Bard

BardParticipant

Master

I was interested in generating a random entry code to test an optimised version of the Kase Dev Stop (KDS) exits and see if my entries on a system I have (that uses the KDS for exits) are better than random or as Trading World Cup champion Kevin Davey succinctly put it: better than a monkey throwing darts at a dart board!

(See page 109 of Building Winning Algorithmic Trading Systems by Kevin J Davey).

I used a random date generator: https://www.random.org/calendar-dates

I wanted to match the 19 trades my system took (7 long and 12 shorts) and randomly assigned some of these dates to go long so I have 7 long positions and the rest going short.

I need to code the entries correctly so it takes the trades on the dates provided by the random date generator. I used this code below but it’s not taking the 19 trades I need.

I also tried changing the AND to OR (between the StartDate code) without it working and also using conditionals like: “If date = StartDate3 AND StartDate6 then TradeLONG =1 and then using If TradeLONG =1 then Buy 10 etc but that didn’t work either?

Obviously you could write separate Buy and Sell lines with the specific StartDate code but that’s clumsy and time consuming, so any help appreciated.

I used the £/$ Daily between 22/10/2012 and 24/10/2018. It produced 51 trades, but on what criteria are all these 51 entries being made because it certainly isn’t the StartDates!?

Also is there a better way of generating random entry/exits because I didn’t understand this RSI based generator: https://www.prorealcode.com/topic/random-value/

Cheers

Bard

// Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

//RORom Dates

StartDate1 = 20131023

StartDate2 = 20130607

StartDate3 = 20130920

StartDate4 = 20131111

StartDate5 = 20141030

StartDate6 = 20150424

StartDate7 = 20150629

StartDate8 = 20150731

StartDate9 = 20150818

StartDate10 = 20150922

StartDate11 = 20151016

StartDate12 = 20151117

StartDate13 = 20160520

StartDate14 = 20170116

StartDate15 = 20170314

StartDate16 = 20170613

StartDate17 = 20180214

StartDate18 = 20180409

StartDate19 = 20180430

If TradingLONG = (opendate = StartDate3 OR StartDate6 OR StartDate8 OR StartDate9 OR StartDate14 OR StartDate18 OR StartDate19) Then

TradingLONG = 1

Endif

If TradingLONG = (opendate = StartDate1 OR StartDate2 OR StartDate4 OR StartDate5 OR StartDate7 OR StartDate10 OR StartDate11 OR StartDate12 OR StartDate13 OR StartDate14 OR StartDate15 OR StartDate16 AND StartDate17) Then

TradingLONG = 0

Endif

// Conditions to enter long positions

IF TradingLONG = 1 THEN

BUY 10 PERPOINT AT MARKET

ENDIF

// Conditions to exit long positions

ignored, ignored, ignored, Dev, ignored, ignored = CALL "Kase Dev Stop LisseSAR4.5/6OPT" [p3]

c1 = (close CROSSES UNDER Dev)

IF c1 THEN

SELL AT MARKET

ENDIF

/////////////////////////

// Conditions to enter short positions

IF TradingLONG = 0 THEN

SELLSHORT 10 PERPOINT AT MARKET

ENDIF

// Conditions to exit short positions

ignored, ignored, ignored, Dev, ignored, ignored = CALL "Kase Dev Stop LisseSAR4.5/6OPT" [p3]

c2 = (close CROSSES OVER Dev)

IF c2 THEN

EXITSHORT AT MARKET

ENDIF

Your trading conditions are wrongly syntaxed, you should test them like this:

TradingLONG = (opendate = StartDate3 OR opendate = StartDate6 OR opendate = StartDate8 OR ...... )

and make another variable but for TradingShort and the others StartDateX, like you did.

BardParticipant

Master

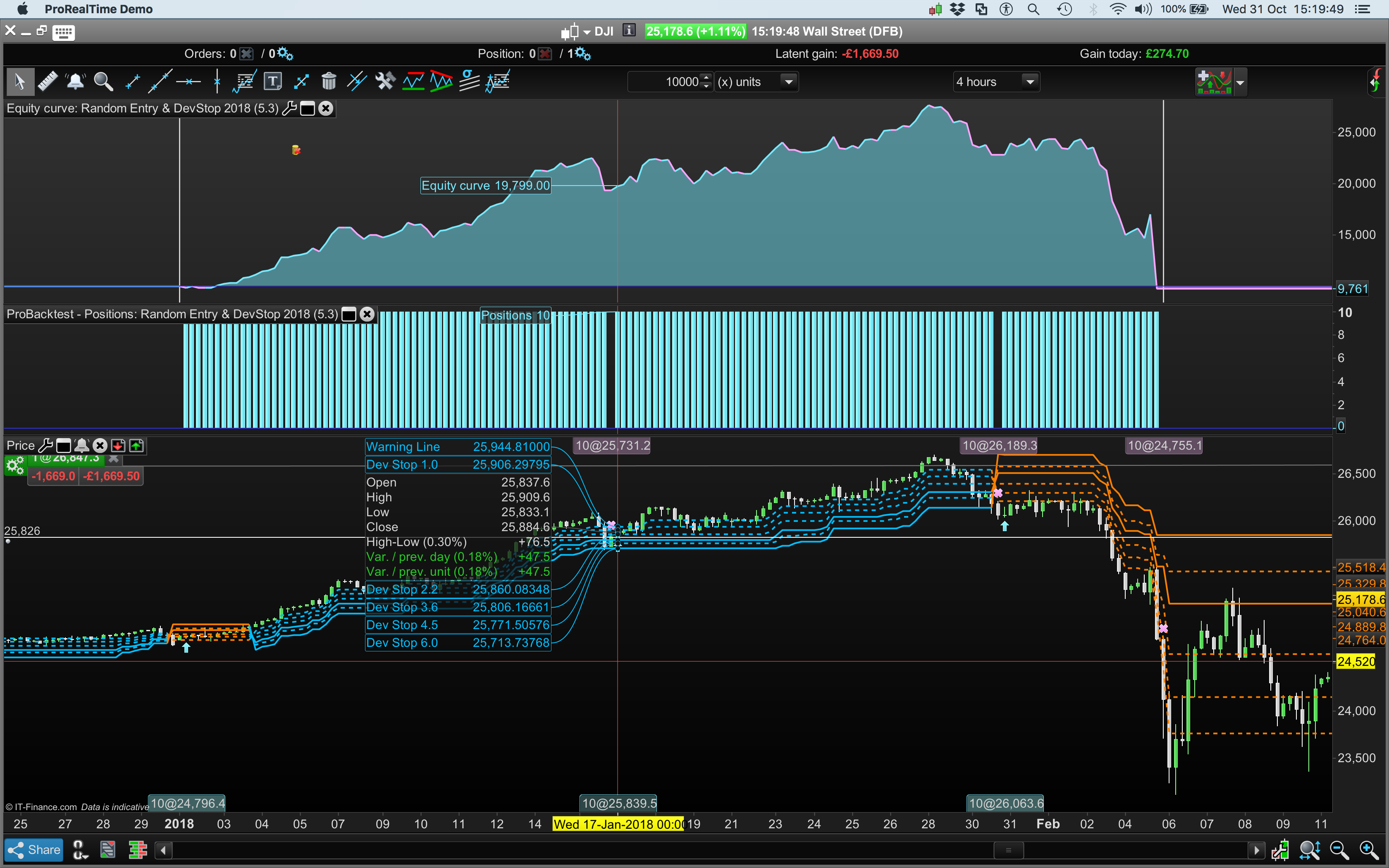

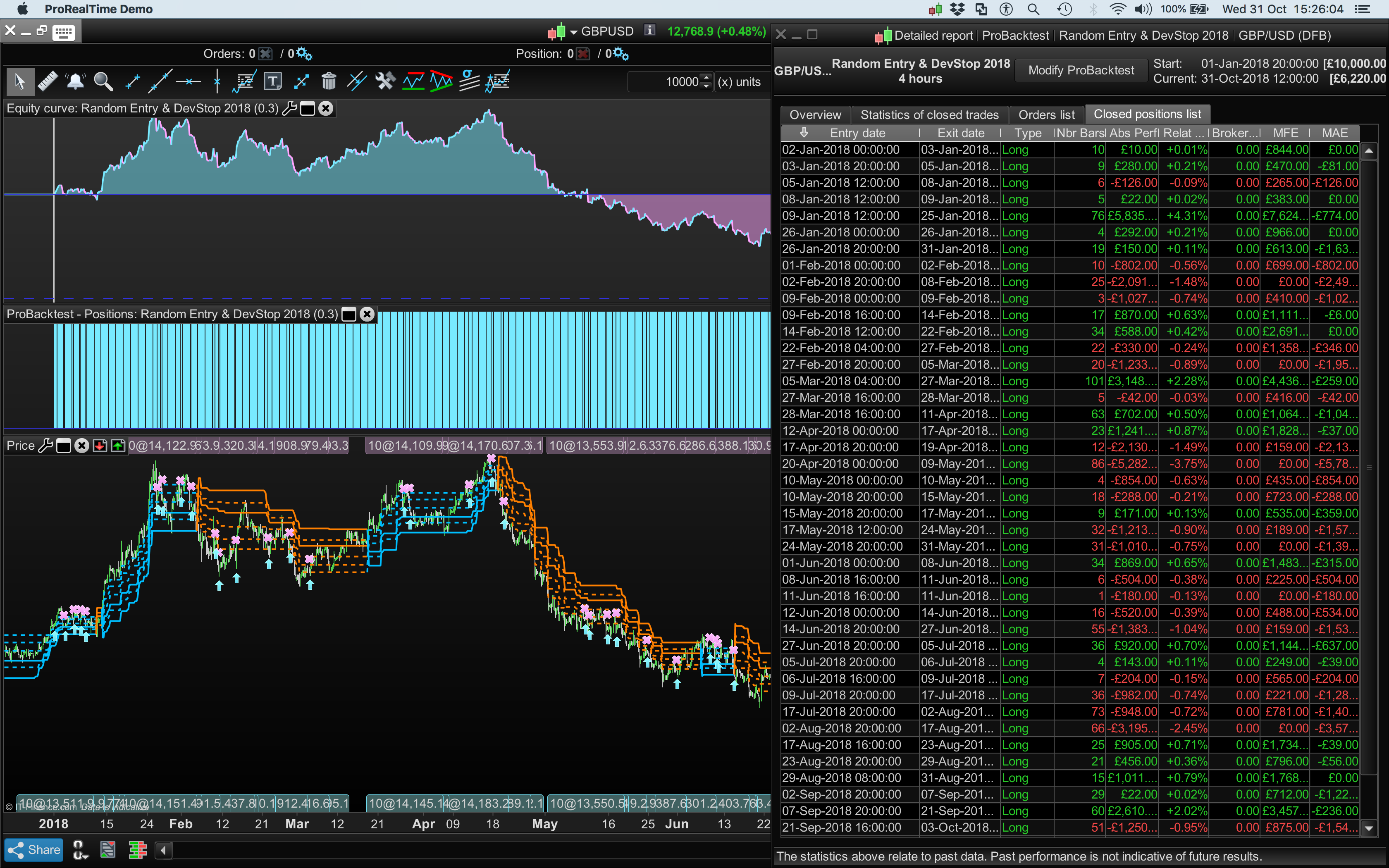

Cheers @nicolas, I’ve amended the code yet it takes positions on dates that don’t respect the opendate = StartDates as seen in these two screenshots below. The purpose of the code is to enter on random dates and ascertain the effectiveness of different exit strategies, in this case the Kase Dev Stops and the amount of standard deviations needed.

(The reason the Startdates are out of order in the TradeLONG / SHORT code is because I determined whether to go long or short by using a random number generator for the 25 trade dates: http://numbergenerator.org/randomnumberpicker#!numbers=25&low=1&high=25&unique=true&start=true)

Can you think of a better way to code random entries (or exits) particularly if you needed eg a 120 trades to match the amount of trades taken by a system so as to check the effectiveness of it’s exit strategy? Thanks.

BardParticipant

Master

Why has this code traded on the 17th Jan 2018 @Nicolas? (Pls see first image above). My random dates don’t include this date? They don’t even include January! Is there a better way to generate random trades?

Cheers

Bard

BardParticipant

Master

This code isn’t working, it’s not only trading on non specified days it’s trading on the wrong month?

Leo

LeoParticipant

Veteran

Hi.

You are creating a code for evaluate the performance in entries at random dates.

Then what? You create a system that entry in the market one of those days in the future?

For me it doesn’t have sense at all.

Just pick whatever strategy and then make an extra condition with a random value from 1 to 5 an add trade if dayofweek = randomvalue.

In any case you can not perform any Evaluation of your code in the past.

We have a thead somewhere that we were trying to make a code for trade totally random. There were many interesting conclusions

BardParticipant

Master

Hi @Leo, I want to compare my system that has an entry that uses an oscillator entry (the Kase Peak Osc. — used in conjunction with the Kase Dev Stop (KDS exit) with a random entry. Note: Entries can be tested in the similar way.

Is my entry using the Kase Peak Osc (KPO) in my system really better than random? (I’m doing this a the KPO is meant to be used with a Kase Convergence Divergence indicator which I posted on these forums and which gives 75+% accuracy according to Cynthia Kase, in entry timing, but which has not be coded yet). So now I want to see how well my KPO entry performs when I use and compare it to a random entry instead of a oscillator type entry (and use the same exit, the KDS) and so I need to generate approximately the same number of entry trades and similar ratio of longs to shorts.

Here is an extract from the book I referenced to explain in detail:

Kevin Davey: (Testing entries) “The first thing I usually want to know when testing a trading system is whether the entry has any usefulness. Many times, what looks like a good entry appears that way only because of the exits. Frequently it is difficult to know the true impact of entries when tested as a whole system. When I evaluate entries by themselves, I typically perform the analysis three ways:

- Fixed‐stop and target exit

- Fixed‐bar exit

- Random exit

Davey then describes these three.. etc etc…

Exit Testing

In a similar fashion to entry testing, there are a few different ways to test an exit. Where it gets complicated is when the exit is tied to the entry is some fashion. An example of this might be using support lines for entries, and resistance lines for exits. It is hard to separate the two. In these cases, I might choose not to even test exits by themselves, and rather proceed to a complete system test, discussed later.

When I do evaluate exits by themselves, I typically perform the analysis two ways:

- Similar‐approach entry

- Random entry

Similar‐Approach Entry

The core idea behind testing exits by themselves is to see if they can help give you an edge. Most people see edges as being applicable only when you enter, but really, exits have just as much, if not more, impact on the bottom line. A carefully designed exit, it has been shown, can make even bad entry systems profitable!

Since I will be testing the actual entry with the actual exit a bit later, at this point I want to see how the exit performs. To do this, I create an entry similar to the entry I want to use. This usually falls in one of two primary categories: trend following and countertrend following. Since I know what type of entry I have, I just create a generic one similar to it. For a trend‐following approach, for example, I may just employ an X‐bar breakout strategy. For a countertrend strategy, maybe I will use a relative strength index (RSI)‐based entry. In either case, I create an entry that is comparable to my actual entry. Then I test it with my exit strategy. A robust exit strategy that is profitable to my similar‐approach entries will likely also be profitable with my actual entry. This is a way to test an exit without involving the entry.

Random Entry

Discussed in a later section, if you have an exit strategy that works well with a random entry, you might have a really good system when you combine it with a solid entry technique. I do not use this approach as much as I used to, but occasionally I do like to see how a new exit technique works with random, no‐edge entries… etc etc..

■ Monkey See, Monkey Do

One of the last tests I like to run is what I call “Monkey See, Monkey Do.” The essence of the test is to see if my strategy does better than a dart‐throwing monkey.

Test 1: “Monkey Entry”

The first test I run is to see if the entry I developed is better than random. I simply replace the entry in my strategy with an entry than creates a randomly generated entry. I run the random entry, with the rest of my strategy intact, 8,000 times. This generates 8,000 unique performance reports, since each run will have different randomly generated entries. By adjusting the frequency of the entry signals, I ensure that I get close to the same number of trades as my walk‐forward history. Also, I try to match the percentage of long and short trades. These two conditions mean that the “monkey” trades as often as my system does, and in roughly the same proportion of long and short trades.

Typically, a good strategy will beat the monkey 9 times out of 10 in net profit and in maximum drawdown. For my 8,000 monkey trials, that means approximately 7,200 must have net profit worse than my results, and the same number of runs with higher maximum drawdown than my walk‐forward results. If I don’t reach these goals, I really have to wonder if my entry is truly better than random.

Test 2: “Monkey Exit”

The second test I run is to see if the exit I developed is better than random. It is much like the entry test, obviously, except in this case the monkey randomly exits the position. I control the random exit primarily by keeping the number of bars in a trade the same as my walk‐forward history. For example, if my walk‐forward history has an average of four bars per trade and always exits at the end of the day, I will tune the random exit to be on average the same. Also, it will always exit at the end of the day, if that is my criterion.

As with the monkey entry, I look for my walk‐forward results to be better than 90 percent of the monkey exits.

Test 3: “Monkey Entry, Monkey Exit”

After determining that my strategy is better than both a monkey entry and a monkey exit, I like to see that my strategy is better than a monkey entry and exit. I do this because sometimes my edge is in the interaction of the entry and exit. For example, it might be that my entry is valid only because I set the exit near a support or re- sistance zone. It might be that the entry, taken alone, or the exit, taken alone, isn’t enough without the other.

In this test, I replace all entry and exit code with random monkey code. I adjust the parameters of the random entry and exit to match my strategy in the following ways:

- Number of trades

- Ratio of long trades to short trades

- Average bars spent in a trade

Note that these conditions are the same I apply to the other monkey tests.Then I run the monkey entry, monkey exit strategy 8,000 times, just like the other tests, and compare results the same way.”

“make an extra condition with a random value from 1 to 5 an add trade if dayofweek = randomvalue.” Do you have a code snippet for that?

Also any link of random entries would be great – the ones I saw so far didn’t make any sense to me!

Cheers

Bard

LeoParticipant

Veteran

I posted a pseudo ramdom value from 1 to 10. Although the median is near 5. I Don like that it produces a lot of 10 and 1.

I read your article.

Still not having sense for me. I always test different Strategies for entry and exits and several combinations of them. I compared them between themself… Still not see the point of random dates in this ecuations… Something totally different is to find a seasonality pattern. That’s totally different.

By the way, I never compare my codes with monkeys trowing dards.

Maybe you can train infinity number of monkeys, one of them will write the code you need in prorealtime and another one will write a copy of a Shakespeare.

BardParticipant

Master

Can anyone fix this random entry code so it trades on the days it’s actually coded to trade on? (Instead of trading on dates that bare no relation to the dates coded?

Much appreciated,

Thanks

// Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

//Random Dates

StartDate1 = 01012018

StartDate2 = 22012018

StartDate3 = 26012018

StartDate4 = 01022018

StartDate5 = 02022018

StartDate6 = 16022018

StartDate7 = 23022018

StartDate8 = 30032018

StartDate9 = 19042018

StartDate10 = 22052018

StartDate11 = 18062018

StartDate12 = 22062018

StartDate13 = 28062018

StartDate14 = 11072018

StartDate15 = 17072018

StartDate16 = 26072018

StartDate17 = 10082018

StartDate18 = 30082018

StartDate19 = 04092018

StartDate20 = 20092018

StartDate21 = 01102018

StartDate22 = 05102018

StartDate23 = 15102018

StartDate24 = 18102018

StartDate25 = 25102018

If TradingLONG = (opendate = StartDate18 OR opendate = StartDate4 OR opendate = StartDate12 OR opendate = StartDate10 OR opendate = StartDate13 OR opendate = StartDate2 OR opendate = StartDate5 OR opendate = StartDate3 OR opendate = StartDate19 OR opendate = StartDate7 OR opendate = StartDate20 OR opendate = StartDate11 OR opendate = StartDate23) Then

TradingLONG = 1

Endif

If TradingLONG = (opendate = StartDate1 OR opendate = StartDate8 OR opendate = StartDate16 OR opendate = StartDate24 OR opendate = StartDate9 OR opendate = StartDate22 OR opendate = StartDate14 OR opendate = StartDate17 OR opendate = StartDate25 OR opendate = StartDate15 OR opendate = StartDate6 OR opendate = StartDate21) Then

TradingLONG = 0

Endif

// Conditions to enter long positions

IF TradingLONG = 1 THEN

BUY 10 PERPOINT AT MARKET

ENDIF

// Conditions to exit long positions

ignored, ignored, ignored, Dev, ignored, ignored = CALL "Kase Dev Stop LisseSAR4.5/6OPT" [p3]

//[p3,n]

c1 = (close CROSSES UNDER Dev)

IF c1 THEN

SELL AT MARKET

ENDIF

/////////////////////////

// Conditions to enter short positions

IF TradingLONG = 0 THEN

SELLSHORT 10 PERPOINT AT MARKET

ENDIF

// Conditions to exit short positions

ignored, ignored, ignored, Dev, ignored, ignored = CALL "Kase Dev Stop LisseSAR4.5/6OPT" [p3]

//[p3,n]

c2 = (close CROSSES OVER Dev)

IF c2 THEN

EXITSHORT AT MARKET

ENDIF