Hi,

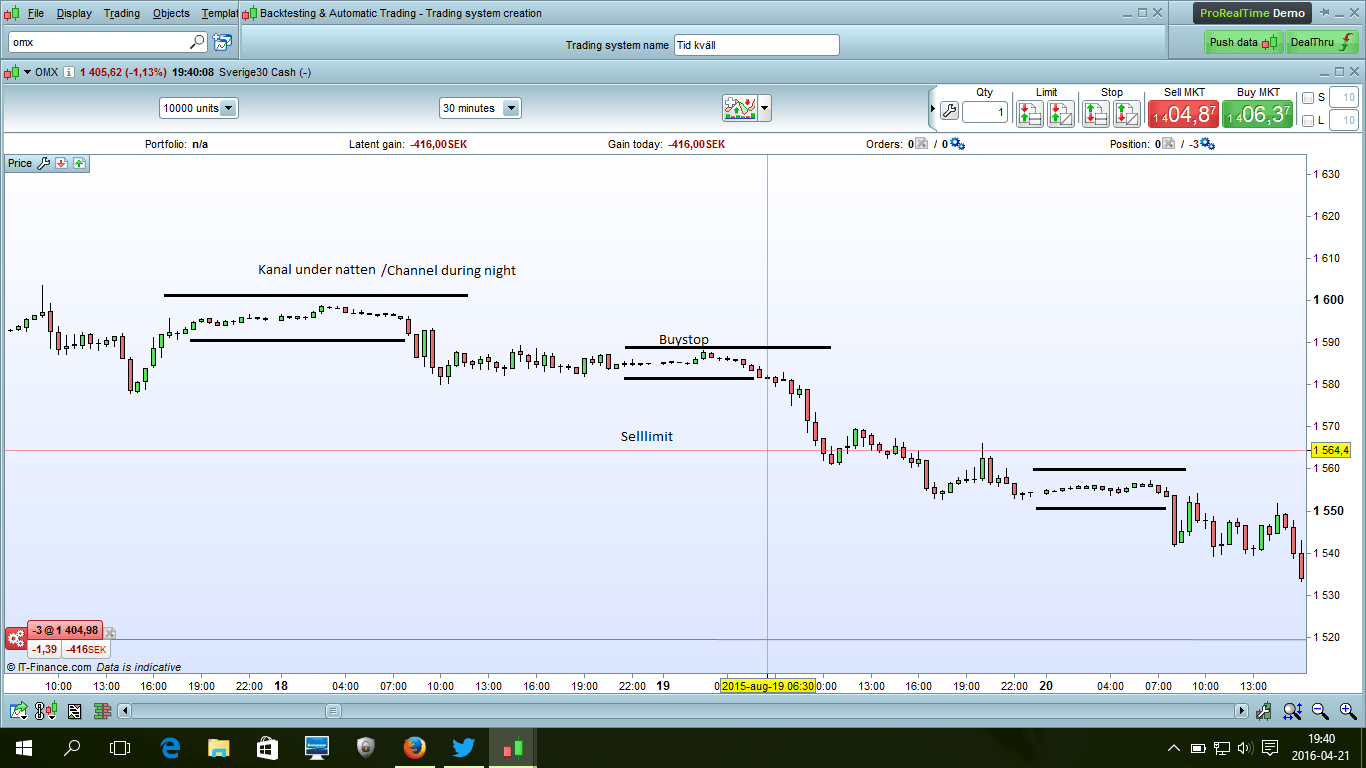

I have tried to write a code that “Catch a move each day with the channel made during night”. It dose that by define a channel each night, and then add some distance to a Buystop and a Sellimit. But I cant get it right, can some please help? 🙂

//Goal to place a buystop some distance over the channel made during night, and a sellimit some distance under the channel made during night.

defparam preloadbars =20

If time = 060000 then // an attempt to define the channel made during night

HL = highest[4](high)

LL = lowest[4](low)

endif

HL1 = HL+2 //an attempt to add distance upp and down on the channel made during night.

LL1 = LL-2

c1 = close > HL1

//c2 = close < LL1

If time > 070000 and time < 170000 and c1 then

buy 1 shares at HL1 stop

sellshort 1 shares at LL1 limit

endif

Exit by Stoploss and takeprofit

Its made for OMX, or similar. And on 30M, or lesser timeframe.

At line 13, for your c1 condition you are testing if close is already above HL1.

Then at line 17 you’re trying to place a stop order at HL1, but you cannot do that, because a stop pending order must be placed above the price (for buying purpose).

If you already known that the price has break up your defined zone (c1 is true), then just BUY at that moment directly on market, without setting a stop order:

buy 1 shares at market

That is for the buy condition. For your sell one, you have totally messed up the whole code here 🙂 Because if you want to set pending orders, don’t test if price has already crossed up or down your trigger prices! Just defined your pending orders and that’s all! 😉

Thanks Nicolas!

I tried this:

defparam preloadbars =400

if intradaybarindex = 0 then

openbuy=0

opensell=0

endif

If time = 060000 then

HL = highest[360](high)

LL = lowest[360](low)

endif

HL1 = HL+2

LL1 = LL-2

c1 = close > HL1

c2 = close < LL1

If time > 060000 and time < 160000 and c1 then

buy 1 shares at market

openbuy = openbuy+1

endif

If time > 060000 and time < 160000 and c2 then

sellshort 1 shares at market

opensell = opensell+1

endif

SET STOP PLOSS 5

But the system takes so many trades a day, like in the picture. I wish it only to take one buy and/or one sell-trade day.

I use it on 1 min timeframe now 🙂

Sorry, I found the problem 🙂

It should be like this:

defparam preloadbars =400

if intradaybarindex = 0 then

openbuy=0

opensell=0

endif

If time = 060000 then

HL = highest[360](high)

LL = lowest[360](low)

endif

HL1 = HL+2

LL1 = LL-2

c1 = close > HL1

c2 = close < LL1

If time > 060000 and time < 160000 and openbuy=0 and c1 then

buy 1 shares at market

openbuy = openbuy+1

endif

If time > 060000 and time < 160000 and opensell=0 and c2 then

sellshort 1 shares at market

opensell = opensell+1

endif

SET STOP PLOSS 5

Hi, i’m working on a breakout strategy and get this:

REM No acumular órdenes

DEFPARAM CumulateOrders=True

REM Horario de operativa

DEFPARAM FlatBefore = 090100

DEFPARAM FlatAfter = 152900

REM APERTURA

//apertura=dopen(0)

REM Maximo y minimo nocturno

if time=080000 then // Select time when max and min are tested

maximo=dhigh(0)+x*pipsize // x= points distance above maximum night range

minimo=dlow(0)-y*pipsize //y= points distance under minimum night range

endif

REM If price is in night range both orders are "STOP"

if HIGH<maximo and LOW>minimo then

if not onmarket then

buy myLOT contract at maximo stop

sellshort myLOT contract at minimo stop

set target pprofit yourprofit

set stop ploss yourstop

endif

REM If price is above maximum

if Close>maximo then

if not longonmarket then

buy myLOT contract at maximo limit // buy in a pullback

buy myLOT contract at market // Buy at market

set target pprofit yourprofit

set stop ploss yourstop

endif

ENDIF

REM ENTRAR AL MERCADO POR DEBAJO DEL RANGO

REM VENDER

IF Close<minimo then

if not shortonmarket and posicion>1 then

sellshort myLOT contract at minimo limit

sellshort mylot shares at market

set target pprofit yourprofit

set stop ploss yourstop

endif

endif

I did a backtest on it and seems like it’s working fine, hope it helps you!

Cheers

Is it possibile maybe to filter trades by, for example, SuperTrend? 🙂

Sorry i don’t know what SuperTrend is… atm!, will check it!

Sorry, my bad, its an indicator:

Supertrend

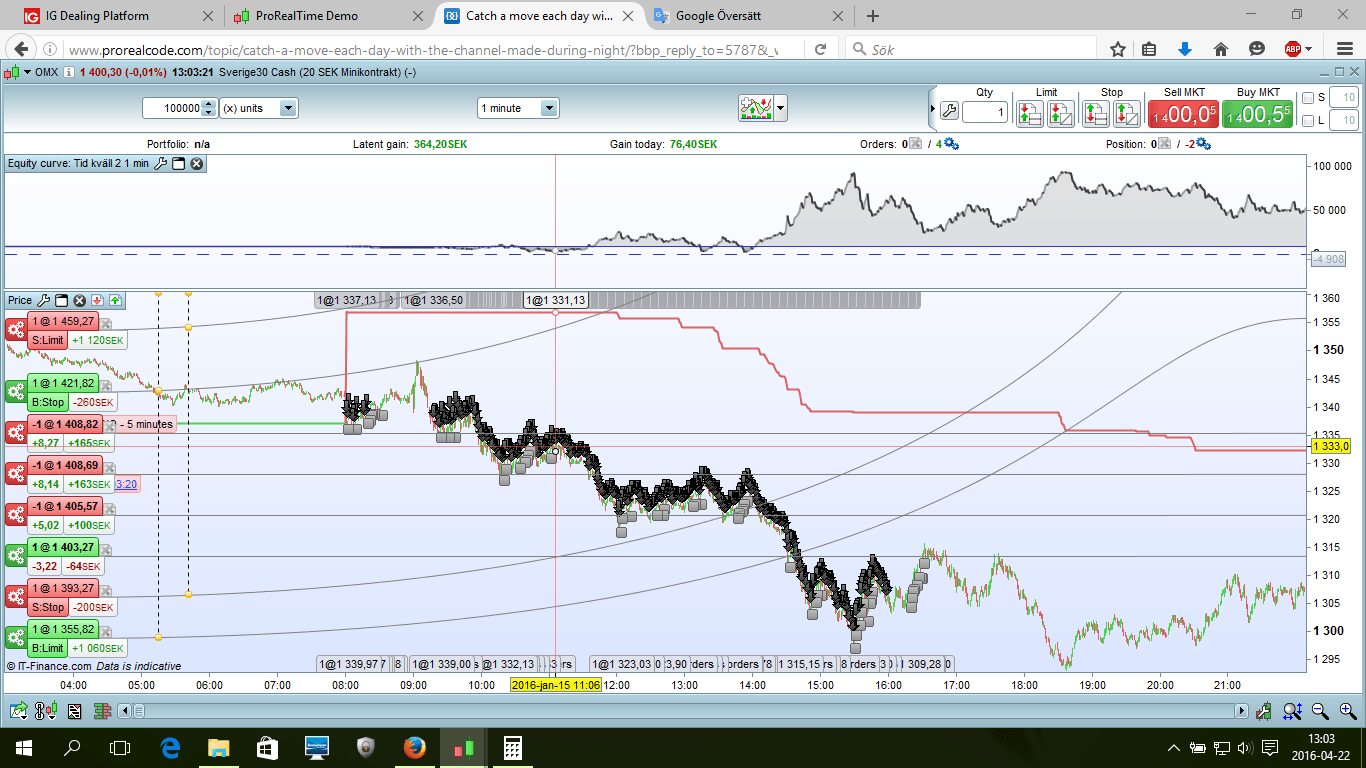

This was the best I came up with today, BUT it need more backtesting!

//-------------------------------------------------------------------------

// Main code : Tid kväll 2 1 min x

//-------------------------------------------------------------------------

defparam preloadbars =800

cl=461

cs=361

x=5

y=4

if intradaybarindex = 0 then

openbuy=0

opensell=0

endif

//SP = Supertrend[30,10]

//SPU = close > SP

//SPD = close < SP

If time = 060000 then

HL = highest[360](high)

LL = lowest[360](low)

endif

HL1 = HL+x

LL1 = LL-y

c1 = close > HL1

c2 = close < LL1

If time > 060000 and time < 150000 and openbuy=0 and c1 then

buy 1 shares at market

openbuy = openbuy+1

endif

If time > 060000 and time < 150000 and opensell=0 and c2 then

sellshort 1 shares at market

opensell = opensell+1

endif

If longonmarket and close<close[cl] then

sell at market

endif

If shortonmarket and close>close[cs] then

exitshort at market

endif

SET TARGET PPROFIT 70

SET STOP PTRAILING 35

// Optimera cl och cs 0, 725, 25

// Optimera x och y 2, 20, 1

It dosent seem to work on other period then I tested on 🙂

Hi again Nicolas, Adolfo or someone else.

I would like to make a filter (or system) witch only allows trades

if the prize sometime during the day,

during a period of 8 hours hasn’t moved more than 2 points.

If the prize after the 8 hours period breaks up or down,

the system should take an order in the direction.

I have tried to make this, but can’t get it right.

I use it on 5 min timeframe.

I tried this:

HL = highest[96](close)

LL = lowest[96](close)

HL1 = HL+x

LL1 = LL-y

channel = LL1 - HL1 <= 2

But I don’t know how to define the “8h, no more than 2 points” channel.

Thanks!

Hi, i found this error:

HL = highest[96](close)

LL = lowest[96](close)

HL1 = HL+x

LL1 = LL-y

channel = HL1 - LL1 <= 2 // High -Low instead Low - high

Cheers!