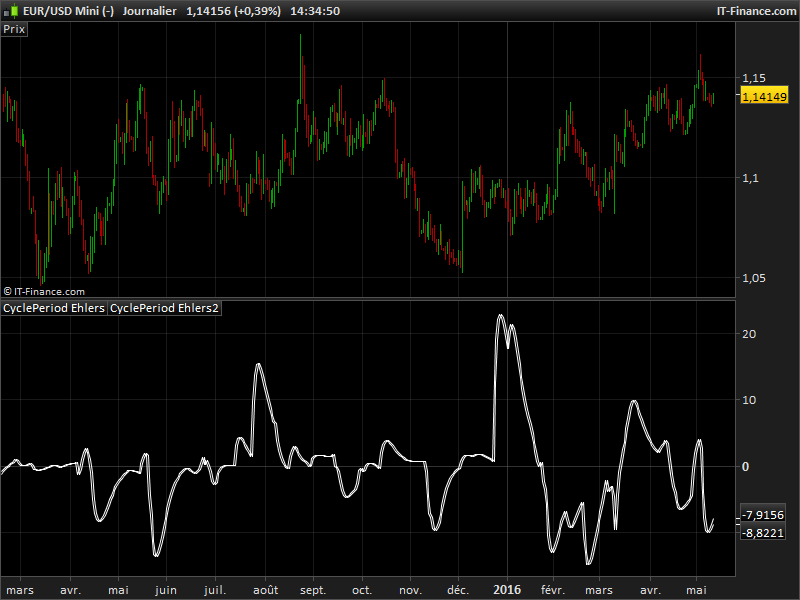

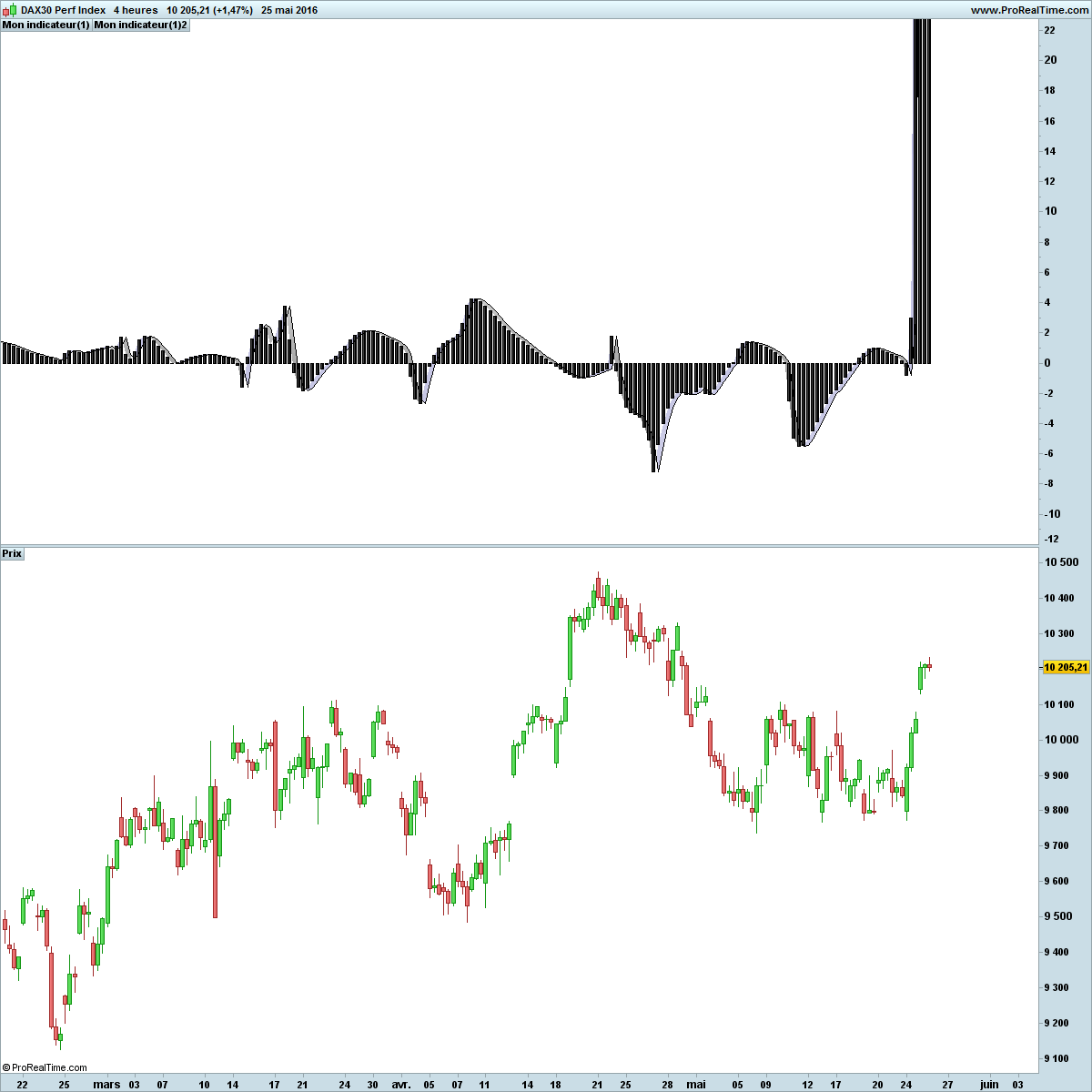

Bonjour à tous,

Je cherche à coder cet indicateur d’Ehlers qui détermine la péridoe du cycle dominant.

Je bute sur la conversion de ce code MT5 en PRT car MT5 n’est vraiment pas ma tasse de thé

Alors si quelqu’un a plus de facilité pour faire la conversion

Merci d’avance

Zilliq

#property copyright "Copyright 2011, Investeo.pl"

#property link "http://Investeo.pl"

#property version "1.00"

#property indicator_separate_window

#property description "CyclePeriod indicator - described by John F. Ehlers"

#property description "in \"Cybernetic Analysis for Stocks and Futures\""

#property indicator_buffers 2

#property indicator_plots 2

#property indicator_width1 1

#property indicator_width2 1

#property indicator_type1 DRAW_LINE

#property indicator_type2 DRAW_LINE

#property indicator_color1 Green

#property indicator_color2 Red

#property indicator_label1 "Cycle"

#property indicator_label2 "Trigger Line"

#define Price(i) ((high[i]+low[i])/2.0)

double Smooth[];

double Cycle[];

double Trigger[];

double Q1[];

double I1[];

double DeltaPhase[];

double InstPeriod[];

double CyclePeriod[];

input double InpAlpha=0.07;

int OnInit()

{

ArraySetAsSeries(Cycle,true);

ArraySetAsSeries(CyclePeriod,true);

ArraySetAsSeries(Trigger,true);

ArraySetAsSeries(Smooth,true);

SetIndexBuffer(0,CyclePeriod,INDICATOR_DATA);

SetIndexBuffer(1,Trigger,INDICATOR_DATA);

PlotIndexSetDouble(0,PLOT_EMPTY_VALUE,0.0);

PlotIndexSetDouble(1,PLOT_EMPTY_VALUE,0.0);

return(0);

}

int OnCalculate(const int rates_total,

const int prev_calculated,

const datetime &time[],

const double &open[],

const double &high[],

const double &low[],

const double &close[],

const long &tick_volume[],

const long &volume[],

const int &spread[])

{

long tickCnt[1];

int i;

int ticks=CopyTickVolume(Symbol(), 0, 0, 1, tickCnt);

if(ticks!=1) return(rates_total);

double DC, MedianDelta;

Comment(tickCnt[0]);

if(prev_calculated==0 || tickCnt[0]==1)

{

int nLimit=rates_total-prev_calculated-1;

ArraySetAsSeries(high,true);

ArraySetAsSeries(low,true);

ArrayResize(Smooth,Bars(_Symbol,_Period));

ArrayResize(Cycle,Bars(_Symbol,_Period));

ArrayResize(CyclePeriod,Bars(_Symbol,_Period));

ArrayResize(InstPeriod,Bars(_Symbol,_Period));

ArrayResize(Q1,Bars(_Symbol,_Period));

ArrayResize(I1,Bars(_Symbol,_Period));

ArrayResize(DeltaPhase,Bars(_Symbol,_Period));

if (nLimit>rates_total-7)

nLimit=rates_total-7;

for(i=nLimit;i>=0 && !IsStopped();i--)

{

Smooth[i] = (Price(i)+2*Price(i+1)+2*Price(i+2)+Price(i+3))/6.0;

if (i<rates_total-7)

{

Cycle[i] = (1.0-0.5*InpAlpha) * (1.0-0.5*InpAlpha) * (Smooth[i]-2.0*Smooth[i+1]+Smooth[i+2])

+2.0*(1.0-InpAlpha)*Cycle[i+1]-(1.0-InpAlpha)*(1.0-InpAlpha)*Cycle[i+2];

} else

{

Cycle[i]=(Price(i)-2.0*Price(i+1)+Price(i+2))/4.0;

}

Q1[i] = (0.0962*Cycle[i]+0.5769*Cycle[i+2]-0.5769*Cycle[i+4]-0.0962*Cycle[i+6])*(0.5+0.08*InstPeriod[i+1]);

I1[i] = Cycle[i+3];

if (Q1[i]!=0.0 && Q1[i+1]!=0.0)

DeltaPhase[i] = (I1[i]/Q1[i]-I1[i+1]/Q1[i+1])/(1.0+I1[i]*I1[i+1]/(Q1[i]*Q1[i+1]));

if (DeltaPhase[i] < 0.1)

DeltaPhase[i] = 0.1;

if (DeltaPhase[i] > 0.9)

DeltaPhase[i] = 0.9;

MedianDelta = Median(DeltaPhase, i, 5);

if (MedianDelta == 0.0)

DC = 15.0;

else

DC = (6.28318/MedianDelta) + 0.5;

InstPeriod[i] = 0.33 * DC + 0.67 * InstPeriod[i+1];

CyclePeriod[i] = 0.15 * InstPeriod[i] + 0.85 * CyclePeriod[i+1];

Trigger[i] = CyclePeriod[i+1];

}

}

return(rates_total);

}

double Median(double& arr[], int idx, int m_len)

{

double MedianArr[];

int copied;

double result = 0.0;

ArraySetAsSeries(MedianArr, true);

ArrayResize(MedianArr, m_len);

copied = ArrayCopy(MedianArr, arr, 0, idx, m_len);

if (copied == m_len)

{

ArraySort(MedianArr);

if (m_len %2 == 0)

result = (MedianArr[m_len/2] + MedianArr[(m_len/2)+1])/2.0;

else

result = MedianArr[m_len / 2];

}

else Print(__FILE__+__FUNCTION__+"median error - wrong number of elements copied.");

return result;

}