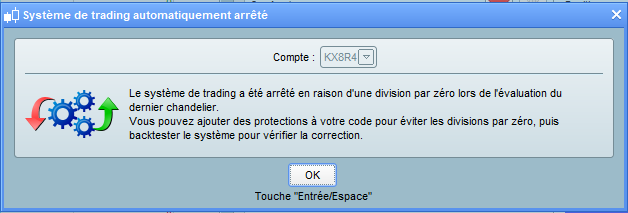

Bonjour, J’ai testé le code ci-dessous trouvé sur ce site et alors que le backtest fonctionne correctement, en réel le trading s’arrête en affichant le message d’erreur (copie d’écran ci-dessous) “division par zéro lors de l’évaluation du dernier chandelier”. Pourriez-vous m’aider à trouver d’où vient l’erreur dans le code?

Merci

//-------------------------------------------------------------------------

//main code : Paul/Bard Renko 1M ML2 v4b machine learning (ml2)

MLx2 applied to Long and Short Boxsize

//https://www.prorealcode.com/topic/machine-learning-in-proorder/page/3/#post-121130

//-------------------------------------------------------------------------

//https://www.prorealcode.com/topic/why-is-backtesting-so-unreliable/#post-110889

//definition of code parameters

defparam cumulateorders = false // cumulating positions deactivated

defparam preloadbars = 1000

//once mode = 0//1 // [0] with minimum distance stop; [1] without

//once minstopdistance = 20

//once percentage = 0 // [1] percentage; [0] points

//Money Management

//Capital = 10000 + strategyprofit //Current profit made by the closed trades of the running strategy.

N = 1//30*Capital / Close

heuristicscyclelimit = 2

once heuristicscycle = 0

once heuristicsalgo1 = 1

once heuristicsalgo2 = 0

if heuristicscycle >= heuristicscyclelimit then

if heuristicsalgo1 = 1 then

heuristicsalgo2 = 1

heuristicsalgo1 = 0

elsif heuristicsalgo2 = 1 then

heuristicsalgo1 = 1

heuristicsalgo2 = 0

endif

heuristicscycle = 0

else

once valuex = startingvalue

once valuey = startingvalue2

endif

if heuristicsalgo1 = 1 then

//heuristics algorithm 1 start

if (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) then

optimise = optimise + 1

endif

//Settings 1 & 2

startingvalue = 40 //5, 100, 10 //LONG BOXSIZE

ResetPeriod = 3 //1, 0.5 Specify no of months after which to reset optimisation

increment = 10 //5, 20, 10

maxincrement = 20 //5, 10 limit of no of increments either up or down

reps = 3 //1 number of trades to use for analysis //2

maxvalue = 50 //50, 20, 300, 150 //maximum allowed value

minvalue = increment //15, 5, minimum allowed value

startingvalue2 = 40 //5, 100, 50 //SHORT BOXSIZE

ResetPeriod2 = 3 //1, 0.5 Specify no of months after which to reset optimisation

increment2 = 10 //5, 10

maxincrement2 = 20 //1, 30 limit of no of increments either up/down //4

reps2 = 3 //1, 2 nos of trades to use for analysis //3

maxvalue2 = 50 //50, 20, 300, 200 maximum allowed value

minvalue2 = increment //15, 5, minimum allowed value

once monthinit = month

once yearinit = year

If (year = yearinit and month = (monthinit + ResetPeriod)) or (year = (yearinit + 1) and ((12 - monthinit) + month = ResetPeriod)) Then

ValueX = StartingValue

WinCountB = 0

StratAvgB = 0

BestA = 0

BestB = 0

monthinit = month

yearinit = year

EndIf

once valuex = startingvalue

once pincpos = 1 //positive increment position

once nincpos = 1 //negative increment position

once optimise = 0 //initialize heuristicks engine counter (must be incremented at position start or exit)

once mode1 = 1 //switches between negative and positive increments

//once wincountb = 3 //initialize best win count

//graph wincountb coloured (0,0,0) as "wincountb"

//once stratavgb = 4353 //initialize best avg strategy profit

//graph stratavgb coloured (0,0,0) as "stratavgb"

if optimise = reps then

wincounta = 0 //initialize current win count

stratavga = 0 //initialize current avg strategy profit

heuristicscycle = heuristicscycle + 1

for i = 1 to reps do

if positionperf(i) > 0 then

wincounta = wincounta + 1 //increment current wincount

endif

stratavga = stratavga + (((positionperf(i)*countofposition[i]*close)*-1)*-1)

next

stratavga = stratavga/reps //calculate current avg strategy profit

//graph (positionperf(1)*countofposition[1]*100000)*-1 as "posperf1"

//graph (positionperf(2)*countofposition[2]*100000)*-1 as "posperf2"

//graph stratavga*-1 as "stratavga"

//once besta = 300

//graph besta coloured (0,0,0) as "besta"

if stratavga >= stratavgb then

stratavgb = stratavga //update best strategy profit

besta = valuex

endif

//once bestb = 300

//graph bestb coloured (0,0,0) as "bestb"

if wincounta >= wincountb then

wincountb = wincounta //update best win count

bestb = valuex

endif

if wincounta > wincountb and stratavga > stratavgb then

mode1 = 0

elsif wincounta < wincountb and stratavga < stratavgb and mode1 = 1 then

valuex = valuex - (increment*nincpos)

nincpos = nincpos + 1

mode1 = 2

elsif wincounta >= wincountb or stratavga >= stratavgb and mode1 = 1 then

valuex = valuex + (increment*pincpos)

pincpos = pincpos + 1

mode1 = 1

elsif wincounta < wincountb and stratavga < stratavgb and mode1 = 2 then

valuex = valuex + (increment*pincpos)

pincpos = pincpos + 1

mode1 = 1

elsif wincounta >= wincountb or stratavga >= stratavgb and mode1 = 2 then

valuex = valuex - (increment*nincpos)

nincpos = nincpos + 1

mode1 = 2

endif

if nincpos > maxincrement or pincpos > maxincrement then

if besta = bestb then

valuex = besta

else

if reps >= 10 then

weightedscore = 10

else

weightedscore = round((reps/100)*100)

endif

valuex = round(((besta*(20-weightedscore)) + (bestb*weightedscore))/20) //lower reps = less weight assigned to win%

endif

nincpos = 1

pincpos = 1

elsif valuex > maxvalue then

valuex = maxvalue

elsif valuex < minvalue then

valuex = minvalue

endif

optimise = 0

endif

// heuristics algorithm 1 end

elsif heuristicsalgo2 = 1 then

// heuristics algorithm 2 start

if (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) then

optimise2 = optimise2 + 1

endif

//Settings 2

once monthinit2 = month

once yearinit2 = year

If (year = yearinit2 and month = (monthinit2 + ResetPeriod2)) or (year = (yearinit2 + 1) and ((12 - monthinit2) + month = ResetPeriod2)) Then

ValueY = StartingValue2

WinCountB2 = 0

StratAvgB2 = 0

BestA2 = 0

BestB2 = 0

monthinit2 = month

yearinit2 = year

EndIf

once valuey = startingvalue2

once pincpos2 = 1 //positive increment position

once nincpos2 = 1 //negative increment position

once optimise2 = 0 //initialize heuristicks engine counter (must be incremented at position start or exit)

once mode2 = 1 //switches between negative and positive increments

//once wincountb2 = 3 //initialize best win count

//graph wincountb2 coloured (0,0,0) as "wincountb2"

//once stratavgb2 = 4353 //initialize best avg strategy profit

//graph stratavgb2 coloured (0,0,0) as "stratavgb2"

if optimise2 = reps2 then

wincounta2 = 0 //initialize current win count

stratavga2 = 0 //initialize current avg strategy profit

heuristicscycle = heuristicscycle + 1

for i2 = 1 to reps2 do

if positionperf(i2) > 0 then

wincounta2 = wincounta2 + 1 //increment current wincount

endif

stratavga2 = stratavga2 + (((positionperf(i2)*countofposition[i2]*close)*-1)*-1)

next

stratavga2 = stratavga2/reps2 //calculate current avg strategy profit

//graph (positionperf(1)*countofposition[1]*100000)*-1 as "posperf1-2"

//graph (positionperf(2)*countofposition[2]*100000)*-1 as "posperf2-2"

//graph stratavga2*-1 as "stratavga2"

//once besta2 = 300

//graph besta2 coloured (0,0,0) as "besta2"

if stratavga2 >= stratavgb2 then

stratavgb2 = stratavga2 //update best strategy profit

besta2 = valuey

endif

//once bestb2 = 300

//graph bestb2 coloured (0,0,0) as "bestb2"

if wincounta2 >= wincountb2 then

wincountb2 = wincounta2 //update best win count

bestb2 = valuey

endif

if wincounta2 > wincountb2 and stratavga2 > stratavgb2 then

mode2 = 0

elsif wincounta2 < wincountb2 and stratavga2 < stratavgb2 and mode2 = 1 then

valuey = valuey - (increment2*nincpos2)

nincpos2 = nincpos2 + 1

mode2 = 2

elsif wincounta2 >= wincountb2 or stratavga2 >= stratavgb2 and mode2 = 1 then

valuey = valuey + (increment2*pincpos2)

pincpos2 = pincpos2 + 1

mode2 = 1

elsif wincounta2 < wincountb2 and stratavga2 < stratavgb2 and mode2 = 2 then

valuey = valuey + (increment2*pincpos2)

pincpos2 = pincpos2 + 1

mode2 = 1

elsif wincounta2 >= wincountb2 or stratavga2 >= stratavgb2 and mode2 = 2 then

valuey = valuey - (increment2*nincpos2)

nincpos2 = nincpos2 + 1

mode2 = 2

endif

if nincpos2 > maxincrement2 or pincpos2 > maxincrement2 then

if besta2 = bestb2 then

valuey = besta2

else

if reps2 >= 10 then

weightedscore2 = 10

else

weightedscore2 = round((reps2/100)*100)

endif

valuey = round(((besta2*(20-weightedscore2)) + (bestb2*weightedscore2))/20) //lower reps = less weight assigned to win%

endif

nincpos2 = 1

pincpos2 = 1

elsif valuey > maxvalue2 then

valuey = maxvalue2

elsif valuey < minvalue2 then

valuey = minvalue2

endif

optimise2 = 0

endif

// heuristics algorithm 2 end

endif

//

boxsizel = ValueX

boxsizes = ValueY

//

renkomaxl = round(close / boxsizel) * boxsizel

renkominl = renkomaxl - boxsizel

renkomaxs = round(close / boxsizes) * boxsizes

renkomins = renkomaxs - boxsizes

//

if high > renkomaxl + boxsizel then

renkomaxl = renkomaxl + boxsizel

renkominl = renkominl + boxsizel

endif

if low < renkomins - boxsizes then

renkomaxs = renkomaxs - boxsizes

renkomins = renkomins - boxsizes

endif

// Conditions to enter long positions

Buy N CONTRACT at renkoMaxL + boxSizeL stop

// Conditions to enter short positions

Sellshort N CONTRACT at renkoMinS - boxSizeS stop

//

//if percentage then

//set stop %loss 0.25 %trailing 0.5

//set target %profit 2

//else

set stop ptrailing 50 //50 + 100

set target pprofit 500

//endif