Hi forum-members! Im have a tricky question for you all.

when creating a new strategy, how long back do you want it to be profitable?

I now have the 200K bar backtest, going back to 2010. Does it need to be profitable all the way or is it OK if its been profitable “only” in the last couple of years?

Any thoughts on this?

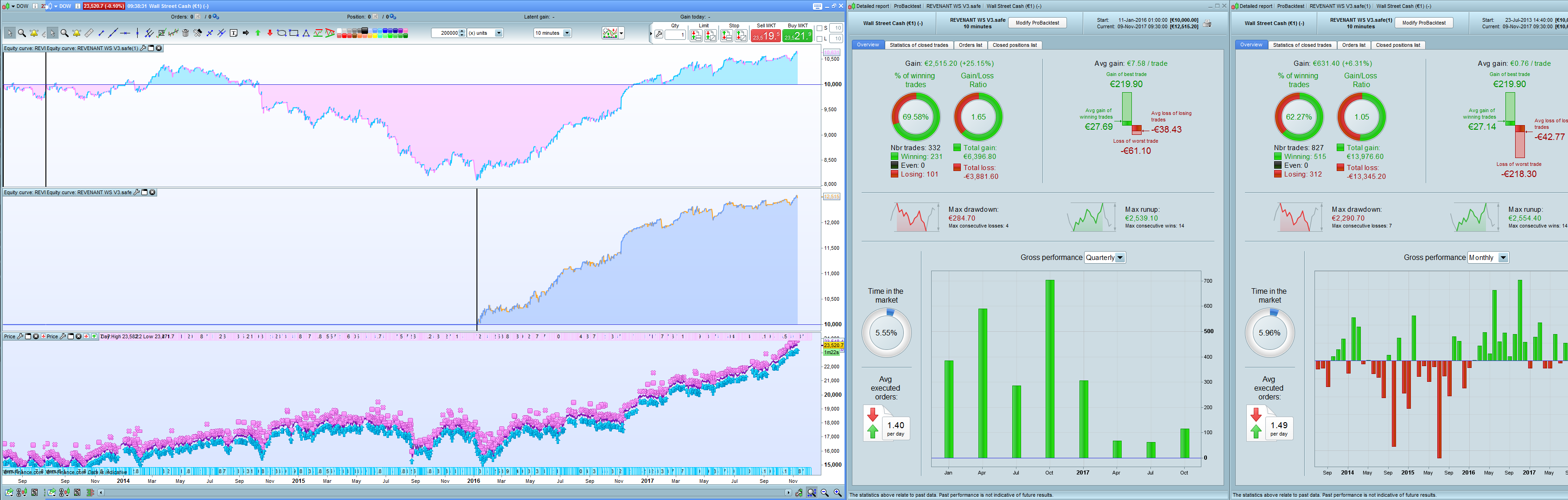

For example i have created this strategy (see photo) and it looks AMAZING from 2016 -> todays date, but if you go further back its not that profitable.

(With this example the biggest drawdowns happens when market continues down long trends.

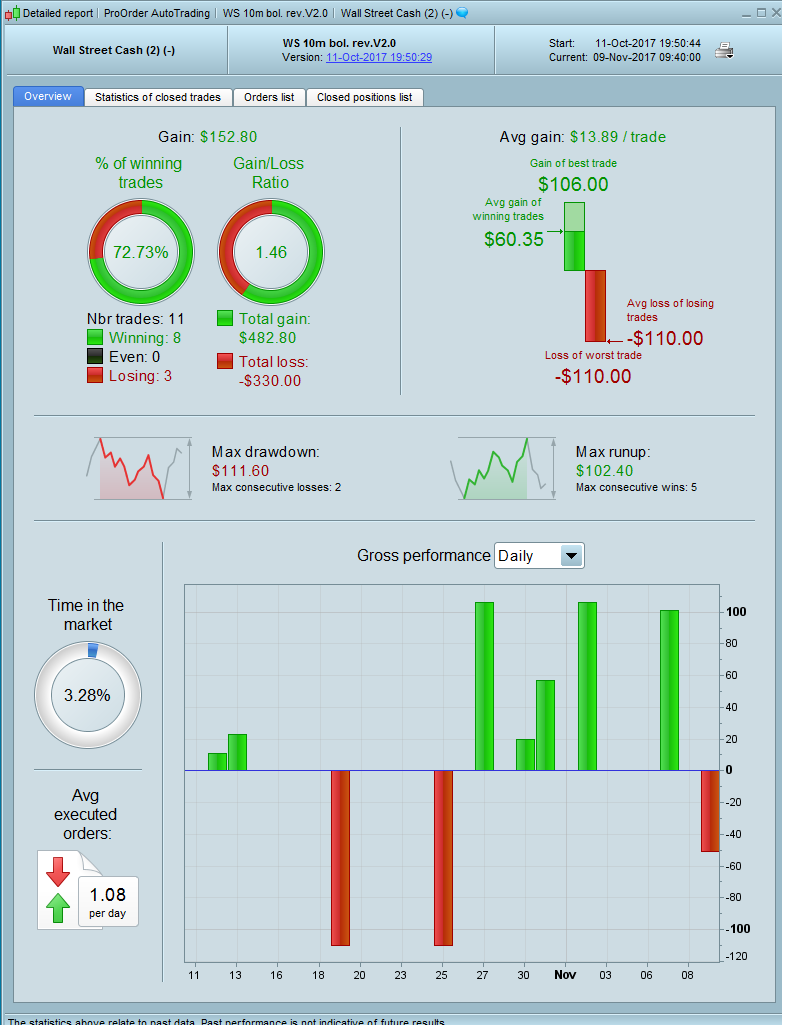

Edit: When i created this i only had the 100K backtest, and that goes back to May 2016, and the strategy has been very profitable since January 2016 -> today. it was about 1 month ago and in demo the strategy has basicly the same results as backtest: 70% winrate and above 1.4 in gains. I’ve added a photo of the demo-version.

edit2: wall st (dow) 10m mean reversion strategy

Hello jebus89,

The more convinced you are that you have found a good method for forecasting the market, the less data you will need to convince yourself 🙂

On the other hand there is a purely statistical approach. Testing results of many different (random) signal and price combinations. Here more data is generally better to gain confidence. A suggestion is to restrict the timeframe to the year when computerized trading was introduced for the specific market.

I guess somebody else can better explain how to utilize the available data best, which can also help to reduce the amount needed.

I would always recommend using as much data as possible. But finally it also depends on how often your strategy trades and how many optimizable variables you have. You should have at least 30 better 50 trades per variable you use. Having 10 trades and 10 variables is a recipe for disaster.

You posted this backtest before. Did you now run a WFA of the strategy? As I pointed out before, periodic reoptimization might improve the result for the early years.

@Derek: I wish there was a firm rule 😀 I think its really hard to stay confident in any market haha.

@Despair: Yes indeed, i do not have the photo right now, but long story short: Optimizing the variables was a little bit better, but hardly enough to be sexy enough to run… there was some profit here and there, but no 45 degree EQ curve to say the least… Edit: I agree with “more data = better”! no doubt about that! Big thanks for the reply tho!

From 2016 they seem really profitable and good, and still to this day in demo they keep winning. But after seeing for example Reiner’s first algo here, and how curve-fitted that was, I feel like im never gonna be confident unless i see profitable and positive backtest from first data available!

Is this a mistake from my part? is it possible to create systems that work the last 50% of your in sample data, or should it be 90-100% or nothing?

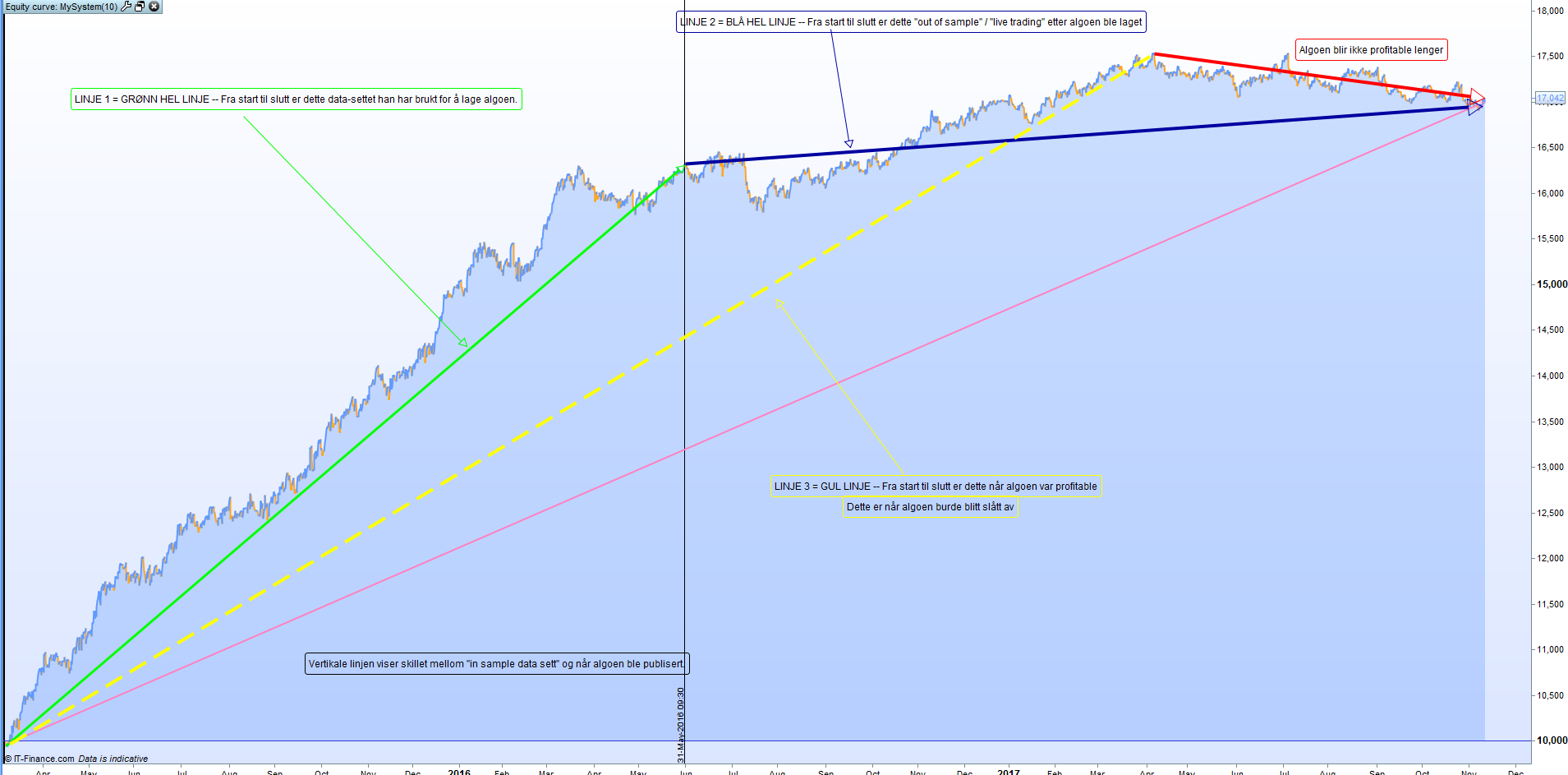

Im just gonna throw in the picture of Reiners first algo. Please note that the text in the photo is in norwegian, but its just to explain “curve-fitting” for a friend of mine!

Horisontal line (date: 31. may 2016) is aprox the date he released it to this forum. meaning everything to the left of this line = IN SAMPLE, and everything to the right of this line = OUT OF SAMPLE.

Also from “Better system trader” podcast today, i heard that you have to expect avg gain to go down after going live with a system, this is clearly shown in the Reiner-example in picture.. And then the system stops working all together and you have to stop it. In the Reiner-example (picture) the system lasted about 1 year until it was no longer profitable.

edit: link to the reiner-code: https://www.prorealcode.com/prorealtime-trading-strategies/trend-surfer-dax/

In the end it’s always up to the trader to set one’s own level of confidence before putting money on the line. Of course you can also paper trade.

By the way: The less variation the backtest results show, the more likely is your system overoptimized.

I think you should rely on WFA. If you get a WFA that produces good results in most periods put it on demo. If it works there for some time, go live with real money.

And yes, usually performance declines OOS from insample. You should expect that. If you have OOS 50% of the profit that you had insample, this is good. Eventually it then stops working at all. Then hopefully re optimization of the parameters can get it back on track.

In the end it’s always up to the trader to set one’s own level of confidence before putting money on the line.

This is in my opinion, one of the best and clever answer about the universal question “is it worth being traded with real money?”.

Leo

LeoParticipant

Veteran

I have your question many time in mind.

When the market have a very good defined trend it seems like most of the strategy works, the problem is when the markets gets choppy. That’s a headache!

I think if you find a way that your strategy minimise losses or no trade at all before 2016, you get the jackpot!

Thanks for taking the time to read my post and reply. Good insight here 🙂