I thought I would start a new thread for this one as it’s a little different and keeps things a bit more organised. Ok Nicolas?

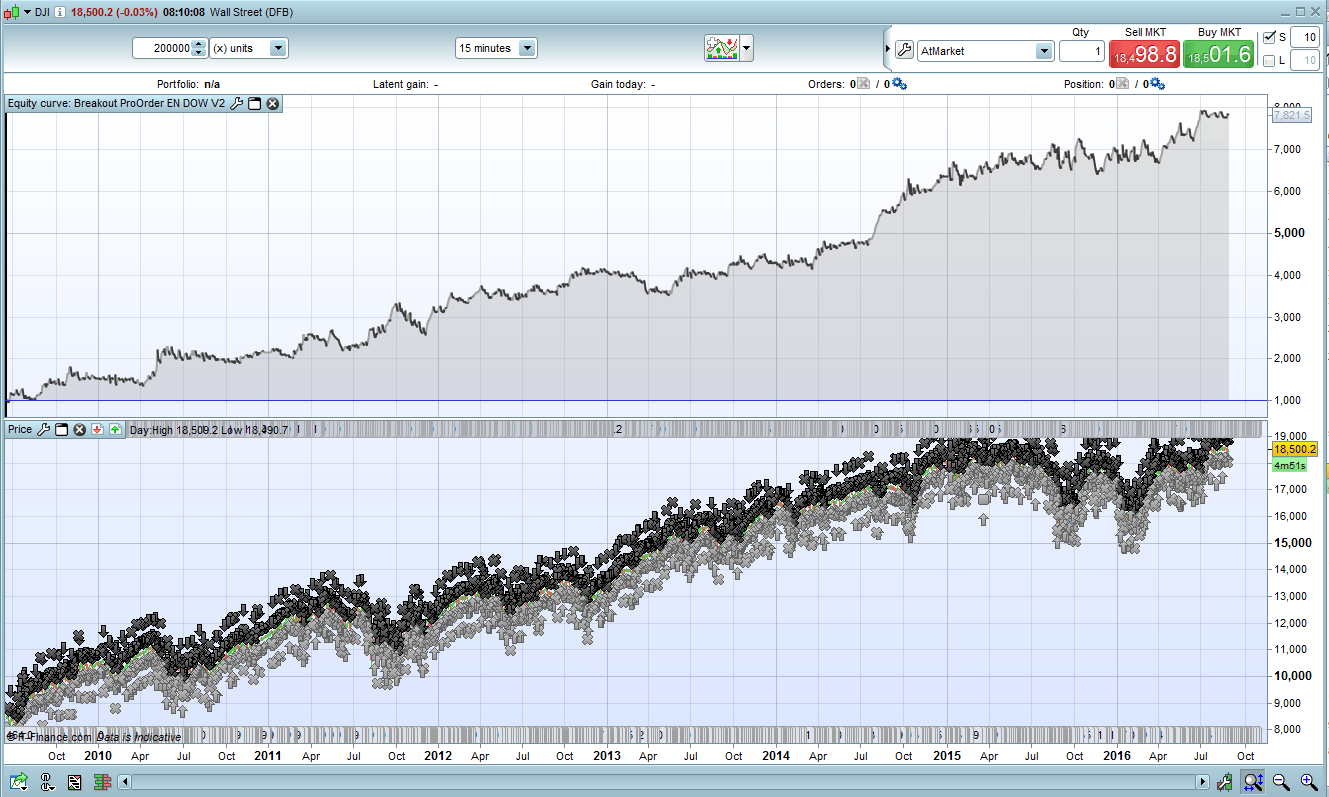

The DOW did not seem to like the first 30min breakout. This had me stuck for a while so I tried a few different things. It prefers the first hour BUT we exclude the first 15min candle.

Optimised to June 2014 IN/OUT Sample

£1pp Fixed position size. £1000 starting capital. 1.8 Spread.

Let me know your thoughts or if we can improve further.

// We do not store datas until the system starts.

// If it is the first day that the system is launched and if it is afternoon,

// it will be waiting until the next day for defining sell and buy orders

//UK TIME ZONE

DEFPARAM PreLoadBars = 0

// Position is closed at 20:30

DEFPARAM FlatAfter = 203000

// No new position will be initiated after the 19:45 candlestick

LimitHour = 200000

// Market scan begin with the 15 minute candlestick that closed at 15:30

StartHour = 151500

// The 24th and 31th days of December will not be traded because market close before 7h45 PM

IF (Month = 5 AND Day = 1) OR (Month = 12 AND (Day = 24 OR Day = 25 OR Day = 26 OR Day = 30 OR Day = 31)) THEN

TradingDay = 0

ELSE

TradingDay = 1

ENDIF

// Variables that would be adapted to your preferences

if time = 144500 then

//PositionSize = max(2,2+ROUND((strategyprofit-1000)/1000)) //gain re-invest trade volume

PositionSize = 1 //constant trade volume over the time

endif

MaxAmplitude = 160

MinAmplitude = 20

OrderDistance = 4

PourcentageMin = 35

// Variable initilization once at system start

ONCE StartTradingDay = -1

// Variables that can change in intraday are initiliazed

// at first bar on each new day

IF (Time <= StartHour AND StartTradingDay <> 0) OR IntradayBarIndex = 0 THEN

BuyTreshold = 0

SellTreshold = 0

BuyPosition = 0

SellPosition = 0

StartTradingDay = 0

ELSIF Time >= StartHour AND StartTradingDay = 0 AND TradingDay = 1 THEN

// We store the first trading day bar index

DayStartIndex = IntradayBarIndex

StartTradingDay = 1

ELSIF StartTradingDay = 1 AND Time <= LimitHour THEN

// For each trading day, we define each 15 minutes

// the higher and lower price value of the instrument since StartHour

// until the buy and sell tresholds are not defined

IF BuyTreshold = 0 OR SellTreshold = 0 THEN

HighLevel = Highest[IntradayBarIndex - DayStartIndex + 2](High)

LowLevel = Lowest [IntradayBarIndex - DayStartIndex + 2](Low)

// Spread calculation between the higher and the

// lower value of the instrument since StartHour

DaySpread = HighLevel - LowLevel

// Minimal spread calculation allowed to consider a significant price breakout

// of the higher and lower value

MinSpread = DaySpread * PourcentageMin / 100

// Buy and sell tresholds for the actual if conditions are met

IF DaySpread <= MaxAmplitude THEN

IF SellTreshold = 0 AND (Close - LowLevel) >= MinSpread THEN

SellTreshold = LowLevel + OrderDistance

ENDIF

IF BuyTreshold = 0 AND (HighLevel - Close) >= MinSpread THEN

BuyTreshold = HighLevel - OrderDistance

ENDIF

ENDIF

ENDIF

// Creation of the buy and sell orders for the day

// if the conditions are met

IF SellTreshold > 0 AND BuyTreshold > 0 AND (BuyTreshold - SellTreshold) >= MinAmplitude THEN

IF BuyPosition = 0 THEN

IF LongOnMarket THEN

BuyPosition = 1

ELSE

BUY PositionSize CONTRACT AT BuyTreshold STOP

ENDIF

ENDIF

IF SellPosition = 0 THEN

IF ShortOnMarket THEN

SellPosition = 1

ELSE

SELLSHORT PositionSize CONTRACT AT SellTreshold STOP

ENDIF

ENDIF

ENDIF

ENDIF

// Conditions definitions to exit market when a buy or sell order is already launched

IF LongOnMarket AND ((Time <= LimitHour AND SellPosition = 1) OR Time > LimitHour) THEN

SELL AT SellTreshold STOP

ELSIF ShortOnMarket AND ((Time <= LimitHour AND BuyPosition = 1) OR Time > LimitHour) THEN

EXITSHORT AT BuyTreshold STOP

ENDIF

// Maximal risk definition of loss per position

// in case of bad evolution of the instrument price

SET STOP PLOSS MaxAmplitude

//set target pprofit //70 //160

Don’t worry, I like things organised too 🙂

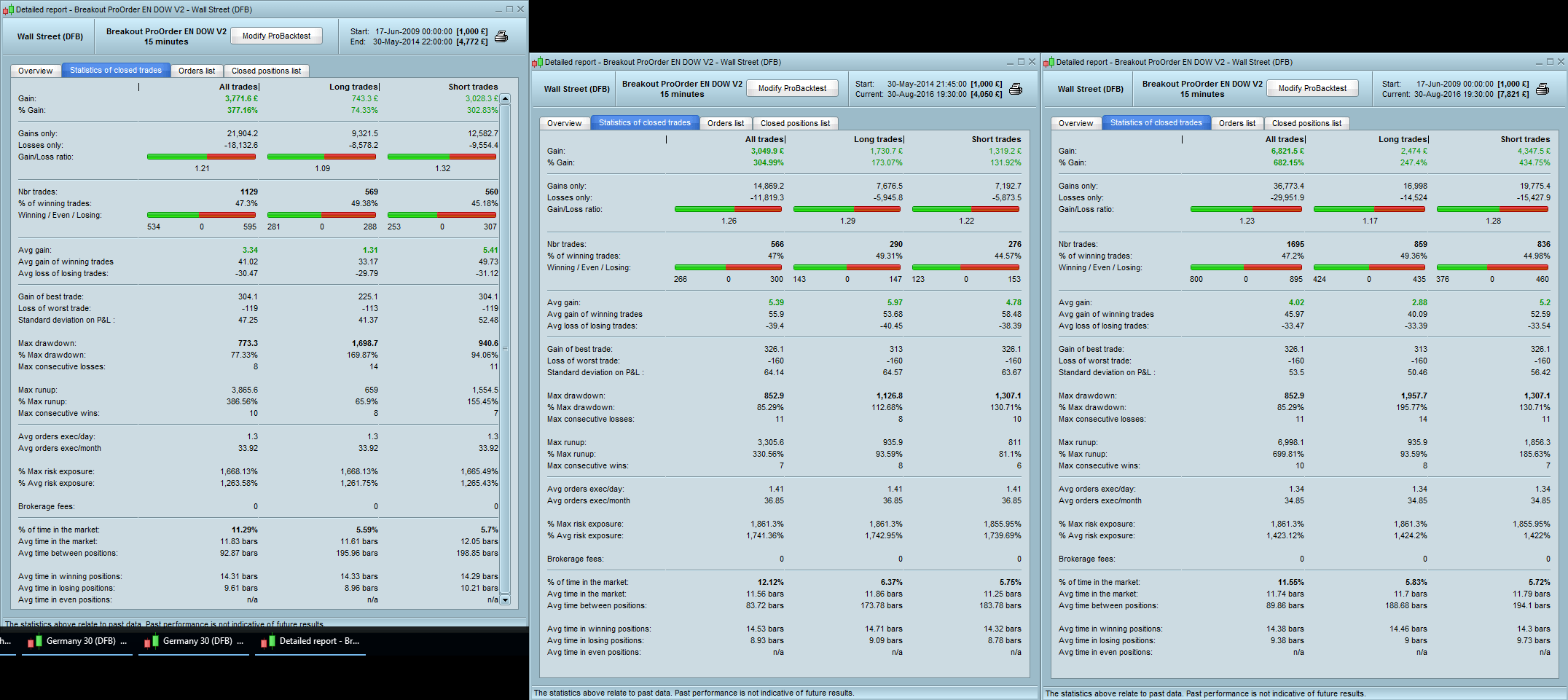

Thanks for this new version of the now famous breakout strategy! To have a better clue if the optimized OOS area have the same behaviour of the IS one, you can make a comparison of how much average trades you have on the 2 samples. Once you get that, you can also have a look on trades symmetry comparison : BUY quantity vs SELL quantity ratio.

I will leave this here to compare later.

Well, the trades symmetry seems good between OOS and IS (the first 2 screenshots on the left), the average buy gain is higher though, I believe it is due to 2015 bullish rally on whole indices. Maybe you could test only 2015 period to see what happen between long and short average gain. Good job Cosmic1!