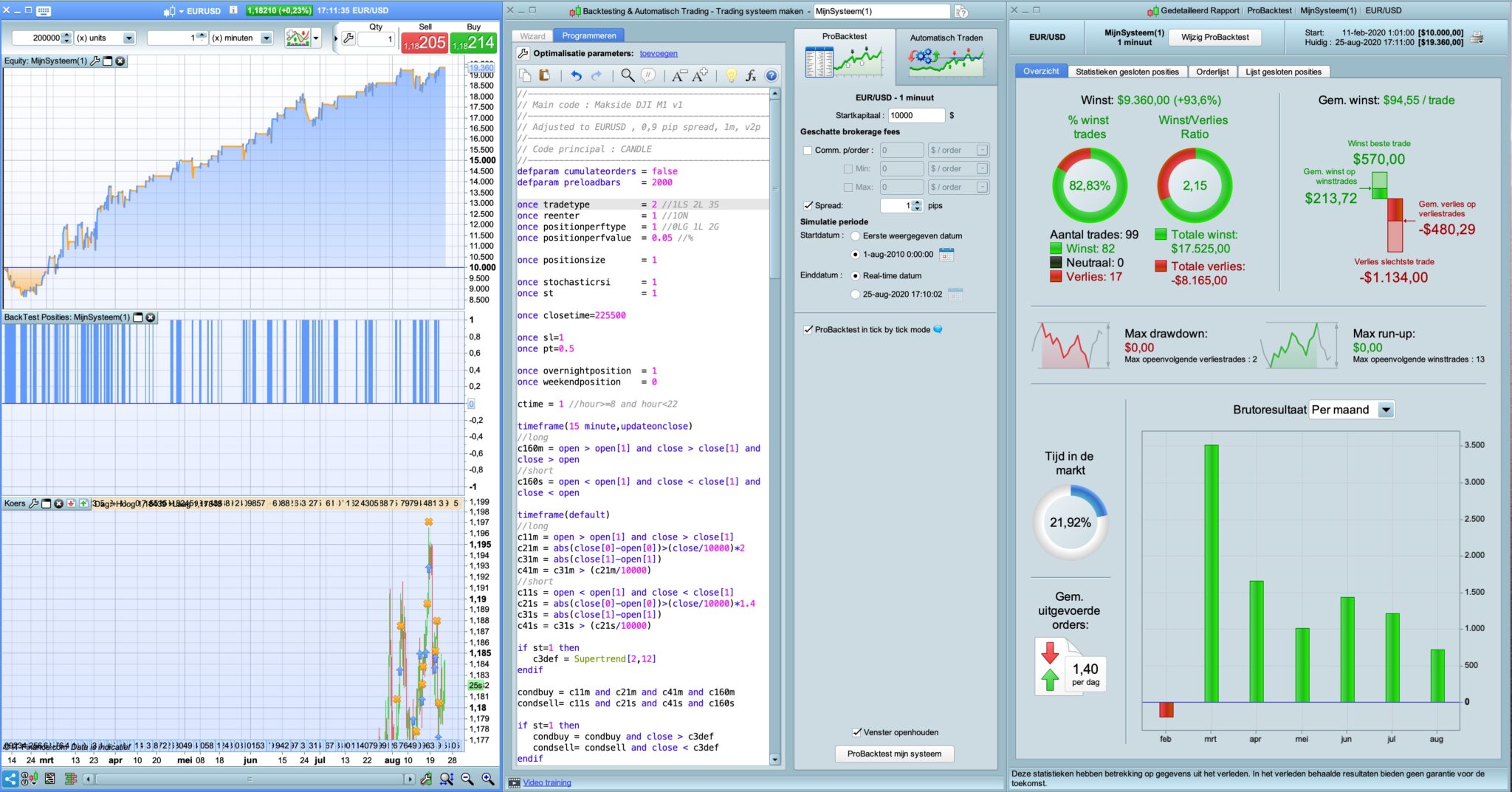

//————————————————————————-

// Main code : Makside DJI M1 v1

//————————————————————————-

// Adjusted to EURUSD , 0,9 pip spread, 1m, v1p

//————————————————————————-

// Code principal : CANDLE

//————————————————————————-

defparam cumulateorders = false

defparam preloadbars = 2000

once tradetype = 1 //1LS 2L 3S

once reenter = 0 //1ON

once positionperftype = 1 //0LG 1L 2G

once positionperfvalue = 0.05 //%

once positionsize = 1

once stochasticrsi = 1

once closetime=225500

once sl=1

once pt=0.5

once overnightposition = 1

once weekendposition = 0

ctime = 1 //hour>=8 and hour<22

timeframe(15 minute,updateonclose)

c160m = open > open[1] and close > close[1] and close > open

timeframe(default)

c11m = open > open[1] and close > close[1]

c21m = abs(close[0]-open[0])>(close/10000)*1.4

c31m = abs(close[1]-open[1])

c41m = c31m > (c21m/10000)

c3def = Supertrend[6,1]

condbuy = c11m and c21m and c41m and c160m

condbuy = condbuy and close > c3def

//Stochastic RSI | indicator

if stochasticrsi then

lengthRSI = 4 //RSI period

lengthStoch = 6 //Stochastic period

smoothK = 2 //Smooth signal of stochastic RSI

smoothD = 6 //Smooth signal of smoothed stochastic RSI

myRSI = RSI[lengthRSI](totalprice)

MinRSI = lowest[lengthStoch](myrsi)

MaxRSI = highest[lengthStoch](myrsi)

StochRSI = (myRSI-MinRSI) / (MaxRSI-MinRSI)

K = average[smoothK](stochrsi)*100

D = average[smoothD](K)

c13 = K>D

condbuy = condbuy and c13 and not c13[1]

endif

condsell=0

// entry criteria

if ctime then

if (tradetype=1 or tradetype=2) then

if condbuy and not longonmarket then

buy positionsize contract at market

if tradetype=1 then

set stop %loss sl

set target %profit pt

elsif tradetype=2 then

set stop %loss sl

set target %profit pt

endif

endif

endif

if (tradetype=1 or tradetype=3) then

if condsell and not shortonmarket then

sellshort positionsize contract at market

if tradetype=1 then

set stop %loss sl

set target %profit pt

elsif tradetype=3 then

set stop %loss sl

set target %profit pt

endif

endif

endif

if reenter then

if positionperftype=1 then

positionperformance=positionperf(0)*100<-positionperfvalue

elsif positionperftype=2 then

positionperformance=positionperf(0)*100>positionperfvalue

else

positionperformance=((positionperf(0)*100)<-positionperfvalue or (positionperf(0)*100)>positionperfvalue)

endif

if (tradetype=1 or tradetype=2) then

if condbuy and longonmarket and positionperformance then

sell at market

endif

if condbuy[1] and not longonmarket then

buy positionsize contract at market

if tradetype=1 then

set stop %loss sl

set target %profit pt

elsif tradetype=2 then

set stop %loss sl

set target %profit pt

endif

endif

endif

if (tradetype=1 or tradetype=3) then

if condsell and shortonmarket and positionperformance then

exitshort at market

endif

if condsell[1] and not shortonmarket then

sellshort positionsize contract at market

if tradetype=1 then

set stop %loss sl

set target %profit pt

elsif tradetype=3 then

set stop %loss sl

set target %profit pt

endif

endif

endif

endif

else

if longonmarket and condsell then

//sell at market

endif

if shortonmarket and condbuy then

//exitshort at market

endif

endif

/// trailing stop percentage

once trailingstoptype=1

if trailingstoptype then

once trailingpercent = 0.165

once steppercent = (trailingpercent/10)*1

if onmarket then

trailingstart = tradeprice(1)*(trailingpercent/100)

trailingstep = tradeprice(1)*(steppercent/100)

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

newsl=0

endif

if longonmarket then

if newsl=0 and low-tradeprice(1)>=trailingstart then

newsl = tradeprice(1)+trailingstep

endif

if newsl>0 and low-newsl>trailingstep then

newsl = newsl+trailingstep

endif

endif

if shortonmarket then

if newsl=0 and tradeprice(1)-high>=trailingstart then

newsl = tradeprice(1)-trailingstep

endif

if newsl>0 and newsl-high>trailingstep then

newsl = newsl-trailingstep

endif

endif

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

if newsl>0 then

if low crosses under newsl then

sell at market

endif

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

if newsl>0 then

if high crosses over newsl then

exitshort at market

endif

endif

endif

endif

if not overnightposition then

if time>=closetime then

sell at market

exitshort at market

endif

endif

if not weekendposition then

if (dayofweek=5 and time>=closetime) then

exitshort at market

sell at market

endif

endif