Hi Can you please help translating the below to ProRealTime code. Thanks

The original Chandelier Exit formula consists of three parts: a period high or period low, the Average True Range (ATR) and a multiplier. Using the default setting of 22-periods on a daily chart, the Chandelier Exit will look for the highest high or lowest low of the last 22 days. Note that there are 22 trading days in a month. This parameter (22) will also be used to calculate the Average True Range.

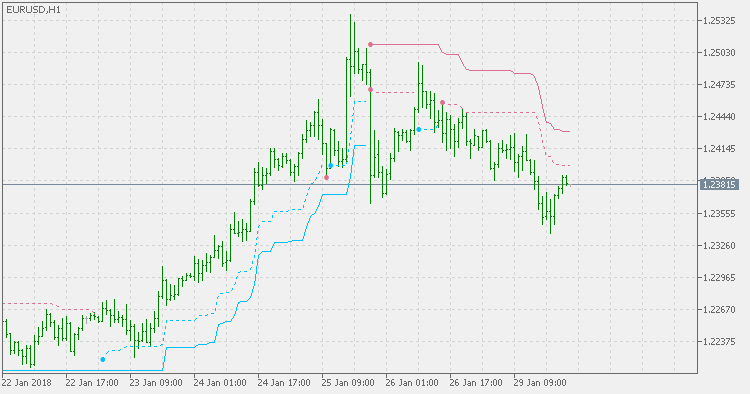

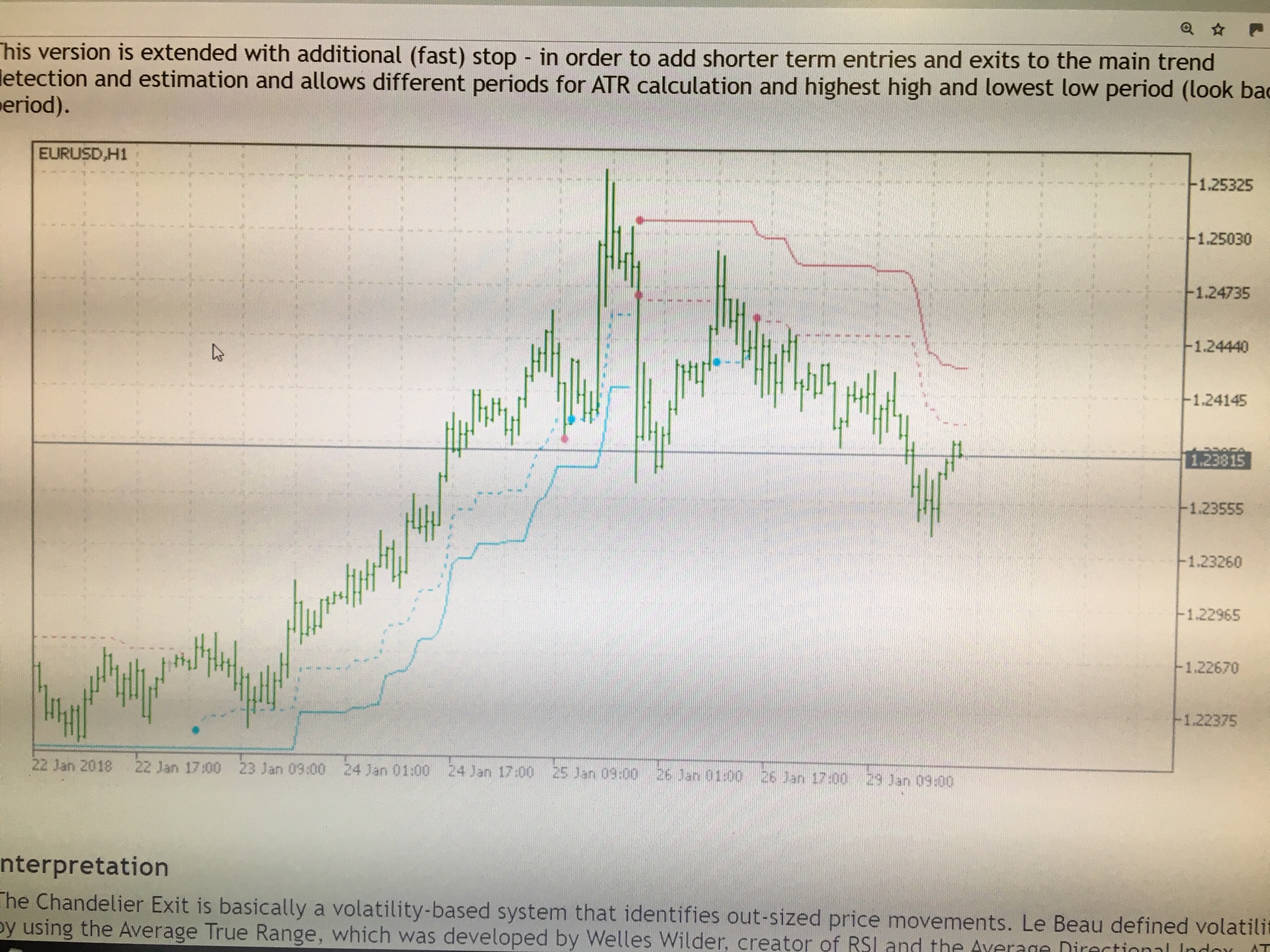

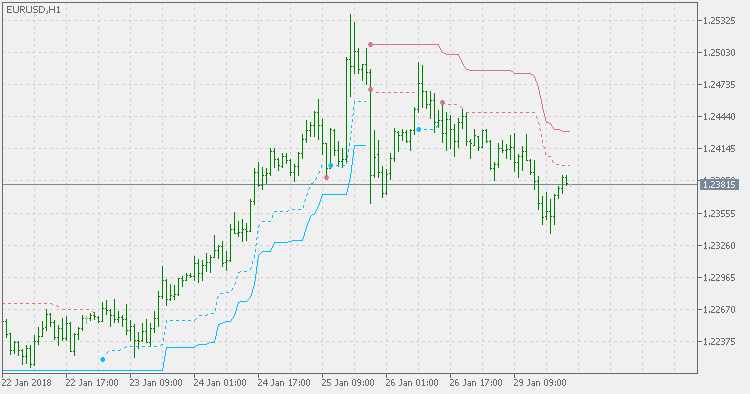

This version is extended with additional (fast) stop – in order to add shorter term entries and exits to the main trend detection and estimation and allows different periods for ATR calculation and highest high and lowest low period (look back period).

input int AtrPeriod = 22; // Atr period

input double AtrMultiplier1 = 3.0; // Atr 1st multiplier

input double AtrMultiplier2 = 4.5; // Atr 2nd multiplier

input int LookBackPeriod = 22; // Look-back period

#property indicator_chart_window

#property indicator_buffers 8

#property indicator_plots 8

#property indicator_type1 DRAW_LINE

#property indicator_color1 clrDeepSkyBlue

#property indicator_style1 STYLE_DOT

#property indicator_type2 DRAW_LINE

#property indicator_style2 STYLE_DOT

#property indicator_color2 clrPaleVioletRed

#property indicator_type3 DRAW_LINE

#property indicator_color3 clrDeepSkyBlue

#property indicator_type4 DRAW_LINE

#property indicator_color4 clrPaleVioletRed

#property indicator_type5 DRAW_ARROW

#property indicator_color5 clrDeepSkyBlue

#property indicator_type6 DRAW_ARROW

#property indicator_color6 clrPaleVioletRed

#property indicator_type7 DRAW_ARROW

#property indicator_color7 clrDeepSkyBlue

#property indicator_type8 DRAW_ARROW

#property indicator_color8 clrPaleVioletRed

//— input parameters

input int AtrPeriod = 22; // Atr period

input double AtrMultiplier1 = 3.0; // Atr 1st multiplier

input double AtrMultiplier2 = 4.5; // Atr 2nd multiplier

input int LookBackPeriod = 22; // Look-back period

double UplBuffer1[],UpdBuffer1[],DnlBuffer1[],DndBuffer1[],UplBuffer2[],UpdBuffer2[],DnlBuffer2[],DndBuffer2[];

//+——————————————————————+

//| Custom indicator initialization function |

//+——————————————————————+

int OnInit()

{

//— indicator buffers mapping

SetIndexBuffer(0,UplBuffer1,INDICATOR_DATA);

SetIndexBuffer(1,DnlBuffer1,INDICATOR_DATA);

SetIndexBuffer(2,UplBuffer2,INDICATOR_DATA);

SetIndexBuffer(3,DnlBuffer2,INDICATOR_DATA);

SetIndexBuffer(4,UpdBuffer1,INDICATOR_DATA); PlotIndexSetInteger(4,PLOT_ARROW,159);

SetIndexBuffer(5,DndBuffer1,INDICATOR_DATA); PlotIndexSetInteger(5,PLOT_ARROW,159);

SetIndexBuffer(6,UpdBuffer2,INDICATOR_DATA); PlotIndexSetInteger(6,PLOT_ARROW,159);

SetIndexBuffer(7,DndBuffer2,INDICATOR_DATA); PlotIndexSetInteger(7,PLOT_ARROW,159);

return (INIT_SUCCEEDED);

}

//

//

//

void OnDeinit(const int reason)

{

}

//+——————————————————————+

//| Work array |

//+——————————————————————+

double work[][6];

#define _hi1 0

#define _lo1 1

#define _hi2 2

#define _lo2 3

#define _trend1 4

#define _trend2 5

//+——————————————————————+

//| Custom indicator iteration function |

//+——————————————————————+

int OnCalculate(const int rates_total,const int prev_calculated,const datetime &time[],

const double &open[],

const double &high[],

const double &low[],

const double &close[],

const long &tick_volume[],

const long &volume[],

const int &spread[])

{

if(Bars(_Symbol,_Period)<rates_total) return(prev_calculated);

if(ArrayRange(work,0)!=rates_total) ArrayResize(work,rates_total);

int i=(int)MathMax(prev_calculated-1,1); for(; i<rates_total && !_StopFlag; i++)

{

UplBuffer1[i] = UpdBuffer1[i] = DnlBuffer1[i] = DndBuffer1[i] = EMPTY_VALUE;

UplBuffer2[i] = UpdBuffer2[i] = DnlBuffer2[i] = DndBuffer2[i] = EMPTY_VALUE;

//

//——————-

//

int _start = MathMax(i-LookBackPeriod,0);

double _atr = 0; for(int k=1; k<=AtrPeriod && (i-k-1)>=0; k++) _atr += MathMax(high[i-k],close[MathMax(i-k-1,0)])- MathMin(low[i-k],close[MathMax(i-k-1,0)]); _atr/=(double)AtrPeriod;

double _max = high[ArrayMaximum(high,_start,LookBackPeriod)];

double _min = low [ArrayMinimum(low ,_start,LookBackPeriod)];

work[i][_hi1] = _max-AtrMultiplier1*_atr;

work[i][_lo1] = _min+AtrMultiplier1*_atr;

work[i][_hi2] = _max-AtrMultiplier2*_atr;

work[i][_lo2] = _min+AtrMultiplier2*_atr;

work[i][_trend1] = (i>0) ? work[i-1][_trend1] : 0;

work[i][_trend2] = (i>0) ? work[i-1][_trend2] : 0;

if(i>0)

{

if(close[i] > work[i-1][_lo1]) work[i][_trend1]= 1;

if(close[i] < work[i-1][_hi1]) work[i][_trend1]= –1;

if(close[i] > work[i-1][_lo2]) work[i][_trend2]= 1;

if(close[i] < work[i-1][_hi2]) work[i][_trend2]= –1;

if(AtrMultiplier1>0 && work[i][_trend1] == 1) { if(work[i][_hi1]<work[i-1][_hi1]) work[i][_hi1]=work[i-1][_hi1]; UplBuffer1[i] = work[i][_hi1]; if(UplBuffer1[i-1]==EMPTY_VALUE) UpdBuffer1[i]=UplBuffer1[i];}

if(AtrMultiplier1>0 && work[i][_trend1] == –1) { if(work[i][_lo1]>work[i-1][_lo1]) work[i][_lo1]=work[i-1][_lo1]; DnlBuffer1[i] = work[i][_lo1]; if(DnlBuffer1[i-1]==EMPTY_VALUE) DndBuffer1[i]=DnlBuffer1[i];}

if(AtrMultiplier2>0 && work[i][_trend2] == 1) { if(work[i][_hi2]<work[i-1][_hi2]) work[i][_hi2]=work[i-1][_hi2]; UplBuffer2[i] = work[i][_hi2]; if(UplBuffer2[i-1]==EMPTY_VALUE) UpdBuffer2[i]=UplBuffer2[i];}

if(AtrMultiplier2>0 && work[i][_trend2] == –1) { if(work[i][_lo2]>work[i-1][_lo2]) work[i][_lo2]=work[i-1][_lo2]; DnlBuffer2[i] = work[i][_lo2]; if(DnlBuffer2[i-1]==EMPTY_VALUE) DndBuffer2[i]=DnlBuffer2[i];}

}

}

return (i);

}

//+——————————————————————+