Hi There,

After 7 months of trading my learning curve is blocked by an incapability to link all the screeners to algo trading strategies.

I have gone through all the mistakes of the newbees but I am still not performing at all…

I precise that my objective is to “industrialize” my trades so I am looking for routines.

I am more a swing trader in style.

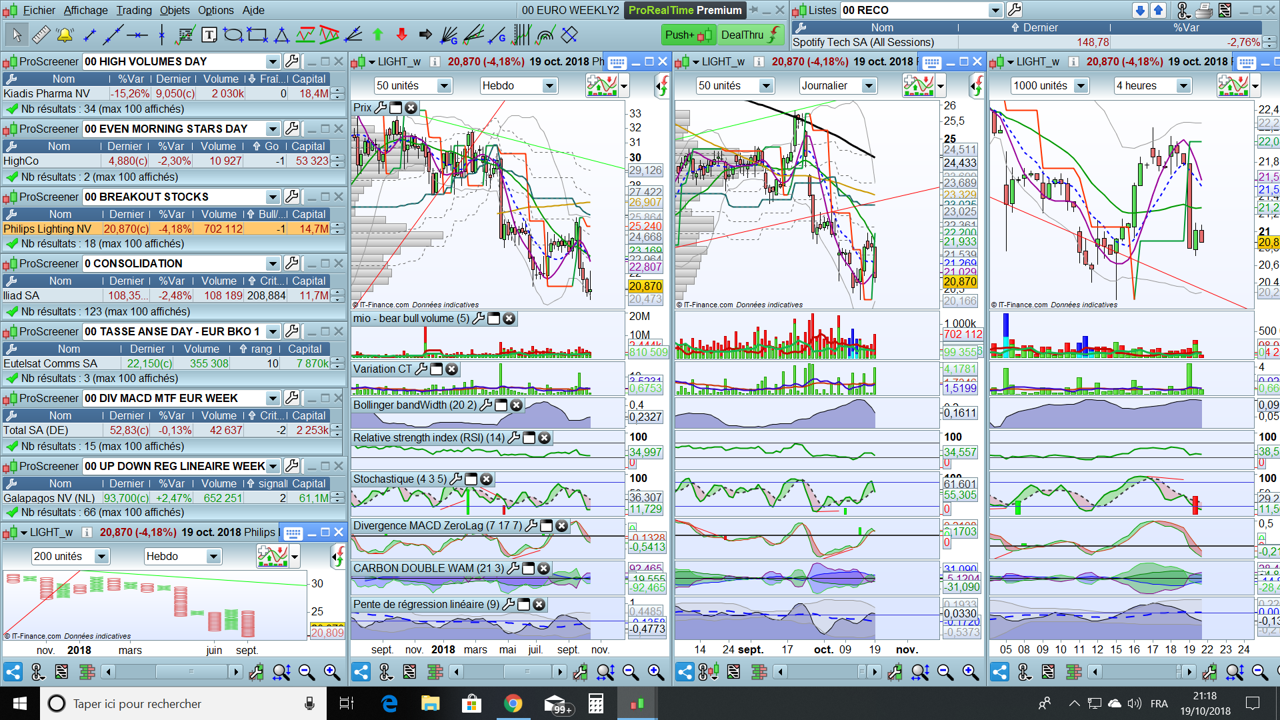

Currently I have on a daily basis the following screeners

- high volumes (daily)

- evening and morning stars (daily)

- breakout stocks (daily)

- consolidating stocks (daily)

- cup and handle patern (weekly)

- positive and negative divergences MACD zero lag (daily & weekly)

- tops and down of the Linear Regression slope (weekly)

1 >> Do you follow other key screeners?

2 >> For each of them which algorithm strategy would you consider ?

3 >> If you would not choose to run strategies on the long run but more programming your entries and exits, what is your basic core code to be adapted to the specific stock? Here under is mine but I don’t feel it is optimised.

defparam preloadbars = 150

defparam cumulateorders = false

equity = 1000 + strategyprofit

n= round(equity/close)

//// trailing stop1

Period=a

inner = 2*weightedaverage[ round( Period/2 ) ](close)-weightedaverage[Period](close)

MMHULL =weightedaverage[ round( sqrt(Period) ) ]( inner )

TrailStop = MMHULL

//

c1 = close > 9

c2 = TrailStop < Close

if c1 and C2 and (not longonmarket) then

buy n shares at market

//first stoploss:

sell at TrailStop stop

dynamicSL = TrailStop

endif

//dynamicSL

if longonmarket then

if (TrailStop>dynamicSL) then

dynamicSL=TrailStop

endif

sell at dynamicSL stop

endif

// vente short (to be defined)

if condition and (not shortonmarket) then

sellshort n shares at market

//first stoploss:

exitshort at TrailStop stop

dynamicSL = TrailStop

endif

//dynamicstopprice

if shortonmarket then

if (TrailStop < dynamicSL) then

dynamicSL = TrailStop

endif

exitshort at dynamicSL stop

endif

I have joined my screen so if you see things that I shoud add, feel free! May be people could share their screens to see how they work!

Dear veteran and profitable traders, thanks for your advices 😉

Chris