In September a human would be trading short. There were only 2 short long phases, otherwise it would be a short month. The short longs were not enough to trigger a TP. There is the solution.

A solution might be an additional slower MA size EMA100 or something similar.

Breakouts in H4 over candles with long top shadow don’t seem to be that good … how can you code candles with long top shadow? Then you could check it out.

you could try

shadow = (high-close)/(high-low) < s

s value > 0.5 means the top shadow is more than half the candle

add shadow as an entry condition

optimize ‘s’ from 0.1 to 1 in steps of 0.1

Thank you, I’ll try tonight.

To see the max amount of CumulateOrders in backtest:

Once MaxOrders = 0

MaxOrders = max(MaxOrders,abs(CountOfPosition))

Graph MaxOrders

edited: CountOfPosition was badly spelled and has been corrected at a later time

As a quick train of thought, in case I’m wrong … the 1 Trade function via H4 bar is built into my version. So if I calculate TP / SL in the M5 over the entire period and then simply switch to an M1 chart and calculate the trailing stop there … We have a system that triggers 1 trade per H4 bar in the M1 with the SL / TP in the M5 Timeframe works well and the trailing stop in the M1 … all months with greater profit / less drawdown than in the M5 chart … without September problems. 😉 Do I understand this logic correctly? Because then the system is damn good without cummulate = true.

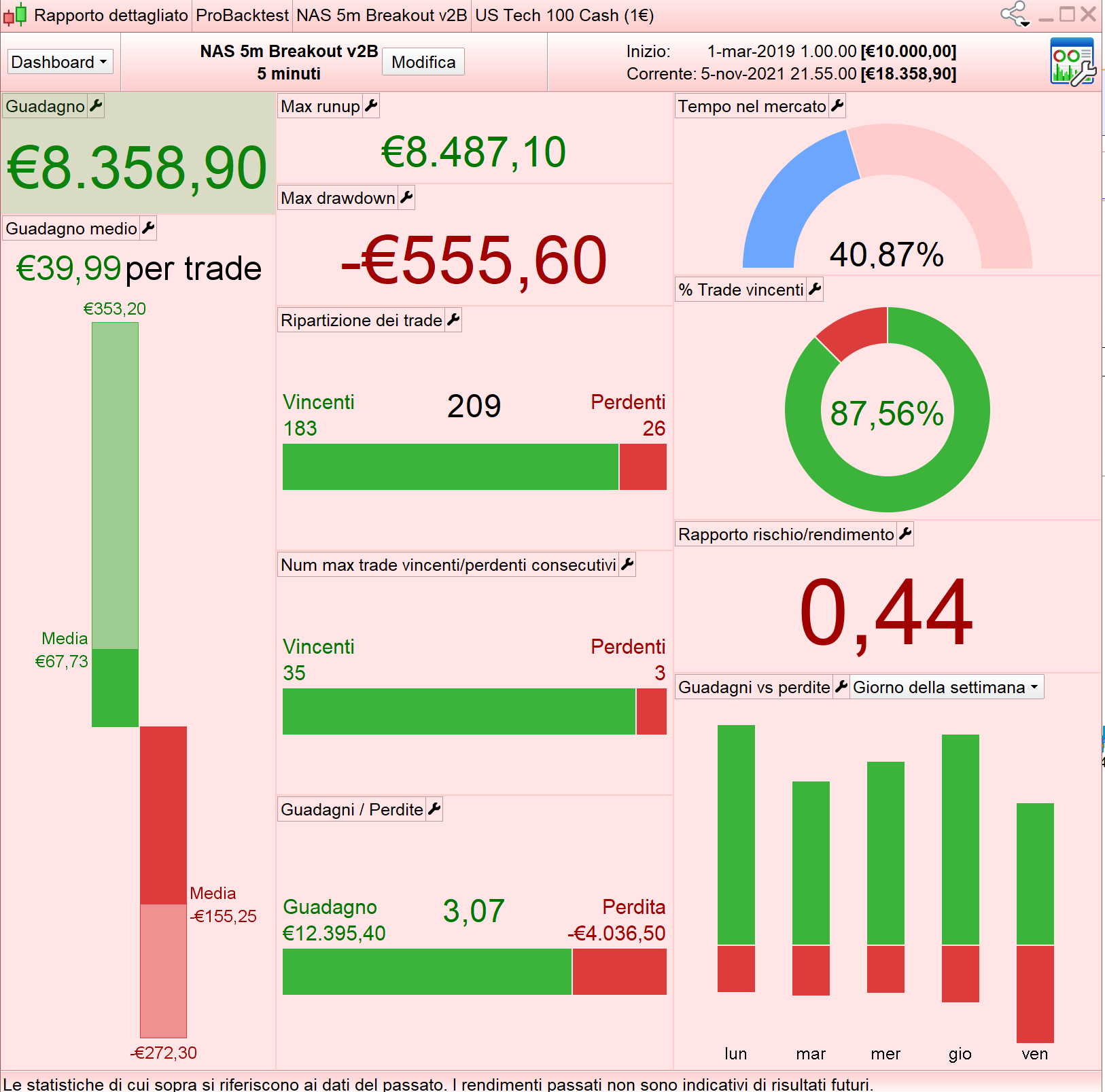

This is essentially the version 2 of Nonetheless with 1 contract. I have changed only TradeTime (from 120000 to 130000) and added a filter with a second moving averages (optimized). This version has a lower DD than version 2 (tested on 200K).

//TS NAS 5m Breakout v2B

DEFPARAM CUMULATEORDERS = false

//spread = 1.5

positionsize = 1

Tradetime = time >=130000 and time <220000

//——————————————————-

timeframe(4 hour, updateonclose)

H4 = high

avg1 = average[40,6](close)

c1 = avg1 > avg1[1] //filter

avg2 = average[110,2](close)

c2 = close > avg2 //new filter II

//——————————————————–

timeframe(5 minutes)

c0 = close crosses over H4 // trigger

If Tradetime and c0 and c1 and c2 Then

Buy PositionSize CONTRACTS AT MARKET

SET STOP %LOSS 1.8

SET TARGET %PROFIT 2.2

ENDIF

//——————————————————-

once trailingStop = 1

If trailingStop then

trailingPercentLong = 0.39

once acceleratorLong = 0.015

once stepPercentLong = (trailingPercentLong/10)*acceleratorLong

If onMarket then

trailingStartLong = positionprice*(trailingPercentLong/100)

trailingsteplong = positionprice*(stepPercentLong/100)

endif

IF NOT ONMARKET THEN

newSL=0

ENDIF

IF LONGONMARKET THEN

IF newSL=0 AND high-tradePrice(1)>=trailingStartLong THEN

newSL = tradePrice(1)+trailingStepLong

ENDIF

IF newSL>0 AND high-newSL>trailingStepLong THEN

newSL = newSL+trailingStepLong

ENDIF

ENDIF

IF newSL>0 THEN

SELL AT newSL STOP

ENDIF

ENDIF

//——————————————————————————————-

RSIexit = 1

if RSIexit then

myrsi=rsi[9](close)

if myrsi<10 and barindex-tradeindex>1 and longonmarket and close>positionprice then

sell at market

endif

if myrsi>85 and barindex-tradeindex>1 and shortonmarket and close<positionprice then

exitshort at market

endif

endif

//—————————————————————————————————-

EZT = 1

if EZT then

IF (longonmarket and barindex-tradeindex(1)>= 1590 and positionperf>0) or (longonmarket and barindex-tradeindex(1)>= 1390 and positionperf<0) then

sell at market

endif

IF (shortonmarket and barindex-tradeindex(1)>= 3500 and positionperf>0) or (shortonmarket and barindex-tradeindex(1)>= 3500 and positionperf<0) then

exitshort at market

endif

endif

//———————————————————————————————————

How does your version with “1 Trade function via H4 bar” phoentzs conpares to MauroPro TS NAS 5m Breakout v2B?

How do I use tradeon. When I use it like below the results no different.

timeframe(4 hour, updateonclose)

H4 = high

avg1 = average[40,6](close)

c1 = avg1 > avg1[1] //filter

avg2 = average[110,2](close)

c2 = close > avg2 //new filter II

barCount = barIndex

//——————————————————–

timeframe(5 minutes)

once tradeOn = 1

if intradayBarIndex = 0 then

tradeOn = 1

endif

tradeBar = barCount

if not onMarket and tradeBar<>tradeBar[1] then

tradeOn = 1

endif

c0 = close crosses over H4 // trigger

If Tradetime and c0 and c1 and c2 and tradeon Then

Buy PositionSize CONTRACTS AT MARKET

SET STOP %LOSS 1.8

SET TARGET %PROFIT 2.2

ENDIF

//——————————————————-

Under line 22: TRADEON = 0

My version has advantages with the additional MA in some market phases, but in sideways phases also disadvantages. So I do not use it first. Besides, I tested average (40.6) and average (15.1) with my “small” SL settings. There is the advantage of average (15.1). This becomes particularly clear if you only test with SL / TP for over 8 years. Conclusion: I think EMA15 is not over-optimized. My modest opinion, but only because I do not like a huge SL. I can fool myself, I’m just apprentice as we all.

we change easily into a M3 chart with the same settings TP / SL only … we see the faster reaction of M3 bars over M5-bars is a great improvement.

How does ur version look like I code phoentzs