My guess is that you ran in to the same problem I did. If you have too high start, base and increase (in some combination), it becomes a trailing take profit after an increase.

Im running 3M timeframe. Is There a range a values thats i not should use i combination?

Would u like to give an example?

It seems a always loose profit bacuse tp/sl move too slow.

This system is wallstreet 15 min

StartPerCentLong = 0.6

StepPerCent = 30

BasePerCent = 0.2

PerCentInc = 0.1

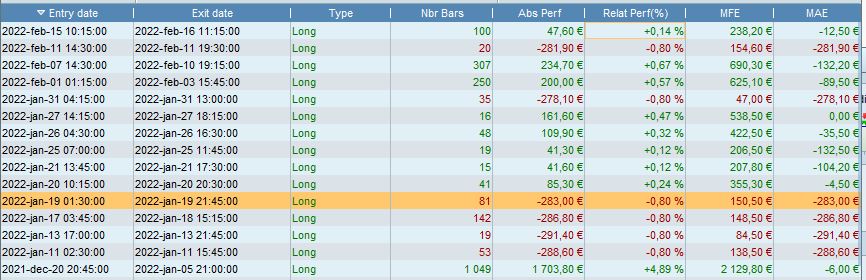

Se attached picture how system got big gain MFE.

The trail has to move slowly enough to allow it, at least occasionally, to reach the target. It’s the only way you can offset the fact that it will also, occasionally, go all the way to the Stop.

If you want to take lots of small profits, you would have to have a fairly small SL … which means lots of small losses as well.

I find that Roberto’s trail generally moves more quickly and captures more MFE than most (compared to % or ATR), but it’s all in the settings.

You can make it go faster if you want, but you won’t necessarily get a better result.

I didn’t follow the discussion from the begining. I see from your 17 Feb. post that you’re running DJ on 15 min TF. If all your code is run on a 15 min chart then your Trailing System will update the SL/TP, etc. every 15 min… depending on the volatility, many things can happen in 15 min including losing all your profits or even worse going from +100pts to -100pts (on DJ it’s very easy). If this 15 min graph assumption is correct, then you might want to try to run your trailing system on 1 min TF and keep the rest on 15 min TF and put everything on 1 min chart. In this case, the Trailing System will update every minute and you can capture more profits before retracement.

TIMEFRAME(15minutes)

Indicator1

Indicator2

Indicator3

Condition1

Condition2

Condition3

If ... THEN

Buy/SellShort

ENDIF

TIMEFRAME(1 minute)

Trailing system

I think that’s the mindset most use… A larger time frame for the signal and entry and a much smaller time frame for the trailing stop.

phoentzs

Hello phoentzs

I’m keen to explore this notion further on PRT, I have used shorter timeframes on other platforms but not on PRT. My understanding though is that the timeframe that the algo runs on is the lowest you can go down to. So if it runs on a 15min chart then the algo cannot be 5 or 1 min. I find this frustrating as I’m forced to use other options which aren’t as good.

How do you solve for this please? Thanks very much

samsampop if you use TIMEFRAME(15 minutes, updateonclose) on a 1 min chart, it should give you the same result than TIMEFRAME(15 minutes, updateonclose) on a 15 min chart.

thanked this post

So if it runs on a 15min chart then the algo cannot be 5 or 1 min

15min, 5min, 3min and 1 min can be combined in the same Algo.

15min and 4 min cannot be combined in the same Algo … due to 15min not divisible by 4 (min) ).

thanked this post

What samsampop wants to achieve is to have a 15-minute chart displayed, with the strategy using ALSO 1-miute, or 5-minute, timeframes.

This is not possible as the PRT platform executes strategies when a bar closes, so it would still access the 1-minute or 5-minute code only once every 15 minutes!

thanked this post

Bonjour Mr robertogozzi

merci pour votre création de break even que j’utilise dans mes algo.

J’ai remarqué que lorsque mon trade est parti et qu’il arrive au TrailStart défini à 10 par exemple il redescend et mon stop n’ai pas monté. Est ce que c’est normal ? Je crois comprendre que le stop sera remonté à la cloture de la bougie avec votre formule c’est bien ca?

Je voudrais pouvoir le déplacer en cours de bougie est ce possible parce que je m’aperçois que je rate beaucoup de tardes .

Dans l’attente de vous lire

merci encore.

Hello Mr robertogozzi thank you for your creation of break even that I use in my algo. I noticed that when my trade left and it arrives at the TrailStart defined at 10 for example it goes down and my stop did not go up. Is it normal ? I understand that the stop will be raised to the close of the candle with your formula is that right? I would like to be able to move it during the candle, is this possible because I realize that I miss a lot of delays. Looking forward to reading from you, thank you again.

@Marlaynicolas

Only post in the language of the forumthat you are posting in. For example English only in the English speaking forums and French only in the French speaking forums,

Thank you 🙂

@Marlaynicolas

strategies are only executed at the closing of each candle, but you can take advantage of the Multi Time Frame support to use a lower TF, such as 5 minutes or 1 minute.

Hi Roberto.

This morning my SL was a secured win. Then market moved in a favoured direction and trailinprofit apered,but now SL is not secured win any more.

I would like SL to stay secured win. How can i do this?

SPCL=0.65

SPCS=0.14

SPC=1.7

BPC=0.08

PCI=0.1

//------------------------------------------------------------------------------------------------------------------------------------------------

// Trailing Start

//------------------------------------------------------------------------------------------------------------------------------------------------

If trail then

DirectionSwitch = (LongOnMarket AND ShortOnMarket[1]) OR (LongOnMarket[1] AND ShortOnMarket) //True when there's been a change in the direction (likely to be due to a Stop & Reverse)

//

IF Not OnMarket OR DirectionSwitch THEN

//

// when NOT OnMarket or thare's been a change in direction, reset values to their default settings

//

StartPerCentLong = SPCL //0.25% to start triggering Trailing Stop

StartPerCentShort = SPCS

StepPerCent = SPC //50% (of the 0.25% above) as a Trailing Step (set to 100 to make StepSize=TrailStart, set to 200 to make it twice TrailStart)

BasePerCent = BPC //0.1-1 Profit percentage to keep when setting BreakEven

PerCentInc = PCI // 0.1-1 PerCent increment after each StepSize chunk

//

TrailStartLong = (close / PipSize) * StartPerCentLong / 100 //use current price (CLOSE) for calculations

TrailStartShort = (close / PipSize) * StartPerCentShort / 100 //use current price (CLOSE) for calculations

StepSizeLong = TrailStartLong * StepPerCent / 100

StepSizeShort = TrailStartShort * StepPerCent / 100

//

RoundTO = -0.5 //-0.5 rounds always to Lower integer, +0.4 rounds always to Higher integer, 0 defaults PRT behaviour

PriceDistance = 8 * pipsize //7 minimun distance from current price

y1 = 0 //reset to 0

y2 = 0 //reset to 0

ProfitPerCent = BasePerCent //reset to desired default value

//PositionCount = 0

SellPrice = 0

SellPriceX = 0

ExitPrice = 9999999

ExitPriceX = 9999999

ELSE

//------------------------------------------------------

// --- Update Stop Loss after accumulating new positions

//------------------------------------------------------

//PositionCount = max(PositionCount,abs(CountOfPosition))

//

// update Stop Loss only when PositionPrice has changed (actually when increased, we don't move it if there's been some positions exited)

//

//IF PositionCount <> PositionCount[1] AND (ExitPrice + SellPrice)<>9999999 THEN //go on only if Trailing Stop had already started trailing

IF PositionPrice <> PositionPrice[1] AND (ExitPrice + SellPrice) <> 9999999 THEN //go on only if Trailing Stop had already started trailing

IF LongOnMarket THEN

q1 = PositionPrice + ((Close - PositionPrice) * ProfitPerCent) //calculate new SL

SellPriceX = max(max(SellPriceX,SellPrice),q1)

SellPrice = max(max(SellPriceX,SellPrice),PositionPrice + (y1 * pipsize)) //set exit price to whatever grants greater profits, comopared to the previous one

ELSIF ShortOnMarket THEN

r1 = PositionPrice - ((PositionPrice - Close) * ProfitPerCent) //calculate new SL

ExitPriceX = min(min(ExitPriceX,ExitPrice),r1)

ExitPrice = min(min(ExitPriceX,ExitPrice),PositionPrice - (y2 * pipsize)) //set exit price to whatever grants greater profits, comopared to the previous one

ENDIF

ENDIF

// --- Update END

ENDIF

//

IF LongOnMarket AND Close > (PositionPrice + (y1 * pipsize)) THEN //LONG positions

//

// compute the value of the Percentage of profits, if any, to lock in for LONG trades

//

x1 = (Close - PositionPrice) / pipsize //convert price to pips

IF x1 >= TrailStartLong THEN // go ahead only if N+ pips

Diff1 = abs(TrailStartLong - x1) //difference from current profit and TrailStart

Chunks1 = max(0,round((Diff1 / StepSizeLong) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks1 * PerCentInc)) //compute new size of ProfitPerCent

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y1 = max(x1 * ProfitPerCent, y1) //y1 = % of max profit

ENDIF

ELSIF ShortOnMarket AND Close < (PositionPrice - (y2 * pipsize)) THEN //SHORT positions

//

// compute the value of the Percentage of profits, if any, to lock in for SHORT trades

//

x2 = (PositionPrice - Close) / pipsize //convert price to pips

IF x2 >= TrailStartShort THEN // go ahead only if N+ pips

Diff2 = abs(TrailStartShort - x2) //difference from current profit and TrailStart

Chunks2 = max(0,round((Diff2 / StepSizeShort) + RoundTO)) //number of STEPSIZE chunks

ProfitPerCent = BasePerCent + (BasePerCent * (Chunks2 * PerCentInc)) //compute new size of ProfitPerCent

ProfitPerCent = max(ProfitPerCent[1],min(100,ProfitPerCent)) //make sure ProfitPerCent doess not exceed 100%

y2 = max(x2 * ProfitPerCent, y2) //y2 = % of max profit

ENDIF

ENDIF

//------------------------------------------------------------------------------

// manage actual Exit, if needed

//------------------------------------------------------------------------------

IF y1 THEN //Place pending STOP order when y1 > 0 (LONG positions)

SellPrice = max(SellPrice,PositionPrice + (y1 * pipsize)) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - SellPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close >= SellPrice THEN

SELL AT SellPrice STOP

ELSE

SELL AT SellPrice LIMIT

ENDIF

ELSE

//

//sell AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

SELL AT Market

ENDIF

ENDIF

IF y2 THEN //Place pending STOP order when y2 > 0 (SHORT positions)

ExitPrice = min(ExitPrice,PositionPrice - (y2 * pipsize)) //convert pips to price

//

// check the minimun distance between ExitPrice and current price

//

IF abs(close - ExitPrice) > PriceDistance THEN

//

// place either a LIMIT or STOP pending order according to current price positioning

//

IF close <= ExitPrice THEN

EXITSHORT AT ExitPrice STOP

ELSE

EXITSHORT AT ExitPrice LIMIT

ENDIF

ELSE

//

//ExitShort AT MARKET when EXITPRICE does not meet the broker's minimun distance from current price

//

EXITSHORT AT Market

ENDIF

ENDIF

Endif

Please post a working code with the details about the timeframe and istrument used and the candle where the incorrect trade started.

Hi @robertogozzi,

Is there a formula of what StepPerCent, PerCentInc and BasePerCent can be max?

I’ve noticed that some combinations overshoots the price and becomes a target instead of a trailing stop.

StepPerCent = 50

BasePerCent = 0.5

PerCentInc = 0.5

works

StepPerCent = 10

BasePerCent = 0.5

PerCentInc = 0.5

overshoots

StepPerCent = 25

BasePerCent = 0.5

PerCentInc = 0.2

works

StepPerCent = 10

BasePerCent = 0.5

PerCentInc = 0.2

overshoots

StepPerCent = 80

BasePerCent = 0.6

PerCentInc = 0.6

works

StepPerCent = 20

BasePerCent = 0.6

PerCentInc = 0.6

overshoots