Salve, vorrei sapere qual’è il modo più semplice per tenere valida una condizione per n barre. Un semplice esempio : supponiamo che dopo essere entrati long si voglia uscire dalla strategia con due condizioni, C1 e C2.

C1= rottura del massimo a 10 periodi , mentre C2 = low<low[2]. Come faccio a tener valida la condizione C1 per 10 barre, in modo che se entro 10 barre si verifica anche C2 la strategia esce, altrimenti si utilizzano altre uscite (trailing….).

Ho provato a fissare la rottura con barIndex, riprendendo un esempio dal manuale, ma sicuramente sbaglio qualcosa. Riporto un semplice esempio inventato al volo. Il problema è che il Ts non esce mai dal mercato una volta entrato.

If not longOnMarket and close>close[20] then

buy 1 contract at market

endif

hh=highest[10](high)

nBar=10

if close>hh and close[1]<hh[1] then

myBuy =close

myIndex =barIndex

endif

if barIndex<myIndex+nBar and low<low[2] then

myBuy =0

endif

if longOnMarket and myBuy>0 then

sell 1 contract at market

endif

GRAZIE

Per favore usa sempre il pulsante “Insert PRT code” quando inserisci il codice nei tuoi post per facilitare la lettura degli altri.

Grazie 🙂

Eccolo:

If not longOnMarket and close>close[20] then

buy 1 contract at market

endif

hh=highest[10](high)

nBar=10

if close crosses over hh[1] then

myBuy =close

myIndex =barIndex

endif

if barIndex>(myIndex+nBar) then

myBuy =0

endif

if longOnMarket and myBuy>0 and low<low[2] then

sell 1 contract at market

endif

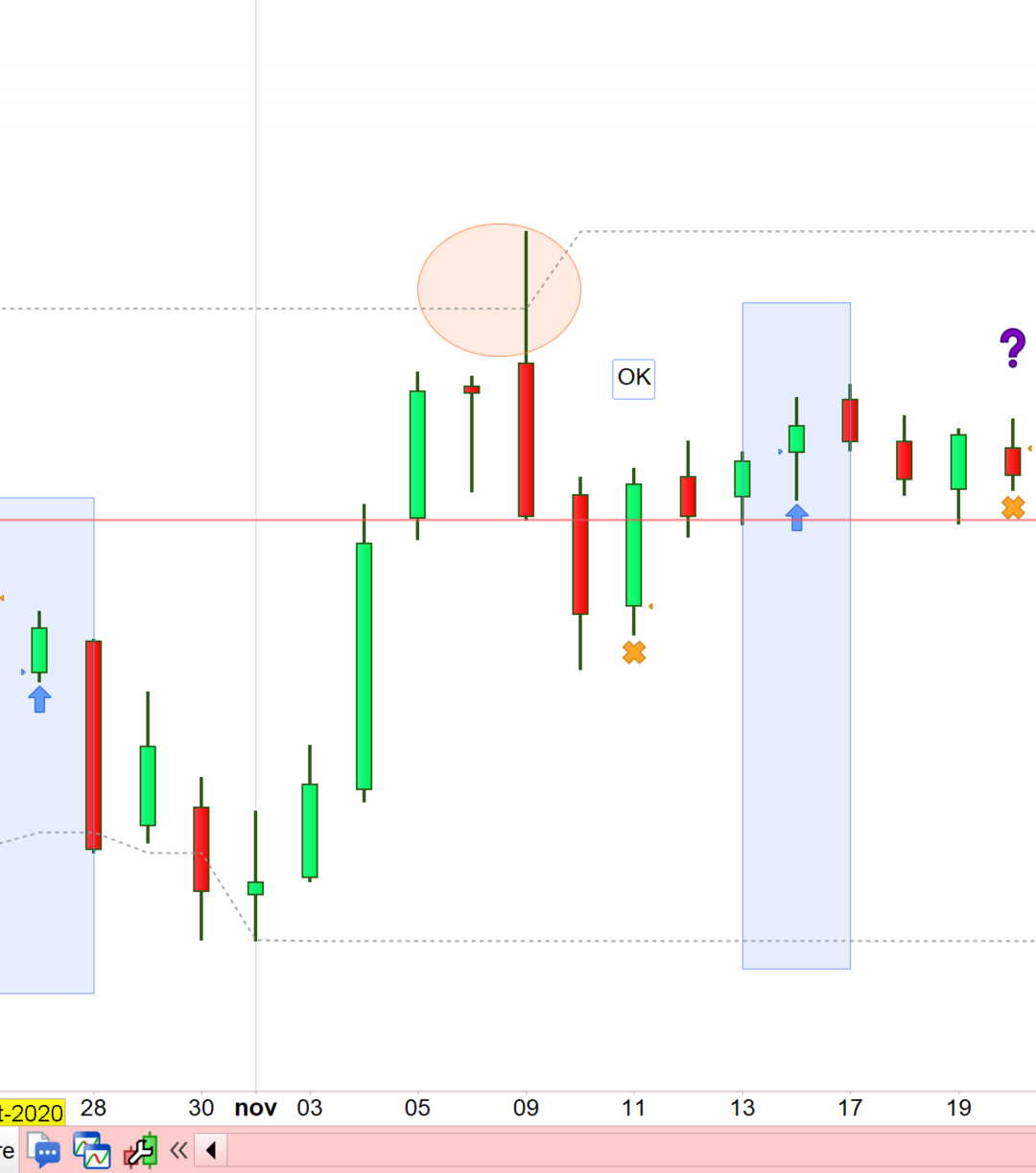

Ciao Roberto, seguirò la regola di usare il pulsante “Insert PRT” per i codici in futuro. Ho provato il Ts corretto. Ora esce, però non rispetta sempre la condizione c1, ossia non tiene sempre conto del breakout del massimo hh. Nell’immagine allegata, nel primo segnale si rispettano sia c1 che c2, nel secondo segnale solo c2.

Ho plottato per errore i massimi a 20 periodi al posto di 10, ma rimane il problema sopra riportato. Grazie

Aggiungi la riga:

myBuy = 0

tra la 14 e la 15, perché se myBuy non viene azzerato continua ad uscire.

Ciao Roberto, ho provato, ma non funziona ancora. Poi non capisco perchè alla riga 6 il close si riferisce a hh[1] e non hh. Non è: close>hh e close[1]<hh[1] identico a close crosses over hh? Grazie

CLOSE come può essere > HIGH?

Però in caso di Break Out può essere > del precedente HIGH.

Certo, mi sono sbagliato. Un ultima cosa, si potrebbe scrivere il codice con soltanto barIndex-myIndex e nBar? Oppure è fondamentale usare anche in vari punti myBuy? Grazie

Si, certo, puoi eliminare le righe 7 e 10-12, sostituendo alla riga 13 myBuy > 0 con:

barIndex <= (myIndex+nBar)

Ho provato a riscrivere il codice senza “myBuy”, come mi h

hh=highest[10](high)

nBar=10

if not longOnMarket and close>close[20] then

buy 1 contract at market

endif

if close crosses over hh[1] then

myBuy = close

myIndex = barIndex

endif

if barIndex>=(myIndex+nBar) then

myBuy = 0

endif

if longOnMarket and myBuy>0 and low<low[2] then

sell 1 contract at market

myBuy = 0

endif

ai consigliato sopra, ma i risultati sono molto differenti. Il primo codice, quello con myBuy funziona, quindi è il secondo da rivedere. Allego i due esempi di TS con insertPRT.

hh=highest[10](high)

nBar = 10

if not longOnMarket and close>close[20] then

buy 1 contract at market

endif

if close crosses over hh[1] then

myIndex = barIndex

endif

if longOnMarket and barIndex <= (myIndex + nBar) and low<low[2] then

sell 1 contract at market

endif

Usa il primo.

Non è obbligatorio togliere myBuy.

Ciao Roberto, chiudo questo topic, riscrivendo nel modo più semplice e chiaro l’esempio di sopra per mantenere mobile una condizione (di acquisto o vendita), sperando possa servire ad altri utenti

hh=highest[10](high)

nBar=10

if not longOnMarket and close>close[20] then

buy 1 contract at market

endif

if close crosses over hh[1] then

crossOverIndex=barIndex

cExit=1

endif

if barIndex>=(crossOverIndex+nBar) then

cExit=0

endif

if longOnMarket and cExit=1 and low<low[2] then

sell 1 contract at market

cExit=0

endif