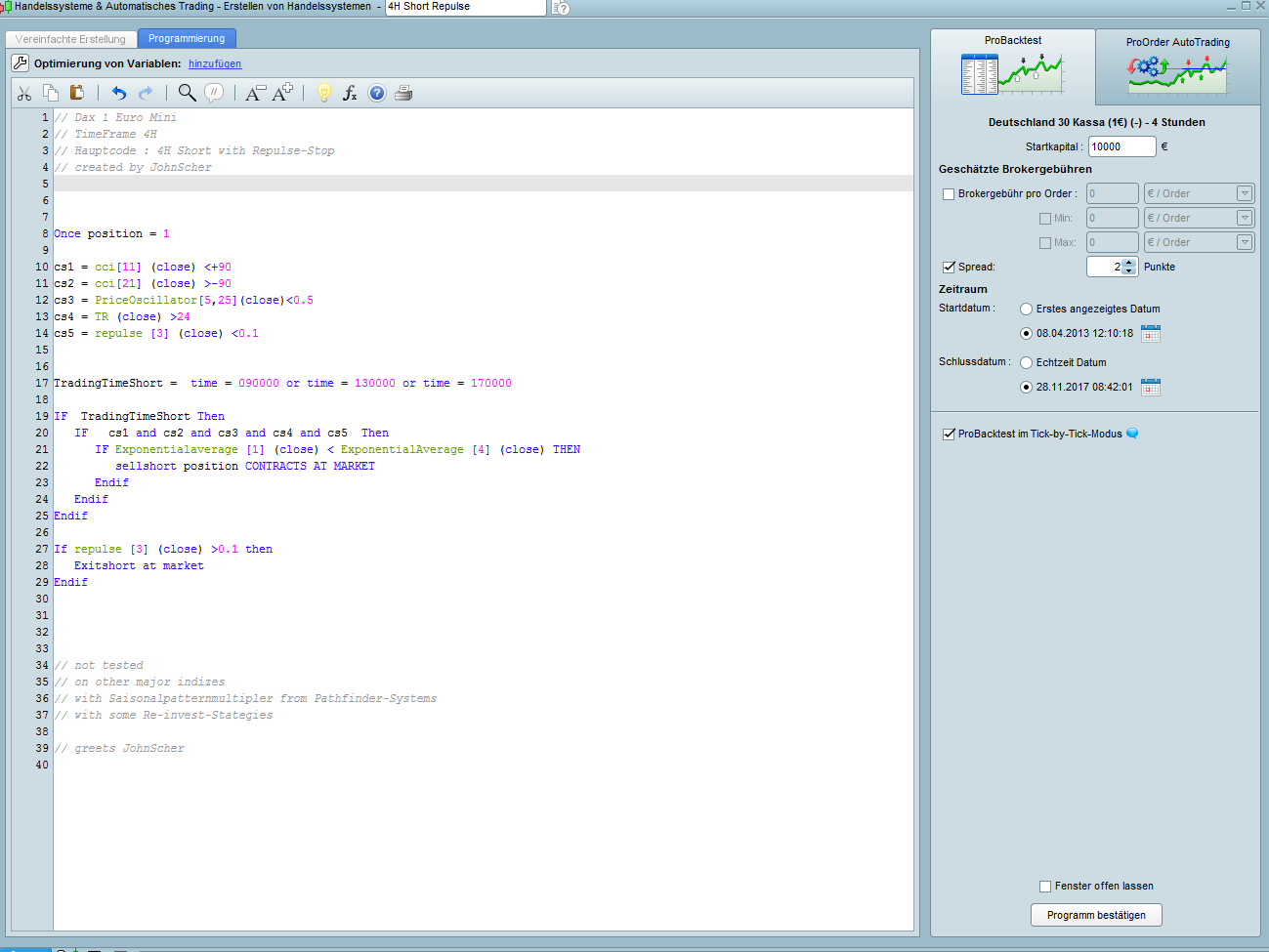

// Dax 1 Euro Mini

// TimeFrame 4H

// Hauptcode : 4H Short with Repulse-Stop

// created by JohnScher

// tested 08.04.2013 - 26.11.17 with PRT 10.3

// 2 Points Spread

// won 161 loose 212

// max DrawDown 853 Euro max RunUp 5.035

// winnings total 4,473 Euro

defparam flatafter = 210000

defparam cumulateorders = true

Once position = 1

cx1 = cci[11] (close) <+90

cx2 = cci[21] (close) >-90

cx3 = PriceOscillator[5,25](close)<0.5

cx4 = TR (close) >15

cx5 = repulse [3] <0.1

TradingTimeShort = time = 090000 or time = 130000 or time = 170000

IF TradingTimeShort Then

IF cx1 and cx2 and cx3 and cx4 and cx5 Then

IF Exponentialaverage [1] (close) < ExponentialAverage [4] (close) THEN

sellshort position CONTRACTS AT MARKET

Endif

Endif

Endif

If repulse [3] >0.2 then

Exitshort at market

Endif

// not tested

// on other major indizes

// with Saisonalpatternmultipler from Pathfinder-Systems

// with some Re-invest-Stategies

// greets JohnScher

hi there.

Is it correct and clean coded?

I would like to ask if someone can check the results of the backtest and let you know if they have the same results?

kind regards

JohnScher

This is what i get with spread=2.

BTW: This post belongs in the proorder section.

Hi, thanks a lot!

You have gone much further back with the beginning of the backing test.

Can PRT return the data back valid so far? That would be very nice.

I would like to check this again and ask you if you can give me the exact start date of your back test?

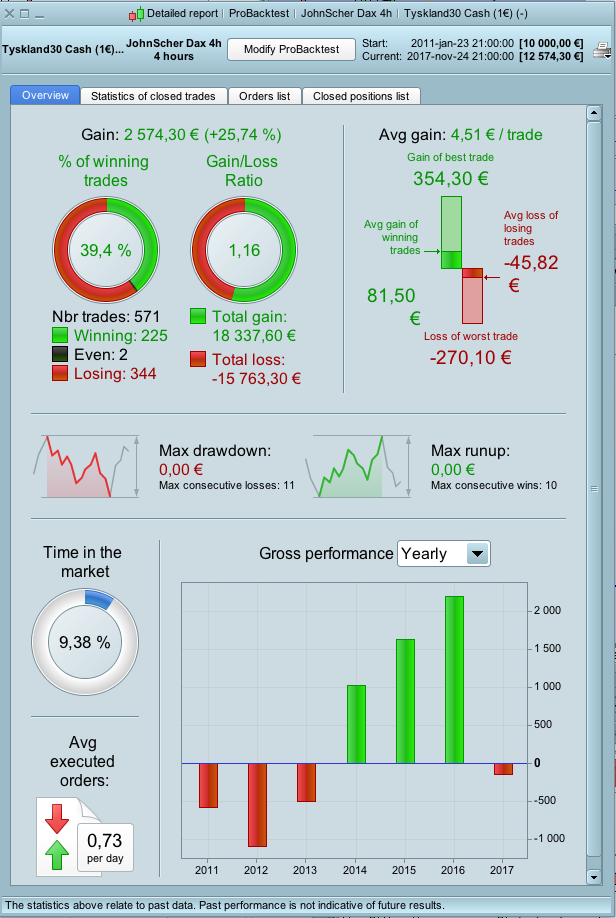

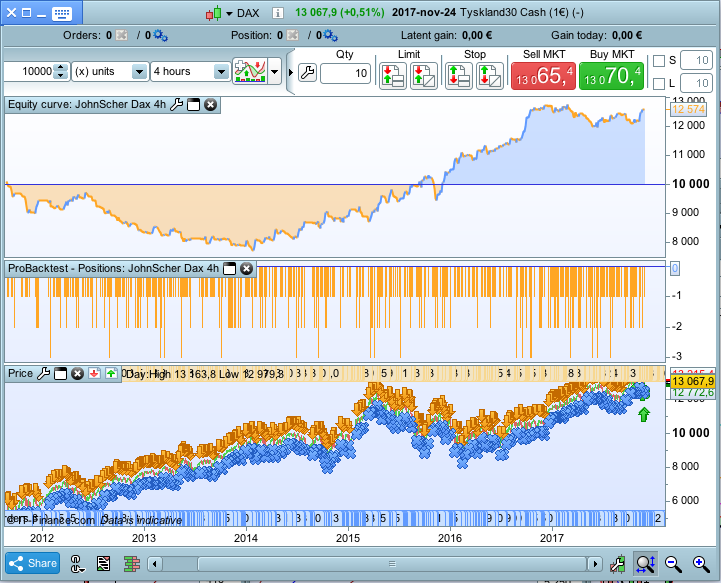

This was a 10000 bar backtest starting 23rd january 2011 (as you see on the first picture).

Thank you very much again.

I don’t have that result.

I’ll try to find the bug and then report back to you.

So thank you again!

Hello again.

I couldn’t find any mistakes.

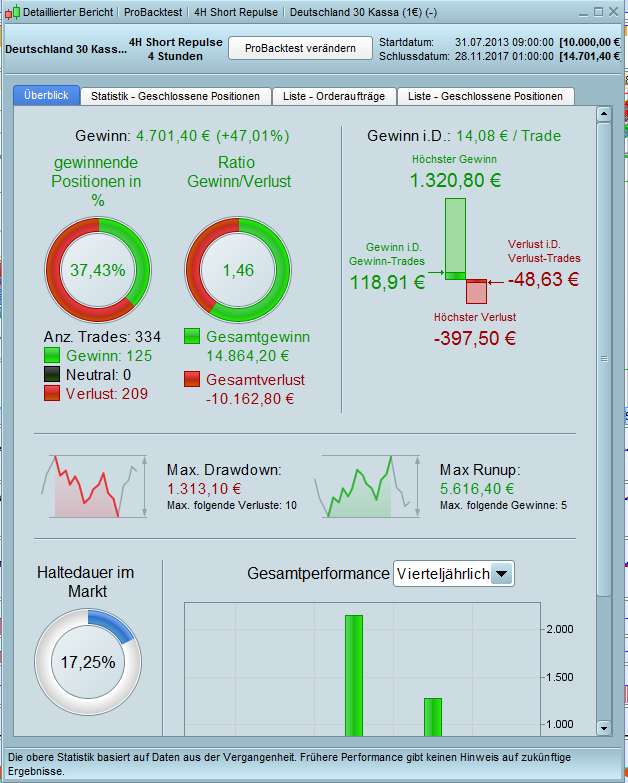

But here are the screenshots.

Strategy in the demo version

//-------------------------------------------------------------------------

// Hauptcode : 4H Short Repulse

//-------------------------------------------------------------------------

// Dax 1 Euro Mini

// TimeFrame 4H

// Hauptcode : 4H Short with Repulse-Stop

// created by JohnScher

// backtest 08.04.2013 - 26.11.17 with PRT 10.3

// 2 Points Spread

// won 161 loose 212

// max DrawDown 853 Euro max RunUp 5.035

// winnings total 4,473 Euro

defparam flatafter = 210000

defparam cumulateorders = true

// define saisonal position multiplier for each month 1-15 / 16-31 (>0 - long / <0 - short / 0 no trade)

ONCE January1 = 3 //0 risk(3)

ONCE January2 = 0 //3 ok

ONCE February1 = 3 //3 ok

ONCE February2 = 3 //0 risk(3)

ONCE March1 = 3 //0 risk(3)

ONCE March2 = 2 //3 ok

ONCE April1 = 1 //3 ok

ONCE April2 = 3 //3 ok

ONCE May1 = 1 //0 risk(1)

ONCE May2 = 2 //0 risk(2)

ONCE June1 = 1 //1 ok

ONCE June2 = 2 //3 ok

ONCE July1 = 3 //1 chance

ONCE July2 = 2 //3 ok

ONCE August1 = 2 //1 chance 1

ONCE August2 = 3 //3 ok

ONCE September1 = 3 //0 risk(3)

ONCE September2 = 0 //0 ok

ONCE October1 = 3 //0 risk(3)

ONCE October2 = 2 //3 ok

ONCE November1 = 1 //1 ok

ONCE November2 = 3 //3 ok

ONCE December1 = 3 // 1 chance

ONCE December2 = 2 //3 ok

// set saisonal multiplier

currentDayOfTheMonth = OpenDay

midOfMonth = 15

IF CurrentMonth = 1 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = January1

ELSE

saisonalPatternMultiplier = January2

ENDIF

ELSIF CurrentMonth = 2 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = February1

ELSE

saisonalPatternMultiplier = February2

ENDIF

ELSIF CurrentMonth = 3 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = March1

ELSE

saisonalPatternMultiplier = March2

ENDIF

ELSIF CurrentMonth = 4 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = April1

ELSE

saisonalPatternMultiplier = April2

ENDIF

ELSIF CurrentMonth = 5 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = May1

ELSE

saisonalPatternMultiplier = May2

ENDIF

ELSIF CurrentMonth = 6 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = June1

ELSE

saisonalPatternMultiplier = June2

ENDIF

ELSIF CurrentMonth = 7 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = July1

ELSE

saisonalPatternMultiplier = July2

ENDIF

ELSIF CurrentMonth = 8 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = August1

ELSE

saisonalPatternMultiplier = August2

ENDIF

ELSIF CurrentMonth = 9 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = September1

ELSE

saisonalPatternMultiplier = September2

ENDIF

ELSIF CurrentMonth = 10 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = October1

ELSE

saisonalPatternMultiplier = October2

ENDIF

ELSIF CurrentMonth = 11 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = November1

ELSE

saisonalPatternMultiplier = November2

ENDIF

ELSIF CurrentMonth = 12 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = December1

ELSE

saisonalPatternMultiplier = December2

ENDIF

ENDIF

//-------------------------------------------------------------------------------------

Once position = 1

cs1 = cci[11] (close) <+90

cs2 = cci[21] (close) >-90

cs3 = PriceOscillator[5,25](close)<0.5

cs4 = TR (close) >24

cs5 = repulse [3] (close) <0.1

TradingTimeShort = time = 090000 or time = 130000 or time = 170000

IF TradingTimeShort Then

IF cs1 and cs2 and cs3 and cs4 and cs5 Then

IF Exponentialaverage [1] (close) < ExponentialAverage [4] (close) THEN

sellshort position*saisonalPatternMultiplier CONTRACTS AT MARKET

Endif

Endif

Endif

If repulse [3] (close) >0.1 then

Exitshort at market

Endif

// not tested

// on other major indizes

// with some Re-invest-Stategies

// greets JohnScher

I moved the topic to ProOrder support.

Thanks.

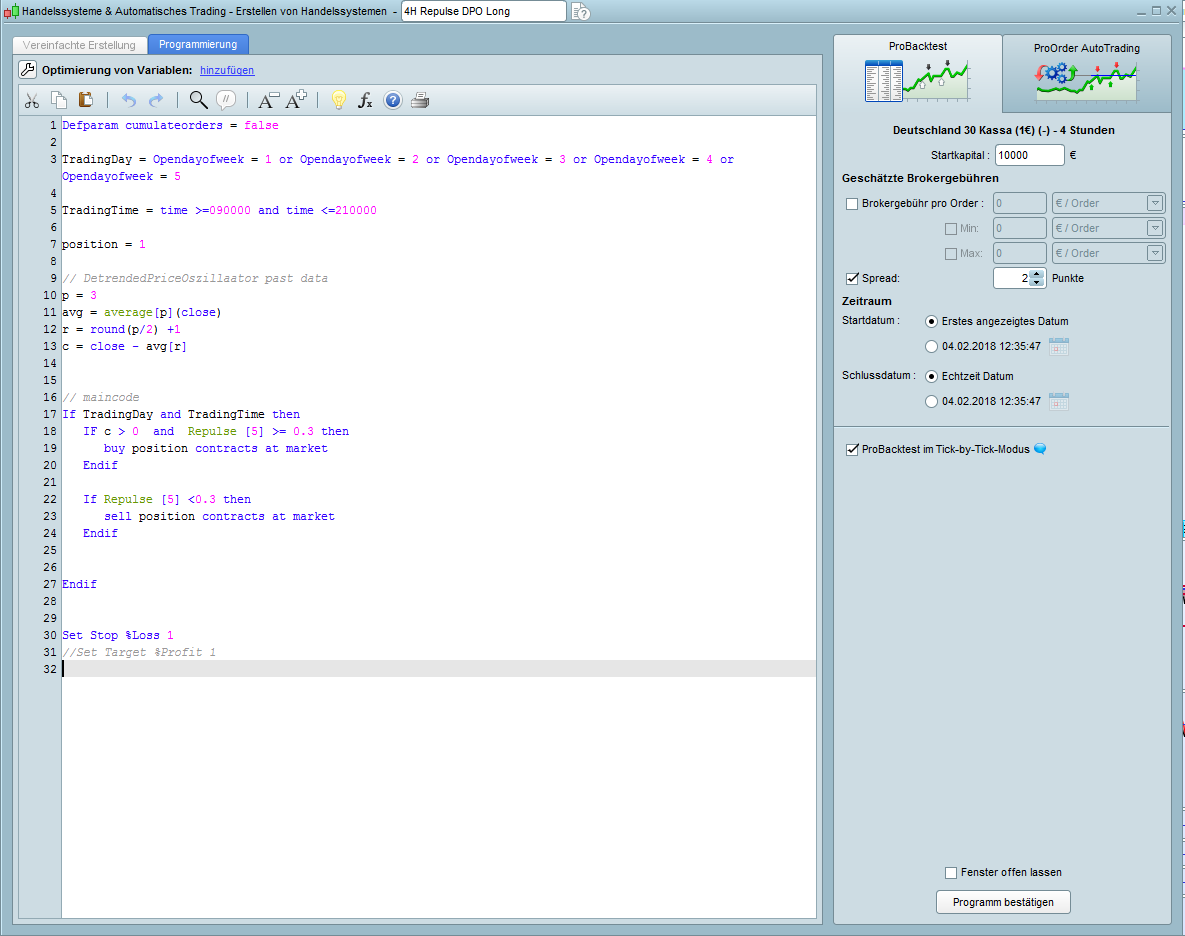

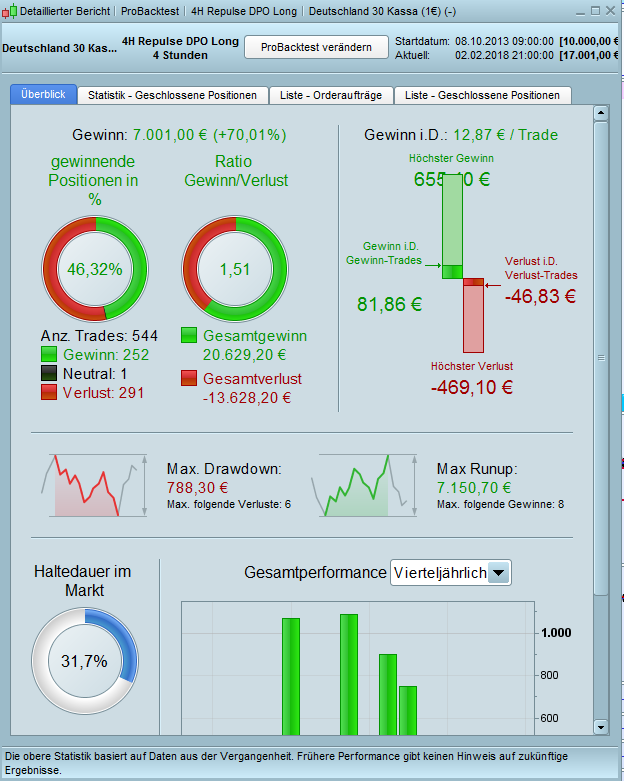

I converted the 4H Short with Repulse Stop into a 4H Long with Repulse Stop.

In this way..

Defparam cumulateorders = false

TradingDay = Opendayofweek = 1 or Opendayofweek = 2 or Opendayofweek = 3 or Opendayofweek = 4 or Opendayofweek = 5

TradingTime = time >=090000 and time <=210000

position = 1

// DetrendedPriceOszillaator past data

p = 3

avg = average[p](close)

r = round(p/2) +1

c = close - avg[r]

// maincode

If TradingDay and TradingTime then

IF c > 0 and Repulse [5] >= 0.3 then

buy position contracts at market

Endif

If Repulse [5] <0.3 then

sell position contracts at market

Endif

Endif

Set Stop %Loss 1

//Set Target %Profit 1

That should go far enough good. If necessary, can someone check the backtest result?

However, I have a question about Repulse.

This is provided by PRT as an indicator. I would like to check how the repulses relate to the rejecting average.

For example, for

Is it profitable? when you go long

if the reject average >0 and the repulse crosses the reject average upwards

if the reject average <0 and the repulse crosses the reject average upwards

Unfortunately my programming skills are not so good, so I wanted to ask if someone could put the code for the repulse in here? I could then continue my deliberations.

Enclosed the last picture. The red line is the rejecting average.

Translated with

http://www.DeepL.com/Translator

Translated with

http://www.DeepL.com/Translator