Salve a tutti,

ho questo codice per multichart che vorrei codificare in PRT, codice su Gold tf 1h, qualcuno potrebbe aiutarmi?

grazie

PS.

gli orari sono quelli di Chicago

input:valoreSL(1500);

vars: LongTrades(0), ShortTrades(0);

If date<>date[1] then

begin

LongTrades=0;

ShortTrades=0;

end;

var : giornoIndecisione (false);

giornoIndecisione = absvalue(opend(1)-closed(1)) <= 0.50*(Highd(1)-LowD(1)); // Filtro indecisione giorno precedente

If Marketposition = 0 and Time>1000 and Time<2400 and

LongTrades=0 and

giornoIndecisione and

Momentum(close,5)<2*avgtruerange(5) and Highest(High[1],3)<maxlist(HighD(1), HighD(2)) [1]

then buy next bar maxlist(HighD(1), HighD(2))stop;

If Marketposition = 0 and Time>100 and Time<1000 and

ShortTrades=0 and

giornoIndecisione and

Momentum(close,5)<2*avgtruerange(3) and

lowest(Low[1],3)>minlist(LowD(1), LowD(2))[1]

then sellshort next bar minlist(LowD(1), LowD(2)) stop;

If Marketposition = 1 and Time=200 then sell next bar market;

If Marketposition = -1 and Time=1000 then buytocover next bar market;

//casual friday

If dayofweek(date)=5 and T=1600 then

Begin

sell next bar market;

buytocover next bar market;

end;

input: percentualeDaily(80), ATRLength(4);

If MarketPosition <>0 then

begin

sell Next Bar at (EntryPrice -(percentualeDaily/100) * AvgTrueRange(ATRLength) of Data2) stop;

buytocover Next Bar at (EntryPrice + (percentualeDaily/100) * AvgTrueRange(ATRLength) of Data2) stop;

end;

if valoreSL <> 0 then setstoploss(valoreSL );

DANY

DANYParticipant

Senior

Ciao,

eccolo !

- Ho assunto che il DATA2 di Multicharts fosse sempre sul GOLD e con Timeframe giornaliero.

- Importante sarebbe sapere se Multichart gira su Ora Locale o su “Exchange Time” perchè in tal caso andrebbero riportati gli orari Exchange o meglio convertiti in Local per PRT. Io al momento li ho tenuti invariati.

- Andrebbe ottimizzato lo STOP Loss che ho tenuto ad 1/10 del contratto Future GOLD.

- Risultato complessivamente non male ma CFD e Future non sono sempre confrontabili. Però è interessante e ci si può lavorare…. Se ne hai altri li traduco senza problemi. Ci metto 10 minuti. Al limite sentiamoci direttamente se preferisci.

Ciao.

valoreSL=150 //x CFD 10 oz, un decimo del Gold standard

If date<>date[1] then

LongTrades=0

ShortTrades=0

endif

giornoIndecisione=0

giornoIndecisione = abs(dopen(1)-dclose(1)) <= 0.50*(dHigh(1)-dLow(1)) // Filtro indecisione giorno precedente

CondL1=Momentum[5](close)<2*averagetruerange[5](close)

CondL2=Highest[3](High[1])<max(dHigh(1), dHigh(2))[1] //??

If not OnMarket and Time>100000 and Time<240000 and LongTrades=0 and giornoIndecisione and CondL1 and CondL2 then

buy 1 contract at max(dHigh(1), dHigh(2)) stop

endif

CondS1=Momentum[5](close)<2*averagetruerange[3](close)

CondS2=Lowest[3](Low[1])>min(dLow(1), dLow(2))[1] //??

If not OnMarket and Time>010000 and Time<100000 and ShortTrades=0 and giornoIndecisione and CondS1 and CondS2 then

sellshort 1 contract at min(dLow(1), dLow(2)) stop

endif

If LongOnMarket = 1 and Time=020000 then

sell at market

endif

If ShortOnMarket and Time=100000 then

exitshort at market

endif

//casual friday

If dayofweek=5 and Time=160000 then

sell at market

exitshort at market

endif

percentualeDaily=80

ATRLength=4

timeframe(daily)

VarATR=AverageTrueRange[ATRLength](close)

timeframe(default)

If OnMarket then

sell at (PositionPrice - (percentualeDaily/100) * VarATR) stop

exitshort at (PositionPrice + (percentualeDaily/100) * VarATR) stop

endif

if valoreSL <> 0 then

set stop ploss valoreSL

endif

DANYParticipant

Senior

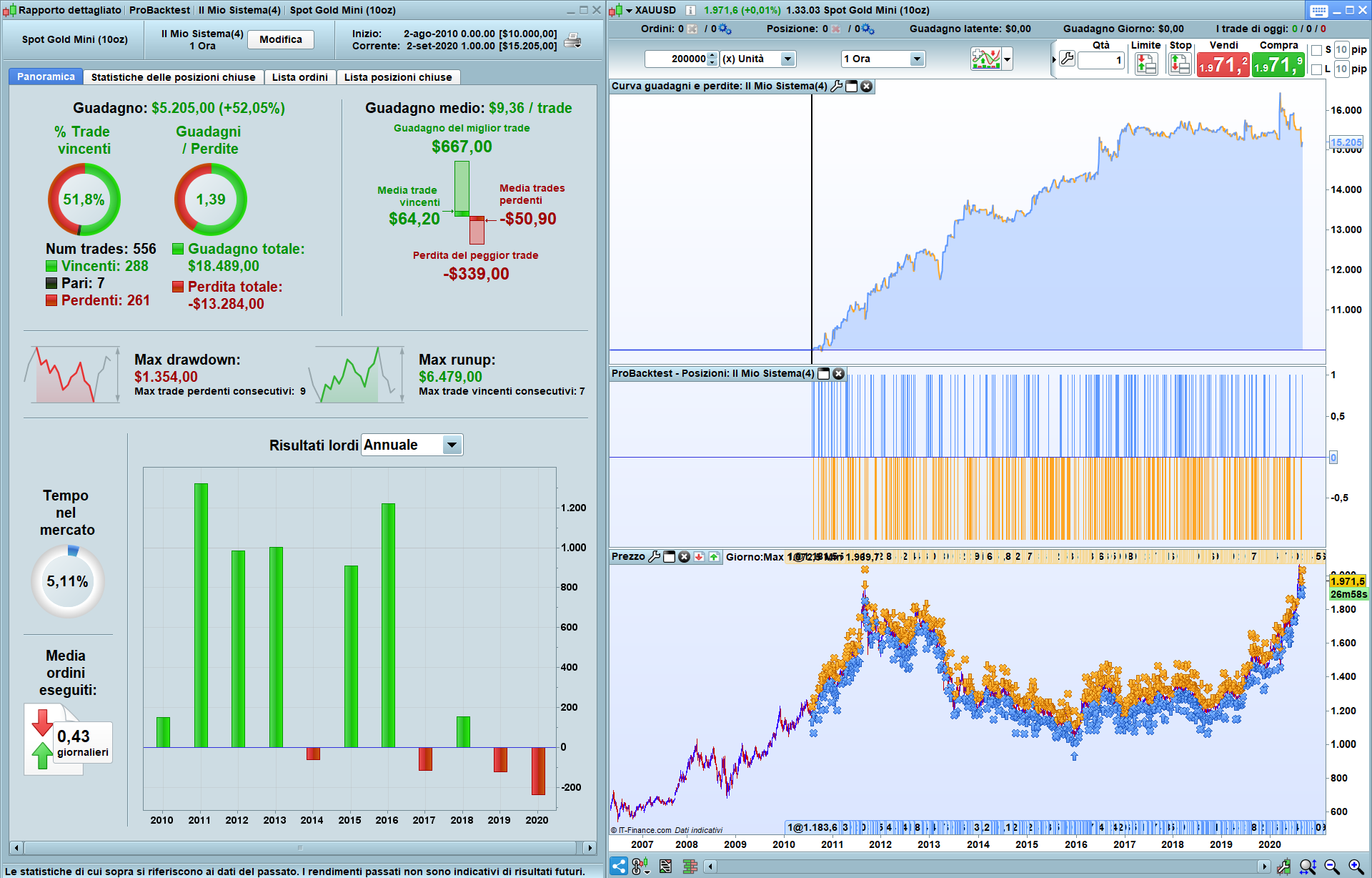

Scusa, vedo solo ora che avevi specificato l’exchange time di Chicago…. Ho convertito gli orari. Molto meglio sino al 2017 (vedi immagine allegata) ma poi non guadagna più anche se non perde. Bisogna lavorarci un po’ per vedere se il sistema magari è un po’ vecchio e ha smesso di funzionare oppure se ci sono solo da ottimizzare un po’ le variabili.

valoreSL=150 //x CFD 10 oz, un decimo del Gold standard

If date<>date[1] then

LongTrades=0

ShortTrades=0

endif

giornoIndecisione=0

giornoIndecisione = abs(dopen(1)-dclose(1)) <= 0.50*(dHigh(1)-dLow(1)) // Filtro indecisione giorno precedente

CondL1=Momentum[5](close)<2*averagetruerange[5](close)

CondL2=Highest[3](High[1])<max(dHigh(1), dHigh(2))[1] //??

//100000-> 170000

//240000-> 070000

If not OnMarket and ((Time>170000 and Time<230000) OR (Time>010000 AND time<070000)) and LongTrades=0 and giornoIndecisione and CondL1 and CondL2 then

buy 1 contract at max(dHigh(1), dHigh(2)) stop

endif

CondS1=Momentum[5](close)<2*averagetruerange[3](close)

CondS2=Lowest[3](Low[1])>min(dLow(1), dLow(2))[1] //??

//010000 -> 080000

If not OnMarket and (Time>080000 and Time<170000) and ShortTrades=0 and giornoIndecisione and CondS1 and CondS2 then

sellshort 1 contract at min(dLow(1), dLow(2)) stop

endif

//020000 -> 090000

If LongOnMarket = 1 and Time=090000 then

sell at market

endif

If ShortOnMarket and Time=170000 then

exitshort at market

endif

//casual friday

If dayofweek=5 and Time=230000 then

sell at market

exitshort at market

endif

percentualeDaily=80

ATRLength=4

timeframe(daily)

VarATR=AverageTrueRange[ATRLength](close)

timeframe(default)

If OnMarket then

sell at (PositionPrice - (percentualeDaily/100) * VarATR) stop

exitshort at (PositionPrice + (percentualeDaily/100) * VarATR) stop

endif

if valoreSL <> 0 then

set stop ploss valoreSL

endif

Grazie mille DANY per aver dedicato del tempo ad aiutare gli altri membri con le loro richieste. Apprezzo molto! 😉

GRAZIE 1000 Dany,

quale è la tua mail? ti contatto

grazie

Per favore non includere informazioni personali come indirizzi e-mail o numeri di telefono nei tuoi post.

Grazie 🙂

DANYParticipant

Senior

Giustamente come dice Roberto non è permesso mettere i propri dati in chiaro. Se per te non ci sono problemi posso continuare a darti assistenza sul forum, altrimenti segui pure le indicazioni di Roberto. Ciao.