The trailing stop I use is not consistent in real trading. I can’t figure out the reason, because sometimes it is and sometimes it isn’t! The backtest shows it correct.

The cause is the trailing stop and there’s no profit-target.

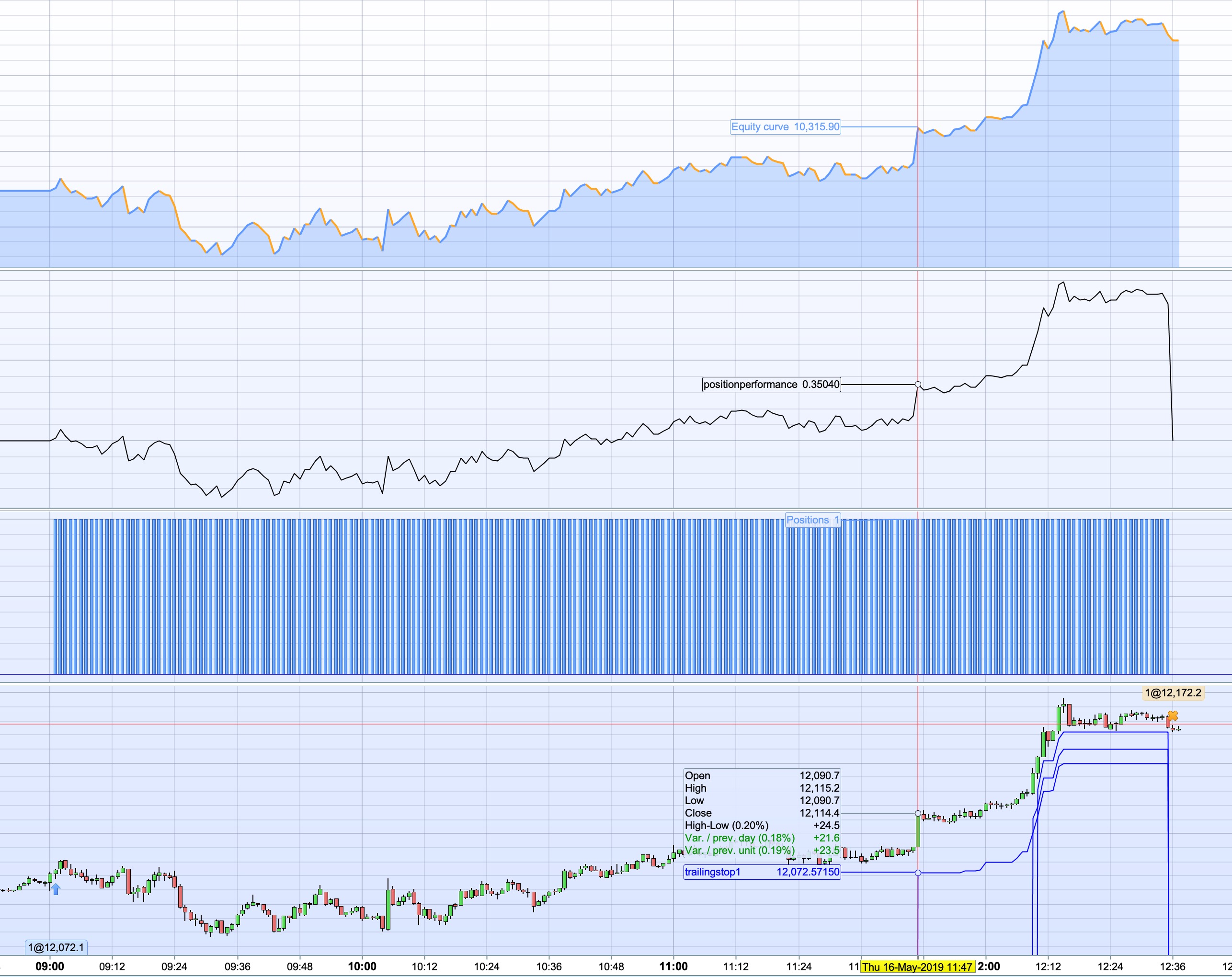

The question is, why is it selling at 0.35% sharp while that’s the level the trailing-stop should kick in? It works beautifully in the backtest, but it has to work realtime the same, all the time!

The “underlaying” only purpose is to make this code adjustable for other markets.

On 13 and 14th it worked correctly.

In the screenshots there are 2 different strategies and both executed at the same time or about.

once enablets = 1 // trailing stop

once displayts = 1 // trailing stop

ts1=0.35

ts2=0.30

ts3=0.20

switch =ts3+ts2

switch2=ts2+ts1

underlaying=100

if enablets then

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

trailingstop1 = (tradeprice(1)/100)*ts1

trailingstop2 = (tradeprice(1)/100)*ts2

trailingstop3 = (tradeprice(1)/100)*ts3

endif

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

maxprice1=0

minprice1=close

priceexit1=0

maxprice2=0

minprice2=close

priceexit2=0

maxprice3=0

minprice3=close

priceexit3=0

a1=0

a2=0

a3=0

pp=0

endif

if longonmarket then

pp=((close/tradeprice(1))-1)*100

if pp>=ts1 then

a1=1

endif

if pp>=switch then

a2=1

endif

if pp>=switch2 then

a3=1

endif

elsif shortonmarket then

pp=((close/tradeprice(1))-1)*-100

if pp>=ts1 then

a1=1

endif

if pp>=switch then

a2=1

endif

if pp>=switch2 then

a3=1

endif

endif

//first leg long

if longonmarket then

maxprice1=max(maxprice1,close)

if a1 then

if maxprice1-tradeprice(1)>=(trailingstop1) then

priceexit1=maxprice1-(trailingstop1/(underlaying/100))*pointsize

endif

endif

endif

//first leg short

if shortonmarket then

minprice1=min(minprice1,close)

if a1 then

if tradeprice(1)-minprice1>=(trailingstop1) then

priceexit1=minprice1+(trailingstop1/(underlaying/100))*pointsize

endif

endif

endif

//2nd leg long

if longonmarket then

maxprice2=max(maxprice2,high)

if a2 then

if maxprice2-tradeprice(1)>=(trailingstop2) then

priceexit2=maxprice2-(trailingstop2/(underlaying/100))*pointsize

endif

endif

endif

//2nd leg short

if shortonmarket then

minprice2=min(minprice2,low)

if a2 then

if tradeprice(1)-minprice2>=(trailingstop2) then

priceexit2=minprice2+(trailingstop2/(underlaying/100))*pointsize

endif

endif

endif

//3rd leg long

if longonmarket then

maxprice3=max(maxprice3,high)

if a3 then

if maxprice3-tradeprice(1)>=(trailingstop3) then

priceexit3=maxprice3-(trailingstop3/(underlaying/100))*pointsize

endif

endif

endif

//3rd leg short

if shortonmarket then

minprice3=min(minprice3,low)

if a3 then

if tradeprice(1)-minprice3>=(trailingstop3) then

priceexit3=minprice3+(trailingstop3/(underlaying/100))*pointsize

endif

endif

endif

//first leg exit

if longonmarket and priceexit1>0then

sell at priceexit1 stop

endif

if shortonmarket and priceexit1>0then

exitshort at priceexit1 stop

endif

//2nd leg exit

if longonmarket and priceexit2>0then

sell at priceexit2 stop

endif

if shortonmarket and priceexit2>0 then

exitshort at priceexit2 stop

endif

//3rd leg exit

if longonmarket and priceexit3>0then

sell at priceexit3 stop

endif

if shortonmarket and priceexit3>0 then

exitshort at priceexit3 stop

endif

if displayts then

graphonprice priceexit1 coloured(0,0,255,255) as "trailingstop1"

graphonprice priceexit2 coloured(0,0,255,255) as "trailingstop2"

graphonprice priceexit3 coloured(0,0,255,255) as "trailingstop3"

endif

endif

Any idea’s?

wait… could the cause be there’s no space between > 0 and then?

priceexit1>0then

that the backtest still works correctly, but realtime doesn’t?