Hello, I’d like to:

1/ compare in Intraday current volume to Average[20](Volume) taking into account only volume during normal market hours, for example 9am to 5.30pm for DAX. The average should exclude volumes during the period 5.30pm to 9.00am next day.

2/ compare current volume (today) VS yesterday’s volume at the same time, for example volume today between 9.00am and 9.30am VS volume the day before between 9.00am and 9.30 am.

Thanks

Khaled – I guess that you are requesting someone to code you an indicator? If so then you have posted in the wrong forum. I have moved your topic to the place for indicators.

Post your topic in the correct forum:

_ ProRealTime Platform Support: only platform related issues.

_ ProOrder: only strategy topics.

_ ProBuilder: only indicator topics.

_ ProScreener: only screener topics

_ General Discussion: any other topics.

_ Welcome New Members: for new forum members to introduce themselves.

Good morning, maybe my initial request was not clear enough…

Let’s assume:

volume 5 min bar closing at 17:25 is 50 (the previous day)

volume 5 min bar closing at 17:30 is 70 (the previous day)

volume 5 min bar closing at 08:50 is 100

volume 5 min bar closing at 08:55 is 120

volume 5 min bar closing at 09:00 is 200

volume 5 min bar closing at 09:05 is 250

I’d like to calculate the Simple Average Volume on last 4 bars excluding the time from 17:30pm to 08:59 am, i.e. average of (50, 70, 200, 250)=142.5

When I apply the condition

if time>=090000 and time<=173000 then

xVol = Average[4](Volume)

endif

the first average calculated at 09:00 will take into account the four bars closing before 09:00, i.e. (09:00, 08:55, 08:50, 08:45)

Thank you for you help.

Thank you Roberto. I’m afraid this doesn’t solve my problem.

I have copied the “Time Range Simple Moving Average” code and changed “TRSMA” into “TRAV” (Time Range Average Volume” and replaced “Close” with “Volume”. Kept Periods = 20

// TRAV - Time Range Average Volume

DEFPARAM CalculateOnLastBars = 200

//Periods = 20

//StartTime = 090000

//EndTime = 173000

Periods = max(2,min(999,Periods))

StartTime = max(0,min(240000,StartTime))

EndTime = max(0,min(240000,EndTime))

//

i = 0

TRAV = 0

FOR j = 0 TO 3000

IF opentime[j] >= StartTime AND opentime[j] <= EndTime THEN

TRAV = TRAV + Volume[j]

i = i + 1

IF i = Periods THEN

BREAK

ENDIF

ENDIF

NEXT

TRAV = (TRAV / Periods)

IF TRAV = 0 THEN

TRAV = Volume

ENDIF

Return TRAV AS "TRAV"

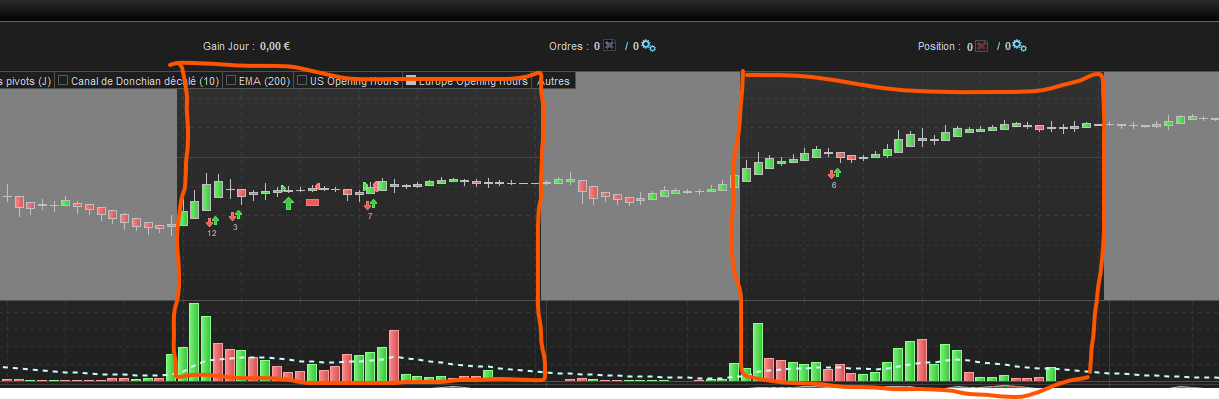

On a 5 min TF, if you look at the candle starting 28 Dec. at 09:00 the volume is 1199 but the TRAV is 59.95 (1199/20). The second candle starting at 09:05 shows a volume of 727, so the average (from the begining of the day) shoud be = 963, but the TRAV shows 96.30 (dividing by 20 instead of dividing by the number of candles since 09:00am). So the code divides the cumulative volume by 20.

I tried to tweak the code to get this value corresponding to the average but I was unsuccesful.

Can you please look again at this (maybe using summation or average formula)?

Thanks a million.

Maybe this?

Only works on v11

p = 4

starttime = 090000

endtime = 173000

once avg = undefined

if opentime >= starttime and opentime < endtime then

a = a + 1

$vol[a] = volume

if a >=p then

total = 0

for b = a downto a-p

total = total + $vol[b]

next

avg = total/p

endif

else

avg = 0

endif

return avg

Thank you Vonasi. Doesn’t work on the first bar of the 28th Dec. Divides the Vol by 4 instead of 1, same issue with the second bar, divides the Cumulative Vol by 4 instead of 2.

Solved! Thank you very much for your help, Roberto and Vonasi!!!!

DEFPARAM CALCULATEONLASTBARS = 200

// Average Volume Intraday

IF time = 090000 then

barstart= barindex

ENDIF

IF time>=090000 and time<=173000 then

n = max(1, (intradaybarindex-barstart+1))

AV = SUMMATION[n](volume)/ n

ENDIF

RETURN AV as "Average Volume Intraday"

As you can see, the Avg Vol on the first 30 min bar is equal to the volume of the first bar, works well for the second, etc.

Glad you found your answer. I didn’t get that that was the problem you were trying to solve from your descriptions and I guess Roberto didn’t either. 🙂

You might want to change TIME for OPENTIME as TIME is the closing time of a candle so you will miss the first candle in your session.

This does the same thing:

DEFPARAM CALCULATEONLASTBARS = 1000

IF opentime = 090000 then

n = 0

myvolume = 0

endif

IF opentime >= 090000 and opentime < 173000 then

n = n + 1

myvolume = myvolume + volume

av = myvolume / n

endif

return av as "Average Volume Intraday"

Thank you so much Vonasi! Will use this associated with STD on Vol and compare the Current Session to Day-1 and/or Week-1 (same day) to confirm acceleration in the market activity (sort of filter).

Good to hear you have solved it!

The average is made to account for PERIODS units, no matter the time. If your time starts at 9, it will consider 1 current bar + the last 19 bars of the previous day before 17:30.

Since volume was 0 last Thursday, actually it seems the average of the first candle is volume / 20 periods. NO, it’s the sum of the volume of the last 20 periods / 20 periods. Of course it considers only periods within the defined time range.