BC

BCParticipant

Master

I am stucking on a basic coding…how to code below?

Buy 1 contract after Bullcondition appear BullCandleStyle.

Thanks

Bin

//Buy condition

Bullcondition=low crosses over Average[20](close)

//Candle style

BC1 = Close[1] < Close[2]

BC2 = Close > Close[1]

BullCandleStyle=BC1 and BC2

//Long Entry

IF after Bullcondition appear BullCandleStyle then

BUY 1 CONTRACT AT market

Endif

Any good or am I misunderstanding the request or the strategy?

IF Bullcondition AND BullCandleStyle then

BUY 1 CONTRACT AT market

Endif

BCParticipant

Master

Hi Grahal

Thanks, your suggestion is buy when both condition appear at same time.

But my idea is: When bullcondition, hold the buy until BullCandle Style appear.

IF Bullcondition Then

BarIndex = BullIndex

Endif

If BullCandleStyle and BarIndex > BullIndex Then

BUY 1 CONTRACT AT Market

Endif

Or something similar … I’ll sleep on it! 🙂

How long you want to hold the condition? Couldn’t be forever as BullCondition may not be valid, so maybe you need below?

You can optimise variable x

IF Bullcondition Then

BarIndex = BullIndex

Endif

If BullCandleStyle and ((BarIndex - BullIndex) < x) Then

BUY 1 CONTRACT AT Market

Endif

As your Bull Condition is …

Bullcondition=low crosses over Average[20](close)

why not just use …

Bullcondition = Low > Average[20](close)

Then you could have …

If BullCondition and BullCancdle Them

Buye 1 Share at Market

Endif

BCParticipant

Master

Thanks Grahal, actually the bull condition contain 3MA and need confirm by a candle pull back.

I found this intersting strategy from internet and seem workable, you can take a look via below link.

http://www.tradingstrategyguides.com/big-three-trading-strategy/

Yeah link looks good, easy to read and well laid out website … I’ll digest better with my tea tonight. 🙂 It looks a lot like the Alligator Strategy?

I felt the simplistic explanation of the Alligator a bit naff when I first studied it, but I’m pleased to say it has stuck with me and I guess that is the reason (naff)! 🙂

https://www.forextraders.com/forex-education/forex-indicators/alligator-indicator-explained/

There is an Indicator on here …

https://www.prorealcode.com/prorealtime-indicators/bill-williams-alligator/

There is also the PRT Default … see attached.

GraHal

BCParticipant

Master

Hi Grahal

I am working on big three strategy, however I stuck on the stop loss coding.

eg: When long, stop loss should be (MA80-tradeprice), but Prorealtime only read previous tradeprice instead of current tradeprice.

😫😫😫

Didnt use TradePrice(1) did you?

If you put your code on here (using <> icon) we may be able to spot the reason?

BCParticipant

Master

yes, I try blank, (1) and (0), still not work.

I am out for some alcohol to relax, will post code later a moment later.

BCParticipant

Master

Hi GraHal

Here u go.

defparam preloadbars = 3000

defparam cumulateorders =false //true //false

//Big Three MA

FMA=Average[20](close) //green coloured(0,255,0)

MMA=Average[40](close)//blue coloured(0,0,255)

SMA=Average[80](close)//red coloured(255,0,0)

//High Low Bar Setting

CP=10

//Long Entry

if BC and BCandle then

//BUY min(25,PositionSizeLong) CONTRACT AT MARKET

BUY 1 CONTRACT AT MARKET

StopLossLong=Tradeprice-SMA[1]

//takeProfit = takeProfitLong

endif

//Long Exit

if LongonMarket and close crosses under SMA then

sell at market

endif

//short entry

if SC and SCandle then

//SELLSHORT min(25,PositionSizeShort) CONTRACT AT MARKET

SELLSHORT 1 CONTRACT AT MARKET

StopLossShort=SMA[1]-Tradeprice

//takeProfit = takeProfitShort

endif

//Short Exit

if ShortonMarket and close crosses over SMA then

exitshort at market

endif

// Stop Loss

if LongonMarket then

SET STOP LOSS StopLossLong

endif

if ShortonMarket then

SET STOP LOSS StopLossShort

endif

graph SMA

graph Tradeprice

graph StopLossLong

graph StopLossShort

BCParticipant

Master

miss condition

defparam preloadbars = 3000

defparam cumulateorders =false //true //false

//Big Three MA

FMA=Average[20](close) //green coloured(0,255,0)

MMA=Average[40](close)//blue coloured(0,0,255)

SMA=Average[80](close)//red coloured(255,0,0)

//High Low Bar Setting

CP=10

//Buy Signal

B1=low > SMA and low>MMA and low>FMA

B2=high >= highest[CP](high)

BC=B1 and B2

//Buy Candle

BC1 = Close[1] < Close[2]

BC2 = Close > Close[1]

BC3 = Close > Open

BCandle = BC1 and BC2 and BC3

//Sell Signal

S1=high < FMA and high<MMA and high<SMA

S2=low <= lowest[CP](low)

SC=S1 and S2

//Sell Caandle

SC1 = Close[1] > Close[2]

SC2 = Close < Close[1]

SC3 = Close < Open

SCandle = SC1 and SC2 and SC3

//Long Entry

if BC and BCandle then

//BUY min(25,PositionSizeLong) CONTRACT AT MARKET

BUY 1 CONTRACT AT MARKET

StopLossLong=Tradeprice-SMA[1]

//takeProfit = takeProfitLong

endif

//Long Exit

if LongonMarket and close crosses under SMA then

sell at market

endif

//short entry

if SC and SCandle then

//SELLSHORT min(25,PositionSizeShort) CONTRACT AT MARKET

SELLSHORT 1 CONTRACT AT MARKET

StopLossShort=SMA[1]-Tradeprice

//takeProfit = takeProfitShort

endif

//Short Exit

if ShortonMarket and close crosses over SMA then

exitshort at market

endif

// Stop Loss

if LongonMarket then

SET STOP LOSS StopLossLong

endif

if ShortonMarket then

SET STOP LOSS StopLossShort

endif

graph SMA

graph Tradeprice

graph StopLossLong

graph StopLossShort

what instrument / market and timeframe you running this on?

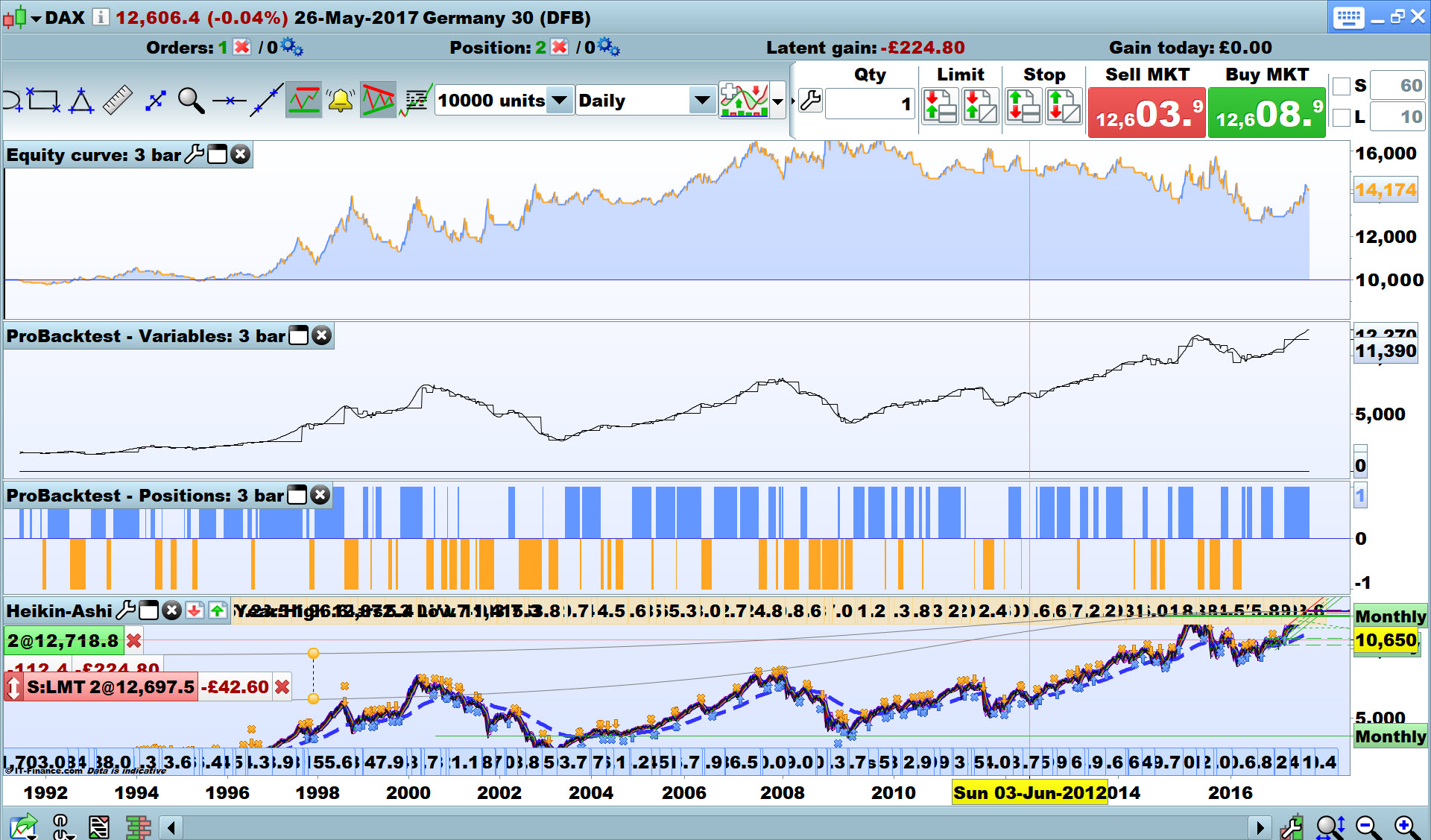

I got it going, see attached. You check it out to see if it’s doing what you want?

Here are the code differences …

40 StopLossLong = Tradeprice - (TradePrice-SMA[1])

53 StopLossShort= Tradeprice - (SMA[1]-Tradeprice)

BCParticipant

Master

Hi Grahal

I found below work.

//Long Entry

if BC and BCandle then

BUY 1 CONTRACT AT MARKET

BuyPrice=Close

StopLossLong = BuyPrice - SMA

endif