Hello – I hope this finds everybody well.

As I’ve just made my first foray into coding, after hanging around on the site for sometime over a year now, I thought I’d share and of course would welcome any feedback. By way on context, I’ve been fiddling around with trading (via a spread betting account with IG) for a couple of years. I’ve been up a bit, down a bit and a couple of months ago found myself pretty much back where I started, and struggling to find the time to concentrate properly what with a full time job and a young family. I’ve had several false starts with ProRealCode and never got as far as putting a system live – until about 3 weeks ago.

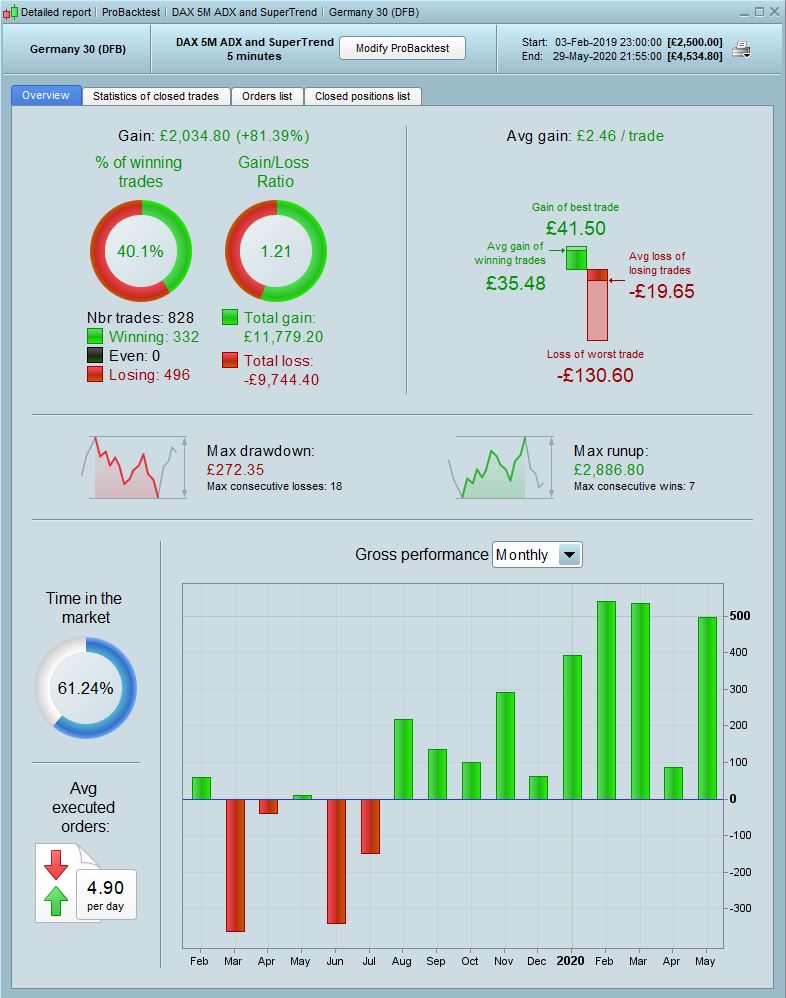

The very simple system runs on DAX 5 minute chart and uses a 200 period EMA and SuperTrend as filters, and an ADX/ADXR crossover as entry trigger. Stops and profit target is fixed (about a 1 to 1.6 R/R). Back-testing showed it to be profitable based on a 100K bars test (starting in February 2019), but with a horrible curve – a fairly consistent losing streak early on, but consistently profitable since about the end of last July. Now, I know this is far from satisfactory for the purist, but recent performance was enough to persuade me to make it live, with low position size and guaranteed stops.

I absolutely don’t expect this to run for ever – it’s going to stop working based on back test, but it’s given me the confidence that there’s something to build on for the future. Happily after 3 and a bit weeks of running, account is up about 18% and win rate is just the right side of 50%.

// Definition of code parameters

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

// Common indicators

indicator1 = ExponentialAverage[200](close)

indicator2 = SuperTrend[3,10]

indicator3 = ADX[11]

indicator4 = ADXR[11]

// Common variable values

adxval = 22

profitpoints = 83

losspoints = 50

// Conditions to enter long positions

c1 = (close > indicator1)

c2 = (close > indicator2)

c3 = (indicator3 CROSSES OVER indicator4)

c4 = indicator3 > adxval

IF c1 AND c2 AND c3 AND c4 THEN

BUY 0.5 PERPOINT AT MARKET

ENDIF

// Conditions to enter short positions

c5 = (close < indicator1)

c6 = (close < indicator2)

c7 = (indicator3 CROSSES OVER indicator4)

c8 = indicator3 > adxval

IF c5 AND c6 AND c7 AND c8 THEN

SELLSHORT 0.5 PERPOINT AT MARKET

ENDIF

// Stops and targets

SET STOP pLOSS losspoints

SET TARGET pPROFIT profitpoints

//EXIT for Weekend

IF opendayofweek = 5 and openhour >= 21 and openminute >= 50 then

sig=1

else

sig=0

endif

IF sig=1 THEN

SELL AT MARKET

EXITSHORT AT MARKET

ENDIF

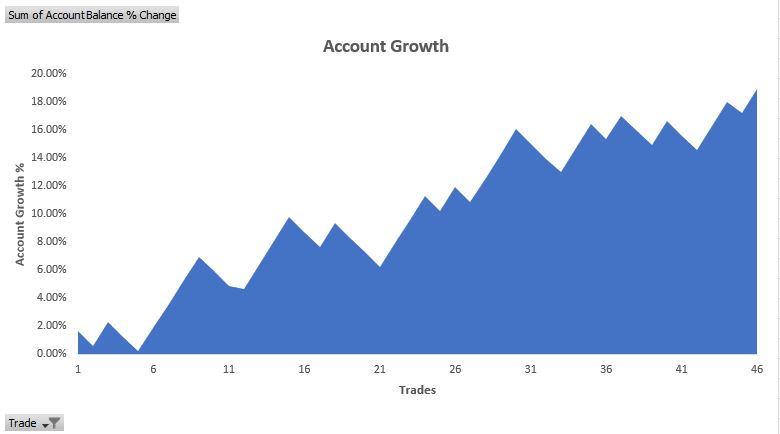

Back test view attached along with account growth chart based on the 46 trades placed to date.

Comments and advice welcome. I’m very new to this, and not even scratched the surface.

Cheers

WT

Thanks for sharing your code.

I think it will be useful to many and a source for new ideas 🙂

Any news from the recent results of your strategy? Thanks for sharing! 🙂

So, I ran this live for 2 months – 11th May to around 11th July. As per my original post, it started very well then began to tail off as market conditions changed. I lucked out really starting it at a good time. Win rate for the period was about 42% overall and it was a couple of hundred quid in profit when I stopped it. My intention has always been to go back and look at how I can refine it, probably initially looking at some multi-timeframe filters. Also keen to explore alternative exit (e.g. trailing stop) rather than fixed points target.

Results from running in back-test from 11th July to current are very bad, but the market’s basically been going sideways. So it definitely needs some better filtering to look for trending periods.

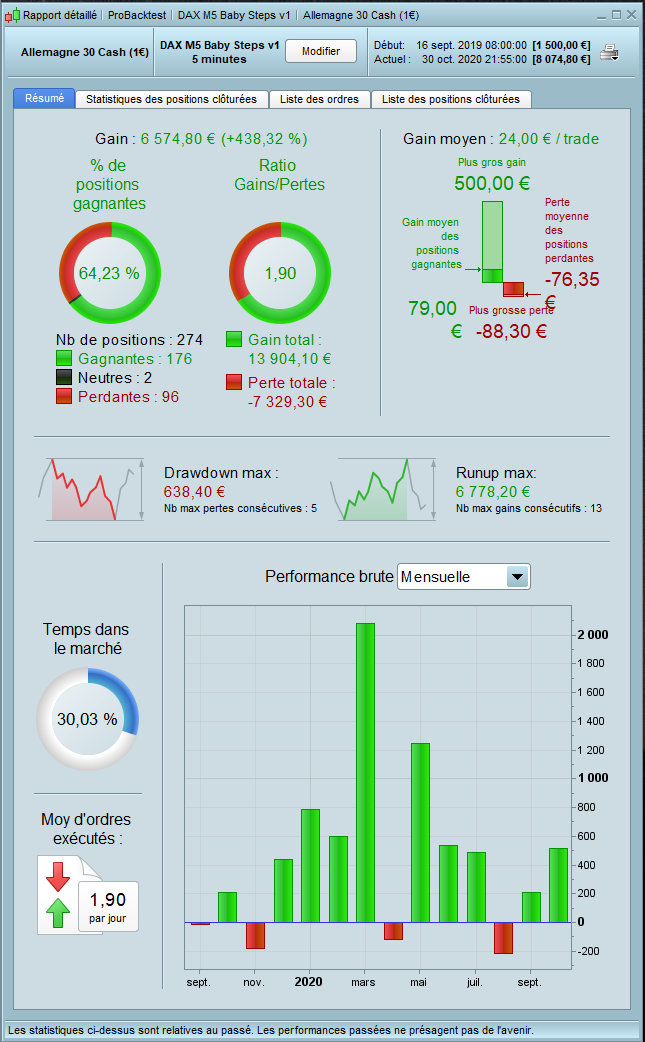

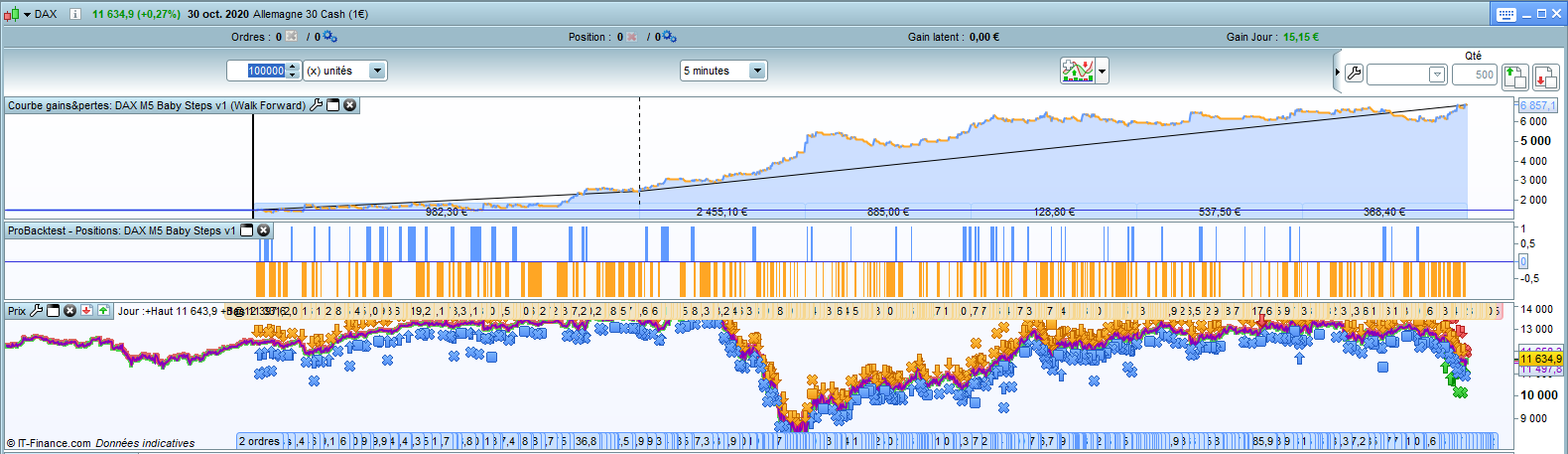

Hi Welshtrader, thank you for sharing your code. I’m a beginner, so please bear with me. I’ve added a few conditions (VWAP, KST and VWMA) to increase the WinRate to around 64% (Sept. 16th 2019 to date) with a R/R of x1.9 (Capital of 1500€, TF 5 minutes and Size = 1 DAX 1€ Contract). I’ve also copied the ML code from juanj (https://www.prorealcode.com/topic/machine-learning-in-proorder/) and the MFE from Nicolas (https://www.prorealcode.com/blog/learning/trailing-stop-max-favorable-excursion-mfe/).

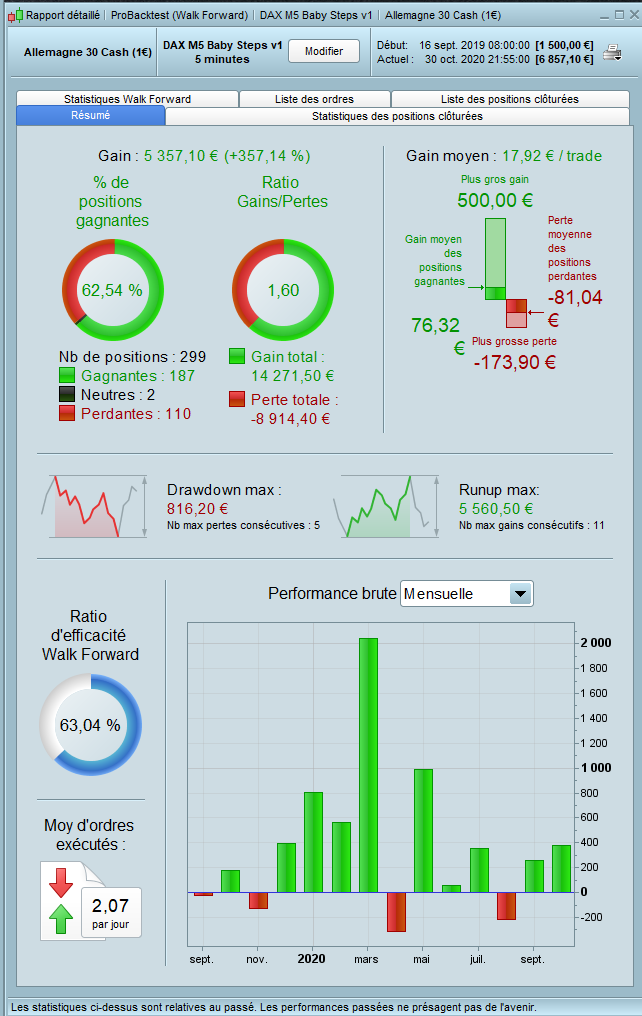

Walk Forward shows a Win Rate of 62.5% and R/R of x1.6.

Not sure of the Tick by Tick mode in the backtest.

Please test and let me know…

A big thank you to robertogozzi and Nicolas who guided me through my learning process.

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

N = 1

Timeframe(5 minutes)

EMA200 = ExponentialAverage[200](close)

SupT = SuperTrend[3,10]

iADX = ADX[13]

iADXR = ADXR[13]

VWAP = CALL "VWAP Intrady"

OscKST, SignalKST = CALL "KST8"

VWMA3 = CALL "VWMA Intraday"

EMA3 = ExponentialAverage[3](close)

// Common variable values

adxval = StartingValue

profitpoints = 500

losspoints = 84 //(Best in WF 94)

trailingstop = 50

///////////////////////////////////////////////////////////////////////

// Conditions to enter long positions

c1 = (close > EMA200) AND (close > VWAP) AND (OscKST > SignalKST) AND (VWMA3 > EMA3)

c2 = (close > SupT)

c3 = (iADX CROSSES OVER iADXR)

c4 = iADX > adxval

// Conditions to enter short positions

c5 = (close < EMA200)

c6 = (close < SupT)

c7 = (iADX CROSSES OVER iADXR)

c8 = iADX > adxval

/////////////////////////////////////////////////////////////////////////

// Heuristics Algorithm Start

If onmarket[1] = 1 and onmarket = 0 Then

optimize = optimize + 1

EnDif

StartingValue = 24 //(Best in WF 24)

ResetPeriod = 8 //Specify no of months after which to reset optimization

Increment = 1

MaxIncrement = 4 //Limit of no of increments either up or down

Reps = 5 //Number of trades to use for analysis

MaxValue = 29 //Maximum allowed value

MinValue = increment //Minimum allowed value

once monthinit = month

once yearinit = year

If (year = yearinit and month = (monthinit + ResetPeriod)) or (year = (yearinit + 1) and ((12 - monthinit) + month = ResetPeriod)) Then

ValueX = StartingValue

WinCountB = 0

StratAvgB = 0

BestA = 0

BestB = 0

monthinit = month

yearinit = year

EndIf

once ValueX = StartingValue

once PIncPos = 1 //Positive Increment Position

once NIncPos = 1 //Neative Increment Position

once Optimize = 0 ////Initialize Heuristicks Engine Counter (Must be Incremented at Position Start or Exit)

once Mode = 1 //Switches between negative and positive increments

If Optimize = Reps Then

WinCountA = 0 //Initialize current Win Count

StratAvgA = 0 //Initialize current Avg Strategy Profit

For i = 1 to Reps Do

If positionperf(i) > 0 Then

WinCountA = WinCountA + 1 //Increment Current WinCount

EndIf

StratAvgA = StratAvgA + (((PositionPerf(i)*countofposition[i]*100000)*-1)*-1)

Next

StratAvgA = StratAvgA/Reps //Calculate Current Avg Strategy Profit

If StratAvgA >= StratAvgB Then

StratAvgB = StratAvgA //Update Best Strategy Profit

BestA = ValueX

EndIf

If WinCountA >= WinCountB Then

WinCountB = WinCountA //Update Best Win Count

BestB = ValueX

EndIf

If WinCountA > WinCountB and StratAvgA > StratAvgB Then

Mode = 0

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 1 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 1 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA < WinCountB and StratAvgA < StratAvgB and Mode = 2 Then

ValueX = ValueX + (Increment*PIncPos)

PIncPos = PIncPos + 1

Mode = 1

ElsIf WinCountA >= WinCountB or StratAvgA >= StratAvgB and Mode = 2 Then

ValueX = ValueX - (Increment*NIncPos)

NIncPos = NIncPos + 1

Mode = 2

EndIf

If NIncPos > MaxIncrement or PIncPos > MaxIncrement Then

If BestA = BestB Then

ValueX = BestA

Else

If reps >= 10 Then

WeightedScore = 10

Else

WeightedScore = round((reps/100)*100)

EndIf

ValueX = round(((BestA*(20-WeightedScore)) + (BestB*WeightedScore))/20) //Lower Reps = Less weight assigned to Win%

EndIf

NIncPos = 1

PIncPos = 1

ElsIf ValueX > MaxValue Then

ValueX = MaxValue

ElsIf ValueX < MinValue Then

ValueX = MinValue

EndIF

Optimize = 0

EndIf

// Heuristics Algorithm End

/////////////////////////////////////////////////////////////////////////

IF c1 AND c2 AND c3 AND c4 THEN

BUY N CONTRACT AT MARKET

ENDIF

IF c5 AND c6 AND c7 AND c8 THEN

SELLSHORT N CONTRACT AT MARKET

ENDIF

//trailing stop

//resetting variables when no trades are on market

if not onmarket then

MAXPRICE = 0

MINPRICE = close

priceexit = 0

endif

//case SHORT order

if shortonmarket then

MINPRICE = MIN(MINPRICE,close) //saving the MFE of the current trade

if tradeprice(1)-MINPRICE>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MINPRICE+trailingstop*pointsize //set the exit price at the MFE + trailing stop price level

endif

endif

//case LONG order

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close) //saving the MFE of the current trade

if MAXPRICE-tradeprice(1)>=trailingstop*pointsize then //if the MFE is higher than the trailingstop then

priceexit = MAXPRICE-trailingstop*pointsize //set the exit price at the MFE - trailing stop price level

endif

endif

//exit on trailing stop price levels

if onmarket and priceexit>0 then

EXITSHORT AT priceexit STOP

SELL AT priceexit STOP

endif

// Stops and targets

SET STOP pLOSS losspoints

SET TARGET pPROFIT profitpoints

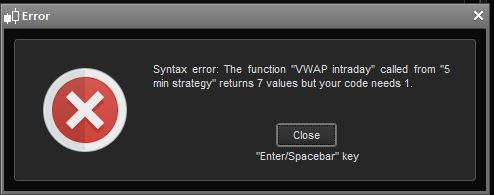

i get this error using the code…

Below the code I’ve used for VWAP courtesy of one of the members here. Let me know if you spot an error in the code.

// VWAP@Time intraday

// 10.04.2020

// Daniele Maddaluno

DEFPARAM CalculateOnLastBars = 2500

startTime=080000

endTime= 235959

if opentime < startTime or opentime > endTime then

n = 0

dwapT1 = 0

//dwapT2 = 0

priced = 0

shared = 0

summ = 0

vwap = close

//vwapstd = 0

else

n = n + 1

// This if has been added just for plot reasons

if n <= 1 then

dwapT1 = 0

//dwapT2 = 0

else

dwapT1 = 190

//dwapT2 = 128

endif

priced = priced + (totalprice*volume)

shared = shared + volume

if shared>0 then

vwap = priced/shared

summ = summ + square(totalprice - vwap)

//vwapstd = sqrt(summ / n)

endif

endif

// Manage the coloring of vwap mid line

if close > vwap then

dwapR = 0

dwapG = 128

dwapB = 192

else

dwapR = 255

dwapG = 0

dwapB = 0

endif

return vwap coloured(dwapR, dwapG, dwapB, dwapT1) as "vwap"

V WAP … hmm, brings to mind a certain song title. And everything else. And now you’re all going to think of that every time you see that indicator, hahaha.

Cardi. B? Can you please post the lycrics here? ))))))

No … you will be banned! 🙂

I’d never heard of Cardi B or the song, but being an inquisitive chap I had to check it out! 🙂

Just checked, it’s Megan T. S. Anyway, everyone here undertands what VWAP stands for 🙂

What is Heuristics used for in your program.

don’t use valueX

fifi743

Thank you for spotting this gross mistake. My bad!

I’ve “tried” to correct it and run again backtest and WF.

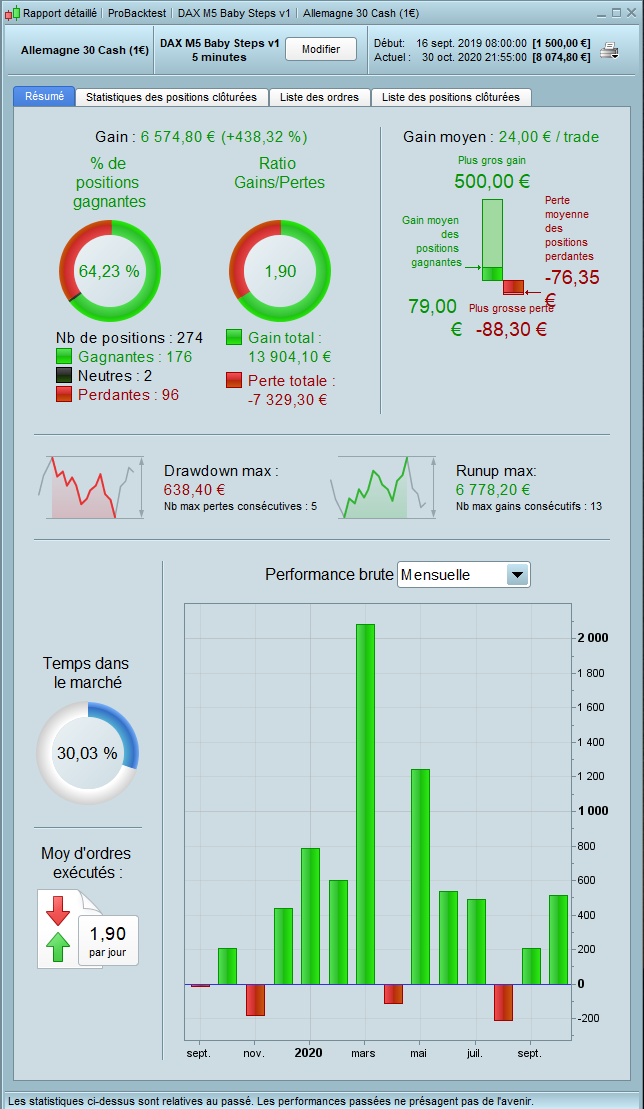

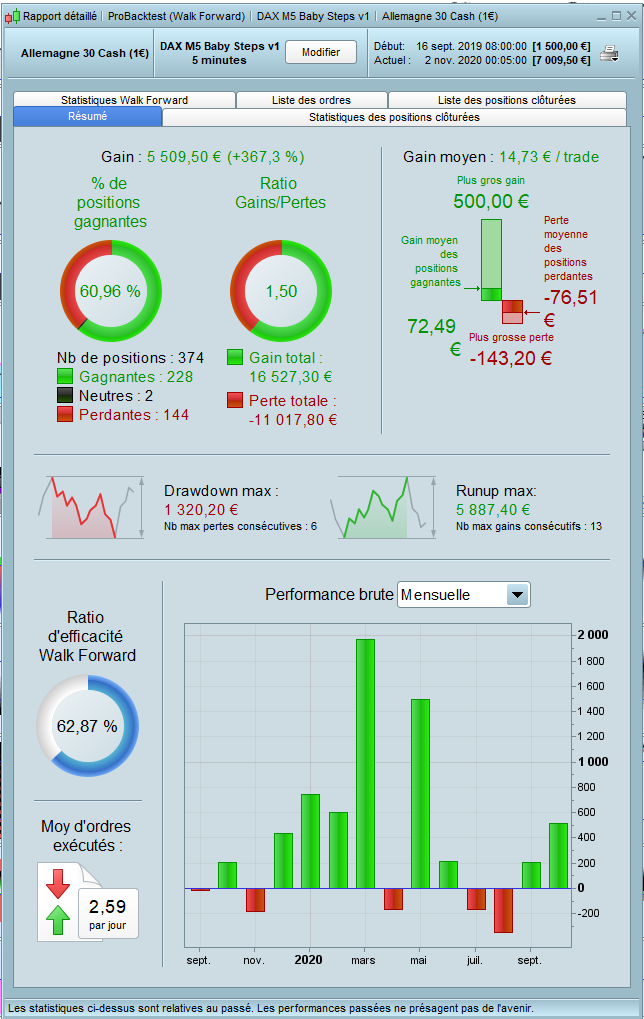

So, the initial version (ver 1 ) I posted (working witout ML) did generate in backtest 6574€ WinRate 64.23% and Profit Rate 1.9x. When running the WF, the results are 5509€ WinRate 60.96% and Profit Rate 1.5x. (files below)

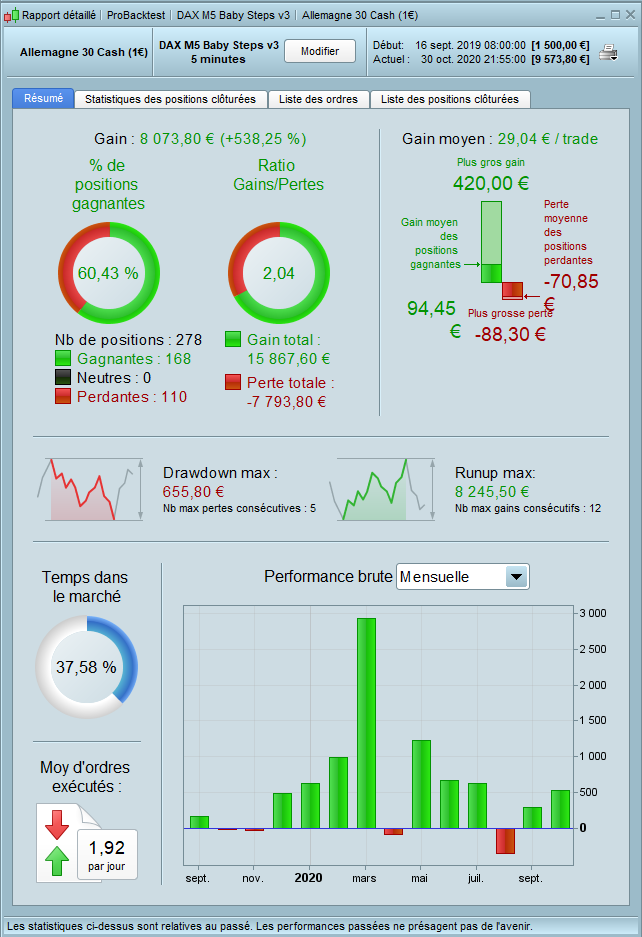

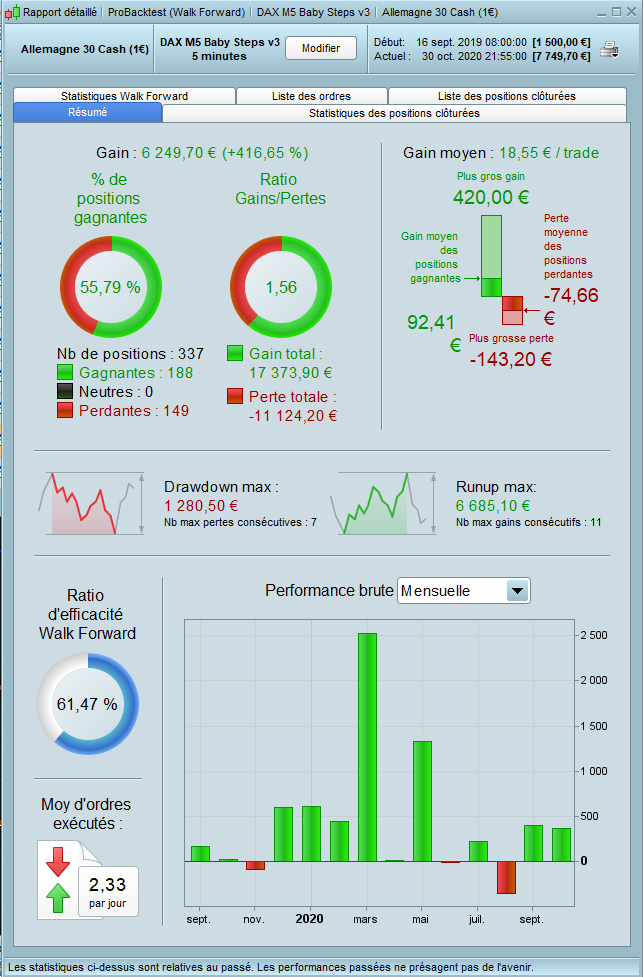

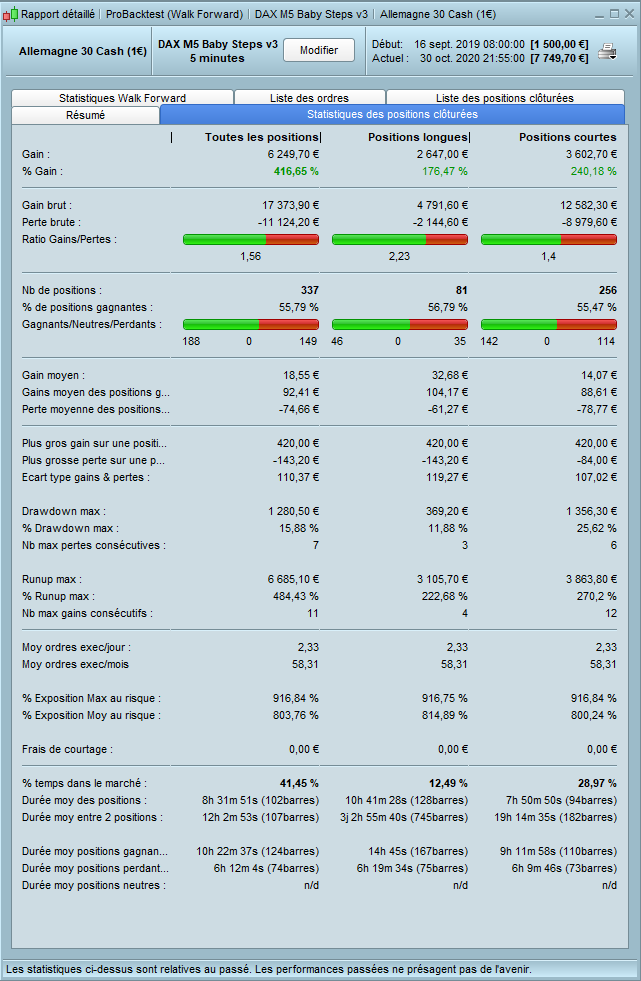

The version with ML embedded (ver 3) did generate in backtest 8073€ WinRate 60.43% and Profit Rate 2.04x. When running the WF, the results are 6249€ WinRate 55.79% and Profit Rate 1.56x. (files below + ITF)

So, the results with ML appear to be better in normal backtest and in WF.

Please review and let me know how we can further improve the result.