JS

JSParticipant

Veteran

Thanks, the 10-minute timeframe originally comes from another system I ran, that system was based on the size of the difference between two candles, for example (Close – Close[1]), where the magnitude of the difference could indicate a potential trend reversal…

In that system, I achieved the best results with a 10-minute timeframe and I also find that this timeframe best reflects the dynamics between buyers and sellers, hence the 10 minutes…

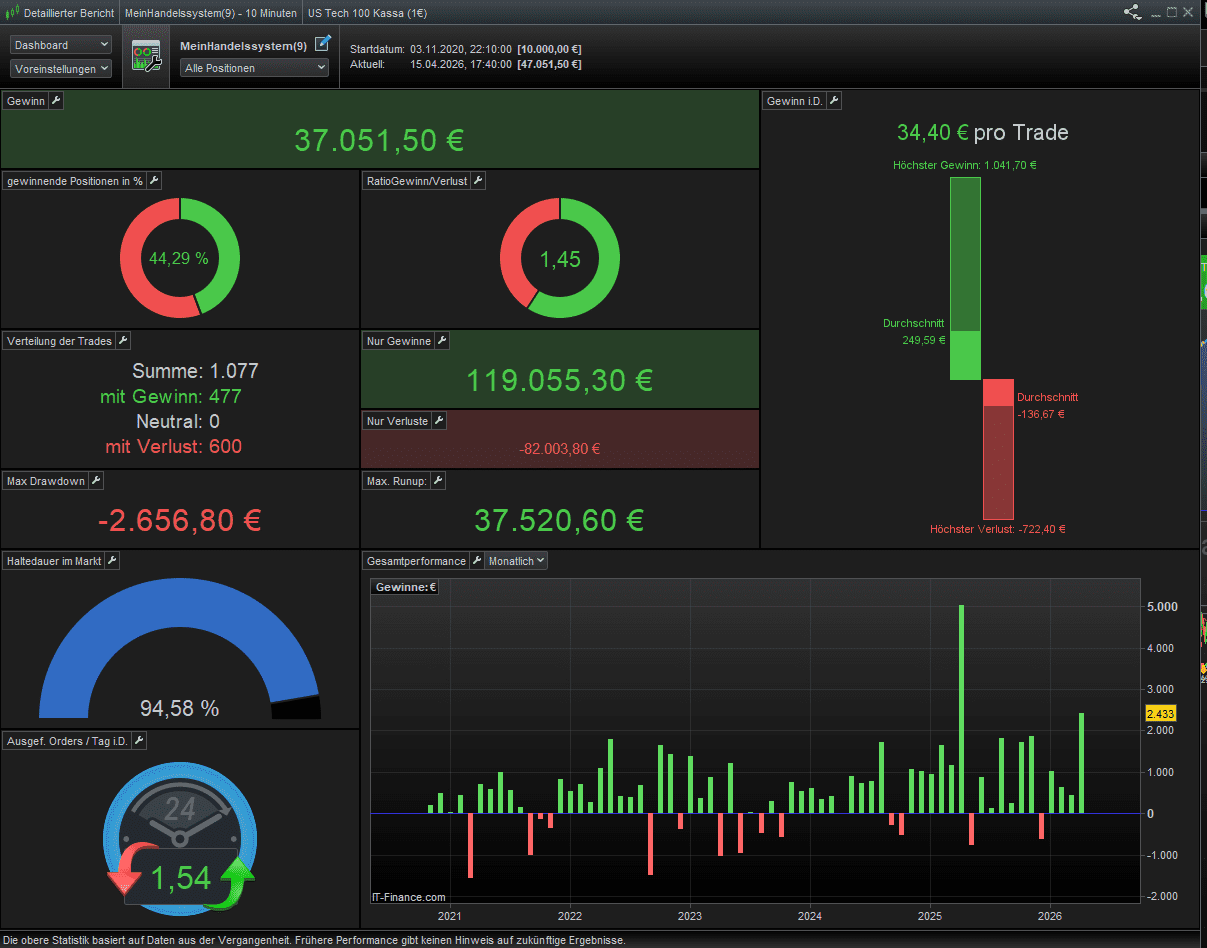

Thanks for the post JS! Are you trading this with IG CFD contracts or Futures on IB/IG? As its 100% time in market, I reckon it would be impossible to trade this on IGs cash contract as the fee’s would eat all profit, correct?

JSParticipant

Veteran

Hi, that’s right, I use futures via IB…

The results are fantastic! I initially had doubts about whether the price structure would work, but you have absolutely proven the concept.

I do have one question: You mentioned that trades are triggered by a break in structure, so why was there a 16-minute gap between trades? Does the system not always flip immediately from long to short?

JSParticipant

Veteran

Hi Dipont,

Thanks, in principle, the position is always reversed immediately, except in one case: when the “emergency stop” is triggered. In that situation, positions are closed and the system waits for the next signal…

I have rebuilt your system using this concept on the Nasdaq CFD ($1 per point). While it is challenging to reach a 1.85 Profit Factor and match your great win rate, I am already very pleased with it. My focus now is on refining the logic to reduce the size and frequency of losses. I hope this isn’t another case of overfitting.

JSParticipant

Veteran

It looks good, and for a fair comparison, the profit should be multiplied by two (74,103), since IG uses a point value of 1 dollar and IB uses a point value of 2 dollars…

Remarkably low drawdown and over 94% market exposure — nice…

JSParticipant

Veteran

Before you start comparing everything, you should know that there is a significant difference between IG and IB, and it’s not just the price difference between a CFD and a future…

I’ve never managed to achieve the same results with IG as I did with IB…

… so you two now sucking all the money from the markets! please leave few cents for me as well 😀

Dipont,

It seems from you screen shot that you are trading the cash instrument. Are you considering the overnight cost in the results? Or are you exiting daily before the overnight charges are applied?

I guess in JS case, since he trades the Futures, those charges are not a thing, as there are captured in the Future instrument price as contango and maybe why he, at some point says, the short trades are better R:R (decay working in his favor).

Thanks for the tip. I know about CFD costs and spreads—that’s why my live runing systems exposure is usually below 15%. With CFDs, you have to be a sniper, not a diver.

I like this system because it’s a 60-line proof of concept for SMC. You can define the periods and pick entries/exits to boost PF and win rate. I’ve built many systems with different concepts, but this one stands out. Another concept I haven’t been able to prove with a trading system is Supply and Demand. If anyone could provide a breakthrough, I would be deeply grateful.

I’m still impressed by JS’s PF and win rate, especially with his higher market exposure.

By the way my backtesting performs much worse now with the same settings, which shows it’s too fragile. I need to fix that.

You have over 90% market time. If you trade CFDs and consider overnight fees during all these years, your system is probably no longer profitable, unfortunately.

I’m aware of that. I wouldn’t go live with CFDs under these conditions. However, even if you pay the overnight fee every day, it still amounts to less than 20% of the total profit