Hi Alfonso,

Thanks for the kind words, really glad to hear you’re getting strategies with Monte Carlo grades above 60, that’s a great sign!

Let me go through your questions one by one.

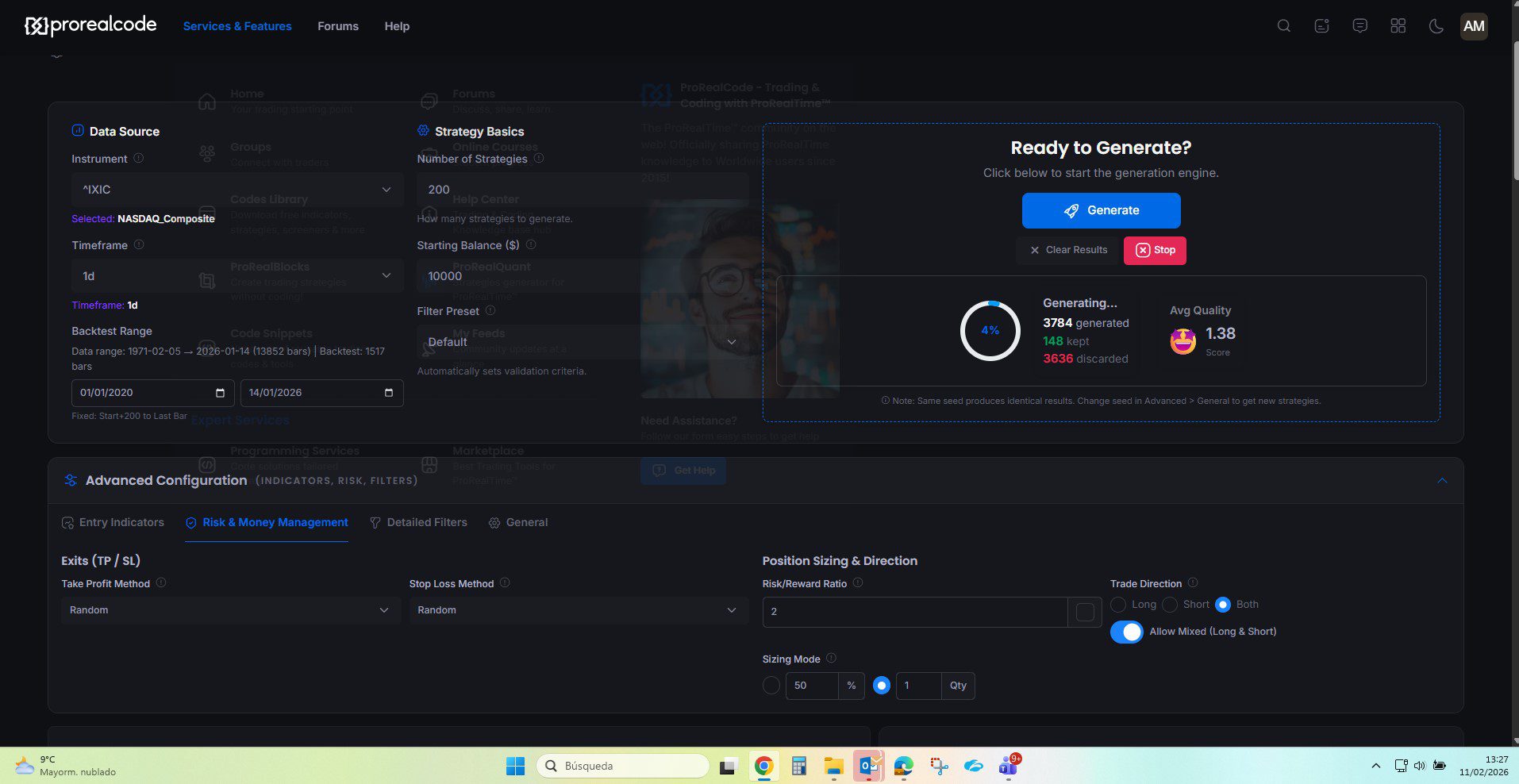

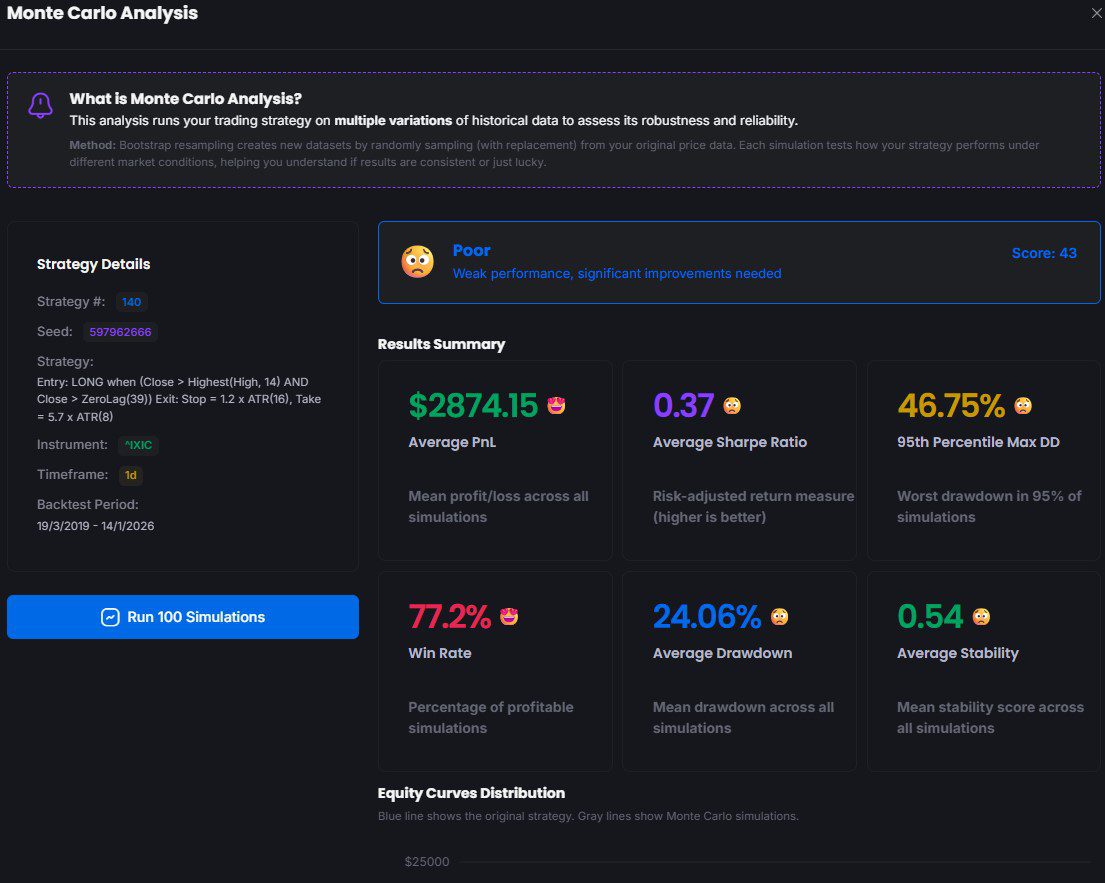

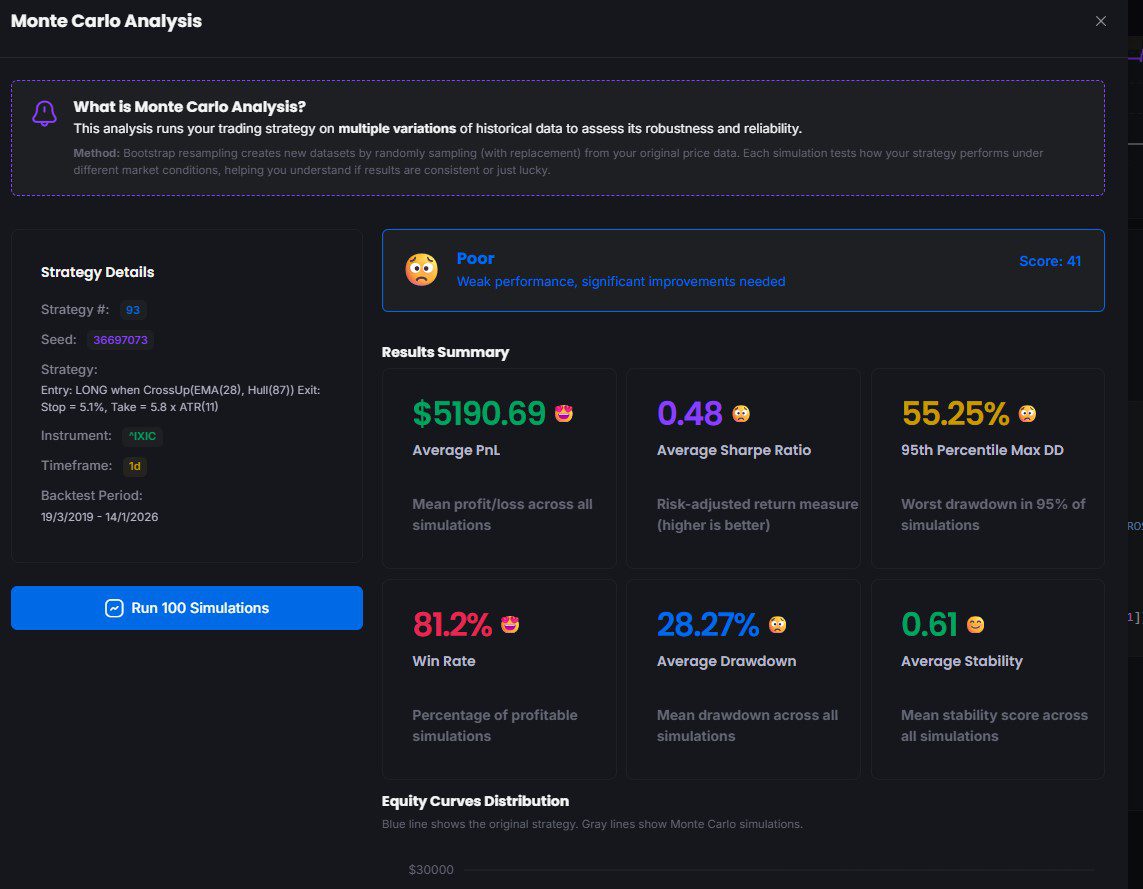

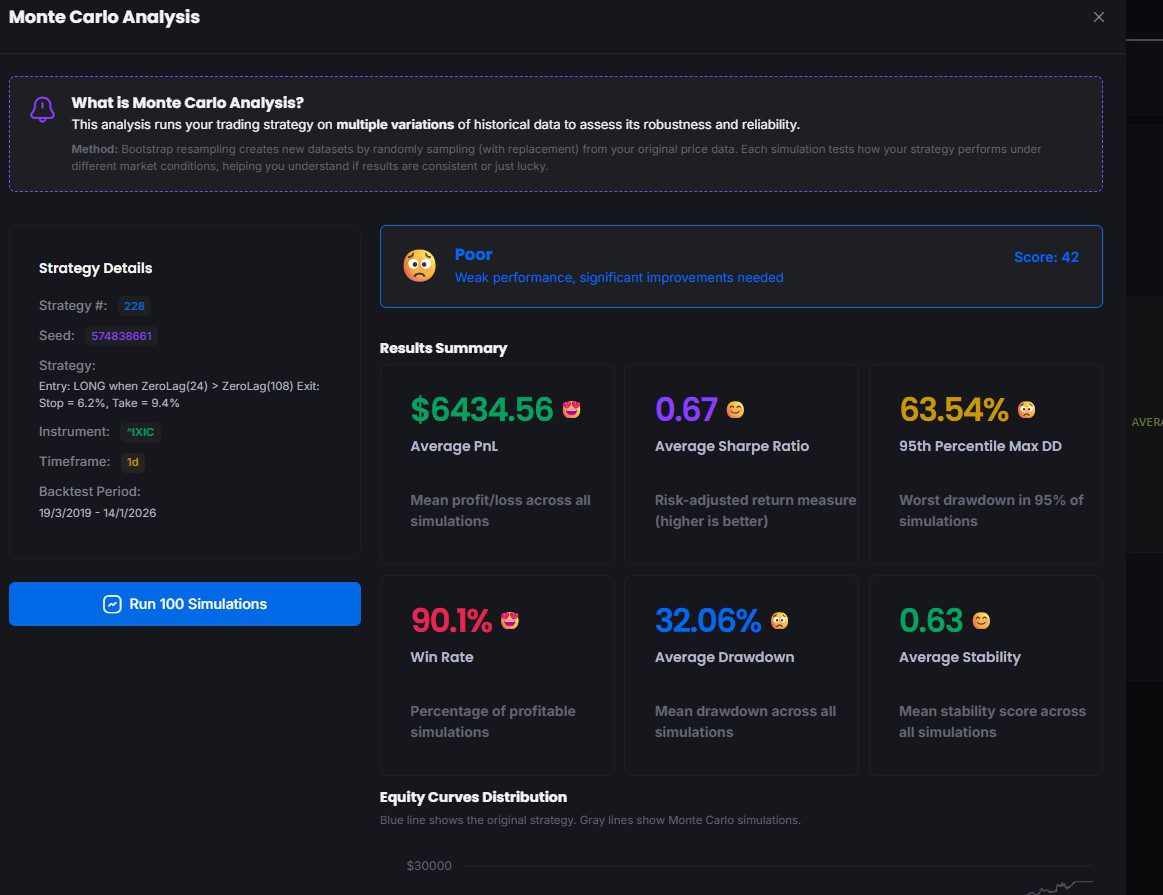

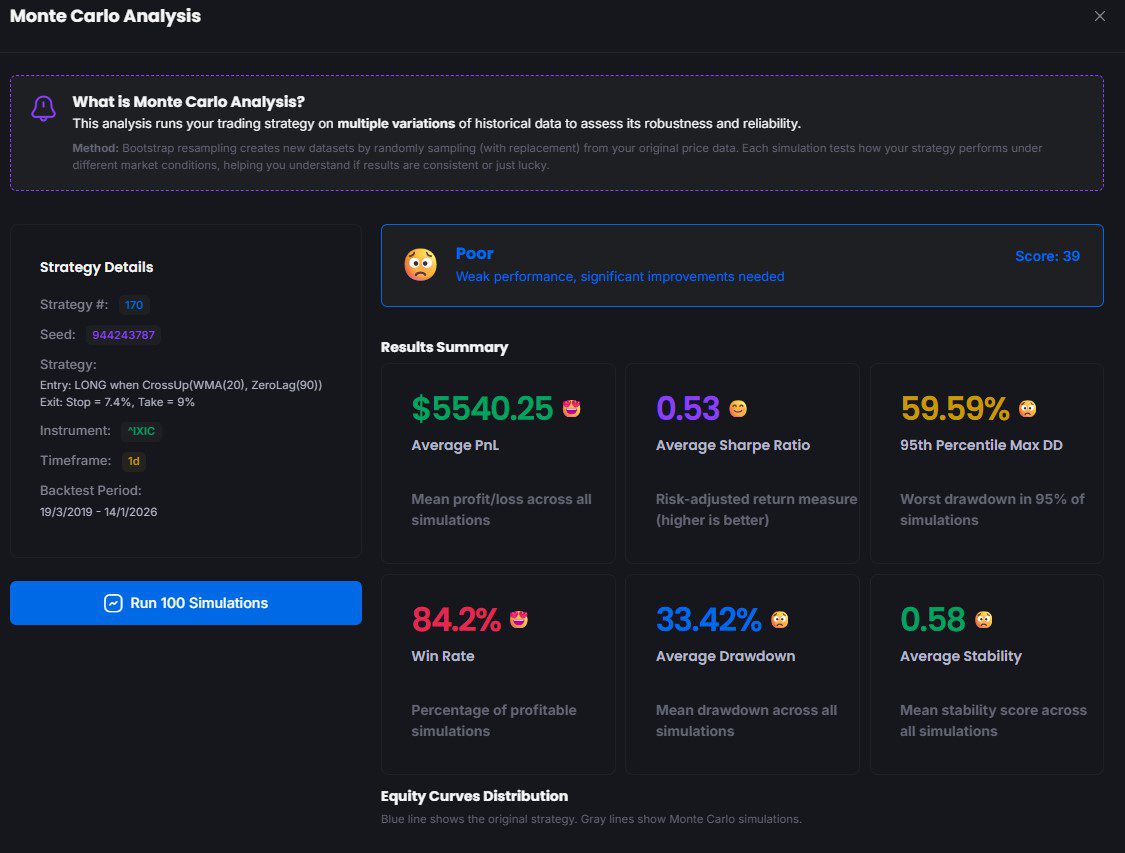

1. Monte Carlo variability

Yes, you’re correct. Each time you run Monte Carlo, it generates 100 new random synthetic price series using block bootstrap resampling, so the results will naturally vary slightly between runs. This is expected behavior, not a flaw. If you want more confidence in the grade, you can simply run it 3 to 5 times and look at the average or the range. If a strategy consistently scores above 60 across multiple runs, that’s a solid indicator of robustness. If it swings between 45 and 70, it’s more borderline. There’s no magic number of runs, but 3 to 5 gives you a reasonable picture.

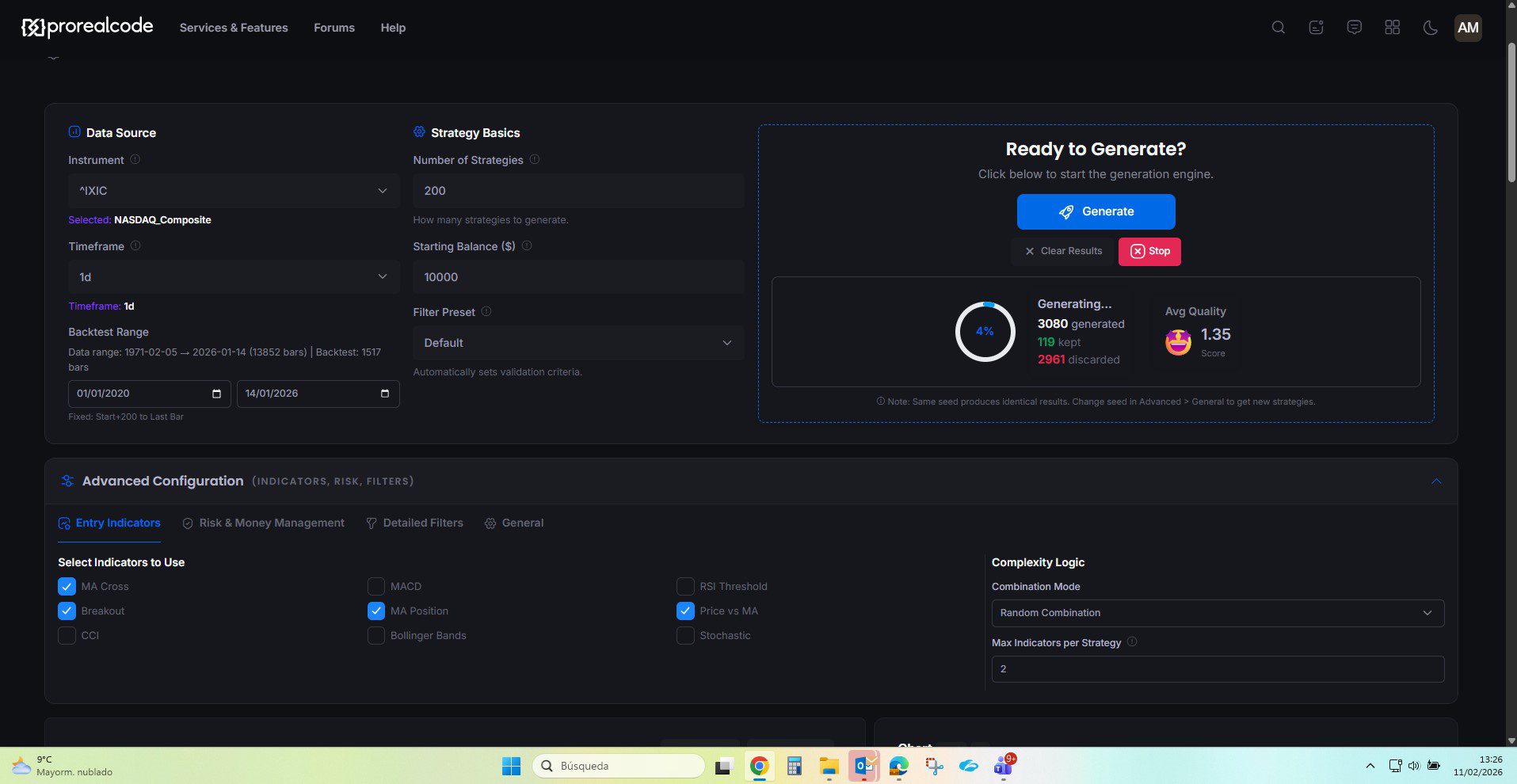

2. DAX H1

Intraday data like DAX H1 is trickier for several reasons. Intraday data tends to be noisier, so I’d recommend using the Conservative preset, setting Max Complexity to 1 (single indicator strategies), and keeping the Risk/Reward ratio enforced at 2:1 or above. Also try focusing on Long only or Short only rather than Both, as mixed strategies on intraday are harder to validate. If you’re still struggling, try increasing the number of strategies generated (1000+) in continuous mode, the hit rate is naturally lower on intraday so you need more attempts. And because the whole history I added cover a lof of different stages of market, it is way more difficult to find an edge on the complete set..

Also important, try to use only ATR takeprofit and stoploss, percentage of price in intraday strategies is not recommended.

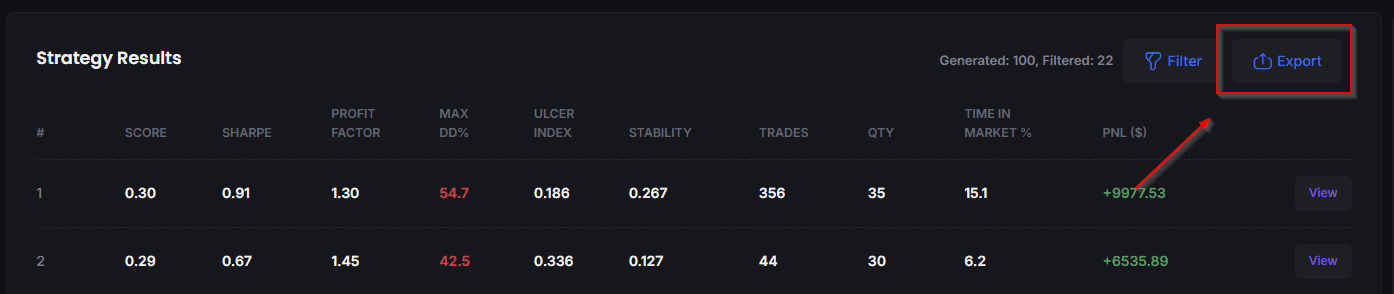

3. Automating the next phase (filters, exits, trailing)

Not at this stage. ProRealQuant is designed to find the raw skeleton of a strategy, a valid entry logic with basic stop/take profit exits that shows statistical robustness. The next phase of refinement (adding trailing stops, time filters, session filters, additional exit conditions) is intentionally manual for now. The reason is that automating that layer would dramatically increase the risk of overfitting, you’d essentially be curve-fitting on top of curve-fitting. My recommendation is to take a strategy with Monte Carlo > 60, export the ProBuilder code, and then manually test incremental improvements in ProRealTime’s backtester, validating each addition separately. That said, AI-assisted refinement is something I’m thinking about for the future, but it needs to be done carefully to preserve the anti-overfitting philosophy of the tool (or maybe a “simple” Walk Forward IS/OOS tester).

4. Forex pairs and commodities

Good suggestion, and I’ve noted it. Adding more instruments is on the roadmap. I’ll look into adding some popular Forex pairs and commodities to the pre-loaded dataset in a future update.

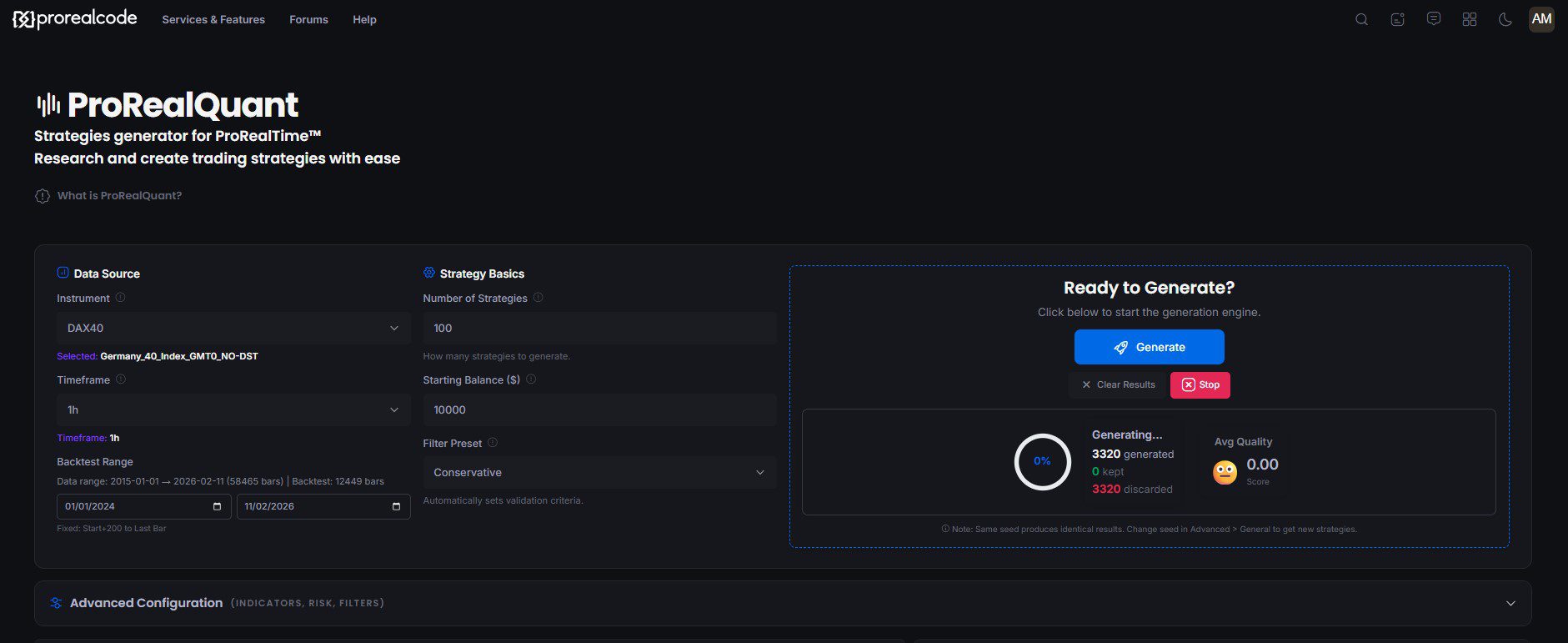

5. Strategies on stocks

Strategies on stocks should work fine, the pre-loaded data includes AAPL, AMZN, GOOG, META, MSFT, NVDA and TSLA. If you’re getting no results at all, the most likely cause is that your filters are too strict for the selected stock. Try resetting to the Default preset first to confirm that strategies are being generated, then gradually tighten filters. Also make sure the date range you’ve selected contains enough data. Some stocks may also need different parameter ranges, for example a stock with lower volatility might not trigger breakout conditions as often, so try disabling Breakout and focusing on MA Cross, RSI or Price vs MA entries. And if you are using the complete history, I think it might not be relevant to include more than 10-15 years of data?

Thanks again Alfonso, and don’t hesitate if you have more questions!