Has made a simple code for DAX 30 which runs between 09:00 and 17:20.

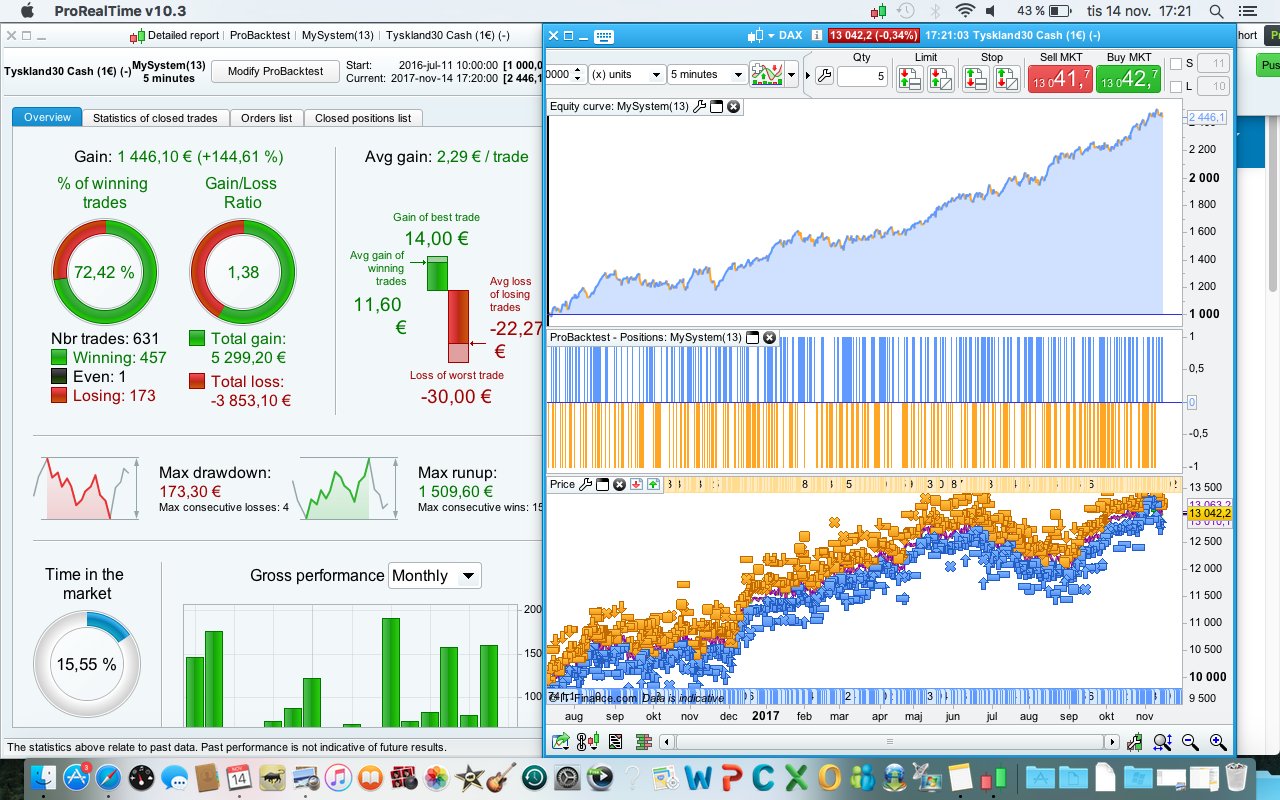

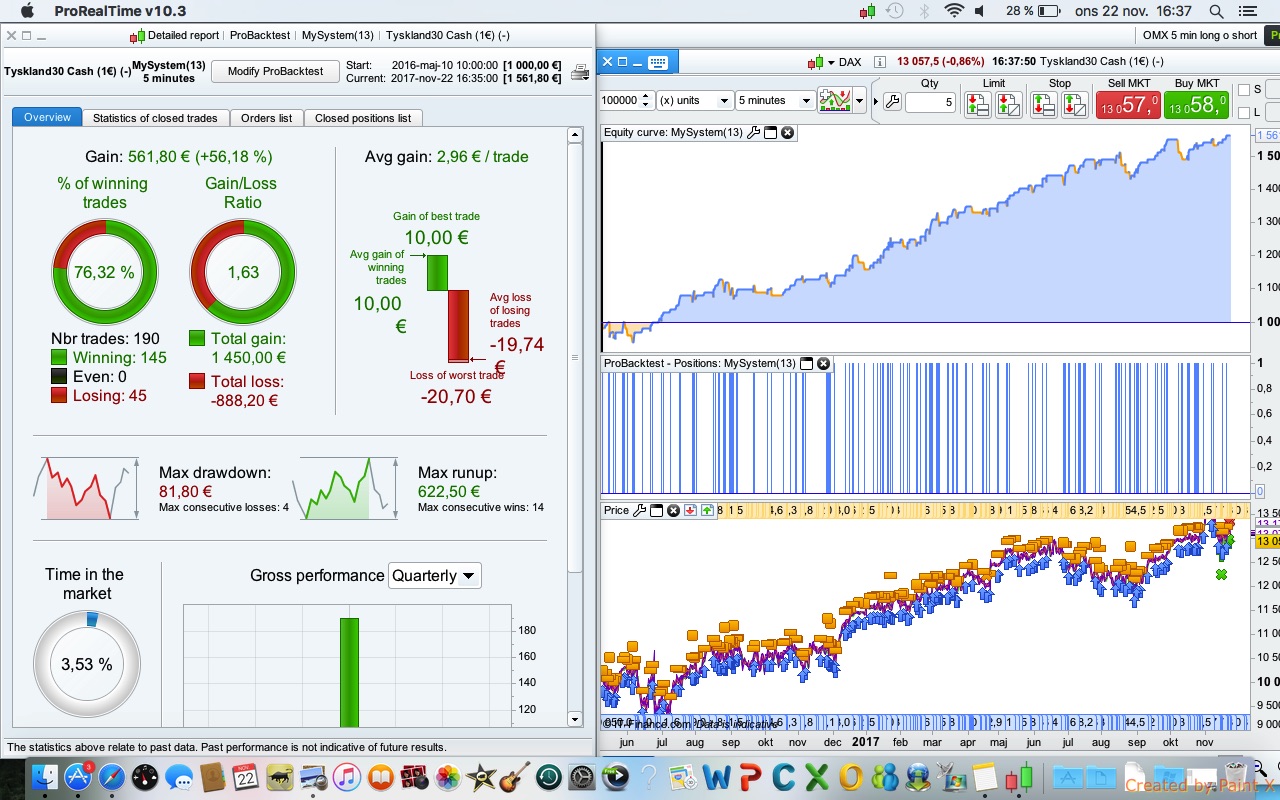

According to the 100k backtest, is looks ok..

It would be interesting to see a 200k backtest on it 🙂

Spread 1p.

DEFPARAM CumulateOrders = False

DEFPARAM FLATBEFORE = 090000

DEFPARAM FLATAFTER = 172000

// Conditions to enter long positions

indicator1 = BollingerDown[19](close)

c1 = (close <= indicator1)

indicator2 = Stochastic[15,3](close)

c2 = (indicator2 CROSSES UNDER 13)

IF c1 AND c2 THEN

BUY 1 CONTRACT AT MARKET

ENDIF

// Conditions to enter short positions

indicator10 = BollingerUp[21](close)

c10 = (close >= indicator10)

indicator20 = Stochastic[14,3](close)

c20 = (indicator20 CROSSES OVER 70)

IF c10 AND c20 THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

// Stops and targets

SLL = 27

TPL = 14

if longonmarket then

SET STOP pLOSS SLL

sET TARGET pPROFIT TPL

ENDIF

SLS = 30

TPS = 10

if SHORTonmarket then

SET STOP pLOSS SLS

sET TARGET pPROFIT TPS

ENDIF

Eric

EricParticipant

Master

Avg gain 2,29

not much room for slippage but on limit orders you could get positive slippage (det du förlorar på karusellen tar du kanske igen på gungorna?)

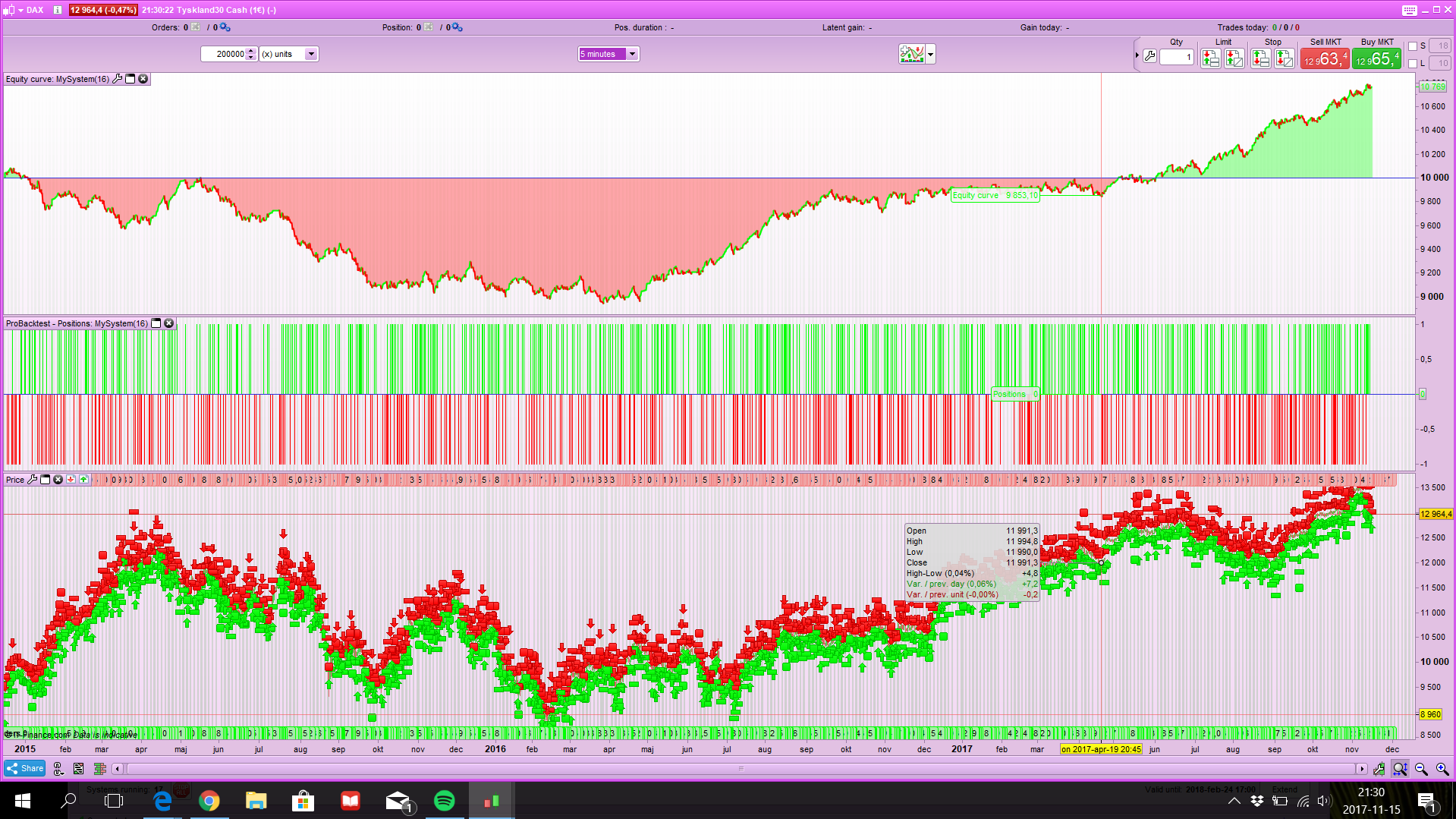

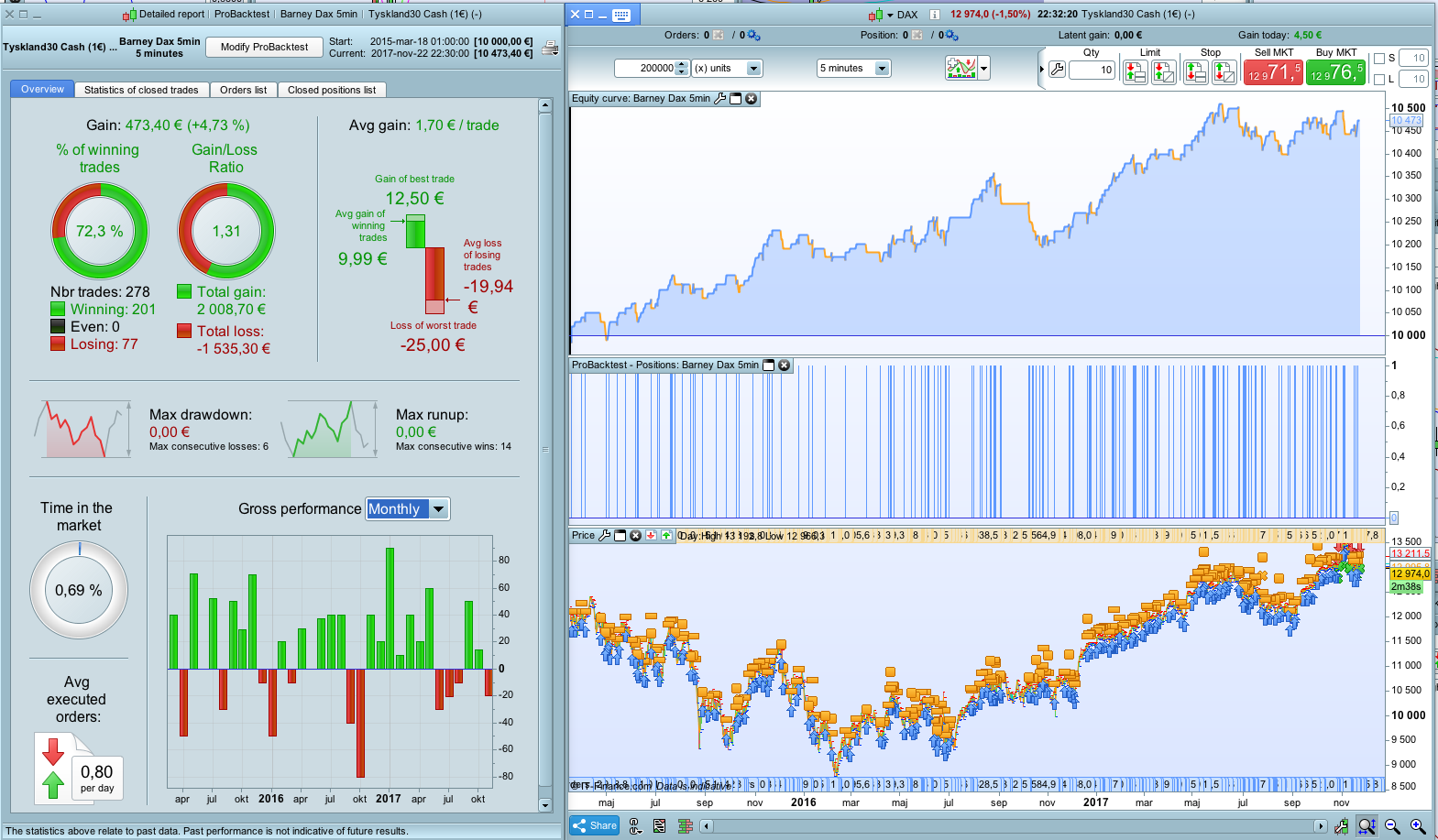

Hi Barney, here is the backtest with 200000 bars.

Sorry Barney, couldn’t resist 🙂

Leo

LeoParticipant

Veteran

Sorry Barney, couldn’t resist

Haha!!! It so early in the morning and it is awesome to read a joke in the forum! Hahah! XD

Doh 🙂 Been there done that Barney..

Thanks for the 200k backtest!

I do not feel completely satisfied with the result though.

Seems to be difficult to get simple codes to work, it feels like you need a 200 k test to see if algon is something to have or not(especially at 5 min algos).

If it was easy….. 😉

I know exactly how you feel. Before i got the 200K backtest premium for myself, i had several systems that looked so good in 100K, when in 200K tho…

Even made a post about it: https://www.prorealcode.com/topic/creating-strategies-questions-about-backtest-and-periods/

In short, it just does not feel sexy when its HORRIBLE before 2016, but SEXY after 😀

I guess that if you curve-fit something there might be a chance that the same curve might work tomorrow.. I mean you can be pretty sure that it will STOP working i guess… and thats why i dont want to run stuff that only looks good on 100K… Even though i have for example the linked system going in demo, making money, i just know that its going to stop working maybe tomorrow, or maybe in a week or maybe in a month. I’d rather have a more robust system than that…

Ps: i do not have alot of experience with live automated systems trading 🙂

All periods and stoploss / takeprofit values have been optimized, that’s why it is curvefitted. You can do optimisation of course, but do WFA to prove robustness of it! The past 100k bars before your own test are pure Out Of Sample data that could validate or not your strategy, but it doesnt.

You have 2 ways to make things better:

- develop your idea on at least 1 In Sample period (70% of data) and test in the next 30%

- if you are in a optimisation process, do a simple WFA with one or many IS/OOS iterations to find the good edge

Come one Barney, I know you can make it!

https://www.prorealcode.com/blog/learning/prorealtime-walk-analysis-tool/

This was one of the reasons i came to this forum!

Big thanks to nicolas for the good work 🙂

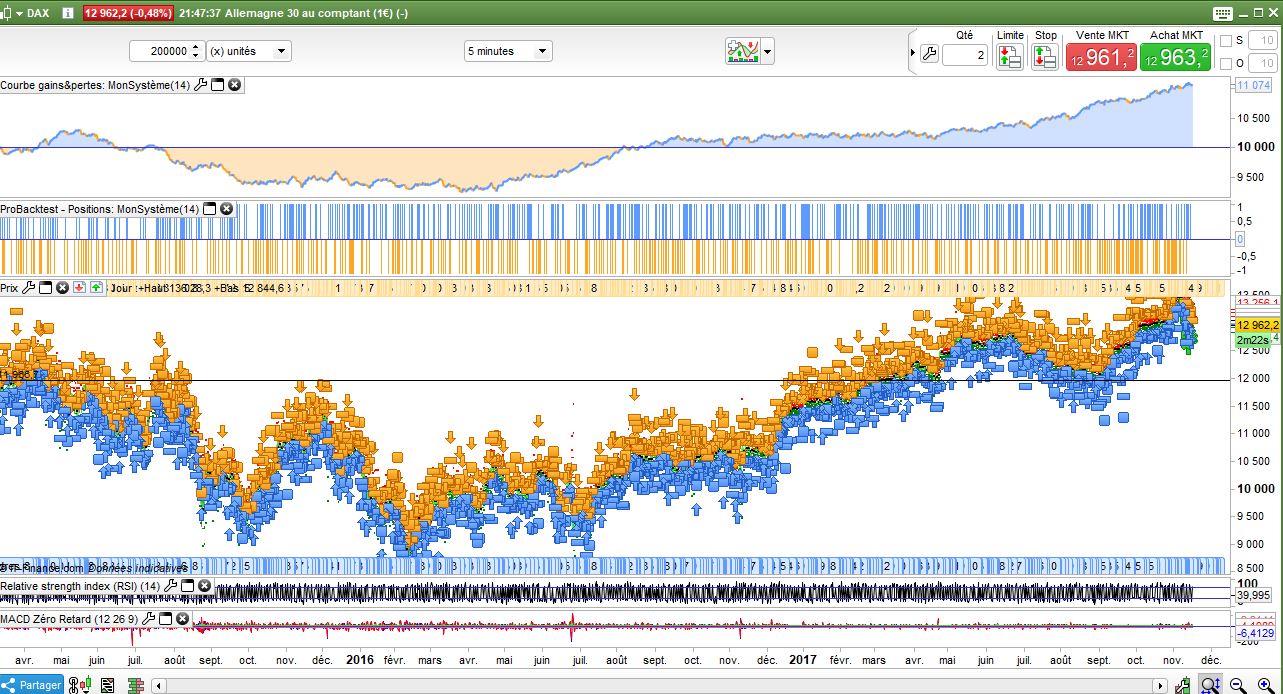

Ok, here coms a code that is not over optimized. Simple code again thugh!

DAX 5 min spread 1.

DEFPARAM CumulateOrders=False

defparam flatbefore = 090000

defparam flatafter = 173000

indicator1 = ExponentialAverage[46](close)

indicator2 = ExponentialAverage[10](close)

c1 = (indicator1 > indicator2[1])

indicator3 = AroonUp[20]

indicator4 = Aroondown[76]

c2 = (indicator3 CROSSES OVER indicator4)

indicator100 = close

indicator101 = Supertrend[7,1]

c100 = indicator100 > indicator101

IF c1 and c2 and c100 THEN

BUY 1 CONTRACTs AT MARKET

ENDIF

set stop ploss 20

set target pprofit 10

Would be nice if someone would try 200k on it 🙂

Here you go. Not bad IMO.

Thanks Despair for the 200k test.

Will probably start it live 🙂