@nonethless What do you think of Highest high 2 as an outbreak in H4? So a Donchian 2?

you could try it, but I think it will just delay the opening and buy at a worse price.

might make sense with a shorter TF but a new 4 hour high, in conjunction with the rising MA, is a fairly significant move by itself – you can see that it works!

With my own possibilities, I cannot come up with a better result than yours. I’ll switch the system to demo.

Can you please explain to me how your trailing stop works? I usually use Nicolas Code with pips.

Is the minimum distance from the broker missing for the trailing stop? At least I can’t find any. Or does this stop not need one?

the trailing stop I use is Paul’s work (which I think was based on Nicolas’s)

the main difference is that it works with cumulative orders true or false

It also has a more subtle way of calculating the trailing step, and a choice of how to trigger it (close, high, low, typicalprice)

Both the start and the step are in percentages, in this case it goes to breakeven at 0.39% – approx 64 points. This is unusually high but it seems to work, normal setting would be between 0.2 – 0.3%

I have mine on demo, opened a trade yesterday, still in play.

The stop itself doesn’t need a min distance, but tick the box for ‘Readjust stops’ when you launch it.

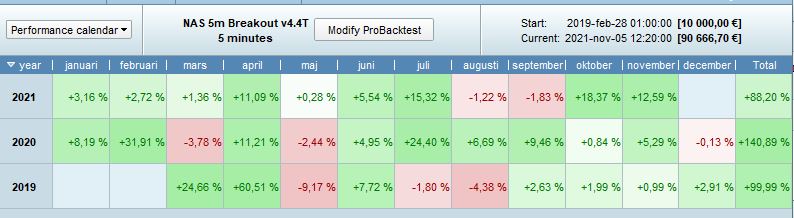

Wow. Interesting algo. For all strategies september 2021 seems to be very tuff to get by without losing money.

A short version of this setup would be interesting.

Unfortunately, I cannot afford version V4.4T. 😉 It is good to see, however, that there are no unforeseen events and that the principle therefore works well. I tested the V2 on the M15 yesterday to have a longer test period … and it works. Even if I still prefer EMA15 in the H4.

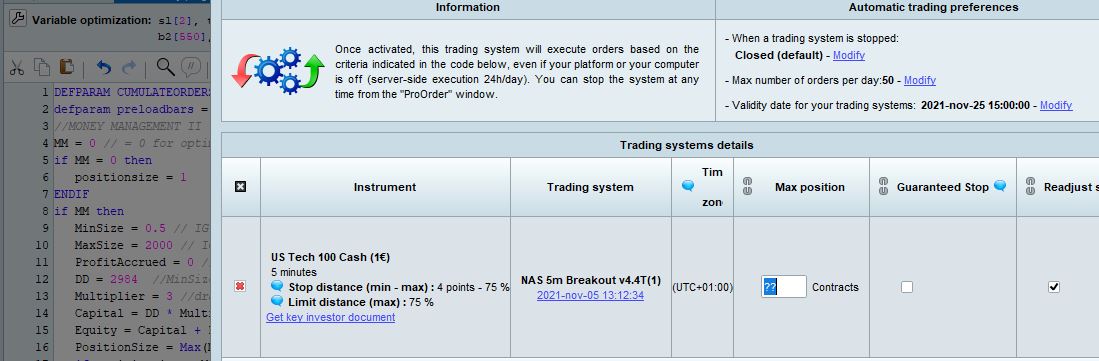

One questing. What do i write in “max position” when code has “DEFPARAM CUMULATEORDERS = true”

See attached picture

Even if I still prefer EMA15

Hmm, why would you prefer it when it works less well? Irrational bias is disastrous in this game!

as for the v4.4, some people are put off by cumulative orders but potential rewards are so much greater. All my best algos use it, but you have to really trust your entry conditions.

In this case, the drawdown looks high, but relative to the max runup it’s not that bad. My rule of thumb is to have a minimum ratio of 10:1 between those two

sorry. Wrong picture. Yes I meant when MM=1 and:

if MM then

MinSize = 0.5 // IG minimum position size allowed

MaxSize = 2000 // IG tier 2 margin limit

ProfitAccrued = 0 // when restarting strategy, enter profit or loss to date in instrument currency

DD = 2984 //MinSize drawdown in instrument currency

Multiplier = 3 //drawdown multiplier

Capital = DD * Multiplier

Equity = Capital + ProfitAccrued + StrategyProfit

PositionSize = Max(MinSize, Equity * (MinSize/Capital))

if positionsize > MaxSize then

positionsize = MaxSize

endif

PositionSize = Round(PositionSize*100)

PositionSize = PositionSize/100

ENDIF

actually for demo purposes you can put any large number for max positions, like 200 or 2000 – you wont get anywhere near that so it doesn’t matter.

Note that the MM works on the ratio between Minsize and DD. So in this case, if you want to start with Minsize = 1, you should also put DD = 5968

The Multiplier controls how fast positionsize will increase. 3 is fairly safe, I sometimes use 2 … depends on your attitude to risk.

Can you incorporate the function that only one trade is possible every 4 hours? So only the first cross counts? I can code one trade a day, but once every 4 hours?

do you mean with cumulative orders? so each cross above the 4h candle opens another position?