Dear Traders and Coders,

I’ve coded a system that takes very short term entries using a simple moving average cross over, but also looks at the higher time frame to filter the direction it takes.

I also use the ATR as the value for a trailing stop loss.

My question is this:

Is there a way to adjust bet size so that it’s 0.5% of account equity for each trade?

This would need to take the ATR value and account equity into account and then adjust the bet size accordingly for each trade.

Here is what I’ve cobbled together so far:

//Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

//Check for trend on higher timeframe

timeframe(1 day,updateonclose)

emaHTF100 = ExponentialAverage[100]

emaHTF200 = ExponentialAverage[200]

C1= (close > emaHTF100)

C3= (close < emaHTF100)

C5= (close < emaHTF200)

C6= (close > emaHTF200)

// Conditions to enter long positions

timeframe(default)

indicator1 = ExponentialAverage[5]

indicator2 = ExponentialAverage[20]

C2= (indicator1 CROSSES OVER Indicator2)

IF CountOfPosition < 2 AND C1 AND C2 THEN

BUY 1 PERPOINT AT MARKET

ENDIF

// Conditions to enter short positions

timeframe(default)

C4= (indicator1 CROSSES UNDER Indicator2)

IF CountOfPosition < 2 AND C3 AND C4 THEN

SELLSHORT 1 PERPOINT AT MARKET

ENDIF

// TRAILING STOP

myATR = 5* averagetruerange[14](close)

//trailing stop

SET STOP TRAILING myATR

Many Thanks

Matt

//Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

//Check for trend on higher timeframe

timeframe(1 day,updateonclose)

emaHTF100 = ExponentialAverage[100]

emaHTF200 = ExponentialAverage[200]

C1= (close > emaHTF100)

C3= (close < emaHTF100)

C5= (close < emaHTF200)

C6= (close > emaHTF200)

// Conditions to enter long positions

timeframe(default)

indicator1 = ExponentialAverage[5]

indicator2 = ExponentialAverage[20]

C2= (indicator1 CROSSES OVER Indicator2)

IF CountOfPosition < 2 AND C1 AND C2 THEN

BUY PositionSize CONTRACTS AT MARKET

ENDIF

// Conditions to enter short positions

timeframe(default)

C4= (indicator1 CROSSES UNDER Indicator2)

IF CountOfPosition < 2 AND C3 AND C4 THEN

SELLSHORT PositionSize CONTRACTS AT MARKET

ENDIF

REM Money Management

Capital = 50000

Risk = 0.005

StopLoss = myATR

REM Calculate contracts

equity = Capital + StrategyProfit

maxrisk = round(equity*Risk)

PositionSize = abs(round((maxrisk/StopLoss)/PointValue)*pipsize)

// TRAILING STOP

myATR = 5* averagetruerange[14](close)

//trailing stop

SET STOP TRAILING myATR

This was my attempt, it seems to work, but the worst trade is always larger than 5% of 50,000. So that makes me think that at some point it’s not always doing it right. Because with a trailing SL the absolute maximum starting risk should be at £250 (5% of £50k) and often when booking a losing trade it would have moved into profit at least a bit and this would then have trailed the stop up meaning the ‘Loss of Worst Trade’ should always be under £250 regardless of the number of points the trailing stop loss used (taking 5x ATR as the max/start point).

Anybody have any other suggestions or alternatives methods?

Cheers

Try adding this snippet between lines 14 and 15 of your first code:

ONCE Capital = 10000

ONCE PerCent = 0.5 //0.5%

Equity = Capital + StrategyProfit

Risk = -(Equity * PerCent / 100)

CurrentGain = PositionPerf * PositionPrice * PipValue

IF CurrentGain <= Risk THEN

SELL AT Market

EXITSHORT AT Market

ENDIF

it exits as soon as the current loss reaches your RISK level. Of course on a low TF this will be quite accurate, while on a higher TF (such as 1+ hour) the loss can easily exceed your planned risk (MTF might help much in this case).

Change your Capital as needed.

0,5% is quite low, it may turn your code into a hugely losing strategy.

Thank you for the reply Roberto. I’ve added that snippet to the existing code, and added a few time restrictions. So now the code looks like this:

//Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

// Prevents the system from creating new orders to enter the market or increase position size before the specified time

noEntryBeforeTime = 080000

timeEnterBefore = time >= noEntryBeforeTime

// Prevents the system from placing new orders to enter the market or increase position size after the specified time

noEntryAfterTime = 190000

timeEnterAfter = time < noEntryAfterTime

//Check for trend on higher timeframe

timeframe(1 day,updateonclose)

emaHTF100 = ExponentialAverage[100]

emaHTF200 = ExponentialAverage[200]

C1= (close > emaHTF100)

C3= (close < emaHTF100)

C5= (close < emaHTF200)

C6= (close > emaHTF200)

// Conditions to enter long positions

timeframe(default)

ONCE Capital = 50000

ONCE PerCent = 0.5 //0.5%

Equity = Capital + StrategyProfit

Risk = -(Equity * PerCent / 100)

CurrentGain = PositionPerf * PositionPrice * PipValue

IF CurrentGain <= Risk THEN

SELL AT Market

EXITSHORT AT Market

ENDIF

indicator1 = ExponentialAverage[5]

indicator2 = ExponentialAverage[20]

C2= (indicator1 CROSSES OVER Indicator2)

IF CountOfPosition < 2 AND (timeEnterBefore AND timeEnterAfter) AND C1 AND C2 THEN

BUY PositionSize CONTRACTS AT MARKET

ENDIF

// Conditions to enter short positions

timeframe(default)

C4= (indicator1 CROSSES UNDER Indicator2)

IF CountOfPosition < 2 AND (timeEnterBefore AND timeEnterAfter) AND C3 AND C4 THEN

SELLSHORT PositionSize CONTRACTS AT MARKET

ENDIF

REM Money Management

Capital = 50000

Risk = 0.005

StopLoss = myATR

REM Calculate contracts

equity = Capital + StrategyProfit

maxrisk = round(equity*Risk)

PositionSize = abs(round((maxrisk/StopLoss)/PointValue)*pipsize)

// TRAILING STOP

myATR = 5* averagetruerange[1000](close)

//trailing stop

SET STOP TRAILING myATR

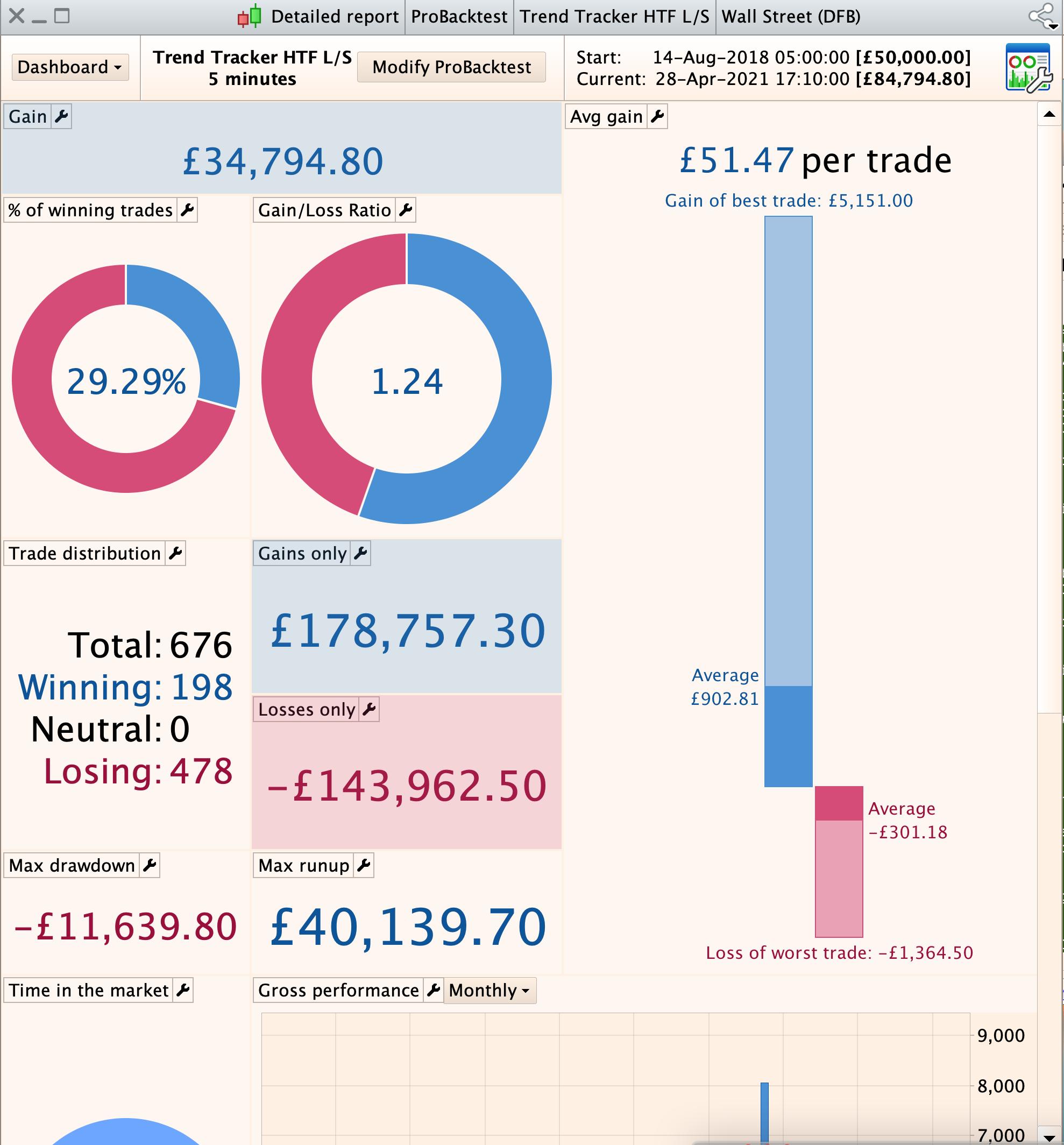

It appears to be working, but it’s hard to tell as the backtest results at present on PRT seem to be giving some suspicious data back, occasionally only returning like 5 trades over 2 years, when clearly it should have easily placed hundreds. However, for the time being these are the results I’m seeing when run on the 5minute charts on the DOW.

One issue is line 61, since it is executed every bar, it changes while a trade is open, affecting the trailing stop each time. It should be left unchanged when OnMarket:

IF Not OnMarket THEN

myATR = 5* averagetruerange[1000](close)

ENDIF

another issue is line 64, since SET STOP TRAILING only sets a pace, not a start. Most people (and myself as well) use the redy-to-run snippet by Nicolas from lines 17 to 56 at https://www.prorealcode.com/blog/trading/complete-trailing-stop-code-function/.

Do I also need to repeat this snippet to apply to the short trades too? Or does adding it in between lines 14 and 15 work for both long and short orders?

I’m afraid my novice skills are being tested here and I’m probably making more of a mess of it.

Using Nicholas’ trailing SL code and your snippet above, this is what I have. It’s incredibly profitable, but it’s not right haha.

//Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

// Prevents the system from creating new orders to enter the market or increase position size before the specified time

noEntryBeforeTime = 080000

timeEnterBefore = time >= noEntryBeforeTime

// Prevents the system from placing new orders to enter the market or increase position size after the specified time

noEntryAfterTime = 190000

timeEnterAfter = time < noEntryAfterTime

//Check for trend on higher timeframe

timeframe(1 day,updateonclose)

emaHTF100 = ExponentialAverage[100]

emaHTF200 = ExponentialAverage[200]

C1= (close > emaHTF100)

C3= (close < emaHTF100)

C5= (close < emaHTF200)

C6= (close > emaHTF200)

// Conditions to enter long positions

timeframe(default)

ONCE Capital = 50000

ONCE PerCent = 0.5 //0.5%

Equity = Capital + StrategyProfit

Risk = -(Equity * PerCent / 100)

CurrentGain = PositionPerf * PositionPrice * PipValue

IF CurrentGain <= Risk THEN

SELL AT Market

EXITSHORT AT Market

ENDIF

indicator1 = ExponentialAverage[5]

indicator2 = ExponentialAverage[20]

C2= (indicator1 CROSSES OVER Indicator2)

IF CountOfPosition < 2 AND (timeEnterBefore AND timeEnterAfter) AND C1 AND C2 THEN

BUY PositionSize CONTRACTS AT MARKET

ENDIF

// Conditions to enter short positions

timeframe(default)

C4= (indicator1 CROSSES UNDER Indicator2)

IF CountOfPosition < 2 AND (timeEnterBefore AND timeEnterAfter) AND C3 AND C4 THEN

SELLSHORT PositionSize CONTRACTS AT MARKET

ENDIF

REM Money Management

Capital = 50000

Risk = 0.005

StopLoss = myATR

REM Calculate contracts

equity = Capital + StrategyProfit

maxrisk = round(equity*Risk)

PositionSize = abs(round((maxrisk/StopLoss)/PointValue)*pipsize)

// TRAILING STOP

myATR = 5* averagetruerange[1000](close)

//************************************************************************

//trailing stop function

trailingstart = myATR //trailing will start @trailinstart points profit

trailingstep = 1 //trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

//************************************************************************

There may well be some redundant code in there now, I really appreciate your help and patience here.

Cheers

It works for both Long and Short trades.

If you use MyATR then you have to change line 65:

trailingstart = myATR/PipSize

because MyATR is a (difference in) price, while that code requires pips.

It works fine as it is now with Nasdaq, Dax and other indices, but not with other instruments such as fx currency pairs.