Hi Guys,

To continue my trials and tests to confirm that the strategy is of no importance in the results of an algorythm and results of OOS we will do another test with the Repulse Indicator (A previsouly indicated for me the most important things to work is Money Management, Market structure, Simplify and optimize code, indicator (it should work with all but some give better results) and so on …

Because if the strategy has no importance we should have pretty good results with any Signal Indicator with more or less luck it should work

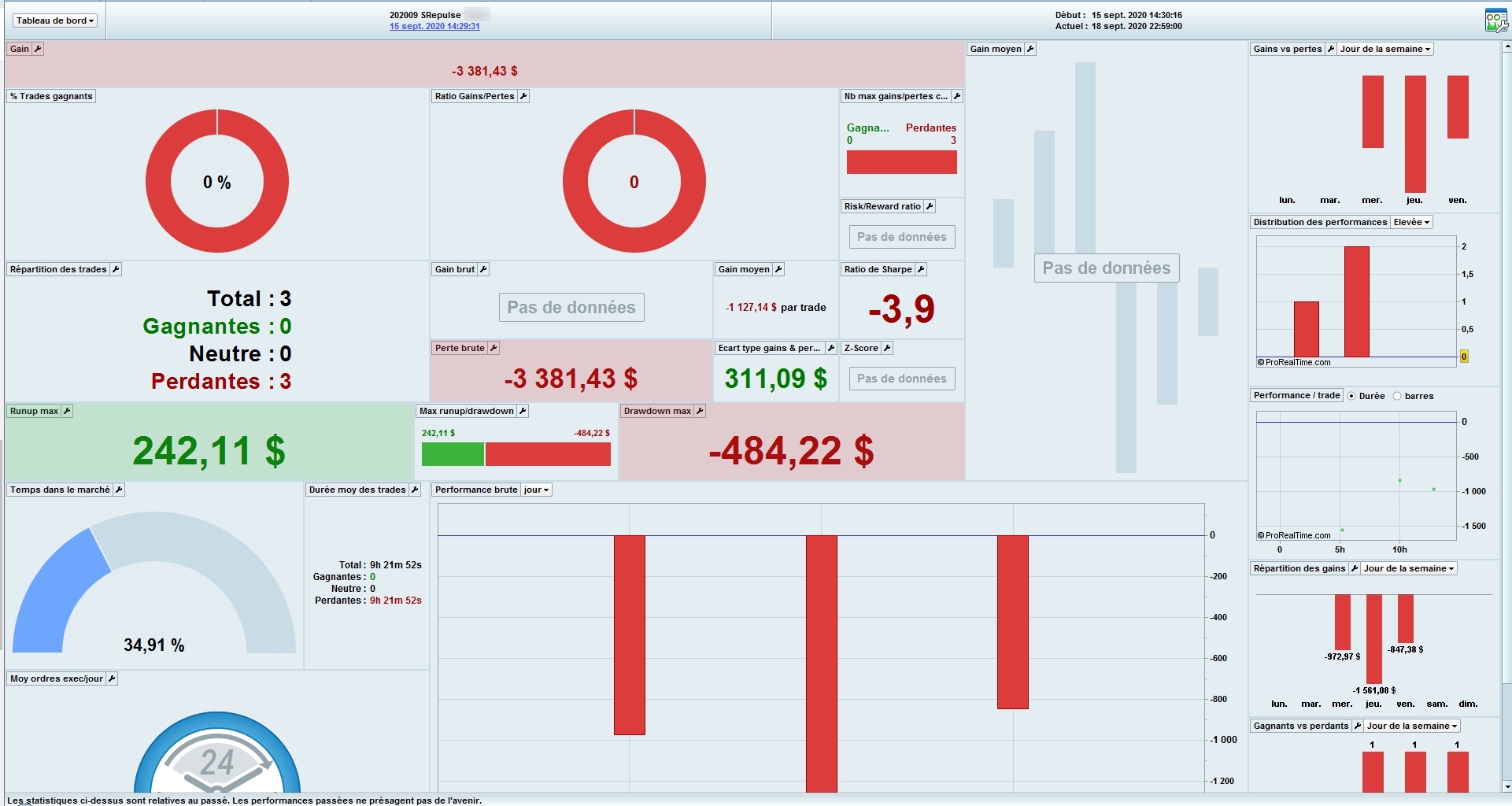

But for now with the previous algo it doesn’t work as you see on the picture 🙁

So, I modify the analyze of the market structure and add some improvments and we will do a test all this week

Same test : EUR/USD 1 mn Backtest IS 100 000 units 3 variables, one for Signal, one for market structure one for money management

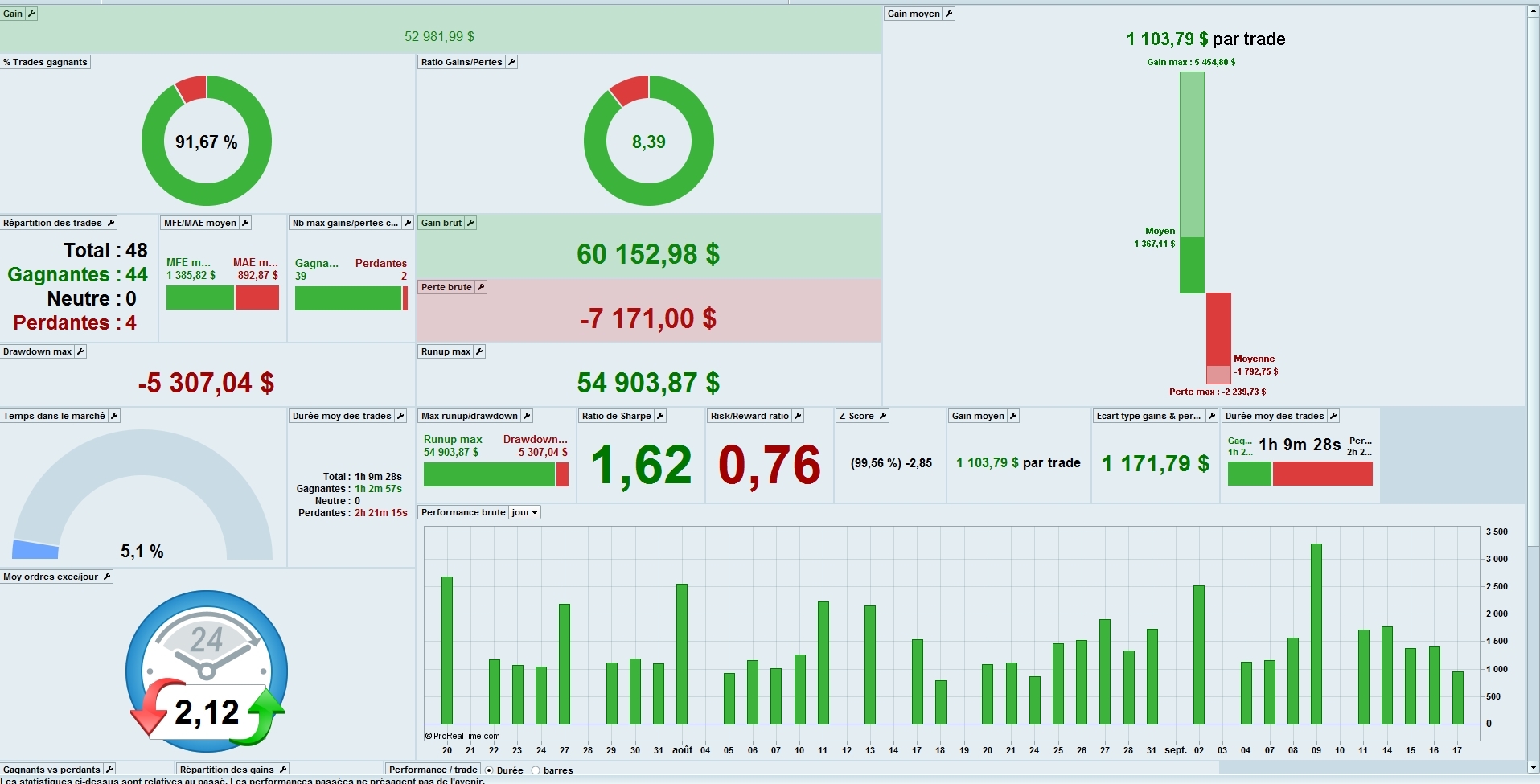

And lets go. You will find here the results of the IS backtest 91 ,67 % winners 8.39 Win/Loss Sharpe 1.62.

It’s the first step, but I think a Donkey can have pretty good results on IS Backtest so it’s not very important (It’s just linear regression on x Variables). To have good results on OOS is the second and more difficult Step

And I choose the variables as previously indicated on the CCI file

Have a nice week and see U on Friday

see U on Friday

Why wait until Friday?

If you optimise over the first / most distant 70,000 bars and then run over the full 100,000 bars you would have an OOS period of the most recent 30,000 bars to see if your theory is a winner?

Or to make the whole process quicker for yourself

Use a 60,000 bar period … optimise over the first / most distant 45,000 bars and then run over the the most recent OOS 15,000 bars and then post the results please?

Just what I do in my trading systems …… but there are those who do exactly the opposite and re-optimize everything every week or month because they consider the only way to always keep up with the market.

I don’t think one is right and the other is wrong, and just a different way of looking at things.

I got the impression that most on here think they can do all manner of Backtesting, Walk Forward, Monte Carlo, Robustness Testing etc etc and it will be right first time and then stay right forever?

I take a ‘horses for courses’ approach … whatever will get me profit. That could be … ‘if it ain’t broke don’t fix it’ all the way to … ‘a tinker every week’!! 🙂

Use a 60,000 bar period … optimise over the first / most distant 45,000 bars and then run over the the most recent OOS 15,000 bars and then post the results please?

Thanks for this reminder on how to make a simple walk forward test 😉

I’m now on Holidays until saturday @grahal 😁

@grahal

Yes you’re right but it will be à single pass of Walk forward and only on 70 000 units and not 100 000 units (big différence) and as the most is the better.

In my expérience less unit you have more linear will be your equity curve on IS backtest and more différent will be your OOS

But you’re right why not

the most is the better.

I’m not so sure of that any more … esp since the March 2020 big drop … this drop influences variable values so much that such values don’t work good on price action since March 2020?

I’m getting good Forward Test results recently from optimising over 1,000 to 10,000 bars (depending on TF) and the bonus is … it’s so much quicker to backtest!

Maybe I’ve just not got enough life left to backtest over 100,000 bars any more!!?? 🙂

@grahal

I think nothing change. The more data you have the more event in price you have inside and we can think that after some time, same events on price can reproduce (fractal..)

IF you do backtest on only 10 000 bars you have à big big probability to have OOS results very différent. Make demo OOS and you will See. And remember that backtest on IS is easy and only the first step

The more data you have the more difficult it is to have à linear equity curve but you will have better corrélation on OOS. And the opposite with only 10000 bars

I think the sole exception is if you can have à lot of trades on only few bars. Like with SAR indicator for example. With him you can have quite 100 trades on only 10 000 bars

Bye

IF you do backtest on only 10 000 bars you have à big big probability to have OOS results very différent.

Yes and no. If the market behaves the same way as in the previous 10k bars, IMHO, the OOS should be ok. Same goes for 20k, 50k or 100k bars. In fact we can’t never be sure and there is not a single way to use the WF tool.

The IS+OOS sequence is a test do determine when we should re-optimize the strategy (if the strategy is optimized though).

Hi @nicolas

Yes, but the probability thé price have thé same behaviour in the same oos time is very very low, notably on forex (See all failures on determining cycle in price). For me price evolve randomly and so thé probability to have thé same pattern is very low.

Have à nice day

For me price evolve randomly and so thé probability to have thé same pattern is very low.

I have found success judging that price has been in an uptrend for, for example, 1k or 10k bars (depending on TF). Not much judging involved … we can all see history! 🙂

Judging from Elliott Waves and Fib retrace / extensions … if I expect the uptrend will continue then an Algo based on that 1K or 10K bars as In Sample has a good chance of success.

The converse is true also.

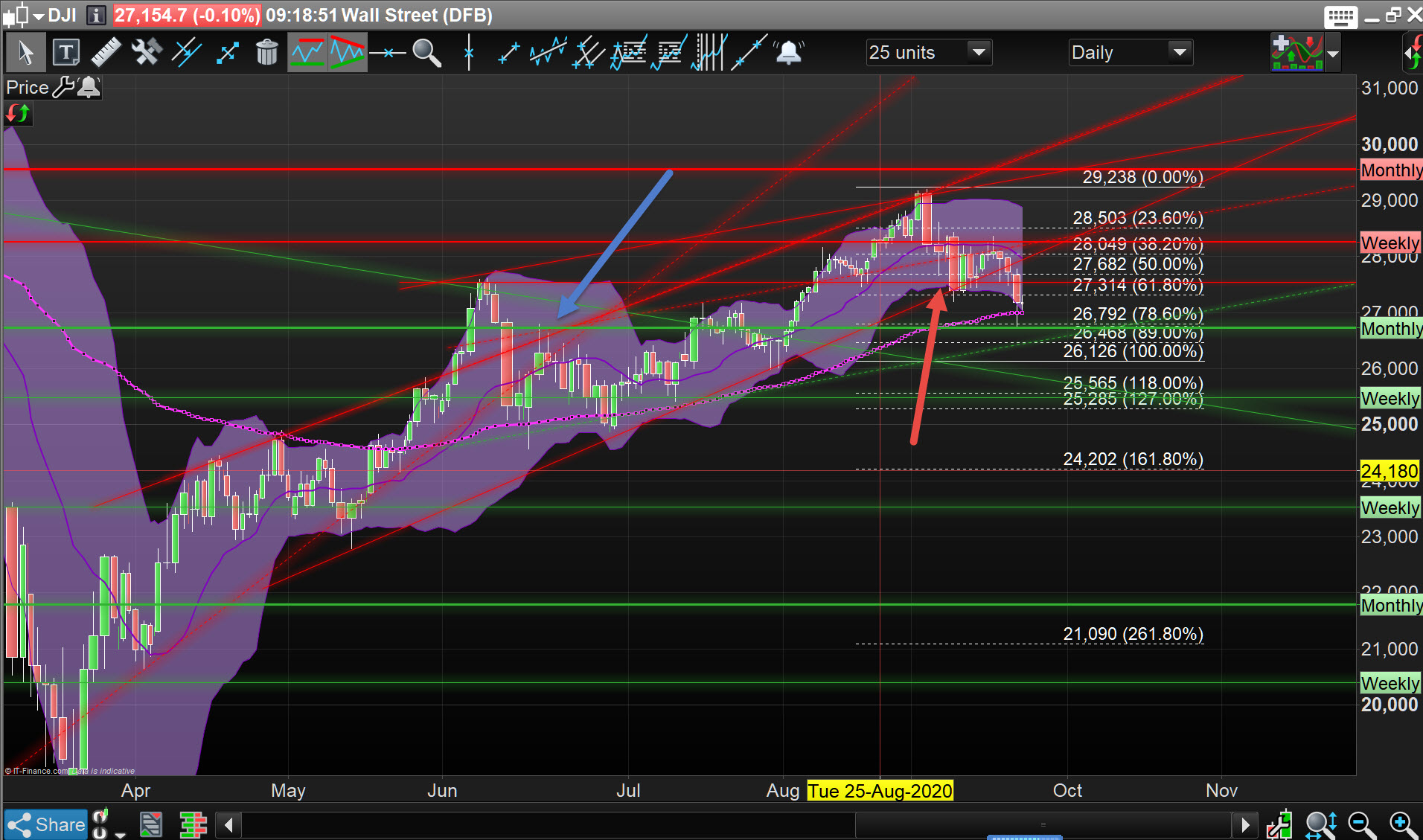

If a long uptrend and then a sharp correction as started on 3 Sep 20 … see red arrowhead on attached. Then it is best to base Algo on 10K bars (or whatever bars) that occurred during the last sharp correction (see blue arrowhead).

Using the 10K bars (or whatever) immediately prior (i.e. the last gasp of the uptrend) to the sharp correction will not be a good basis as an In Sample period.

Okay I know what you are going to say … this is why we use maximum history for optimising – 100K bars, 200K bars. My suggestion is a way round the interminable time that 100K bars takes to optimise.

My method above works for me … but time will tell for sure.

Thanks @grahal

As always it dépends on the market structure

Prices are à combinaison of repetable pattern, we hope to catch with algos, and more or less some random noise

If we are in an uptrend or down trend (but Who knows if it will continue ?), you can probably backtest on 10k only because the pattern will be the same on OOS and you can hope noise will be limited

But in market with permanent up and down (like forex for example) it won’t work because the 10k future won’t be the same as the past 10k, and you need many more bars to catch all variations of noise

There are some time I did only backtest on small period 10k 20k (for faster results) and the backtest on IS was marvelous but very bad on OOS. Since I use at least 100 k (on forex) i have à better corrélation IS/OOS (but it’s much more difficult to have marvelous IS backtest and max drawdown are bigger (it’s normal)

Smaller is your IS backtest more linear will be your equity curve Smaller will be your max drawdown but in an up and down market worst will be your OOS results

But you’re right à backtest on 10 k is much faster than on 100k

Thanks for the interesting discussion

Everyone in building trading systems has their own beliefs … if it’s better in one way or better in another way, there is only one thing that is important … how much can you earn …… clearly as a percentage because one can have 5000 and another 500,000.

As for Forex, I think it is much easier to do Scalping than to build trading systems that make you earn.

Hello