Hi all,

Newbie here with creating PRT strategies and would really welcome feedback on my first effort.

I am developing a strategy for 5 minute candles on DAX.

The concept is such:

- Price makes an extreme RSI reading (Less than 20; Greater than 80)

- Price subsequently closes beyond 21ma (Above for long; below for short)

- Order is placed 2 pips beyond high/low of candle which closed beyond 21ma

- Stop is at the entry candle high/low

- Target = 2*stop distance

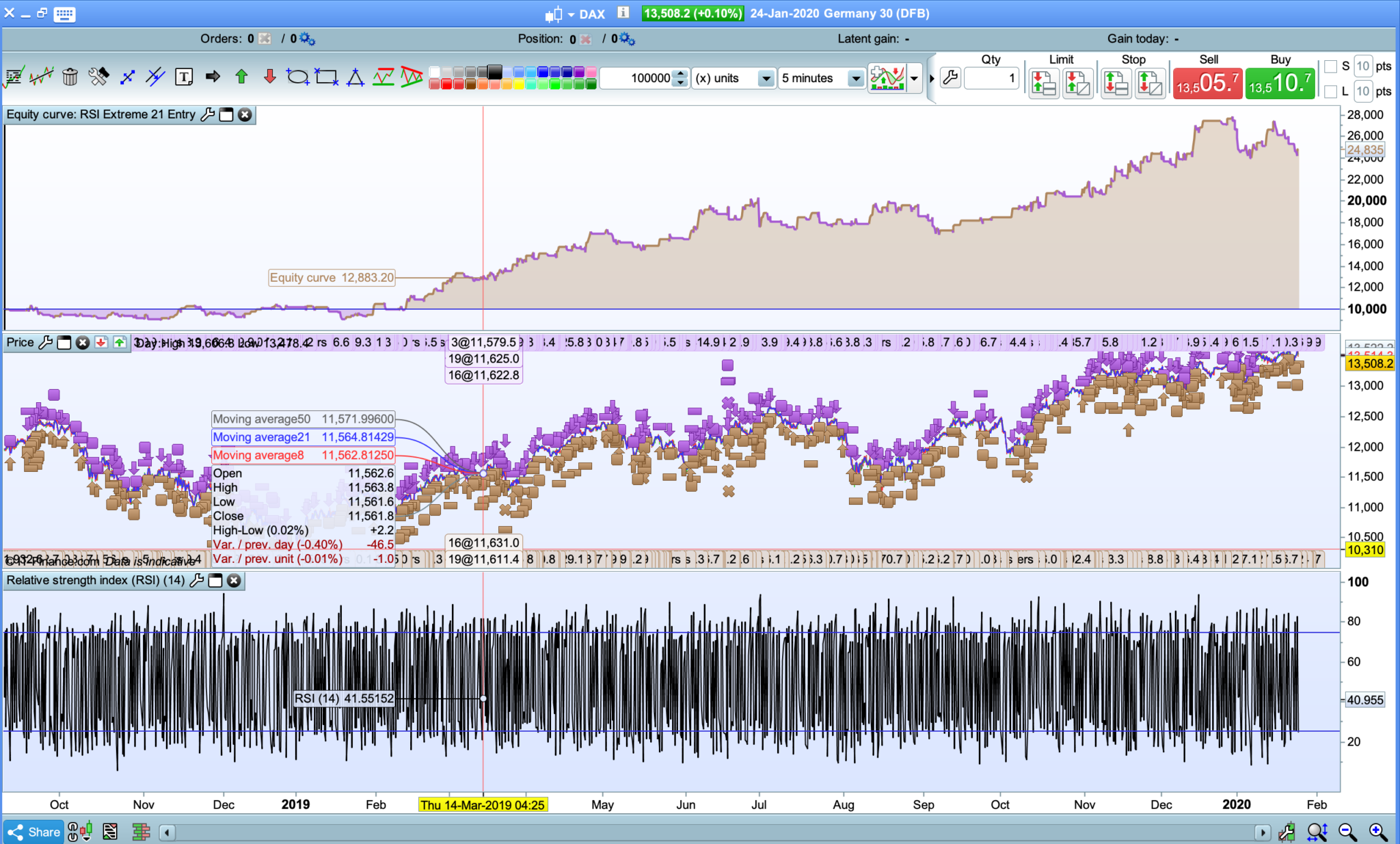

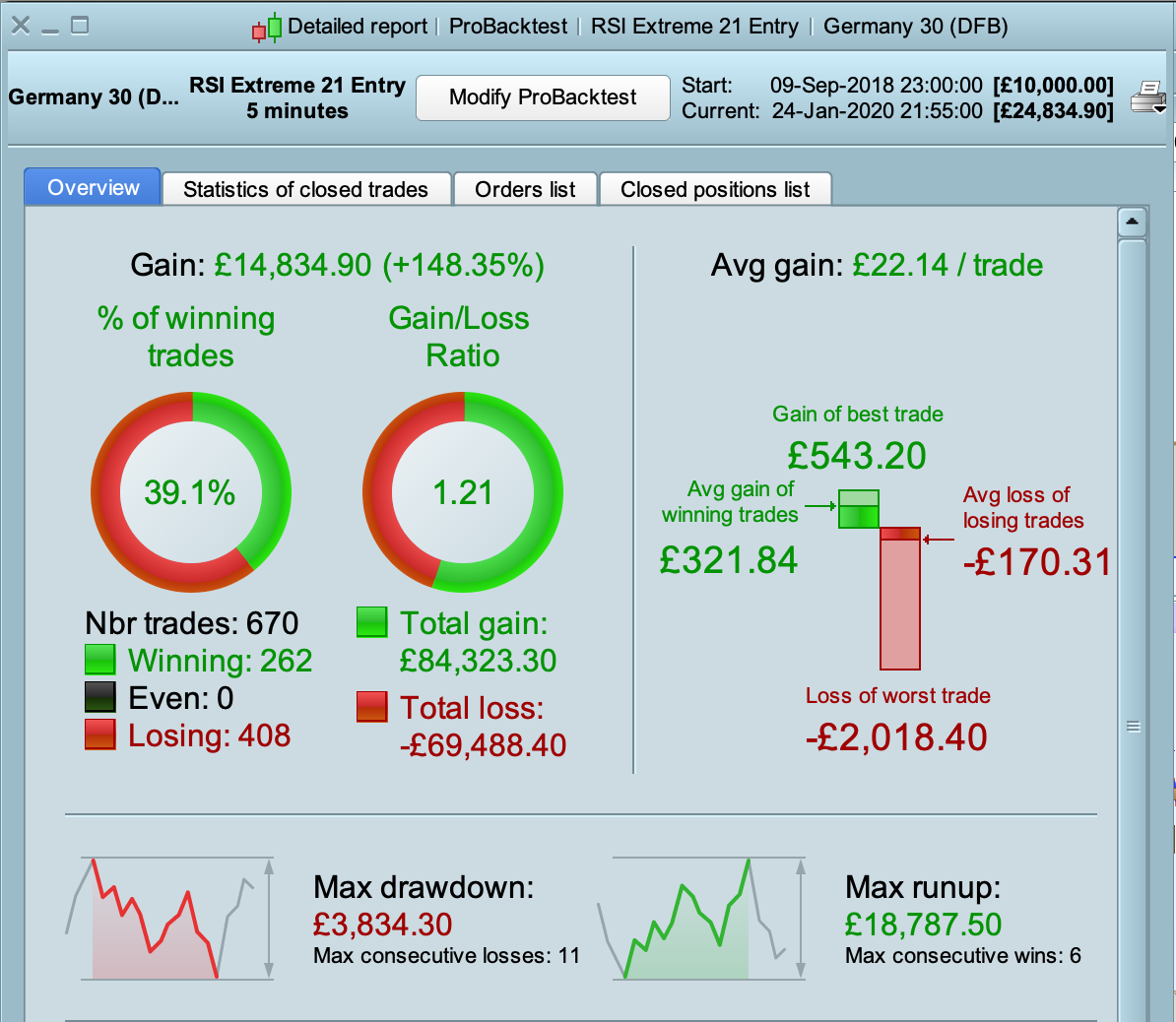

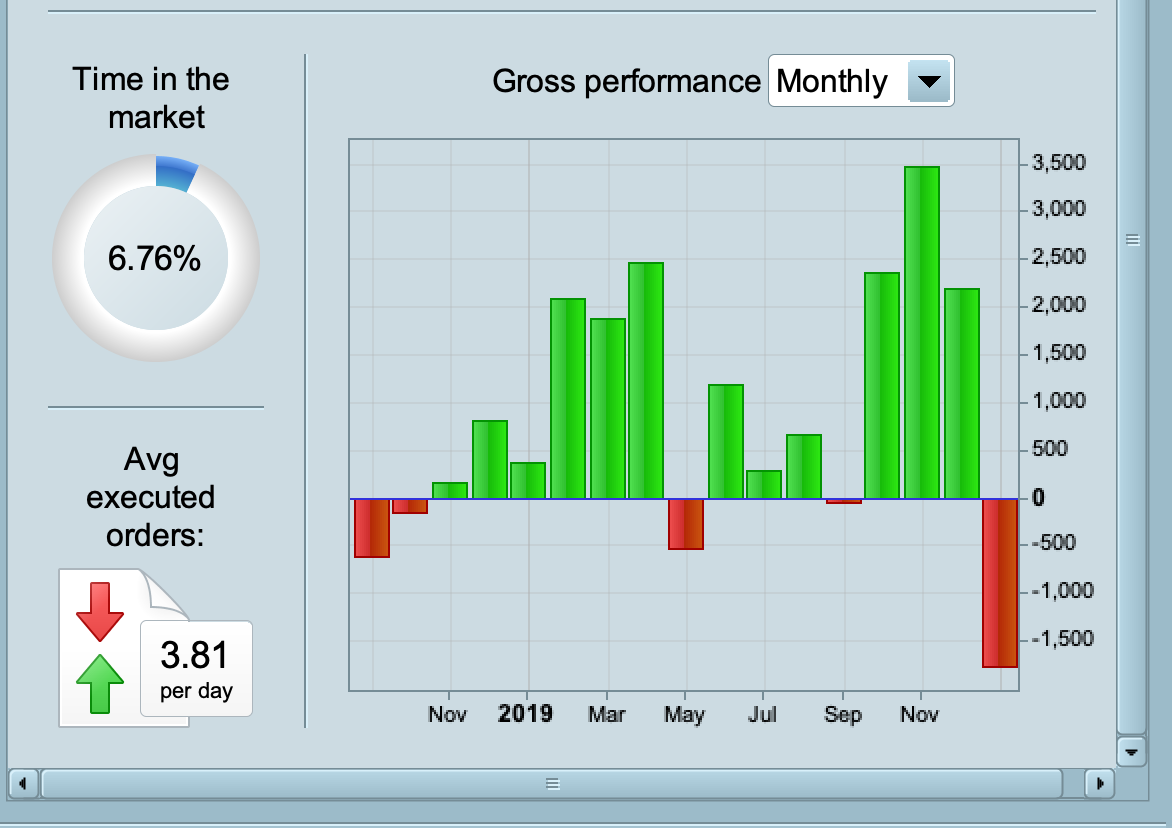

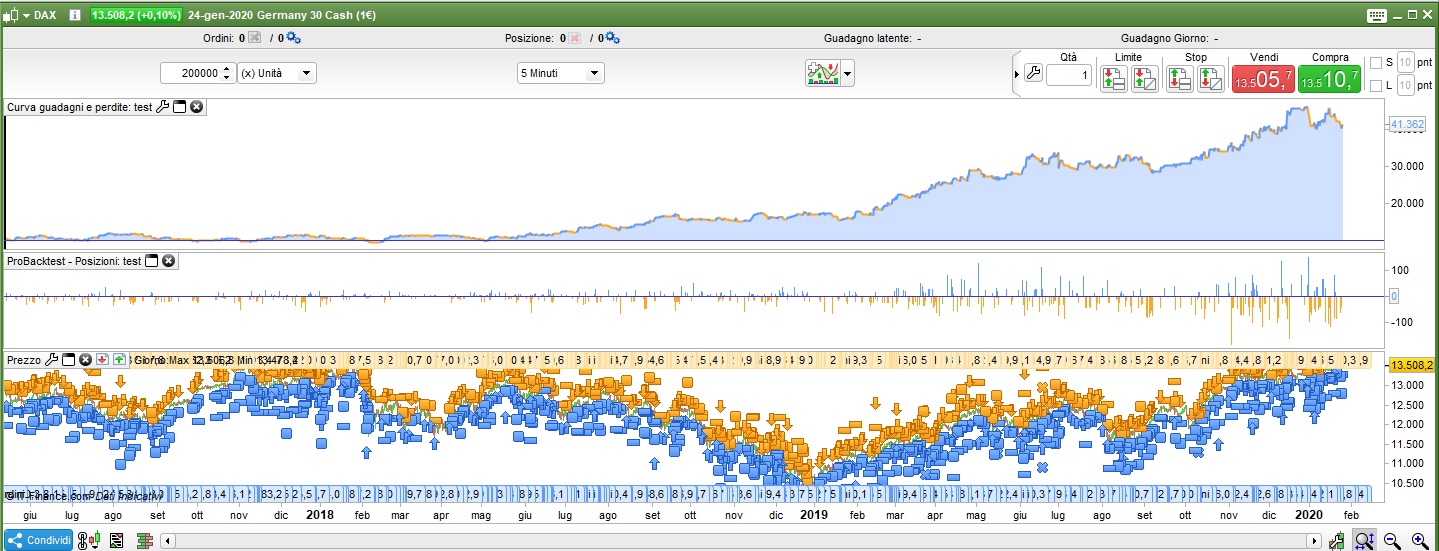

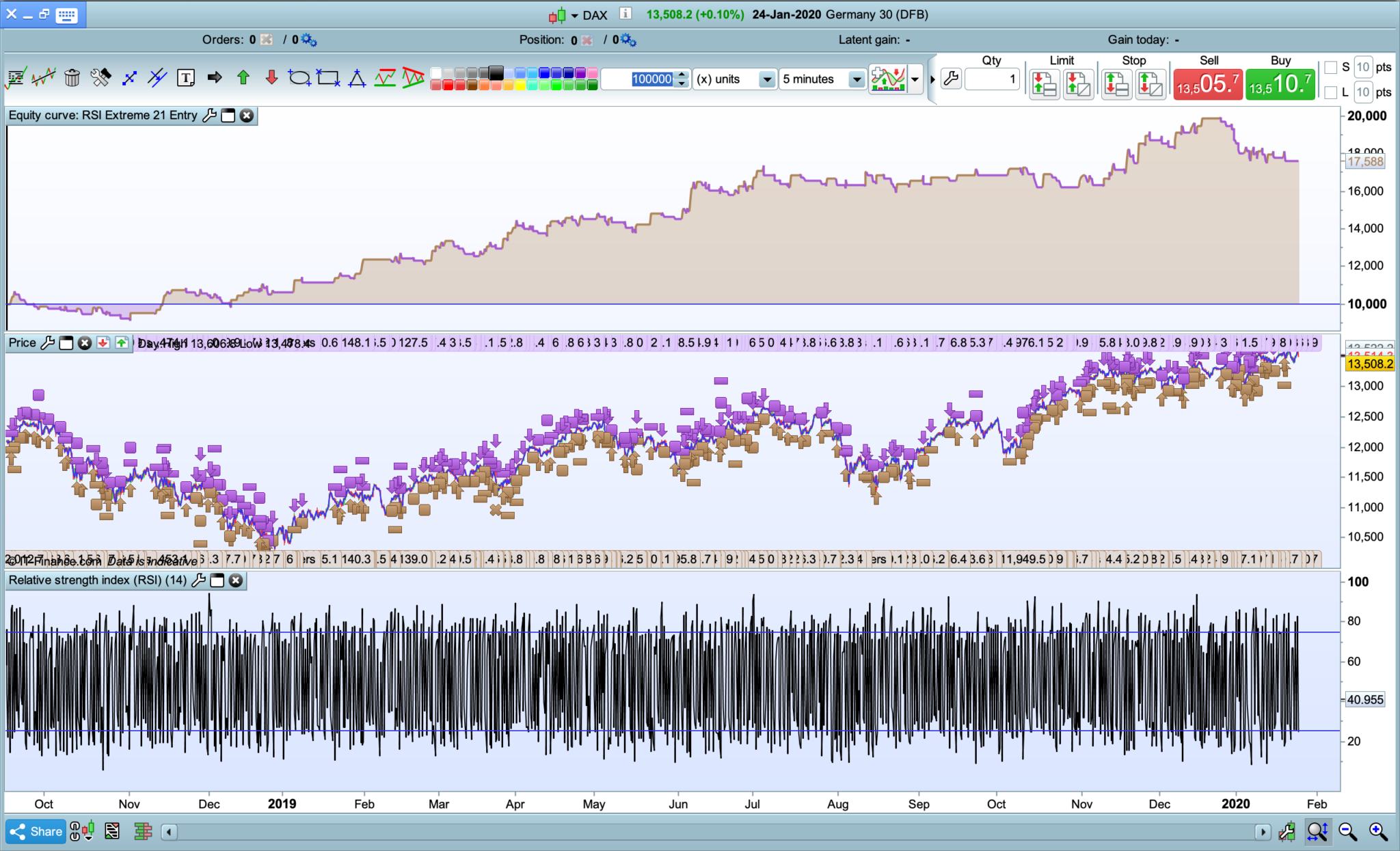

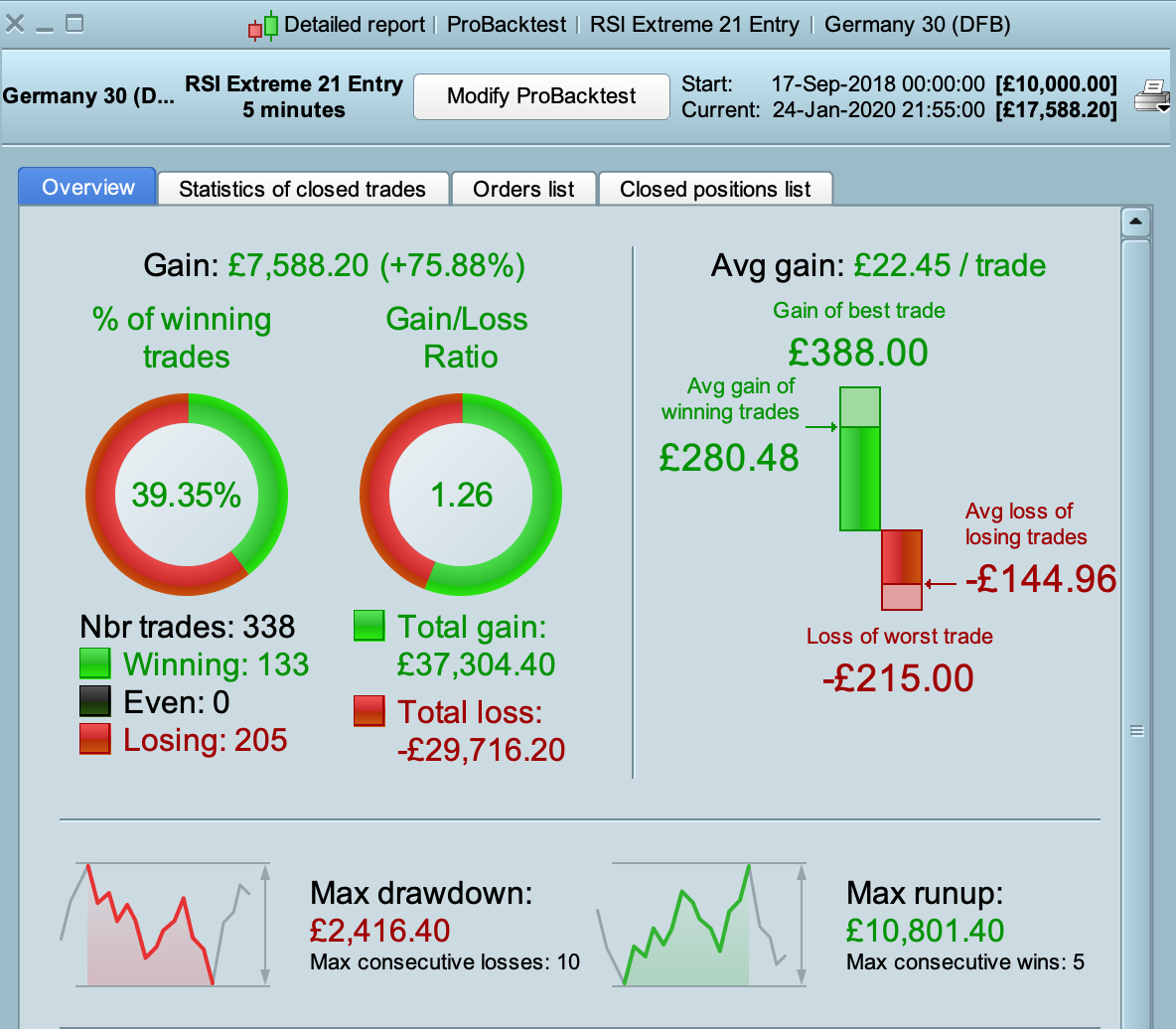

Code below and screenshots of results attached. Results use a risk of 1% with compounding.

Would really appreciate a critical review to determine if this is worth pursuing?

Many thanks

Chip

//Defining variables

ma21 = average [21] (close)

Shortentryprice = low - 2 //Entries taken when low of prior candle is surpassed

Longentryprice = high + 2 //Entries taken when high of prior candle is surpassed

myrsi = RSI [14] (close)

lowestrsi = lowest [20] (myrsi) //Sets to lowest RSI reading for past 20 candles

highestrsi = highest [20] (myrsi) //Sets to highest RSI reading for past 20 candles

Mylongsetup= 1 //This variable is used to determine if a long trade is entered; if set to 0 an entry will not occur

Myshortsetup = 1 //As for above for short setups

//Setting stops and targets

stoplongpoints = longentryprice - low

stopshortpoints = high - shortentryprice

targetlongpoints = stoplongpoints*2 //RR for long trades can be set here

targetshortpoints = stopshortpoints*2 //RR for short trades can be set here

//Detecting RSI extreme

If lowestRSI > 20 then //Cancels long entry by setting mylongsetup to 0 if lowest RSI reading for past 20 candles > 20. I.e. there has been no extreme

mylongsetup = 0

endif

If highestrsi < 80 then //As above but for an extreme of above 80 on RSI

myshortsetup = 0

endif

//Detecting close beyond 21

If close < ma21 then //Cancels long entry if close beyond 21 hasn't occured.

mylongsetup = 0

endif

If close < ma21 then //As above for short

mylongsetup = 0

endif

//Don't take at end of the week

If currentdayofweek = 5 AND currenttime = 215500 then

mylongsetup = 0

myshortsetup = 0

endif

// Money Management

Capital = 10000

Risk = 0.01

If mylongsetup = 1 then

stoploss = stoplongpoints

endif

If myshortsetup = 1 then

stoploss = stopshortpoints

endif

//Calculate contracts

equity = Capital + StrategyProfit

maxrisk = round(equity*Risk)

PositionSize = abs(round((maxrisk/StopLoss)/PointValue)*pipsize)

//Entry conditions

IF NOT LongOnMarket AND mylongsetup = 1 THEN

BUY positionsize lot AT longentryprice stop

set stop ploss stoplongpoints

set target pprofit targetlongpoints

endif

IF NOT shortOnMarket AND myshortsetup = 1 THEN

sellshort positionsize lot AT Shortentryprice stop

set stop ploss stopshortpoints

set target pprofit targetshortpoints

endif

200k backtest, take a look.

Hey looks good esp for a first attempt and doesn’t blow the Account on OOS Test (over the 1st 100k bars provided by Francesco).

Looks like it has a bias towards a rising market, but even so it holds up (no big losses) in that downtrend end June 19 to late Aug 19. Might just need re-optimising as / when the market turns down?

I’m going to try it on my Platform

Thank You for sharing

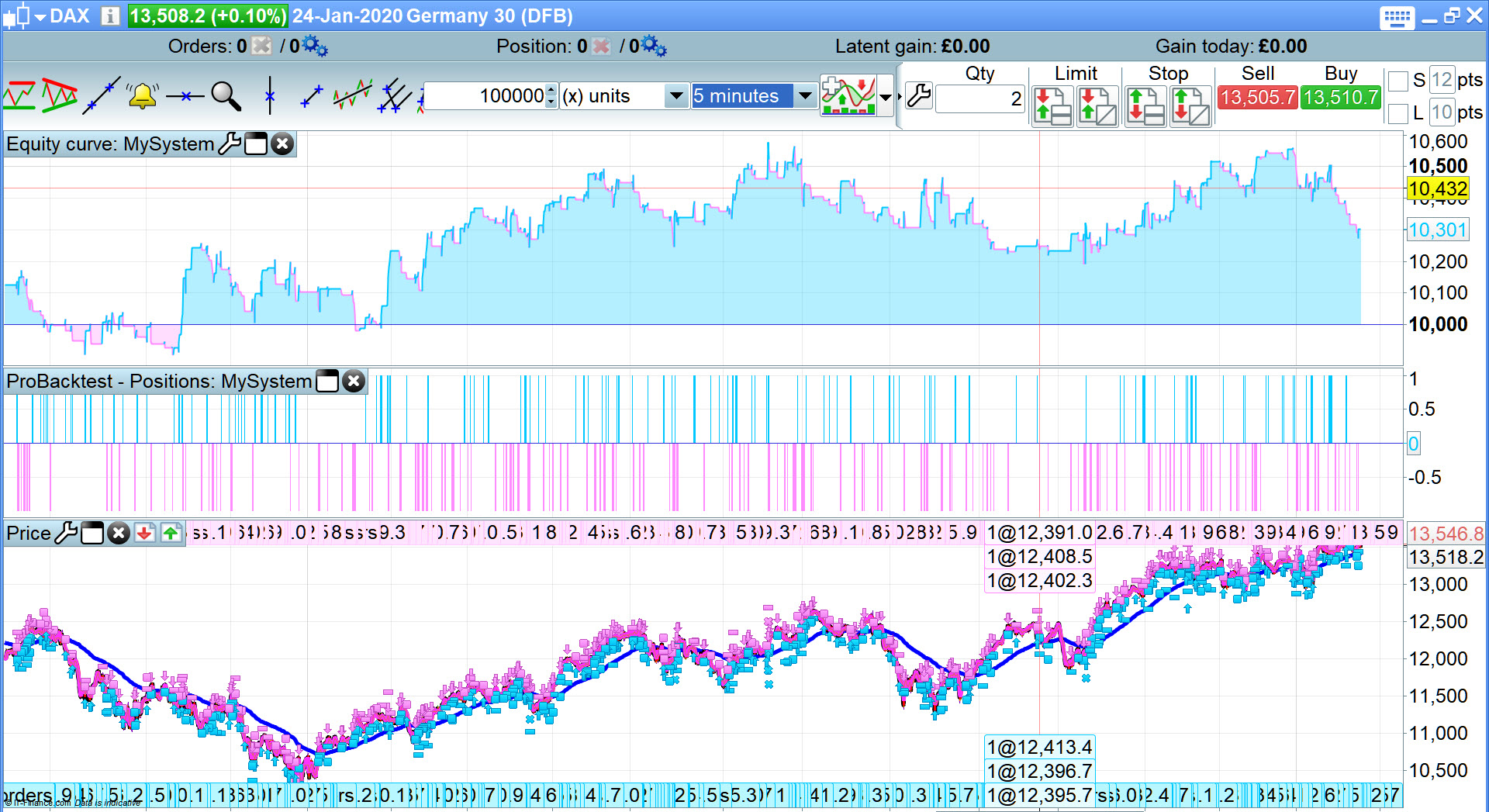

Mmm … attached is what I get Lot size = 1 … and I didn’t get same as you anyway even with Lot Size same as you had it?

I can’t think why my results are different than yours? I’ve only had 2 stubby bottles of beer! 🙂

It’s always best to get a System running as best you can with Lot Size = 1 as compounding can hides problems

Hi @DR Chips

My initial thought is that the numbers of contracts traded are scary and looking at IG.com if you had the stomach for 100+ contracts you system would not have the margin based on the starting capital

Based on my own RSI systems I would suggest trading the EU session only as the spreads are closer along with more volume

I am currently having a play with your code but I would suggest looking at the code here: https://www.prorealcode.com/prorealtime-trading-strategies/grinder-eurusd-5-min-intraday-trading-strategy/ it is similar to yours but adds in a trend filter and is a solid basis across multiple time frames and products

Systems are always worth pursuing as producing them is always a learning experience and any system should be run on a demo account so that you can have an indication as to how it will perform in real life as opposed to a back test and have a feel for it before risking any actual cash

//UK CodeFIN 1 candle delay

DEFPARAM FLATBEFORE = 080000

DEFPARAM FLATAFTER = 163000

//Defining variables

ma21 = average [21] (close)

Shortentryprice = low - 2 //Entries taken when low of prior candle is surpassed

Longentryprice = high + 2 //Entries taken when high of prior candle is surpassed

myrsi = RSI [14] (close)

lowestrsi = lowest [20] (myrsi) //Sets to lowest RSI reading for past 20 candles

highestrsi = highest [20] (myrsi) //Sets to highest RSI reading for past 20 candles

Mylongsetup= 1 //This variable is used to determine if a long trade is entered; if set to 0 an entry will not occur

Myshortsetup = 1 //As for above for short setups

//Setting stops and targets

stoplongpoints = 20

stopshortpoints = 10

targetlongpoints = 80

targetshortpoints = 20

//Detecting RSI extreme

If lowestRSI > 20 then //Cancels long entry by setting mylongsetup to 0 if lowest RSI reading for past 20 candles > 20. I.e. there has been no extreme

mylongsetup = 0

endif

If highestrsi < 80 then //As above but for an extreme of above 80 on RSI

myshortsetup = 0

endif

//Detecting close beyond 21

If close < ma21 then //Cancels long entry if close beyond 21 hasn't occured.

mylongsetup = 0

endif

If close [1] < ma21 then //As above for short

myshortsetup = 0

endif

//Don't take at end of the week

If currentdayofweek = 5 AND currenttime = 215500 then

mylongsetup = 0

myshortsetup = 0

endif

// Money Management

//Capital = 10000

//Risk = 0.01

//

//If mylongsetup = 1 then

//stoploss = stoplongpoints

//endif

//

//If myshortsetup = 1 then

//stoploss = stopshortpoints

//endif

//Calculate contracts

//equity = Capital + StrategyProfit

//maxrisk = round(equity*Risk)

//PositionSize = abs(round((maxrisk/StopLoss)/PointValue)*pipsize)

//Entry conditions

IF NOT LongOnMarket AND mylongsetup = 1 THEN

BUY 1 lot AT longentryprice stop

set stop ploss stoplongpoints

set target pprofit targetlongpoints

endif

IF NOT shortOnMarket AND myshortsetup = 1 THEN

sellshort 1 lot AT Shortentryprice stop

set stop ploss stopshortpoints

set target pprofit targetshortpoints

endif

Hi @Dr Chips

In your original code line 38 appears to have mylongsetup repeated rather than myshortsetup

The code above is a bit over optimised but it’s nearly midnight so please forgive me

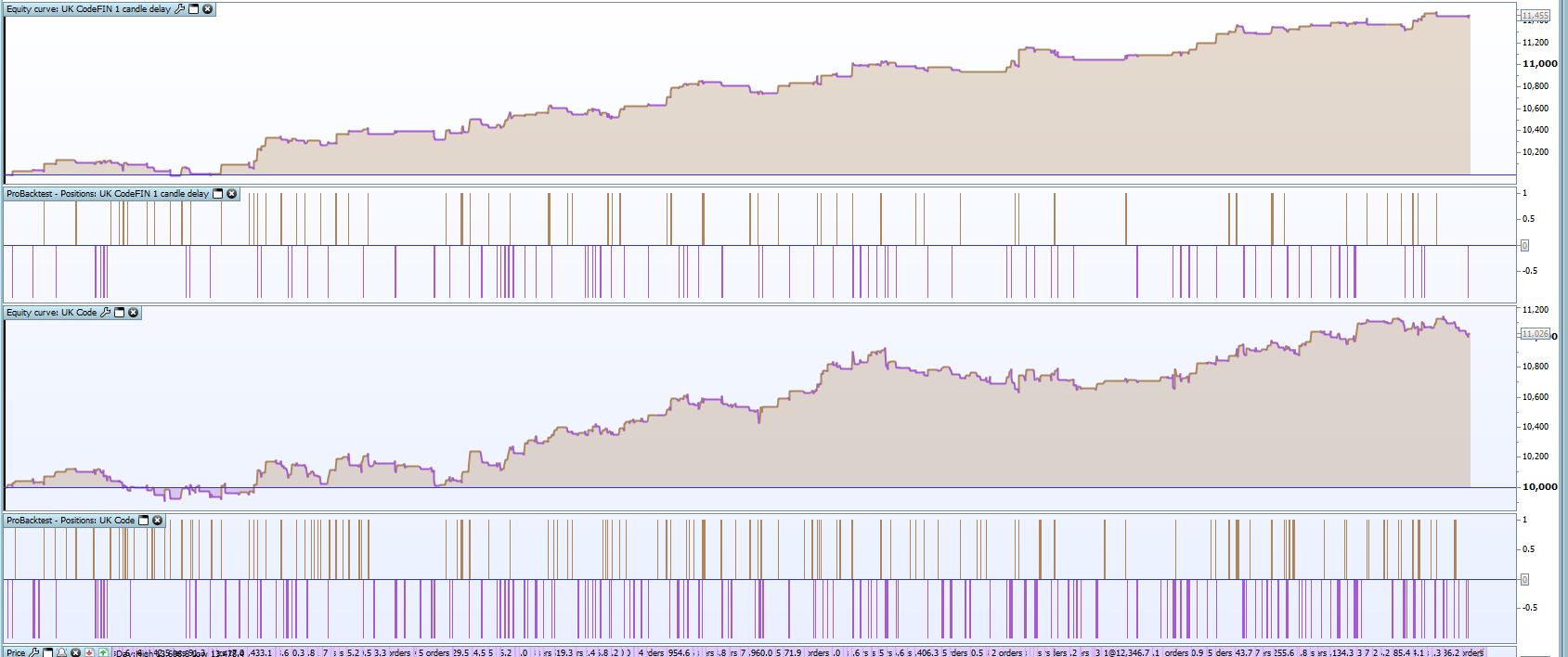

Looking at your results I have changed the system to only trade in the EU session (Lines 1+2) and worked on the stops and take profits (lines 18-21), the attachments compare the original code to the code inserted above

Besides the EU session change one thing I noticed but haven’t got into yet is the timings of the trades, if you look at the opening and closing times of the trades it appears that trade 1 will open and close either with profit or loss then the system waits 5-10 minutes and then trade 2 is placed and so on. This happens with codes that have a prevailing condition in this system the RSI property and can cause several consecutive losses

I also added a delay on line 40 of the above code to short positions

One of the things that I need to do is to put together a video of taking some code and working on it and fully testing it, if it is okay with you then I could do that for this code?

Morning all,

Really appreciate your comments and responses here.

Grahal – I wouldn’t know either why your results are different I’m afraid… as I said, I’m very much a newbie! So even without the beers I’m still struggling to get my head around things!!

Robo Futures Trader – thanks very much for your input on things. I’m going to take some time later to properly read through what you have done here (and do a fair amount of googling to explore further) but yes do please feel free to use as an example for a video – that would be really helpful, thank you!

Many thanks all

Chip

Just had a quick look re your point about the duplication on line 38 @Robo Futures Trade

Yup, this is an error! Have changed this and reposting my (now correct) original code and results below for reference.

//Defining variables

ma21 = average [21] (close)

Shortentryprice = low - 2 //Entries taken when low of prior candle is surpassed

Longentryprice = high + 2 //Entries taken when high of prior candle is surpassed

myrsi = RSI [14] (close)

lowestrsi = lowest [20] (myrsi) //Sets to lowest RSI reading for past 20 candles

highestrsi = highest [20] (myrsi) //Sets to highest RSI reading for past 20 candles

Mylongsetup= 1 //This variable is used to determine if a long trade is entered; if set to 0 an entry will not occur

Myshortsetup = 1 //As for above for short setups

//Setting stops and targets

stoplongpoints = longentryprice - low

stopshortpoints = high - shortentryprice

targetlongpoints = stoplongpoints*2 //RR for long trades can be set here

targetshortpoints = stopshortpoints*2 //RR for short trades can be set here

//Detecting RSI extreme

If lowestRSI > 20 then //Cancels long entry by setting mylongsetup to 0 if lowest RSI reading for past 20 candles > 20. I.e. there has been no extreme

mylongsetup = 0

endif

If highestrsi < 80 then //As above but for an extreme of above 80 on RSI

myshortsetup = 0

endif

//Detecting close beyond 21

If close < ma21 then //Cancels long entry if close beyond 21 hasn't occured.

mylongsetup = 0

endif

If close > ma21 then //As above for short

myshortsetup = 0

endif

//Don't take at end of the week

If currentdayofweek = 5 AND currenttime = 215500 then

mylongsetup = 0

myshortsetup = 0

endif

// Money Management

Capital = 10000

Risk = 0.01

If mylongsetup = 1 then

stoploss = stoplongpoints

endif

If myshortsetup = 1 then

stoploss = stopshortpoints

endif

//Calculate contracts

equity = Capital + StrategyProfit

maxrisk = round(equity*Risk)

PositionSize = abs(round((maxrisk/StopLoss)/PointValue)*pipsize)

//Entry conditions

IF NOT LongOnMarket AND mylongsetup = 1 THEN

BUY positionsize lot AT longentryprice stop

set stop ploss stoplongpoints

set target pprofit targetlongpoints

endif

IF NOT shortOnMarket AND myshortsetup = 1 THEN

sellshort positionsize lot AT Shortentryprice stop

set stop ploss stopshortpoints

set target pprofit targetshortpoints

endif

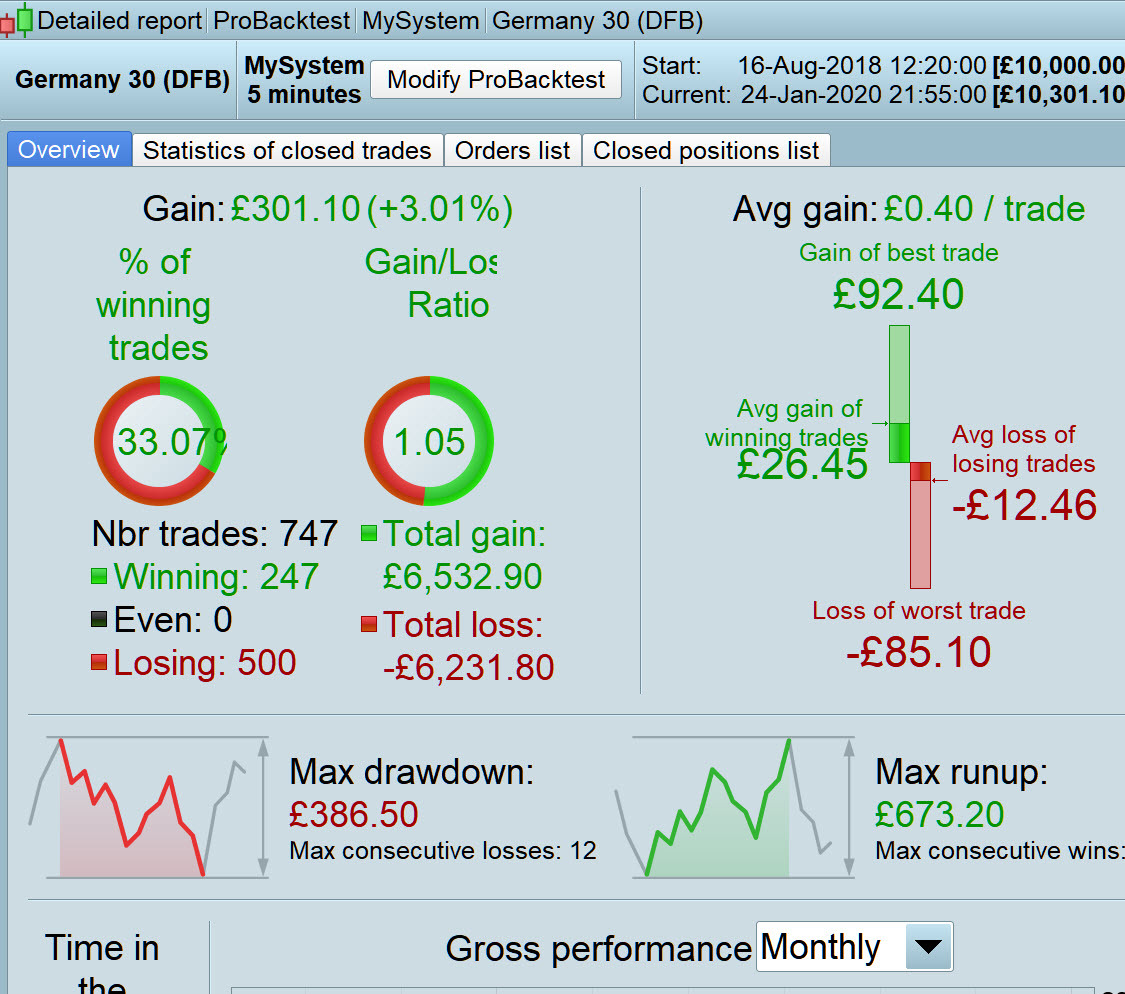

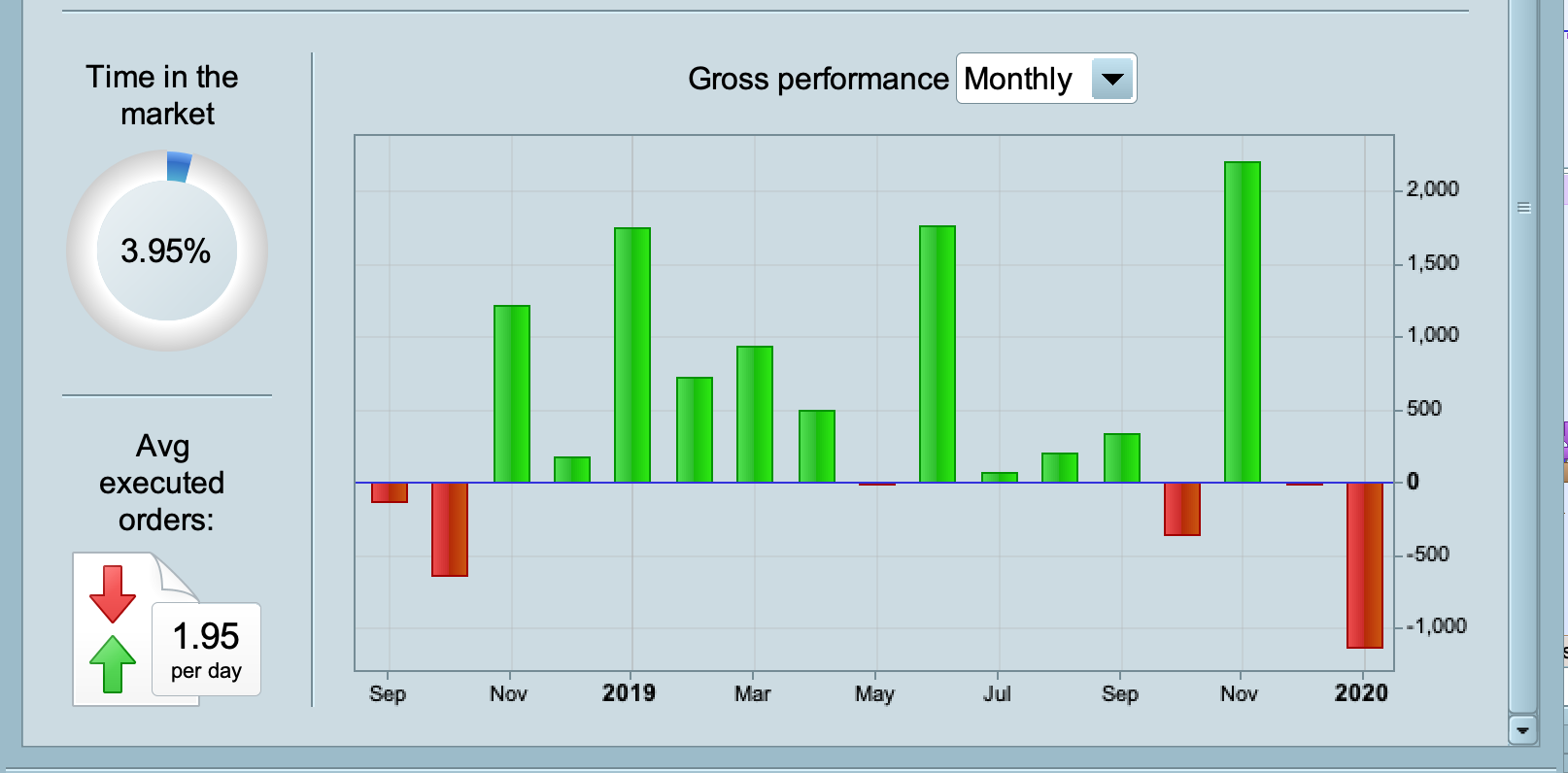

Why are you not showing Lot size under your equity curves?

Position size is needed else it is only half a story.

It be sooo much better if you delete the RSI Chart and add back in the positions Chart.

An average gain of £22.45 does not mean much unless we know how many open positions we need to lose sleep over!? 🙂

Yeah that’s it thank you.

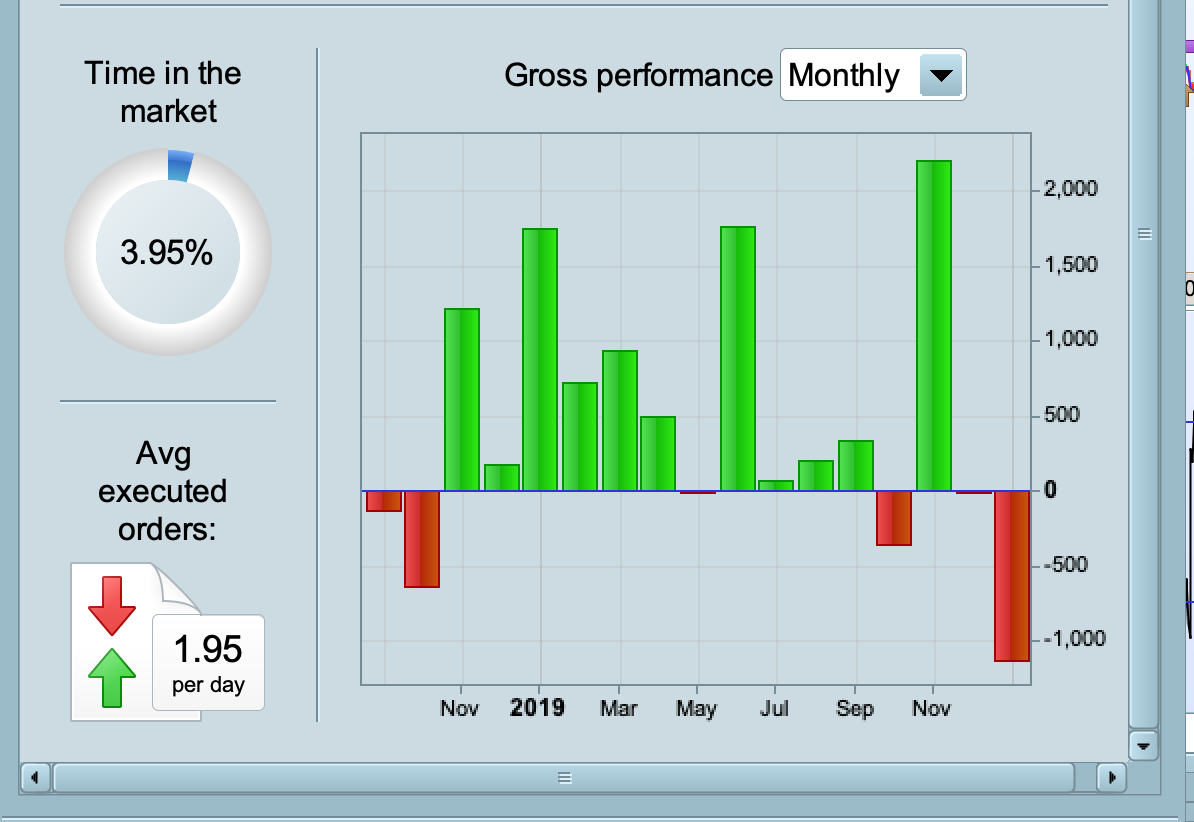

We can now see how much stress there would be to make £10K ish profit (£7.6k to date) over 18 months.

It seems like a simple strategy but in reality there are fourteen possible variables that can be optimised that cover the following areas:

- Time

- Periods for indicators

- Levels

- Order levels

- Stop loss and take profit distances

As it is on a five minute time frame that leaves us with a not very big data sample and a big possibility of curve fitting due to so many variables. I would try optimising each variable independently to see how quickly the strategy falls apart with different values for each of them and then when you spot which variables have the biggest effect then test combinations of them.

Thanks for the advice @vonasi

hello Dr Chips, hope you are in a good shape, how does the strategy work now? do you have any improvement for eur / usd use? cordially

hello Dr Chips, hope you are in a good shape, how does the strategy work now? do you have any improvement for eur / usd use? cordially

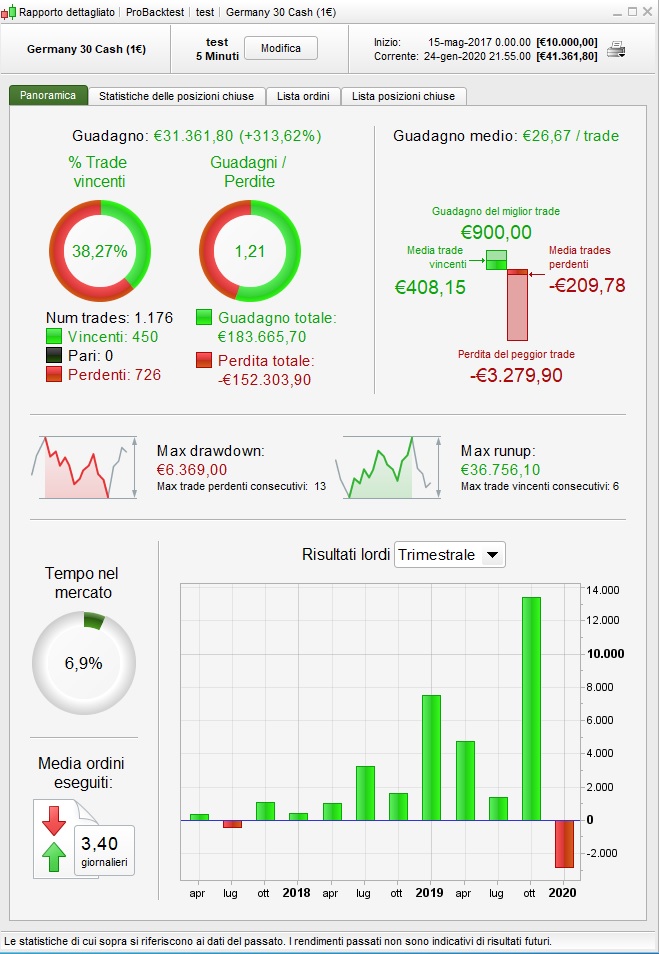

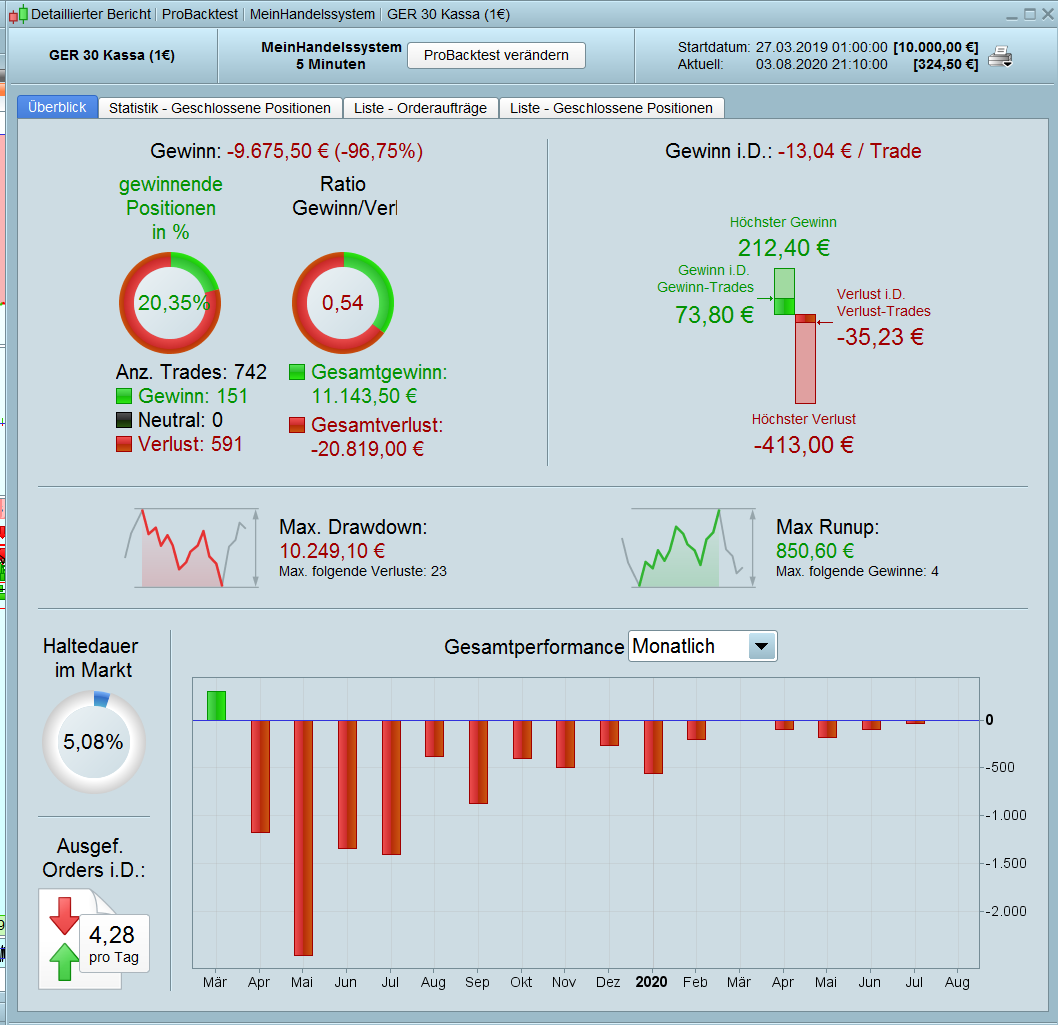

The code from the first postig doesn´t work on my desk. The result from my backtest.