Dear people,

(maybe skip because it is too hard to explain)

In order to explain what I mean, I best describe practice :

When you fill the spread in de (backtest) Editor, you (I) can easily see that it behaves exactly as expected. In attachment 1 and 2 this is the yellow line, and it perfectly matches the spread vs contractamount. Also, my self-calculated gain (not via PositionPerf) always matches the backtest and forward testing. Until … until I start to add position underway. Now, it is relatively complex to check the merits of everything because we’re obviously dealing with averages for position and taken spread (mind you, still backtest / forward test). And, I don’t think I have to tell you that once I have a gain of +100 and take extra position, the gain drops steeply, like 50% when adding the same amount of position as already was in there *plus* additional spread. I can summarize this with : No, I can not mimic that myself, graph it like the examples in the attachments and *now* that I am doing this 100% OK.

This lead to using PositionPerf instead of my own calculations, with the lucky outcome that now my graphs do what I expect, only by a simple replacement of MyOwnGain with PositionPerf. Except …

Except for that PositionPerf does not contain any spread at all;

Nicolas explains in his documentation that no BrokerFee is contained in PositionPerf (which is logic) but this thus also doesn’t contain spread. Well … in Backtesting / Forward testing that is, and how to know it is there in Live …

I was able to add the theoretical spread myself (PositionPerfReal – PositionPerf + Spread) and as I told in the earlier post, that matches to the cent what appears in the closed orders list (and the gain), *also* for added position. Thus, it seems that I overcame the hurdles and at least now can do how the backtesting has been programmed. Unfortunately that does not match reality. A reality which I also always can “match” and sync with forward (or back) testing (except for the varying real spread), but I can NOT accomplish that with additional position.

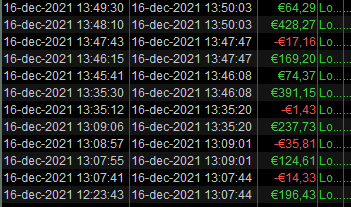

If you’d scroll back to my first post with screenshot of live … compare that with the 3rd attachment of backtesting below. This is not from the same data (time period), but you will believe me if I tell you that none of these “0 bars” exits ever goes negative, because I just don’t allow it (although the lot could run into a very occasional StopLoss). Thus with backtesting / forward testing this is always 100% positive + positive, while with live this is in 90% of cases positive with negative. And this is because my mechanisms to also make that additional trade positive, apparently don’t work. And in the base it uses the exact same PositionPerf + Spread to see what I’m at.

I can make it even more challenging by telling that I surely am able to let all be positive + positive in Live, but this is with my own math of the gain, and unfortunately I can not graph that (it is just too complex to do because of too many variables must be taken into account …).

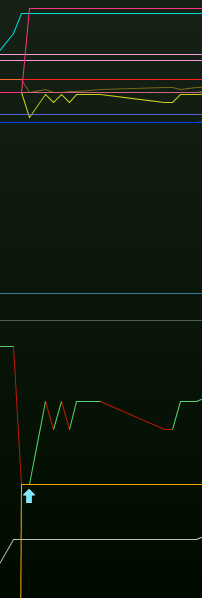

In the 4th attachment I try to show you how complex things actually are, while telling you that here the graphing works as should. The blue UpArrow buys additional position, which readily makes drop the gain line (green) right above the white vertical line, but where the vertical scaling is not adjusted.

We know that a. the spread hammers upon that additional buy and b. that in this case the price also drops right after the buy (see the pink cross and eventually the pink triangle). Thus is seems evident that there can’t be any gain in this second buy. Still the backtest shows 277,52 for the original position and 105,78 for the additional buy. My graph shows 368 prior to the first drop you see and it shows a final PositionPerf incl. spread of 232. The 368 ~ resembles the two trade results (277 + 105) and the 232 is nowhere close. And you know what ? the real Live trade would show probably 350 or so minus ~20 for the additional trade. And with all the cases I examined, this looks right. Same as you see in the 3rd attachment … this looks right to lose in the additional trade. But it looks right with my own graphing ?

So I am in a kind of vicious death circle. I can’t control it.

And then to think that this was the answer to nontheless’s question. 🙁