close)

iRSI = RSI[14](close)

IF HullFast > HullSlow and iRSI > iRSI[1] THEN

LongMA1=1

elsif HullFast < HullSlow and iRSI < iRSI[1] THEN

ShortMA1=-1

ENDIF

IF EndPFast > EndPSlow and iRSI > iRSI[1] THEN

LongMA2=2

elsif EndPFast < EndPSlow and iRSI < iRSI[1] THEN

ShortMA2=-2

ENDIF

IF TSFast > TSSlow and iRSI > iRSI[1] THEN

LongMA3=3

elsif TSFast < TSSlow and iRSI < iRSI[1] THEN

ShortMA3=-3

ENDIF

IF LRFast > LRSlow and iRSI > iRSI[1] THEN

LongMA4=4

elsif LRFast < LRSlow and iRSI < iRSI[1] THEN

ShortMA4=-4

ENDIF

IF ZLEMAFast > ZLEMASlow and iRSI > iRSI[1] THEN

LongMA5=5

elsif ZLEMAFast < ZLEMASlow and iRSI < iRSI[1] THEN

ShortMA5=-5

ENDIF

IF LongMA1=1 OR LongMA2=2 OR LongMA3=3 OR LongMA4=4 OR LongMA5=5 THEN

LongMA=+1

ENDIF

IF ShortMA1=-1 OR ShortMA2=-2 OR ShortMA3=-3 OR ShortMA4=-4 OR ShortMA5=-5 THEN

ShortMA=-1

ENDIF

//////////////////////////////////////////////////////////////////////////////////////////////////////////////////

// Da Vinci Trend Detector

PeriodRangelateral = 8//5

MultiplierATR = 0.5

Points = AverageTrueRange[14](close) * MultiplierATR

InclinedPoints = 15

MAPeriod = 50

n = PeriodRangelateral //4 dax

x = Points * pipsize //5 a 15 laterale dax

MA50 = LinearRegression[MAPeriod](close) //da 20 a 60 triangolare

MAhigh = highest[n](MA50)

MAlow = lowest[n](MA50)

MA50range = Mahigh - MAlow

laterale = MA50range <= x

lateraleinclinato = MA50range>x and ma50range<InclinedPoints+x

trend = ma50range>lateraleinclinato+InclinedPoints

if laterale then

ResultDaVinci=1

elsif lateraleinclinato then

ResultDaVinci=2

elsif trend then

ResultDaVinci=3

endif

IF ResultDaVinci>=2 THEN //and (ResultDaVinci <> ResultDaVinci[1])

TrendDaVinci=+1

ENDIF

// TSI

PeriodTSIFast = 9

PeriodTSISlow = 2 * PeriodTSIFast

aTSI = (ExponentialAverage[PeriodTSIFast](ExponentialAverage[PeriodTSISlow](ROC[1](close))))

bTSI = (ExponentialAverage[PeriodTSIFast](ExponentialAverage[PeriodTSISlow](ABS(ROC[1](close)))))

TSI = 100 * (aTSI/bTSI)

LongMAExit = HullAverage[PExitL](close)

ShortMAExit = HullAverage[PExitS](close)

////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

//////////////////////////////////////////////////////////////////////////////////////////////////////////////////

// Combo

LongDaVinci=0

ShortDaVinci=0

IF LongRMS=+1 AND LongSto=+1 AND LongRVI=+1 AND LongMA=+1 AND TrendDaVinci=+1 AND (TSI>TSI[1]) AND (close>open and close>close[1] and close>open[1]) THEN

LongDaVinci=+1

ENDIF

IF ShortRMS=-1 AND ShortSto=-1 AND ShortRVI=-1 AND ShortMA=-1 AND TrendDaVinci=+1 AND (TSI<TSI[1]) AND (close<open and close<close[1] and close<open[1]) THEN

ShortDaVinci=-1

ENDIF

IF LongDaVinci=+1 THEN

MySignal = LongDaVinci

ENDIF

IF ShortDaVinci=-1 THEN

MySignal = ShortDaVinci

ENDIF

x = MySignal

IF MySignal = MySignal[1] THEN

x = 0

ENDIF

//////////////////////////////////////////////////////////////////////////////////////////////////////////////////

TIMEFRAME(DEFAULT)

//////////////////////////////////////////////////////////////////////////////////////////////////////////////////

IF NOT LongOnMarket AND (x = 1) THEN

BUY 1 CONTRACTS AT MARKET

endif

if LongOnMarket and -(x = -1) then

SELL AT MARKET

SELLSHORT 1 CONTRACTS AT MARKET

ENDIF

IF NOT ShortOnMarket AND -(x = -1) THEN

SELLSHORT 1 CONTRACTS AT MARKET

endif

if ShortOnMarket and (x = 1) then

EXITSHORT AT MARKET

BUY 1 CONTRACTS AT MARKET

ENDIF

//TIMEFRAME(DEFAULT)

If LongOnMarket AND (close crosses under LongMAExit OR -(x = -1)) THEN

SELL AT MARKET

ENDIF

IF ShortOnMarket AND (close crosses over ShortMAExit OR (x = 1)) THEN

EXITSHORT AT MARKET

ENDIF

//////////////////////////////////////////////////////////////////////////////////////////////////////////////////

/////// BREAKEAVEN ///////////

once breakeaven = 1//0 //1 on - 0 off

//StartBreakeven = 30

//PointsToKeep = 5

//reset the breakevenLevel when no trade are on market

if breakeaven>0 then

IF NOT ONMARKET THEN

breakevenLevel=0

ENDIF

// --- BUY SIDE ---

//test if the price have moved favourably of "startBreakeven" points already

IF LONGONMARKET AND close-tradeprice(1)>=startBreakeven*pipsize THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)+PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

SELL AT breakevenLevel STOP

ENDIF

// --- end of BUY SIDE ---

IF SHORTONMARKET AND tradeprice(1)-close>startBreakeven*pipsize THEN

//calculate the breakevenLevel

breakevenLevel = tradeprice(1)-PointsToKeep*pipsize

ENDIF

//place the new stop orders on market at breakevenLevel

IF breakevenLevel>0 THEN

EXITSHORT AT breakevenLevel STOP

ENDIF

endif

//////////////////////////////////////////////////////////////////////////////////////////////////////////

// Trailing Stop

//------------------------------------------------------------------------------------

IF Not OnMarket THEN

//TrailStart = 10 //10 Start trailing profits from this point

//BasePerCent = 0.100 //10.0% Profit to keep

//StepSize = 6 //6 Pips chunks to increase Percentage

//PerCentInc = 0.100 //10.0% PerCent increment after each StepSize chunk

RoundTO = -0.5 //-0.5 rounds to Lower integer, +0.4 rounds to Higher integer

PriceDistance = 4 * pipsize//8.9 minimun distance from current price

y1 = 0

y2 = 0

ProfitPerCent = BasePerCent

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN //go ahead only if N+ pips

Diff1 = abs(TrailStart - x1)

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO))

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc))

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent))

y1 = max(x1 * ProfitPerCent, y1) //y = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN//SHORT

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN //go ahead only if N+ pips

Diff2 = abs(TrailStart - x2)

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO))

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc))

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent))

y2 = max(x2 * ProfitPerCent, y2) //y = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y>0

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

IF abs(close - SellPrice) > PriceDistance THEN

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y>0

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

IF abs(close - ExitPrice) > PriceDistance THEN

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

EXITSHORT AT Market

ENDIF

ENDIF

SET STOP %LOSS 0.5

I expect the signals to be taken on the 1 hour basis

TIMEFRAME(DEFAULT) will read the signal from the TF you are running on (5 minute). You can either run it on 1 hour, or delete TIMEFRAME(DEFAULT)

A LONG signal occurred at the 11:00 candle, which closes at 11:59, so it is valid till 12:59.

A LONG trade was entered at 12:00 (as soon as the 11:00 candle closed) and, since it was exited quite soon, it entered another one according to the same signal.

Thank you robertogozzi and nonetheless!

Do you think of any filter I can add to avoid this or to improve the strategy overall?

Just a trade per H1 candle maybe?

Thank you phoentzs

I tried to limit to 1 trade per hour on H1/M1 TF, but results were not satisfactory.

I kept H1/M1 and optimized Trailing Stop, Stop Loss and Exit Strategy and I now have a reasonable outcome on 5k, R/R 2.28, Sharpe 1.2, Win Rate 69% and Net Gain/Drawdown = 6.4. Now, time to test on 100k and see.

I am excited. I always find it very difficult to track trends on the DAX. SP500 or Nasdaq are easier there.

Choppy market is THE PROBLEM !

I know that’s why I don’t like Dax anymore. Or I’m doing something wrong.

I trade manually only Dow (usually directional and you can capture 50 to 100pts quickly), and I have one Algo on NQ (because usually volatile), which I tested in Demo mode for one year, it generated 500% with 1 lot and an SL of 140pts. I’m trying to write an Algo targeting moves of 200pts on Dow, but it requires large SL (200pts)… Lately, I found myself letting the NQ Algo take the trade, then manage the rest manually. The Algo does usually better than me: Psychology is key! The NQ Algo is extremly simple (39 lines), Stoch + MACD with a few filters.

Hello – thank you for posting this. What time zone are you running it on, as my results are negative when I run a backtest? I know I must be doing something wrong 🙂 Thank you

I am testing on an IG CFD demo account, UK time zone on the NASDAQ 5m time frame

The last screenshot is NQ, (k units, H1/1M TF, which is different from the code I posted above (H1/M5), But when I switched to H1M5, I adapted the SL, Trailing Stop, etc. I’m running under French time zone.

Please note the System above is meant to be an example, it’s not a finished, so please feel free to tweak it and let us know how you improved it.