Bonjour, j’ai un petit souci sur un algo et je ne comprends pas . c’est sur le stop win, qui est prévue à 100 points. il se met bien en clôture( algo en m1) seulement si sur exemple d’une vente le prix baisse le stop s’adapte toutes les minutes, MAIS, si le prix remonte, le stop remonte aussi. il arrive même qu’il se replace au stop d’origine, après le 1 er BE, si les prix remonte soit a moins de 100 points, je me retrouve avec un trade non protéger. j’aimerait juste comprendre mon erreur. Merci

Je ne connais pas le code ni le comportement du trailing stop / breakeven que tu utilises, mais je dirai que ça ressemble à une modification du niveau de sortie peu importe où il se situe actuellement. Je pense qu’il doit manquer quelquepart un test qui permet de ne pas autoriser la modification du niveau de stop si le nouveau niveau n’est pas favorable (comme dans le cas de ta vente où tu ne souhaites bien sûr pas qu’il remonte).

DEFPARAM CumulateOrders = false

DEFPARAM Preloadbars = 3000

daysForbiddenEntry = OpenDayOfWeek = 2

TIMEFRAME (DEFAULT)//(15 minutes)

indicator1 = CALL "992-GT3-RSR-SIGNAL"(close)

c1 = (indicator1 > 0.5)

indicator2 = AverageTrueRange[14](close)

c2 = (indicator2 >= 10)

TIMEFRAME (20 minutes)

dGreen, dRed, dGrey = Call "992-SPYDER-COLOR-ind"(close)

d1green = dGreen

d1red = dRed

d1grey = dGrey

d1red=d1red

d1grey=d1grey

TIMEFRAME (15 minutes)

IF (c1 AND c2 ) AND dgreen and d1green and not daysForbiddenEntry THEN

BUY 1 CONTRACT AT MARKET

ENDIF

TIMEFRAME (15 minutes)

indicator4 = CALL "R-992-RS"

c4 = (close < indicator4)

IF c4 THEN

SELL AT MARKET

ENDIF

indicator5 = CALL "992-GT3-RSR-SIGNAL"(close)

c5 = (indicator5 <= -0.5)

indicator6 = AverageTrueRange[14](close)

c6 = (indicator6 >= 12)

TIMEFRAME(15 minutes)

IF (c5 AND c6 ) AND dRed and d1red AND not daysForbiddenEntry THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

TIMEFRAME(15 minutes)

indicator8 = CALL "R-992-RS"

c8 = (close > indicator8)

IF c8 THEN

EXITSHORT AT MARKET

ENDIF

//*****************************************

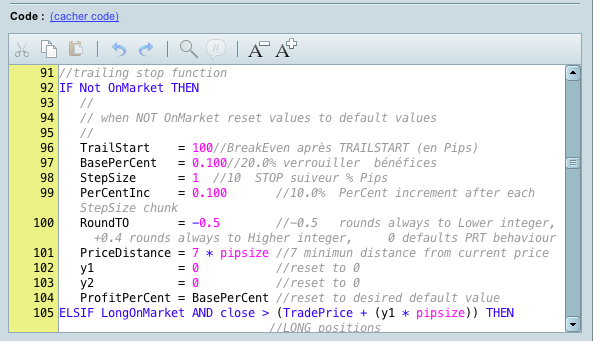

IF Not OnMarket THEN

TrailStart = 100//BreakEven après TRAILSTART (en Pips)

BasePerCent = 0.100//20.0% verrouiller bénéfices

StepSize = 1 //10 STOP suiveur % Pips

PerCentInc = 0.100 //10.0% PerCent increment after each StepSize chunk

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 30 * pipsize //12 minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG positions

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN // go ahead only if N+ pips

Diff1 = abs(TrailStart - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN //SHORT positions

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN // go ahead only if N+ pips

Diff2 = abs(TrailStart - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSize) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = Tradeprice + (y1 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = Tradeprice - (y2 * pipsize) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

endif

if close[0] crosses under average[200] and BARINDEX-TRADEINDEX(1)<5 then

sell at market//35//150

endif

IF longonmarket THEN

IF OpenDayOfWeek = 5 AND time >= 210000 THEN

sell at market

ENDIF

ENDIF

SET STOP %LOSS 1.4//1.7

SET TARGET %PROFIT 3.1//2.1

IF shortonmarket THEN

IF OpenDayOfWeek = 5 AND time >= 210000 THEN

exitshort at market

ENDIF

ENDIF

j espère que j ai bien ajouté le code, Merci Nicolas