I tried to change the time frame for the daily pivot conditions by only considering the 34 candles before 16:30. But apparently that is also not working:(

if time = 163000 then

newdailyhigh = highest[34](high)[0]

newdailylow = lowest[34](low)[0]

newdailyclose = close[0]

endif

Pivot = (newdailyhigh[1] + newdailylow[1] + newdailyclose[1]) / 3

R1 = 2*Pivot - newdailylow[1]

S1 = 2*Pivot - newdailyhigh[1]

rR2 = Pivot + (newdailyhigh[1] - newdailylow[1])

S2 = Pivot - (newdailyhigh[1] - newdailylow[1])

R3 = R1 + (newdailyhigh[1] - newdailylow[1])

S3 = S1 - (newdailyhigh[1] - newdailylow[1])

Is anything working? 🙂

Why don’t you get a simplified / cut down version working then start building it back up again?

If anybody else can offer any help here then feel free? 🙂

Everything else is working:) There is just this little time issue left.

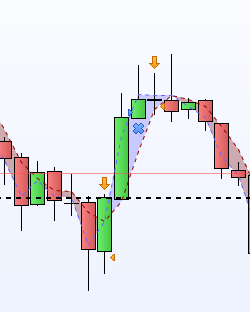

Sorry to bother you again, but it is almost working:) I enhanced to range of the day to the whole day from 0:00 till 23:59 and the pivot lines match those of the chart:) The profit is also still high. But now I have a new issue:( As you can see in the picture, the pivot lines are good for tuesdays till friedays but they are pretty messed up on mondays. I have no idea why that happens.

the pivot lines are good for tuesdays till friedays but they are pretty messed up on mondays

Now I’ve forgotten again what market this is on sorry? 🙂

Are the Pivot lines based on price the day before? If Yes, then the DAX and other markets open for 2 or 3 hours on Sunday night (e.g. EUR/USD @ 22:00 and DAX @ 23:00) so this could be screwing the Pivots for Monday??

Just an idea / immediate thoughts?

You don’t have to say sorry:) Yes it is the DAX, and you where right about sunday. Now I change the code to this and the pivot lines for mondays are align with those within the chart:) Thank you so much!!!

DEFPARAM CumulateOrders = false

DEFPARAM FlatBefore = 000000

DEFPARAM FlatAfter = 234500

if OpenDayOfWeek = 1 then

Pivot = (DHigh(2) + DLow(2) + DClose(2)) / 3

R1 = 2*Pivot - DLow(2)

S1 = 2*Pivot - DHigh(2)

rR2 = Pivot + (DHigh(2) - DLow(2))

S2 = Pivot - (DHigh(2) - DLow(2))

R3 = R1 + (DHigh(2) - DLow(2))

S3 = S1 - (DHigh(2) - DLow(2))

endif

if OpenDayOfWeek = 2 then

Pivot = (DHigh(1) + DLow(1) + DClose(1)) / 3

R1 = 2*Pivot - DLow(1)

S1 = 2*Pivot - DHigh(1)

rR2 = Pivot + (DHigh(1) - DLow(1))

S2 = Pivot - (DHigh(1) - DLow(1))

R3 = R1 + (DHigh(1) - DLow(1))

S3 = S1 - (DHigh(1) - DLow(1))

endif

if OpenDayOfWeek = 3 then

Pivot = (DHigh(1) + DLow(1) + DClose(1)) / 3

R1 = 2*Pivot - DLow(1)

S1 = 2*Pivot - DHigh(1)

rR2 = Pivot + (DHigh(1) - DLow(1))

S2 = Pivot - (DHigh(1) - DLow(1))

R3 = R1 + (DHigh(1) - DLow(1))

S3 = S1 - (DHigh(1) - DLow(1))

endif

if OpenDayOfWeek = 4 then

Pivot = (DHigh(1) + DLow(1) + DClose(1)) / 3

R1 = 2*Pivot - DLow(1)

S1 = 2*Pivot - DHigh(1)

rR2 = Pivot + (DHigh(1) - DLow(1))

S2 = Pivot - (DHigh(1) - DLow(1))

R3 = R1 + (DHigh(1) - DLow(1))

S3 = S1 - (DHigh(1) - DLow(1))

endif

if OpenDayOfWeek = 5 then

Pivot = (DHigh(1) + DLow(1) + DClose(1)) / 3

R1 = 2*Pivot - DLow(1)

S1 = 2*Pivot - DHigh(1)

rR2 = Pivot + (DHigh(1) - DLow(1))

S2 = Pivot - (DHigh(1) - DLow(1))

R3 = R1 + (DHigh(1) - DLow(1))

S3 = S1 - (DHigh(1) - DLow(1))

endif

Why not code fewer lines re days other than Day 1 and use …

if OpenDayOfWeek <> 1 then

Pivot = (DHigh(1) + DLow(1) + DClose(1)) / 3

R1 = 2*Pivot - DLow(1)

S1 = 2*Pivot - DHigh(1)

rR2 = Pivot + (DHigh(1) - DLow(1))

S2 = Pivot - (DHigh(1) - DLow(1))

R3 = R1 + (DHigh(1) - DLow(1))

S3 = S1 - (DHigh(1) - DLow(1))

You are right, that looks better!:)

Unfortunately there still seems to be a problem with my stops.

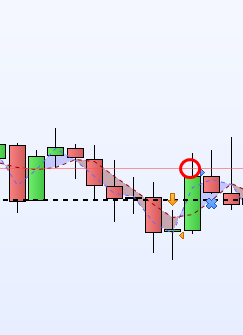

I tried to set the stop to the highest high of the doji or of the confirmation candle right next to the doji. So if the high of the doji is higher, then this is my stop, and vice versa. Additionally the stop should be placed 2 points higher than those highs, because of the spread. But as you can see in the picture the trade is exited by the condition when a close ist higher than the previous high. It should have been closed somewhere around the red line. It would be nice if the stop was triggerd immediately and not at the open of the next candle. Thank you very much for your help!:)

//DAX

//15 min

DEFPARAM CumulateOrders = false

DEFPARAM FlatBefore = 090000

DEFPARAM FlatAfter = 173000

Pivot = (DHigh(1) + DLow(1) + DClose(1)) / 3

R1 = 2*Pivot - DLow(1)

S1 = 2*Pivot - DHigh(1)

rR2 = Pivot + (DHigh(1) - DLow(1))

S2 = Pivot - (DHigh(1) - DLow(1))

R3 = R1 + (DHigh(1) - DLow(1))

S3 = S1 - (DHigh(1) - DLow(1))

dojisize = 4.2*pipsize

doji = Range >= ABS(Open[1] - Close[1]) * dojisize

bearishp = (doji and close[1] <= pivot+2 and close[1] >= pivot-2 and close<low[1])

If bearishp Then

SellShort size Contract at Market

if shortonmarket and high>high[1] then

exitshort at (high+2*pipsize) stop

endif

if shortonmarket and high<high[1] then

exitshort at (high[1]+2*pipsize) stop

endif

Endif

IF shortonmarket and (close >high[1]) then

exitshort at market

ENDIF

To get an immediate exit (not at end of candle) try this …

The difference is that you are setting the Stop at Trade Open.

If bearishp Then

SellShort size Contract at Market

ExitShort at (close >high[1]) Stop

Endif

This did not change anything. And the conditions where it places the stop would also be neglected.

//DAX

//15 min exit strategy

If bearishp Then

SellShort size Contract at Market

exitshort at (high+2*pipsize) stop

exitshort at (high+2*pipsize) stop

Endif

IF shortonmarket and (close >high[1]) then

exitshort at market

ENDIF

I tried a different approach but as soon as I added one more Pivot Line the system fails again and messes up. It works for only one Line, though. Within this approach I tried to store the candle conditions of the entry. It was also not possible to write the exitshort commands within the “if bearishp” conditions. I had to write them into new if conditions afterwards.

I don’t know what to try anymore, or if it will work at all like I planned. Any suggestions?:)

//DAX

// 15 min

DEFPARAM CumulateOrders = false

DEFPARAM FlatBefore = 090000

DEFPARAM FlatAfter = 173000

Pivot = (DHigh(1) + DLow(1) + DClose(1)) / 3

R1 = 2*Pivot - DLow(1)

S1 = 2*Pivot - DHigh(1)

rR2 = Pivot + (DHigh(1) - DLow(1))

S2 = Pivot - (DHigh(1) - DLow(1))

R3 = R1 + (DHigh(1) - DLow(1))

S3 = S1 - (DHigh(1) - DLow(1))

dojisize = 4.2*pipsize

doji = Range >= ABS(Open[1] - Close[1]) * dojisize

bearishp = (doji and close[1] <= pivot+2 and close[1] >= pivot-2 and close<low[1])

bearishr1 = (doji and close[1] <= r1+2 and close[1] >= r1-2 and close<low[1])

If bearishp then

if high<high[1] Then

hdbp = high[1]+2

SellShort size Contract at Market

elsif high>high[1] then

hnbp = high+2

sellshort size contract at market

endif

endif

if shortonmarket then

if hdbp then

exitshort at hdbp stop

elsif hnbp then

exitshort at hnbp stop

endif

endif

If bearishr1 then

if high<high[1] Then

hdbr1 = high[1]+2

SellShort size Contract at Market

elsif high>high[1] then

hnbr1 = high+2

sellshort size contract at market

endif

endif

if shortonmarket and hdbr1 then

exitshort at hdbr1 stop

endif

if shortonmarket and hnbr1 then

exitshort at hnbr1 stop

endif

exitshort at (close >high[1]) stop

Sorry to write again, but I coudn’t edit it anymore. A simple solution might be to set up 8 different trading systems where each system consideres a different Pivot line and execute all of them at the same time. Does that make sense?

I’m not one bit a supa-coder and have to visualise more complex actions happening in order to understand them and so all I have been doing is offering a solution to your snippets that you said did not work.

Maybe supa-coder @RobertoGozzi (or AN Other) might happen along anytime soon and see what is wrong with your System?

In the meantime, to make it easy for helpers …

- Post an equity curve of results from a backtest.

- What is the most significant function that is not working?

I was looking at code at post https://www.prorealcode.com/topic/automated-trading-with-pivot-points-and-dojis/page/3/#post-70557, these are the logical errors I could spot:

- lines 24 and 28 + 41 and 43 may assign new values to the variables that mimic a stoploss at each new bar because they do not tell between being or not ONMARKET and this behaviour will change the results of your attempts to exit due to SL, so they should not be changed ONCE a trade has been opened (line 22 should read If bearishp and Not OnMarket then)

- at lines 34, 36, 53 and 57 variables HDBP, HNBP, HDBR1 and HNBR1 will always be true once they have been set the first time, while you should reset them to ZERO when Not OnMarket, I guess;

- line 61 will NEVER be true, since you want to exit at a price which is either 0 or 1; for sure it won’t work with DAX, it may turn true with EUR/USD if that pair falls to 1.0000 and at that very moment that line is executed, what did you want to do with that line?

First of all, thank you very much!!! 😉

I changed a few things, but it is still not executing the exitshorts when hitting the highest high of the doji or the trigger candle. Where the red circle is, was it supposed to exit.

//DAX

//15 min

DEFPARAM CumulateOrders = false

DEFPARAM FlatBefore = 090000

DEFPARAM FlatAfter = 173000

if OpenDayOfWeek = 1 then

Pivot = (DHigh(2) + DLow(2) + DClose(2)) / 3

R1 = 2*Pivot - DLow(2)

endif

if OpenDayOfWeek = 2 then

Pivot = (DHigh(1) + DLow(1) + DClose(1)) / 3

R1 = 2*Pivot - DLow(1)

endif

if OpenDayOfWeek = 3 then

Pivot = (DHigh(1) + DLow(1) + DClose(1)) / 3

R1 = 2*Pivot - DLow(1)

endif

if OpenDayOfWeek = 4 then

Pivot = (DHigh(1) + DLow(1) + DClose(1)) / 3

R1 = 2*Pivot - DLow(1)

endif

if OpenDayOfWeek = 5 then

Pivot = (DHigh(1) + DLow(1) + DClose(1)) / 3

R1 = 2*Pivot - DLow(1)

endif

dojisize = 4.2*pipsize

doji = Range >= ABS(Open[1] - Close[1]) * dojisize

bearishp = (doji and close[1] <= pivot+2 and close[1] >= pivot-2 and close<low[1])

bearishr1 = (doji and close[1] <= r1+2 and close[1] >= r1-2 and close<low[1])

size = 5

If bearishp and not onmarket then

if high<high[1] Then

hdbp = high[1]+2

SellShort size Contract at Market

elsif high>high[1] then

hnbp = high+2

sellshort size contract at market

endif

endif

if shortonmarket then

if hdbp then

exitshort at hdbp stop

elsif hnbp then

exitshort at hnbp stop

endif

endif

If bearishr1 and not onmarket then

if high<high[1] Then

hdbr1 = high[1]+2

SellShort size Contract at Market

elsif high>high[1] then

hnbr1 = high+2

sellshort size contract at market

endif

endif

if shortonmarket and hdbr1 then

exitshort at hdbr1 stop

endif

if shortonmarket and hnbr1 then

exitshort at hnbr1 stop

endif

if shortonmarket and (close >high[1]) then

exitshort at market

endif

if not onmarket then

hdbp = 0

hnbp = 0

hdbr1 = 0

hnbr1 = 0

endif