Bonsoir,

pour information, est-ce que vous pourriez convertir un code écrit en JAVA (chez mon autre courtier Dukascopy) pour l’adapter au format PRT?

Si oui, je mettrai le code dans l’endroit approprié.

Bonne soirée.

Merci de poster des images avant d’ajouter le code et de bien vérifier que ce code source n’est pas soumis à copyright.

Voici une image de l’indicateur : il ressemble (me semble-t-il) au SAR.

et le code.

Je n’ai pas vu de copyright.

Merci.

package com.dukascopy.indicators;

import com.dukascopy.api.DefaultColors;

import com.dukascopy.api.indicators.DoubleRangeDescription;

import com.dukascopy.api.indicators.IIndicator;

import com.dukascopy.api.indicators.IIndicatorContext;

import com.dukascopy.api.indicators.IndicatorInfo;

import com.dukascopy.api.indicators.IndicatorResult;

import com.dukascopy.api.indicators.InputParameterInfo;

import com.dukascopy.api.indicators.IntegerRangeDescription;

import com.dukascopy.api.indicators.OptInputParameterInfo;

import com.dukascopy.api.indicators.OutputParameterInfo;

public class TrendEnvelopesIndicator1 implements IIndicator {

private IIndicator lwma;

private int timePeriod = 14;

private double deviation = 0.1;

private IndicatorInfo indicatorInfo;

private InputParameterInfo[] inputParameterInfos;

private OutputParameterInfo[] outputParameterInfos;

private OptInputParameterInfo[] optInputParameterInfos;

private final double[][][] inputs = new double[1][][];

private final double[][] outputs = new double[2][];

public void onStart(IIndicatorContext context) {

lwma = context.getIndicatorsProvider().getIndicator("LWMA");

indicatorInfo = new IndicatorInfo("TrendEnvelopes", "Trend Envelope", "Overlap Studies", true, false, true, 1, 2, 2);

inputParameterInfos = new InputParameterInfo[] {

new InputParameterInfo("Price", InputParameterInfo.Type.PRICE)

};

optInputParameterInfos = new OptInputParameterInfo[] {

new OptInputParameterInfo("Time Period", OptInputParameterInfo.Type.OTHER, new IntegerRangeDescription(timePeriod, 2, 500, 1)),

new OptInputParameterInfo("Deviation", OptInputParameterInfo.Type.OTHER, new DoubleRangeDescription(deviation, 0.01, 100, 0.01, 2))

};

outputParameterInfos = new OutputParameterInfo[] {

new OutputParameterInfo("Low Band", OutputParameterInfo.Type.DOUBLE, OutputParameterInfo.DrawingStyle.LINE),

new OutputParameterInfo("High Band", OutputParameterInfo.Type.DOUBLE, OutputParameterInfo.DrawingStyle.LINE)

};

outputParameterInfos[0].setColor(DefaultColors.ROYAL_BLUE);

outputParameterInfos[0].setGapAtNaN(true);

outputParameterInfos[1].setColor(DefaultColors.RED);

outputParameterInfos[1].setGapAtNaN(true);

}

public IndicatorResult calculate(int startIndex, int endIndex) {

if (startIndex - getLookback() < 0) {

startIndex = getLookback();

}

if (startIndex > endIndex) {

return new IndicatorResult(0, 0);

}

double[] dsma = new double[endIndex - startIndex + 1];

lwma.setInputParameter(0, inputs[0][1]);

lwma.setOptInputParameter(0, timePeriod);

lwma.setOutputParameter(0, dsma);

lwma.calculate(startIndex - 1, endIndex - 1);

double[] valuesLow = new double[endIndex - startIndex + 1];

double[] valuesHigh = new double[endIndex - startIndex + 1];

int trend = 0;

for (int i = startIndex, j = 0; i <= endIndex; i++, j++) {

//Inputs: 0 open, 1 close, 2 high, 3 low, 4 volume

valuesLow[j] = (1 - deviation / 100) * dsma[j];

valuesHigh[j] = (1 + deviation / 100) * dsma[j];

if (inputs[0][1][i] > valuesHigh[j]) {

trend = 1;

} else if (inputs[0][1][i] < valuesLow[j]) {

trend = -1;

}

if (trend > 0) {

outputs[1][j] = Double.NaN;

if (j > 0 && valuesLow[j] < valuesLow[j - 1]) {

valuesLow[j] = valuesLow[j - 1];

}

outputs[0][j] = valuesLow[j];

} else {

outputs[0][j] = Double.NaN;

if (j > 0 && valuesHigh[j] > valuesHigh[j - 1]) {

valuesHigh[j] = valuesHigh[j - 1];

}

outputs[1][j] = valuesHigh[j];

}

}

return new IndicatorResult(startIndex, endIndex - startIndex + 1);

}

public IndicatorInfo getIndicatorInfo() {

return indicatorInfo;

}

public InputParameterInfo getInputParameterInfo(int index) {

if (index < inputParameterInfos.length) {

return inputParameterInfos[index];

}

return null;

}

public OptInputParameterInfo getOptInputParameterInfo(int index) {

if (index < optInputParameterInfos.length) {

return optInputParameterInfos[index];

}

return null;

}

public OutputParameterInfo getOutputParameterInfo(int index) {

if (index < outputParameterInfos.length) {

return outputParameterInfos[index];

}

return null;

}

public void setInputParameter(int index, Object array) {

inputs[index] = (double[][]) array;

}

public void setOutputParameter(int index, Object array) {

switch (index) {

case 0:

outputs[index] = (double[]) array;

break;

case 1:

outputs[index] = (double[]) array;

break;

default:

throw new ArrayIndexOutOfBoundsException(index);

}

}

public void setOptInputParameter(int index, Object value) {

switch (index) {

case 0:

timePeriod = (Integer) value;

lwma.setOptInputParameter(0, timePeriod);

break;

case 1:

deviation = (Double) value;

break;

default:

throw new ArrayIndexOutOfBoundsException(index);

}

}

public int getLookback() {

return lwma.getLookback() + 1;

}

public int getLookforward() {

return 0;

}

}

Le code ci-dessous doit être correct, merci de confirmer.

Il s’agit en fait d’un breakout des bandes Enveloppes qui permet le passage de la tendance haussière à baissière et vice-versa.

timePeriod=14

Deviation=0.01

price=customclose

dsma = WeightedAverage[timePeriod](price)

valuesLow = (1 - deviation / 100) * dsma

valuesHigh = (1 + deviation / 100) * dsma

inputs=price

if (inputs > valuesHigh) then

trend = 1

elsif (inputs < valuesLow) then

trend = -1

endif

if (trend > 0) then

alpha1=0

if ( valuesLow < valuesLow[1]) then

valuesLow = valuesLow[1]

endif

if trend[1]>0 then

outputs0 = valuesLow

outputs1 = valueshigh

alpha0 = 255

else

drawtext("●",barindex,valueslow,dialog,bold,22) coloured(65,105,225)

endif

else

alpha0=0

if (valuesHigh > valuesHigh[1]) then

valuesHigh = valuesHigh[1]

endif

if trend[1]<0 then

outputs1 = valuesHigh

outputs0 = valueslow

alpha1 = 255

else

drawtext("●",barindex,valueshigh,dialog,bold,22) coloured(255,0,0)

endif

endif

return outputs0 coloured(65,105,225,alpha0) style(line,4), outputs1 coloured(255,0,0,alpha1) style(line,4)

Bonsoir,

c’est impeccable. Merci et bonne soirée. Par curiosité, cet indicateur se rapproche t il d’un indicateur existant pour PRT ?

Il s’agit d’un principe assez répandu de HiLo switch, si le prix tombe en dessous d’une bande alors on switch sur l’autre et vice-versa. Une autre version répandue avec les bandes de Bollinger : BBands stop

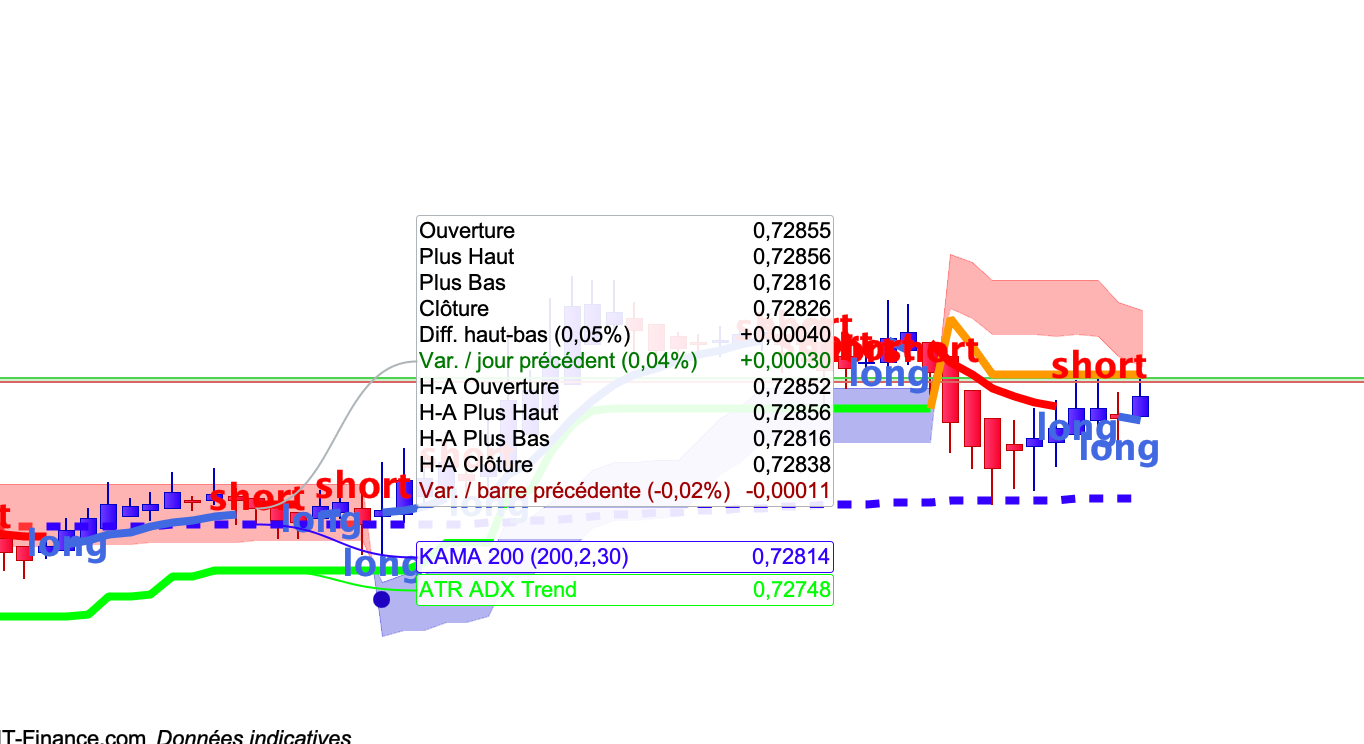

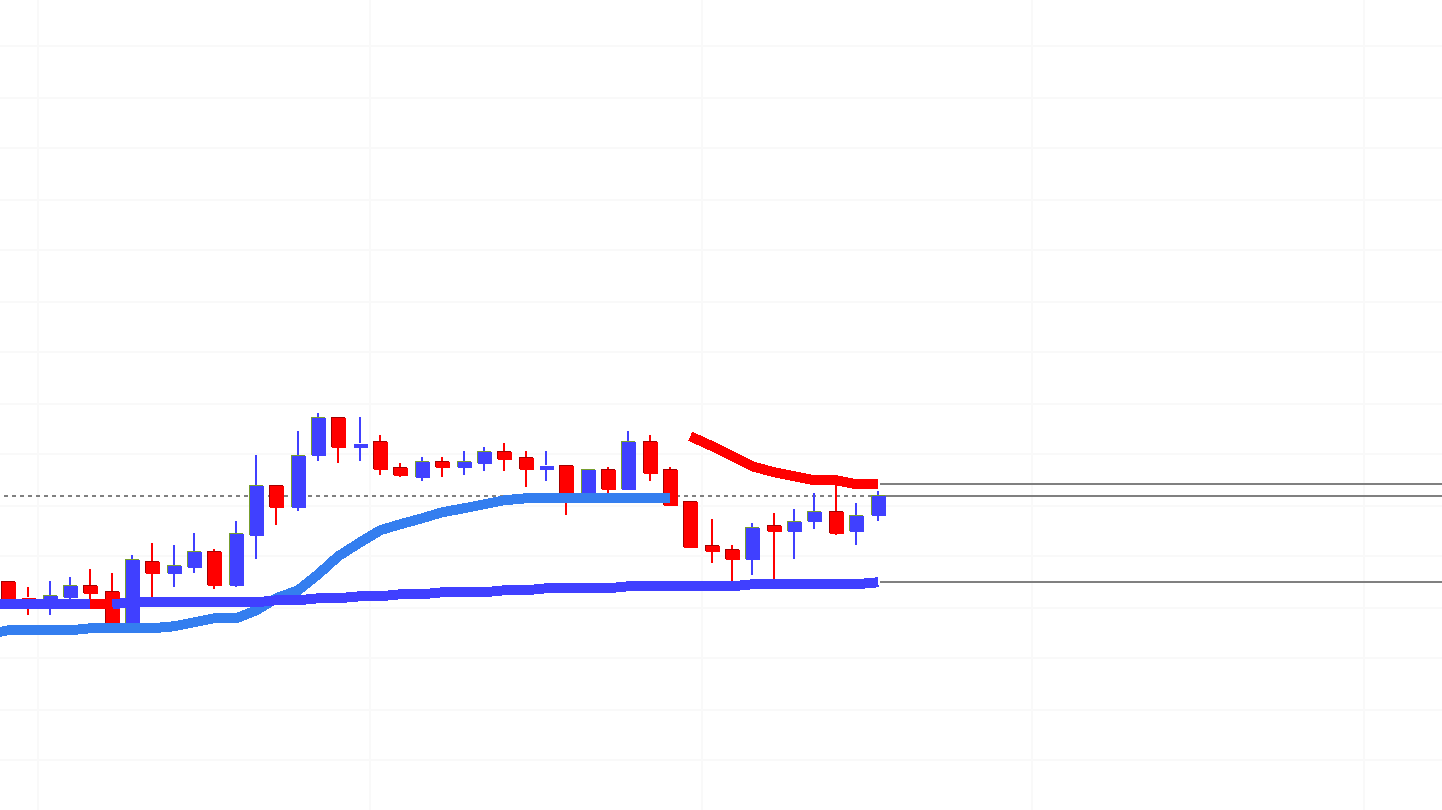

merci pour cette information. Juste une remarque : le signal est plus précoce sur IG que sur Dukascopy : copie écran 1 = IG / copie écran 2 = Dukascopy

Pas de signal chez Dukascopy.

Fr7

Fr7Participant

Master

doble desviación privada = 0,1 ;

Nicolas il y a une petite erreur dans Déviation = 0.01

timePeriod = 14

Desviación = 0,1

precio = personalizadoclose

dsma = WeightedAverage [timePeriod] (precio)

valuesLow = (1 - desviación / 100) * dsma

valores Alto = (1 + desviación / 100) * dsma

insumos = precio

si (entradas> valores alto) entonces

tendencia = 1

elsif (input <valuesLow) luego

tendencia = -1

terminara si

si (tendencia> 0) entonces

alpha1 = 0

si (valuesLow <valuesLow [1]) entonces

valuesLow = valuesLow [1]

terminara si

si la tendencia [1]> 0 entonces

salidas0 = valoresBajo

salidas1 = valores alto

alpha0 = 255

más

drawtext ("●", barindex, valueslow, dialog, bold, 22) coloreado (65,105,225)

terminara si

más

alpha0 = 0

if (valuesHigh> valuesHigh [1]) entonces

valuesHigh = valuesHigh [1]

terminara si

si la tendencia [1] <0 entonces

salidas1 = valores Alto

salidas0 = valores bajo

alpha1 = 255

más

drawtext ("●", barindex, valueshigh, dialog, bold, 22) coloreado (255,0,0)

terminara si

terminara si

devuelve salidas0 color (65,105,225, alpha0) estilo (línea, 4), salidas1 color (255,0,0, alpha1) estilo (línea, 4)

Fr7Participant

Master

timePeriod=14

Deviation=0.1

price=customclose

dsma = WeightedAverage[timePeriod](price)

valuesLow = (1 - deviation / 100) * dsma

valuesHigh = (1 + deviation / 100) * dsma

inputs=price

if (inputs > valuesHigh) then

trend = 1

elsif (inputs < valuesLow) then

trend = -1

endif

if (trend > 0) then

alpha1=0

if ( valuesLow < valuesLow[1]) then

valuesLow = valuesLow[1]

endif

if trend[1]>0 then

outputs0 = valuesLow

outputs1 = valueshigh

alpha0 = 255

else

drawtext("●",barindex,valueslow,dialog,bold,22) coloured(65,105,225)

endif

else

alpha0=0

if (valuesHigh > valuesHigh[1]) then

valuesHigh = valuesHigh[1]

endif

if trend[1]<0 then

outputs1 = valuesHigh

outputs0 = valueslow

alpha1 = 255

else

drawtext("●",barindex,valueshigh,dialog,bold,22) coloured(255,0,0)

endif

endif

return outputs0 coloured(65,105,225,alpha0) style(line,4), outputs1 coloured(255,0,0,alpha1) style(line,4)