Razz

RazzParticipant

Master

Hi

I want my trading system to only do 3 trades a day, what do I have to do?

I don’t know what to do next

Thank you

once Tradetag=0

If onmarket then

Tradetag=date

endif

If not onmarket and time>= Startzeit and time < Endzeit and Tradetag<>date and Spannepoints < MaxBox then

BUY Position Lot AT Hi+L Stop

Sellshort Position Lot AT Lo-S Stop

Try this, it should work.

if intradaybarindex = 0 then

countposition=0

endif

condnbposperday=countposition <= 3

if not longonmarket and condition and condnbposperday then

buy 1 shares at market

countposition=countposition+1

endif

Mauro – your suggestion only works for at market orders. Razz’s example uses stop orders and so it is that a trade can be opened and closed within a candle. This means that simply adding one to a count does not work and using COUNTOFPOSITION does not work as the count would be zero at the candles close in this case.

We need to check both COUNTOFPOSITION and STRATEGYPROFIT at the candles close. Nicolas has a code snippet which hopefully he will share again here soon.

The problem is that Razz is using pending stop orders and so you can’t increase an order count each time you set them, but when they are actually triggered.

Try with this snippet:

if intradaybarindex=0 or day<>day[1] then

count=0

endif

if ( (not onmarket and onmarket[1] and not onmarket[2]) or (tradeindex(1)=tradeindex(2) and tradeindex(1)=barindex[1] and tradeindex(1)>0) or (not onmarket and onmarket[1])) then

count=count+1

endif

if count<3 then

...

endif

“soon” means at the same exact time Vonasi 😆

“soon” means at the same exact time Vonasi 😆

I knew you were fast but not that fast!

RazzParticipant

Master

Thank you for your help, I hope I entered it correctly. I watch how it works.

if intradaybarindex=0 or day<>day[1] then

count=0

endif

if ( (not onmarket and onmarket[1] and not onmarket[2]) or (tradeindex(1)=tradeindex(2) and tradeindex(1)=barindex[1] and tradeindex(1)>0) or (not onmarket and onmarket[1])) then

count=count+1

endif

if count<3 then

Trade=1

endif

If not onmarket and time>= Startzeit and time < Endzeit and Trade=1 and Spannepoints < MaxBox then

BUY Position Lot AT Hi+(Spread/2) Stop

Sellshort Position Lot AT Lo-(Spread/2) Stop

Thank you

It will not work as you never reset “Trade” to 0. You should do it like this:

if intradaybarindex=0 or day<>day[1] then

count=0

endif

if ( (not onmarket and onmarket[1] and not onmarket[2]) or (tradeindex(1)=tradeindex(2) and tradeindex(1)=barindex[1] and tradeindex(1)>0) or (not onmarket and onmarket[1])) then

count=count+1

endif

If not onmarket and time>= Startzeit and time < Endzeit and count<3 and Spannepoints < MaxBox then

BUY Position Lot AT Hi+(Spread/2) Stop

Sellshort Position Lot AT Lo-(Spread/2) Stop

RazzParticipant

Master

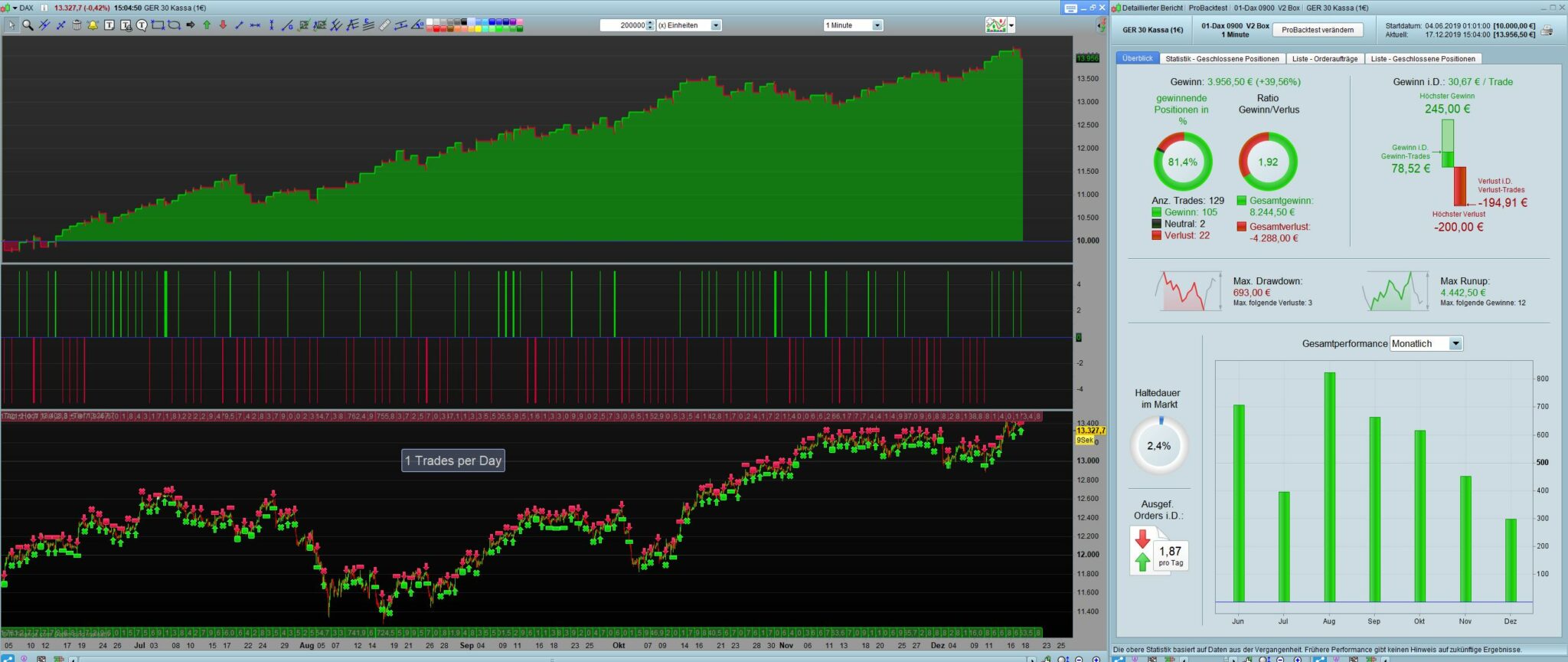

I probably did something wrong, in the picture all 3 systems. 2 trades are not ok

if intradaybarindex=0 or day<>day[1] then

count=0

endif

if ( (not onmarket and onmarket[1] and not onmarket[2]) or (tradeindex(1)=tradeindex(2) and tradeindex(1)=barindex[1] and tradeindex(1)>0) or (not onmarket and onmarket[1])) then

count=count+1

endif

if count<3 then

Trade=1

endif

If not onmarket and time>= Startzeit and time < Endzeit and Trade=1 and Spannepoints < MaxBox then

BUY Position Lot AT Hi+(Spread/2) Stop

Sellshort Position Lot AT Lo-(Spread/2) Stop

ENDIF

// Stops und Targets

SET STOP pLOSS Spannepoints*y

SET TARGET pPROFIT Spannepoints *x

RazzParticipant

Master

Thanks Nicolas the new code is better but he is still buying a position he is not allowed to.

please look at the Picture.

Many thanks for your help

Why not allowed?, the max position is set to 3 per day and I count 3 orders on your last screenshot.

RazzParticipant

Master

3 trades are ok, but the 3 entry must not be, condition should be that the Lo of the range 0800-0900 is the signal.

RazzParticipant

Master

Nicolas I work limited to 2 trades per day, the results have changed very well. less profit trading but more profit. I will continue to watch the whole thing and if I really run the strategy in the real account a programmer should look over there.

Nicolas,Vonasi,Mauro

Many thanks for your help

Good afternoon. I am sorry that I get involved in the Razz issue. I have a similar system in which instead of limiting the number of daily orders, I limit the number of lost orders.

I comment because your system reminds me of one that I have, based on the Mark Fisher ACD system. In this system, the maximum and minimum are set in a time range, but those values are not entered, but the maximum amount is added by the percentage of the average true range value of the previous day and the minimum is subtracted That same percentage. This prevents us from false breaks.

As you can see on the screen you have said you say that the last operation is not allowed, however, notice, that it returns almost to the initial position (that is, at the minimum of the range), then go back down and have a very good operation.

It is simply an idea.

RazzParticipant

Master

Nicolas the code for the 3 trades works, but unfortunately the entry conditions after the 1 trade no longer work. Entry should only be if it goes over the High Line or under the Low Line. If I use crosses over / under it only starts with the next candle. Do you have a solution?

Thank you

once Bars=60

once Hi=0

once Lo=0

If time = 090000 then

Hi=highest[Bars](high)

Lo=lowest[Bars](low)

endif

Spannepoints=(Hi-Lo)/pointsize

MaxBox = MB

if intradaybarindex=0 or day<>day[1] then

count=0

endif

if ( (not onmarket and onmarket[1] and not onmarket[2]) or (tradeindex(1)=tradeindex(2) and tradeindex(1)=barindex[1] and tradeindex(1)>0) or (not onmarket and onmarket[1])) then

count=count+1

endif

If not onmarket and time>= Startzeit and time < Endzeit and count<3 and Spannepoints < MaxBox then

BUY Position Lot AT Hi+(Spread/2) Stop

Sellshort Position Lot AT Lo-(Spread/2) Stop

ENDIF

// Stops und Targets

SET STOP pLOSS Spannepoints*y

SET TARGET pPROFIT Spannepoints *x