Hi Everyone,

I apologise in advance for probably not posting at the right place.

I have been doing a lot of checks on the below strategy that i found on the forum. Unfortunately i cannot remember where i found it as i renamed it as “AOEMA” for Awesome oscillator/Exponential moving average. It was easier for me to remember. I liked its simplicity and the regularity of the results.

I tried it on both long+ short or short only trades but i have a preference for the higher volume of chosing both (fees could prove me wrong?)

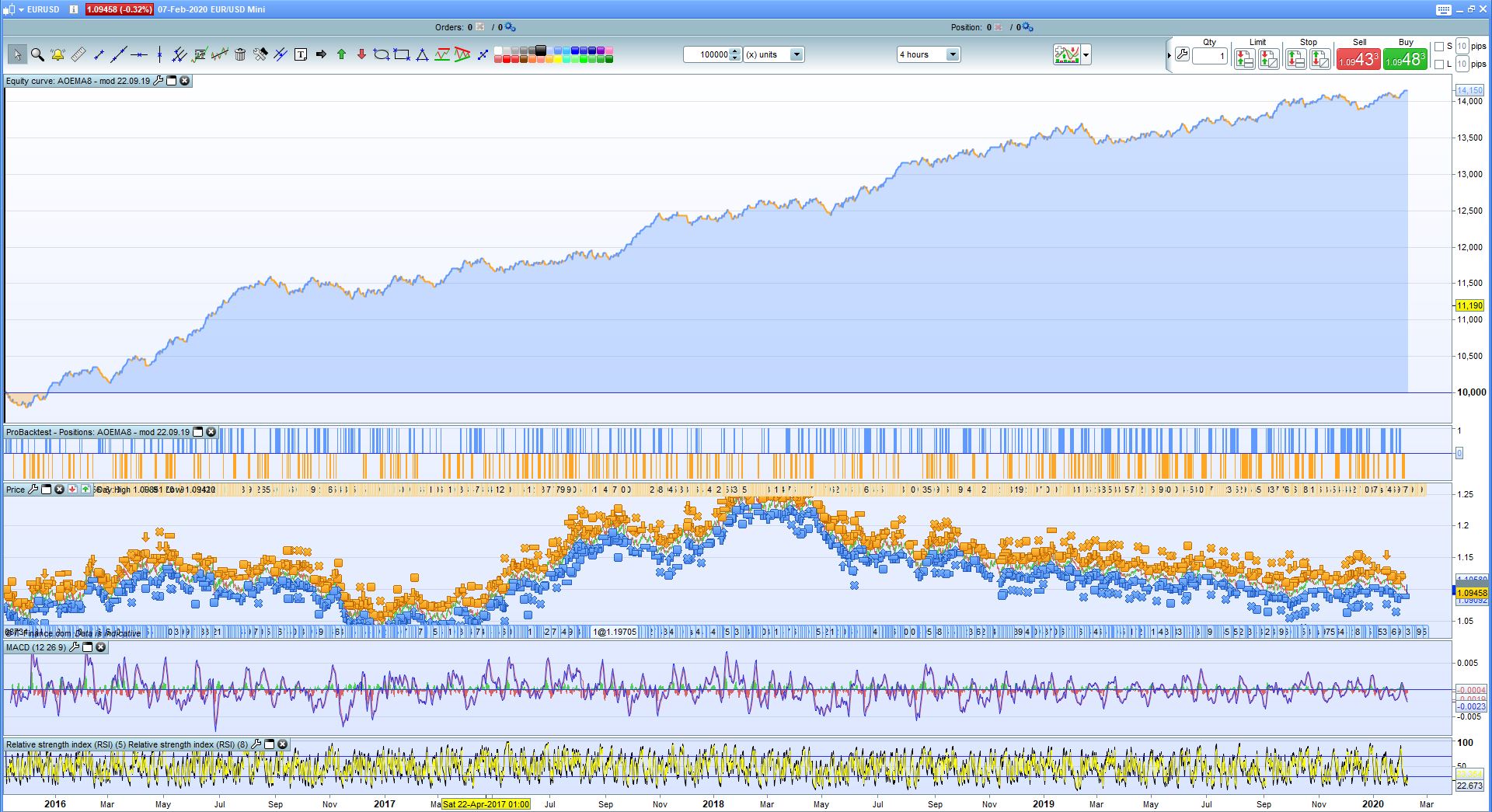

Given the parameters i created were back in Sept’19 and the strategy keeps behaving well, i am posting it in the hope that you can comment on it and maybe extend the check to a longer timeframe (100,000 in my version with spread of 0.7):

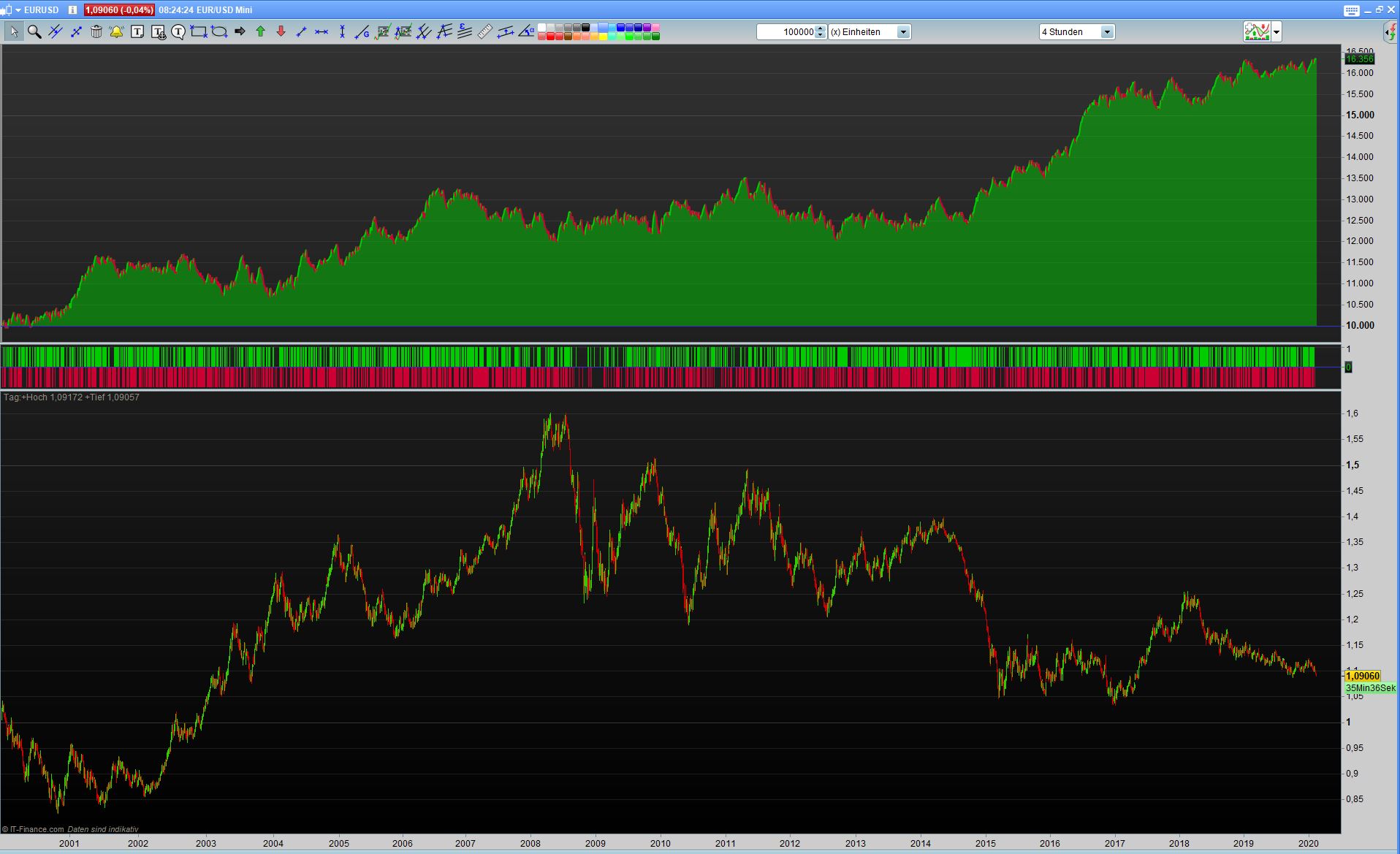

The results on 100,000 from beginning to today are attached.

//Strategy found on ProRealCode forum, mod Sharkool 22.09.19

//EURUSD/4H

Defparam cumulateorders = false

emavaleur=5

TP = 48

SL = 27

valeur = 39

test=3

EMA8 = exponentialaverage[emavaleur](close)

AO = Average[test](medianprice) - Average[valeur](medianprice)

IF AO > AO[1] and close crosses over EMA8 THEN

buy at market

ENDIF

IF AO < AO[1] and close crosses under EMA8 THEN

sellshort at market

ENDIF

set stop Ploss SL // ORIGINAL 0.75%

set target Pprofit TP //ORIGINAL 1.5%

Thank you

Thanks for the feedback about this simple strategy. So you confirm that you haven’t modified the settings since September 2019? So that 4 or 5 months of Out Of Sample results seems steady.

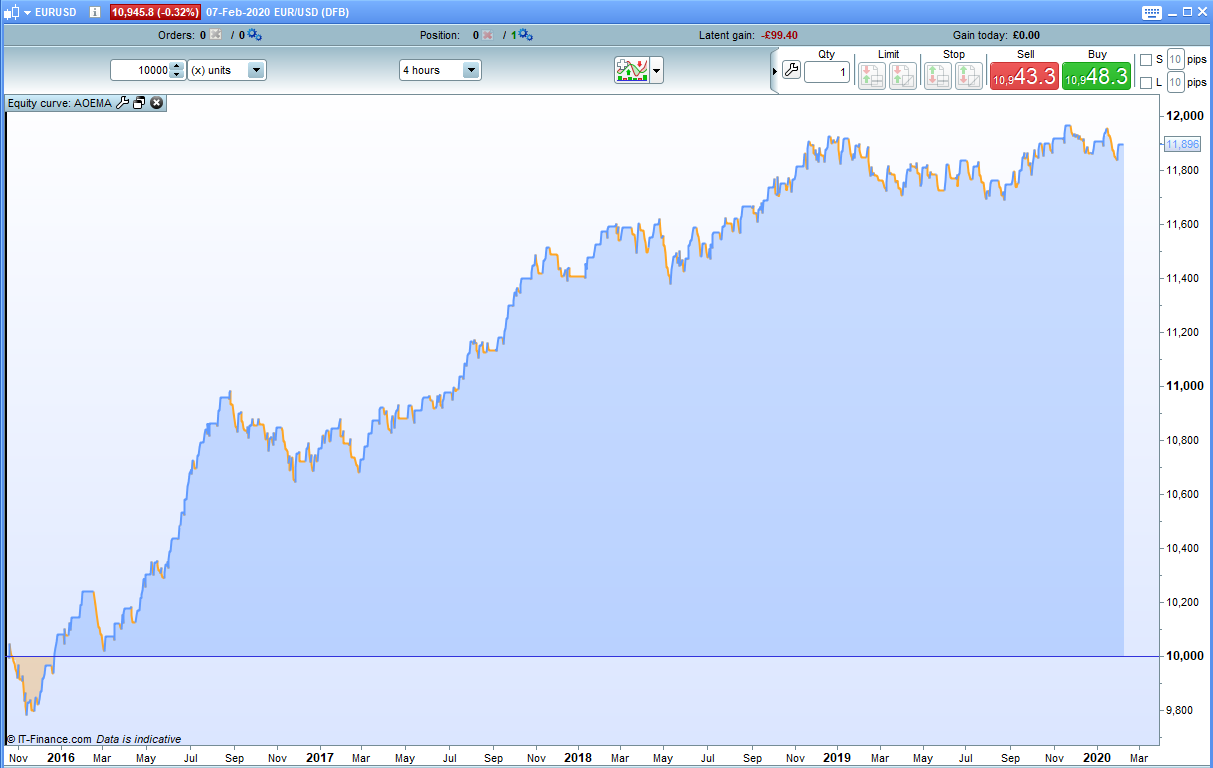

It is always interesting to separate out the long and short in to two strategies especially when there is position direction reversal in a strategy which can be potentially curve fitted to avoid bad trades in the other direction. So attached are the long only and short only equity curves for closing positions rather than reversing positions.

Razz

RazzParticipant

Master

Hello Sharkool

As desired 0.7 pips spread

by

….and that is what they call in the trade ‘a curve fit’! It really shows the benefits of developing on a small IS and then running on an OOS section of data though.

Thanks again for the testing @Razz

@Nicolas yes I haven’t changed the settings since 01/09/2019. I ran some parameters optimization test this morning and the current settings seem to remain the most robust. ema8 at 5 and trigger at 3 or 4 seem to be fairly solid.

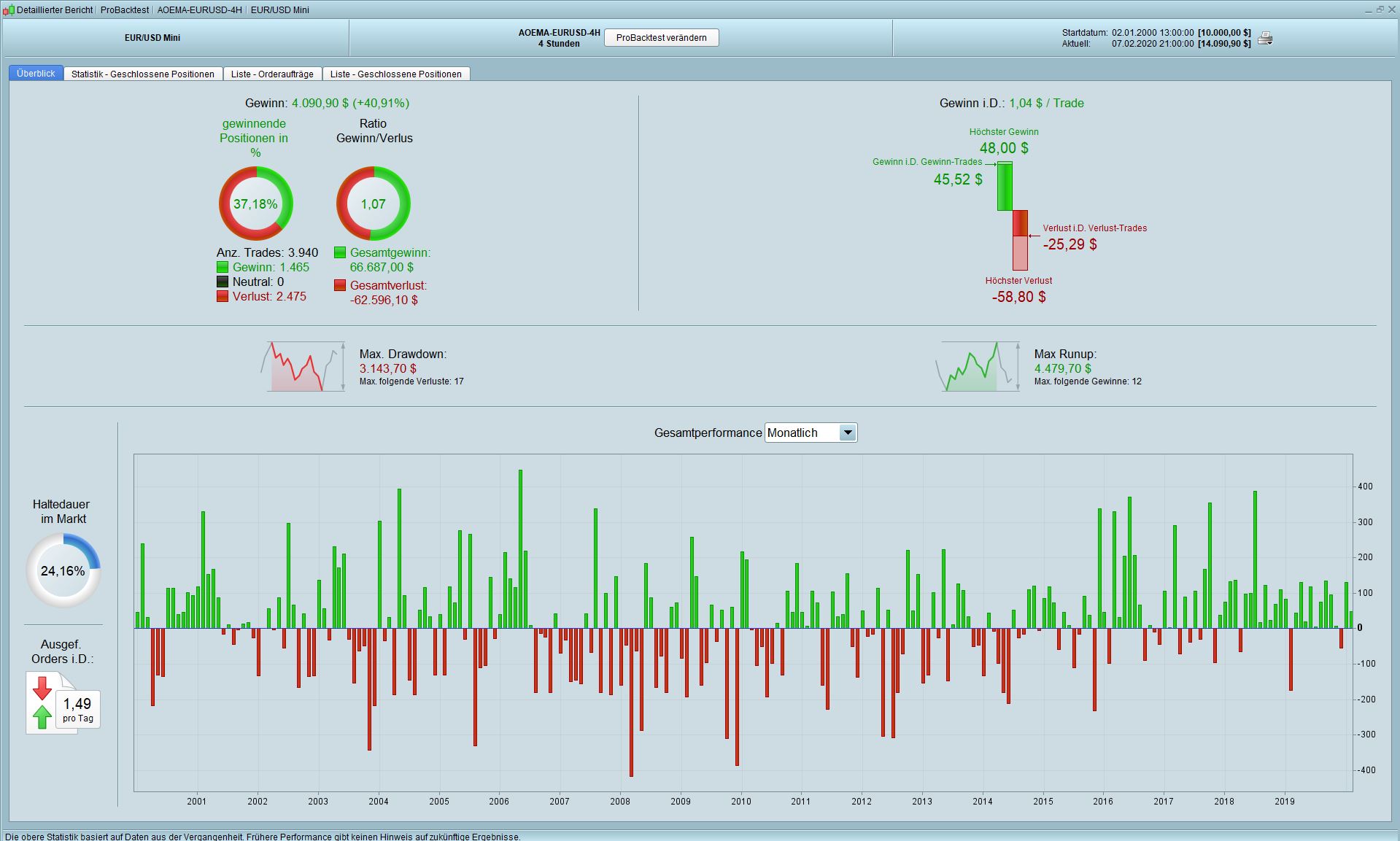

When i ran the test in 01/09/2019 i admit i optimized the result and they were: pip/trade of 5.04 over 751 trades with 43% win.

At 08/02/2020 with the same parameters we get: 5.62 pips/trade over 738 trades with 44% win. (nb of max consecutive losses remains 8 and drawdown remains below 400)

@Vonasi i agree with your view but also in your experience do you think having fairly constant results on more than 700+ trades and over 4years+ can be a sign that the “market spirit” may have changed over the past few tears. By “market spirit” i mostly think of the increase of automated trading. Maybe my optimism makes me think it might be that the combination of these 2 indicators have somehow fallen in line with the majority of combined automatic trading parameters than are used by the big financial institutions or is it wishful thinking?…

This brings the difficult question of knowing over what timeframe a 4H strategy for instance has to be tested and it might well be that this is just over-fitted. It has survived since 01/09/19 so i keep a little bit of hope on that one for now..

For me I’m afraid to say that I think it is just a perfect curve fit to the data that you had and so far you have been lucky and market structure has not changed much and so it is still working. Automatic algo trading has been around since mid 90’s – yes there is much more of it today than in the early days but even if we only look at the few years just prior to your original data sample the strategy performs terribly which shouts curve fit.

You could trade it and hope that it works for a bit longer but one day it will suddenly stop working and that day could be tomorrow. Personally I would bin it. If you had 200k of bars then you could have a play with optimising it on 100k bars and see if you can find anything that then also works on the other 100k bars or do a WF optimisation to see if there is a close range of settings that work before binning it.

Forex is a very random beast that moves at the whims of news and politics and by what the banks want to own today and what they want to sell tomorrow – I don’t think it has ‘market spirit’!

Thanks for the feedback @Vonasi! I fear you are right.

Before i completely lose hope and bin it i’d like to indeed have a quick check with other parameters.

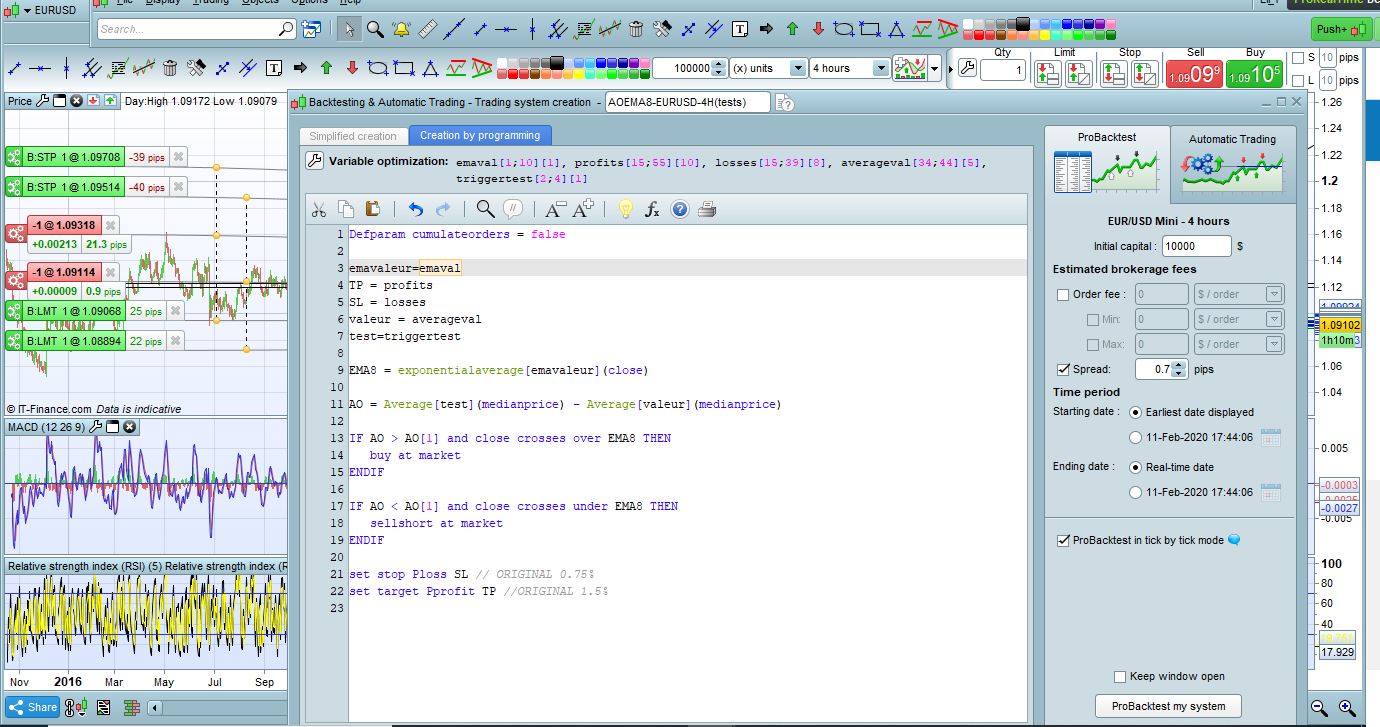

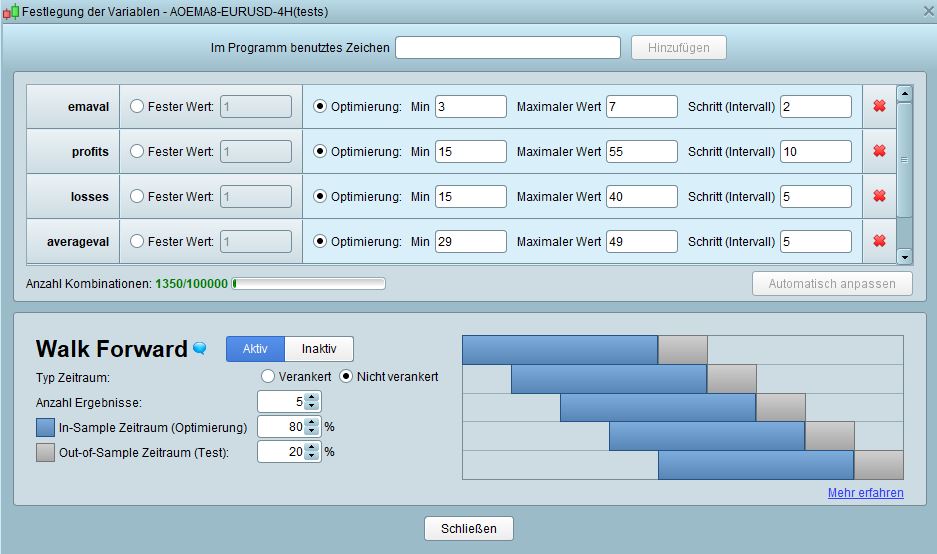

I have prepared the attached & below itf file + printscreen so that someone can run a check on 200,000.

There are 5 variables as per below:

emavaleur=emaval

TP = profits

SL = losses

valeur = averageval

test=triggertest

@Razz, it would be great if you could help me again on this one. If you are in Melbourne i surely owe you a good coffee for all the testings!

Thanks in advance,

Defparam cumulateorders = false

emavaleur=emaval

TP = profits

SL = losses

valeur = averageval

test=triggertest

EMA8 = exponentialaverage[emavaleur](close)

AO = Average[test](medianprice) - Average[valeur](medianprice)

IF AO > AO[1] and close crosses over EMA8 THEN

buy at market

ENDIF

IF AO < AO[1] and close crosses under EMA8 THEN

sellshort at market

ENDIF

set stop Ploss SL // ORIGINAL 0.75%

set target Pprofit TP //ORIGINAL 1.5%

RazzParticipant

Master

Good Morning

No problem, its a pleasure

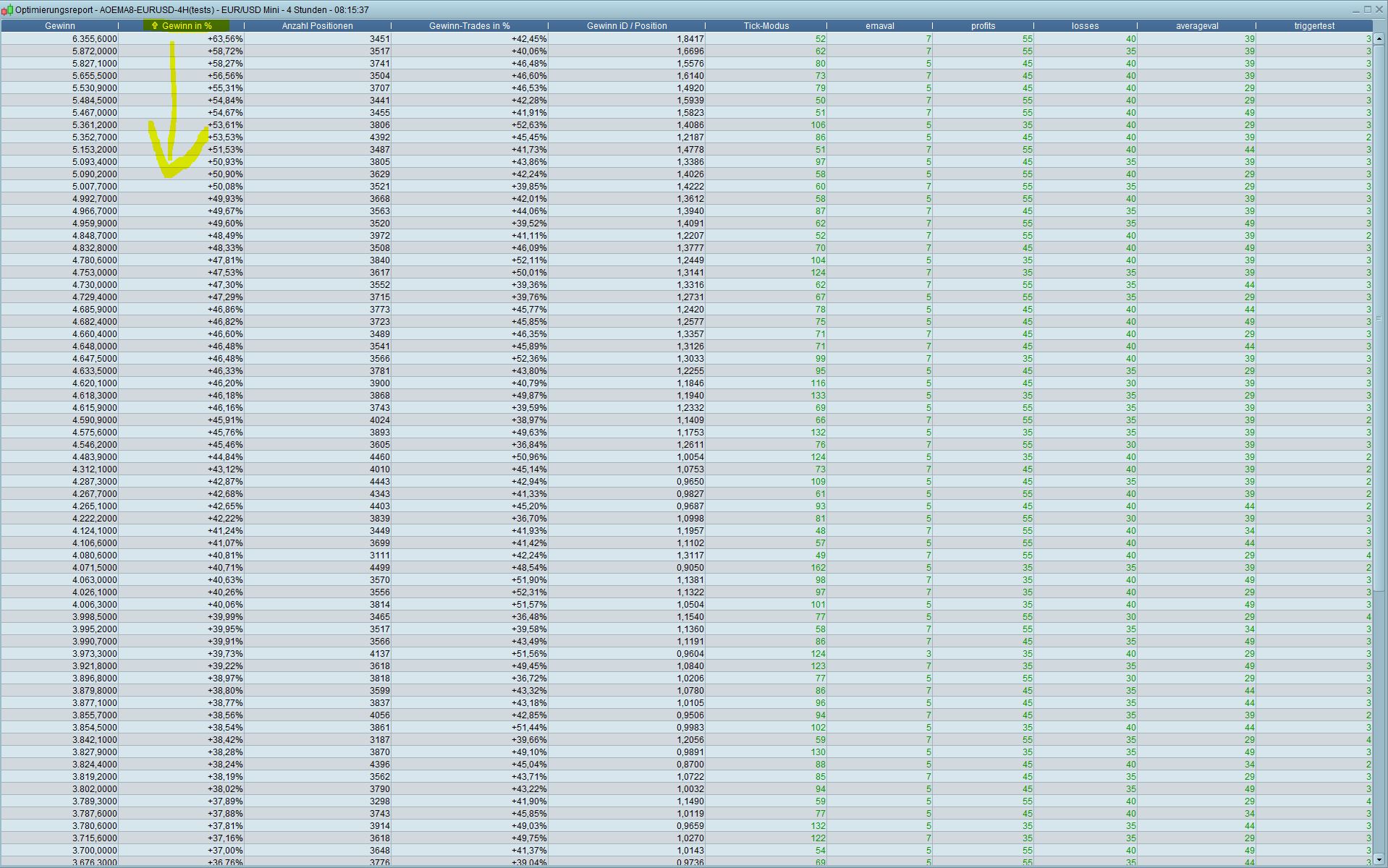

Test 100.000

RazzParticipant

Master

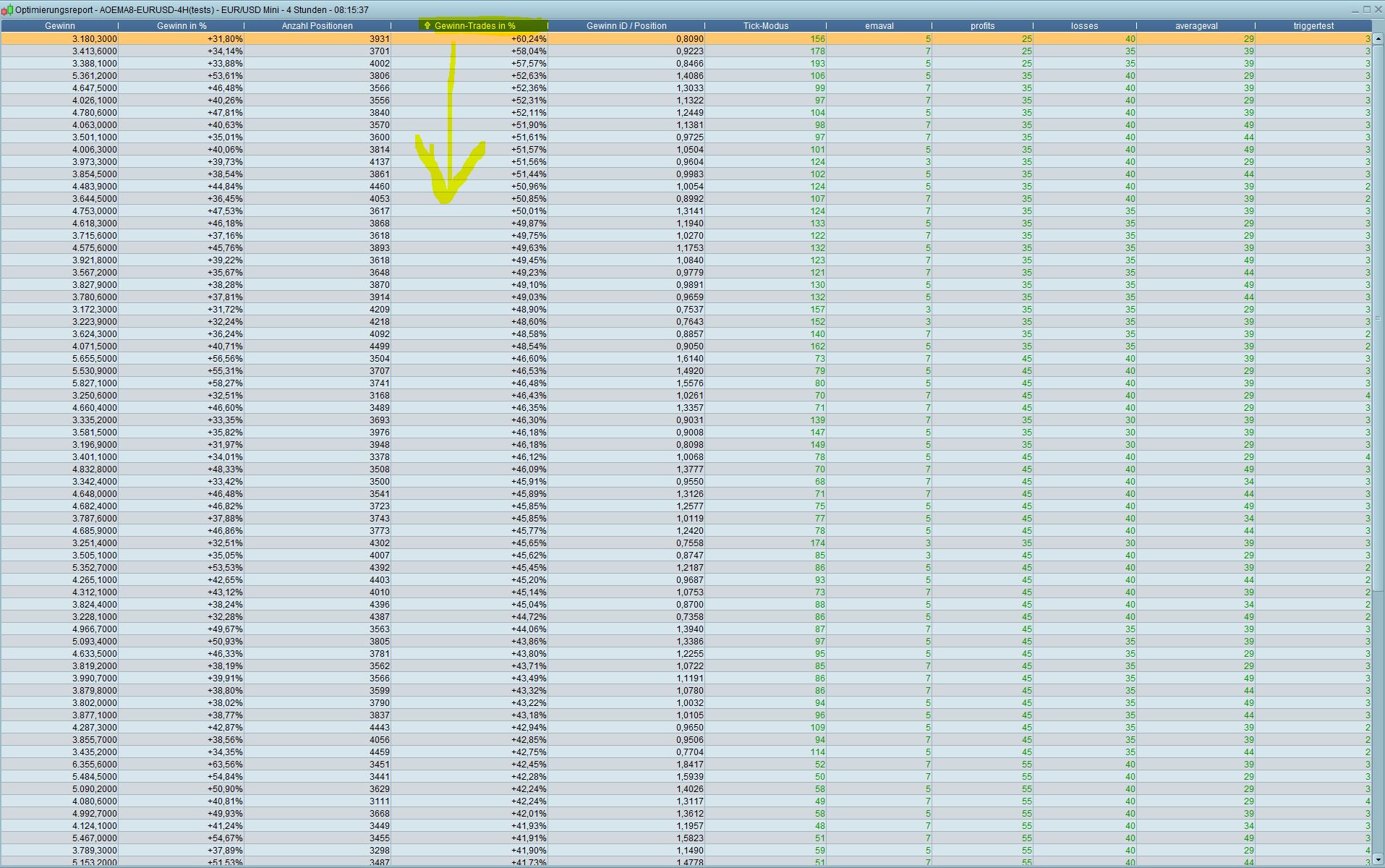

Test 100.00 Sorted By Profit Trades%

But really all you have done there is now curve fit it to all the data that Razz has?

RazzParticipant

Master

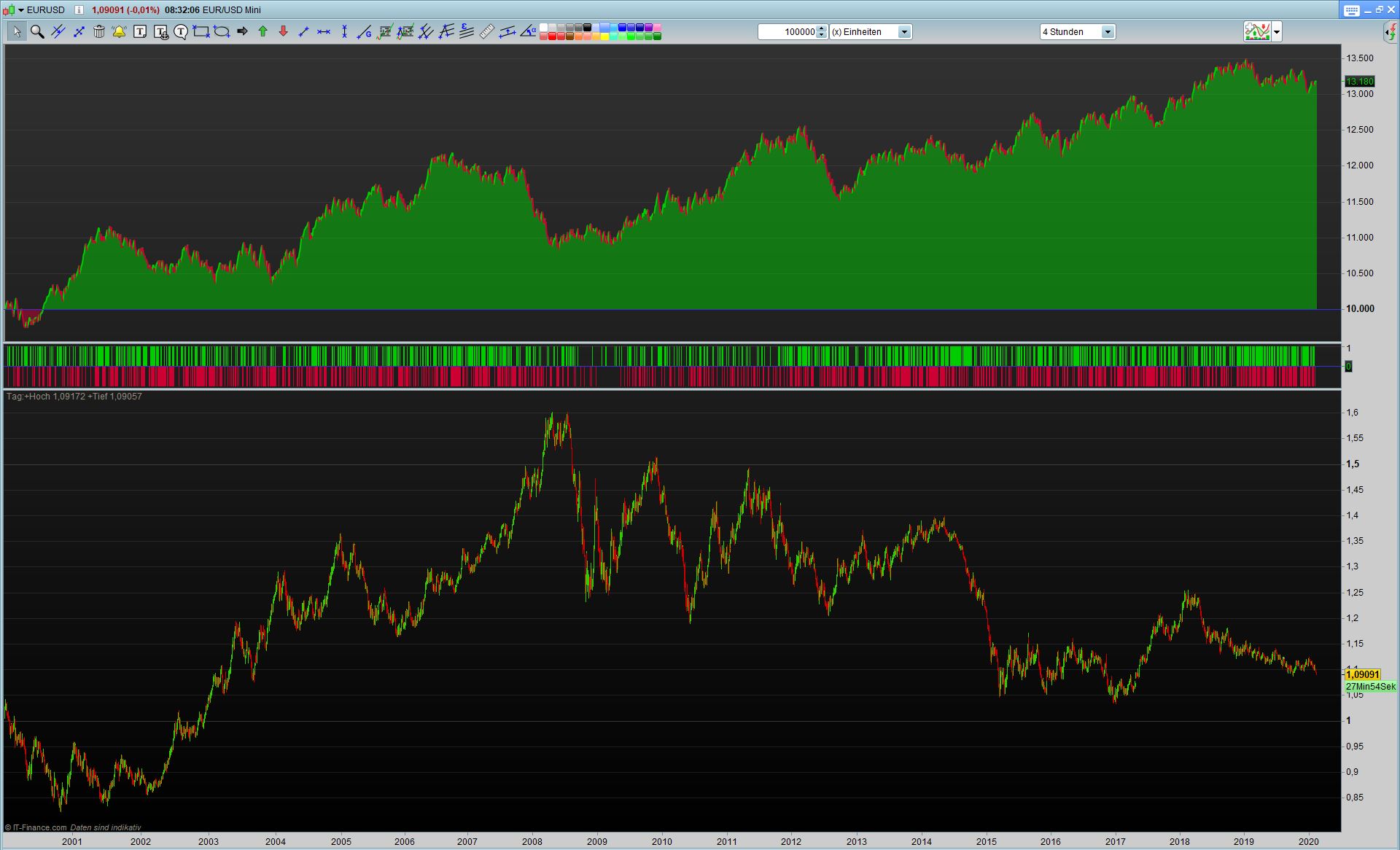

further back like 02.1.2000 I can not come with 200,000 units Sorry.

I did the walk forward maybe it will help you

@Vonasi, i haven’t changed the strategy but just prepared some parameters and ranges in line with my losses/profits tolerances for @Razz to do the test.

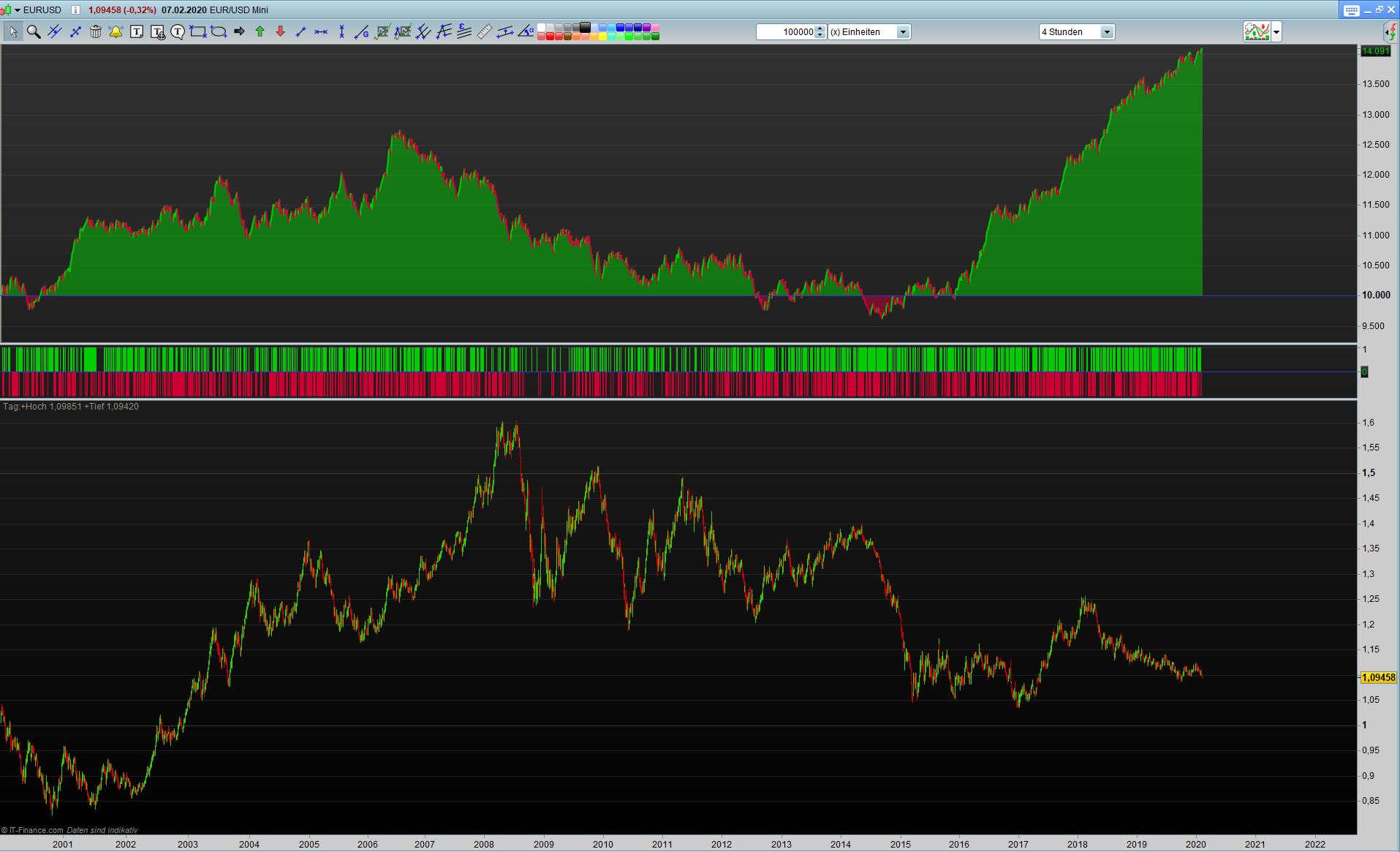

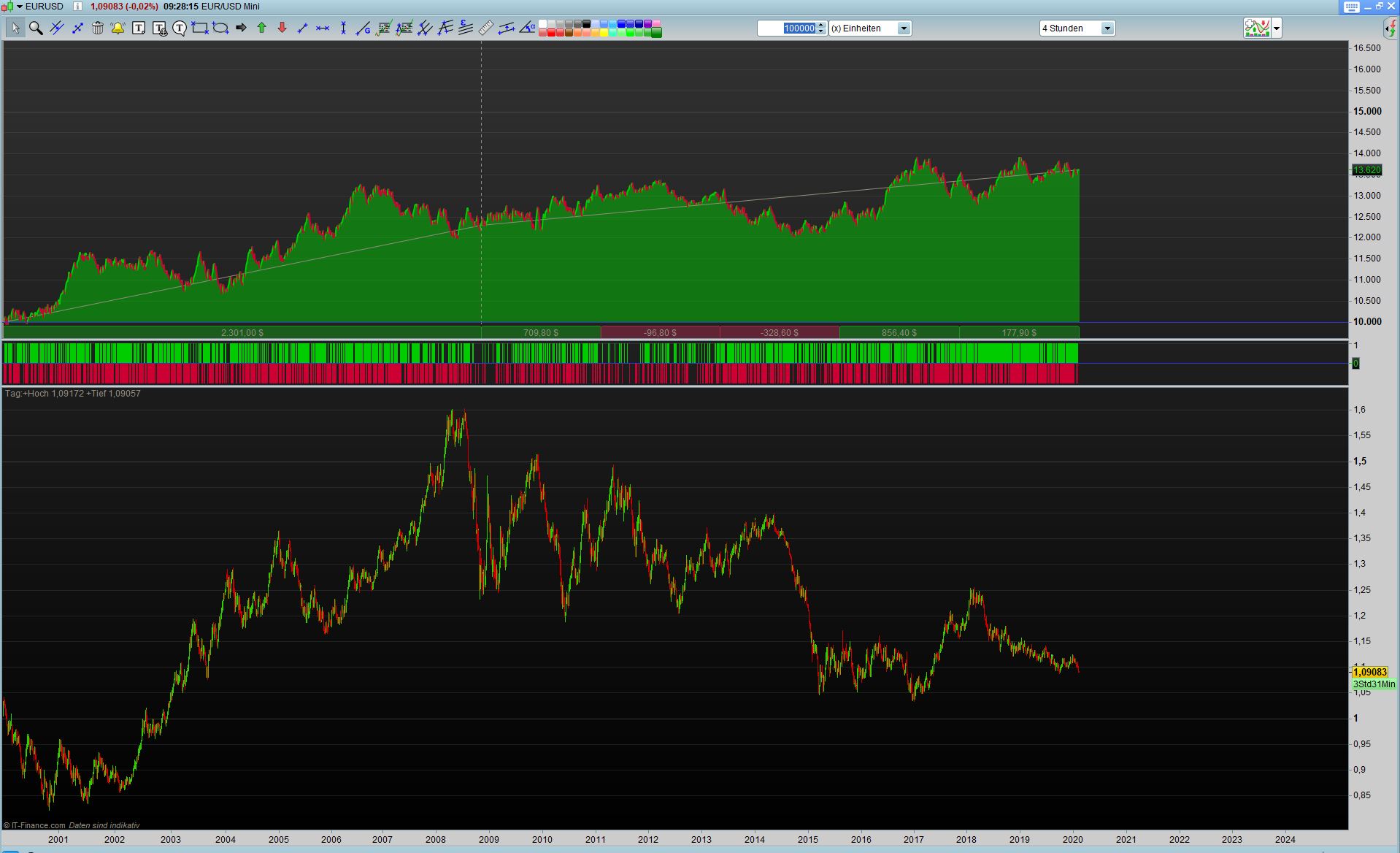

It looks like the performance is indeed not great before 2014 for some reason..