Recently (within a couple of weeks), I have experienced several strategies stopping nighttime due to unknown errors, but they ALL are MTF strategies launched on DAX from 1-minute or 15-second TFs and referencing other higher TFs.

It’s not always the same strategy.

Setting custom trading hours didn’t help.

Has anyone experienced similar problems dealing with MTF or DAX?

I can see now that you wrote the code O-jay8 (Vonasi did not share his code).

As you possibly already know I am not big on giving away complete fish. I prefer handing out fishing rods and the odd hook and line and some tips on how to fish rather than giving away whole fish.

I have now had two minutes to import O-Jay8’s code and compare it with mine. It was a very interesting thing to do to see how someone else goes about attacking the same idea. The codes are quite different!

I use a much simpler long term trend filter and as per all my codes I do not use stop loss or take profit levels – I sell when conditions are met. I also use a totally different RSI setting. I also do not use any time filter. Both strategies are profitable over the back test period so neither is right or wrong or better than the other – forward testing will tell us whether either of them are any good. I will put a note in my calender to re-test both strategies in a months time I think.

Hi

@Grahal, you are welcome. I have not a big problem to share a strategy code mainly as I am still a novice and hope somebody is able to improve my code.

My codes are usually just bits and pieces from other strategies, I have seen here in the forum. I still have so much to learn.

My overall picture what is even possible is still very limited.

@ Vonasi, I understand that you dont want to share a complete strategy especially if you invested a lot of time and effort in it. I am already thankful for your tips and ideas.

i.e. your MTF RSI strategy, which I tried to replicate in my own way.

Often I dont even know where to start (initial strategy) so your idea with the MTF RSI was a good task for me to see whether I can get somehow similar results.

I do like MTF strategies a lot and it opens up so many possibilities. Unfortunately I dont have so much time as I try to code more or less in my spare time.

Where do you guys get your ideas for strategies?

Personally it would be nice if we could share more ideas. Unfortunately I lack imagination.

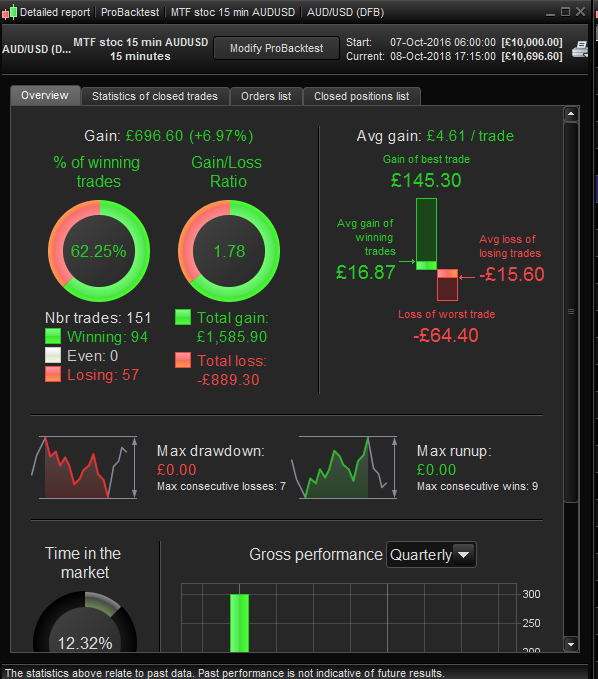

I tried to code stochastic overbought/oversold for MTF for forex pairs as well. (4h,1h,30m and 15 min)

I would say it was medium successful but I dont feel really confident about the future success rate in live but lets see. (attached the picture)

Where do you guys get your ideas for strategies? Personally it would be nice if we could share more ideas. Unfortunately I lack imagination.

A lot of my ideas come from statistical/probability studies of price action or price action along with one indicator value. I’m not interested in complicated strategies or strategies with masses of indicators. If you look at my library posts you will see that a lot of them are more analysis tools than true indicators. It is from analysis that ideas blossom!

I enjoy writing my own indicators and sometimes spot something that can be used from these. For example the Mean Reversal Equity Curve Indicator that I posted recently has turned out to give some very positive filtering results – but I still need a few months of forward testing to be certain of it – if only PRT/IG would fix the end of day and end of week live testing problem!

Sometimes I will read something online or in a magazine that I had not thought of testing. 99% of the time after testing and analysing I dispose of the idea but 1% of the time there is a little gem that can be used.

I receive complete different trade results varying the code at Time Frame of 15 minutes. I am using the 15 minutes graph, which is the lowest timeframe for my testing I would expect the code behind Time Frame, //update on close// and //default// used in the lowest timeframe to give exactly the same trading results. Why NOT is for me a question. timeframe(15 minutes,updateonclose) gives a much higher trade result as timeframe(15 minutes, default)

Problem spotted and identified, should be fixed in a near update.

Jan

JanParticipant

Veteran

Nicolas,

” Problem spotted and identified, should be fixed in a near update. ”

In the meanwhile, what to use for the lowest timeframe ( in my case 15 minutes timeframe) ==> (Timeframe 15 minutes, default) or (Timeframe 15 minutes, updateonclose) ?

Maybe I should test it myself in a live situation, but do you know what the trading algoritme in real live trading will follow when I would use (Timeframe 15 minutes, updateonclose) with a live trading time frame of 15 minutes ? Would it give the higher results as backtested or will it give the lower results as backtested with (Timeframe 15 minutes, default) ?

Thanks for the answer.

Kind regards, Jan

Maybe I should test it myself in a live situation

I would test it in live demo only. MTF is still only in beta testing for exactly this reason so risking real money on it would be a bit like being a jet fighter test pilot – exciting but potentially very dangerous!

In the meanwhile, you should always use the below instruction for the lowest timeframe, which in this case is the “default”:

timeframe(default)

The lowest timeframe, the one on which the strategy is read and executed, will obviously always be read at the end of the bar, so specifying “updateonclose” or “default” doesn’t matter.

Hi

would be possible use daily timeframe and a second time frame of 5 minutes?

How I cuold try my strategy?

thanks a lot

l

Yes, that’s possible, this is the purpose of the MTF functionnality. There is a simple and good example of a MTF strategy in this thread: https://www.prorealcode.com/topic/echelle-de-temps-multiples/#post-82039

Mes salutations .

Comment adapter les indicateurs aux Cryptomonnaies qui n’ont pas d’ouverture ni de cloture ? lequel choisir Cloture , Ouverture , plus haut, plus bas , Typique , Pondéré,Médian ou Total ?

Merci par avance pour cette précision

Cordialement 🙂

———————————————————————————————————————————————————————–

edit: Veuillez utiliser l’anglais sur le forum anglais. Merci. Cependant, j’ai fait la traduction avec Google Transaltor:

My greetings

How to adapt the indicators to cryptocurrencies that have no opening or closing? Which to choose between Closing, Opening, Upper, Lower, Typical, Weighted, Median or Total?

Thanks in advance for this clarification

Sincerely 🙂

Roberto

Guys i am finding a problem today with the MTF, i have several strategies with Default time frame 4h and inside the code i use the 1h time frame to find some filters. Now i have 6 strategies live like this, but today when i try to work on the backtest and others PRT told me that the lower Timeframe is not a multiply of the higher, but thats is not true and specially how is possible that my strategies are working ?????????????

[attachment file=”84082″]

i will post the code as example:

// Pathfinder Trading System based on ProRealTime 10.3

// Reiner @ www.prorealcode.com

// Breakout system triggered by previous daily, weekly and monthly high/low crossings with smart position management

// ProOrder code parameter

DEFPARAM CUMULATEORDERS = true // cumulate orders if not turned off

DEFPARAM PRELOADBARS = 10000

timeframe (1H)

MT = CALL "Main Trend"

FILTROL= MT>CLOSE

timeframe (default)

graph MT COLOURED (229, 43, 80)

// define intraday trading window

ONCE startTime = 90000 // start time of trading window in CET

ONCE endTime = 210000 // end time of trading window in CET

// define instrument signalline with help of multiple smoothed averages

ONCE periodFirstMA = 5 // 5 is center of gravity, do not change

ONCE periodSecondMA = 10 // 10 is center of gravity, do not change

ONCE periodThirdMA = 3 // heartbeat of the instrument

// define filter parameter

ONCE periodLongMA = 150 // period lenght of the long moving average that works as filter

ONCE periodShortMA = 210 // period lenght of the short moving average that works as filter

// define money and position management parameter

// dynamic scaling of the chance/risk profile depending on account size

ONCE startRisk = 1//1 // start risk level e.g 0.25 - 25%, 0.5 - 50%, 0.75 - 75%, 1 - 100% and so on

ONCE maxRisk = 1 // max risk level e.g 1.5 - 150%

ONCE increaseRiskLevel = 2000 // amount of profit from which the risk is to be increased

ONCE increaseRiskStep = 1.5//1//1//1 // step by which the risk should be increased

// size calculation: size = positionSize * trendMultiplier * saisonalPatternMultiplier * scaleFactor

ONCE positionSize = 1 // default start size

ONCE trendMultiplier = 2 // >1 with dynamic position sizing; 1 without

ONCE maxPositionSizePerTrade = 500 // maximum size per trade

ONCE maxPositionSizeLong = 500 // maximum size for long positions

ONCE maxPositionSizeShort = 500 // maximum size for short positions

ONCE stopLossLong = 1.6//2.8 //in %

ONCE stopLossShort = 2.4//2.4 //in %

ONCE takeProfitLong = 1.7//1 //in %

ONCE takeProfitShort =0.8// 0.8 //in %

ONCE trailingStartLong = 0.2 //in %

ONCE trailingStartShort = 0.1 //in %

ONCE trailingStepLong = 0.1 //in %

ONCE trailingStepShort = 0.1 //in %

ONCE maxCandlesLongWithProfit = 1//1//1 //take long profit latest after x candles

ONCE maxCandlesShortWithProfit = 2//2 // take short profit latest after x candles

ONCE maxCandlesLongWithoutProfit = 18 // limit long loss latest after x candles

ONCE maxCandlesShortWithoutProfit = 25 // limit short loss latest after x candles

// define saisonal position multiplier for each month 1-15 / 16-31 (>0 - long / <0 - short / 0 no trade)

ONCE January1 = 3

ONCE January2 = 0

ONCE February1 = 1

ONCE February2 = 3

ONCE March1 = 0

ONCE March2 = 3

ONCE April1 = 3

ONCE April2 = 3

ONCE May1 = 3

ONCE May2 = 1

ONCE June1 = 3

ONCE June2 = 3

ONCE July1 = 0

ONCE July2 = 0

ONCE August1 = 3

ONCE August2 = 3

ONCE September1 = 3

ONCE September2 = 0

ONCE October1 = 3

ONCE October2 = 3

ONCE November1 = 3

ONCE November2 = 2

ONCE December1 = 3

ONCE December2 = 3

// calculate the scaling factor based on the parameter

scaleFactor = MIN(maxRisk, MAX(startRisk, ROUND(StrategyProfit / increaseRiskLevel) * increaseRiskStep))

// dynamic position sizing based on weekly performance

ONCE profitLastWeek = 0

IF DayOfWeek <> DayOfWeek[1] AND DayOfWeek = 1 THEN

IF StrategyProfit > profitLastWeek + 1 THEN

positionSize = MIN(trendMultiplier, positionSize + 1) // increase risk

ELSE

positionSize = MAX(1, positionSize - 1) // decrease risk

ENDIF

profitLastWeek = strategyProfit

ENDIF

// calculate daily high/low (include sunday values if available)

dailyHigh = DHigh(1)

dailyLow = DLow(1)

previousDailyHigh = DHigh(2)

// calculate weekly high, weekly low is a poor signal

If DayOfWeek < DayOfWeek[1] AND lastweekbarindex = 0 THEN

lastWeekBarIndex = BarIndex

ELSE

IF DayOfWeek < DayOfWeek[1] THEN

weeklyHigh = Highest[BarIndex - lastWeekBarIndex](dailyHigh)

lastWeekBarIndex = BarIndex

ENDIF

ENDIF

// calculate monthly high/low

IF Month <> Month[1] AND lastMonthBarIndex=0 THEN

lastMonthBarIndex=barindex

ELSIF Month <> Month[1] THEN

monthlyHigh = Highest[BarIndex - lastMonthBarIndex](dailyHigh)

monthlyLow = Lowest[BarIndex - lastMonthBarIndex](dailyLow)

lastMonthBarIndex = BarIndex

ENDIF

// calculate instrument signalline with multiple smoothed averages

firstMA = WilderAverage[periodFirstMA](close)

secondMA = TimeSeriesAverage[periodSecondMA](firstMA)

signalline = TimeSeriesAverage[periodThirdMA](secondMA)

// save position before trading window is open

IF Time < startTime THEN

startPositionLong = COUNTOFLONGSHARES

startPositionShort = COUNTOFSHORTSHARES

ENDIF

// trade only in defined trading window

IF Time >= startTime AND Time <= endTime THEN

// set saisonal multiplier

currentDayOfTheMonth = OpenDay

midOfMonth = 15

IF CurrentMonth = 1 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = January1

ELSE

saisonalPatternMultiplier = January2

ENDIF

ELSIF CurrentMonth = 2 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = February1

ELSE

saisonalPatternMultiplier = February2

ENDIF

ELSIF CurrentMonth = 3 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = March1

ELSE

saisonalPatternMultiplier = March2

ENDIF

ELSIF CurrentMonth = 4 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = April1

ELSE

saisonalPatternMultiplier = April2

ENDIF

ELSIF CurrentMonth = 5 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = May1

ELSE

saisonalPatternMultiplier = May2

ENDIF

ELSIF CurrentMonth = 6 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = June1

ELSE

saisonalPatternMultiplier = June2

ENDIF

ELSIF CurrentMonth = 7 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = July1

ELSE

saisonalPatternMultiplier = July2

ENDIF

ELSIF CurrentMonth = 8 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = August1

ELSE

saisonalPatternMultiplier = August2

ENDIF

ELSIF CurrentMonth = 9 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = September1

ELSE

saisonalPatternMultiplier = September2

ENDIF

ELSIF CurrentMonth = 10 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = October1

ELSE

saisonalPatternMultiplier = October2

ENDIF

ELSIF CurrentMonth = 11 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = November1

ELSE

saisonalPatternMultiplier = November2

ENDIF

ELSIF CurrentMonth = 12 THEN

IF currentDayOfTheMonth <= midOfMonth THEN

saisonalPatternMultiplier = December1

ELSE

saisonalPatternMultiplier = December2

ENDIF

ENDIF

// define trading filters

// 1. use fast and slow averages as filter because not every breakout is profitable

f1 = close > Average[periodLongMA](close)

f2 = close < Average[periodLongMA](close)

f3 = close > Average[periodShortMA](close)

// 2. check if position already reduced in trading window as additonal filter criteria

alreadyReducedLongPosition = COUNTOFLONGSHARES < startPositionLong

alreadyReducedShortPosition = COUNTOFSHORTSHARES < startPositionShort

// long position conditions

l1 = signalline CROSSES OVER monthlyHigh

l2 = signalline CROSSES OVER weeklyHigh

l3 = signalline CROSSES OVER dailyHigh

l4 = signalline CROSSES OVER monthlyLow

// short position conditions

s1 = signalline CROSSES UNDER monthlyHigh

s2 = signalline CROSSES UNDER dailyLow

s3 = signalline CROSSES UNDER previousDailyHigh

// long entry with order cumulation

IF ( l1 OR l4 OR l2 OR (l3 AND f2) ) AND NOT alreadyReducedLongPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier > 0 THEN

numberContracts = MAX(1, MIN(maxPositionSizePerTrade, positionSize * saisonalPatternMultiplier) * scaleFactor)

IF (COUNTOFPOSITION + numberContracts) <= maxPositionSizeLong * scaleFactor THEN

IF SHORTONMARKET THEN

EXITSHORT AT MARKET

ENDIF

IF FILTROL THEN

BUY numberContracts CONTRACT AT MARKET

ENDIF

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

numberContracts = MAX(1, MIN(maxPositionSizePerTrade, positionSize) * scaleFactor)

IF (COUNTOFPOSITION + numberContracts) <= maxPositionSizeLong * scaleFactor THEN

IF SHORTONMARKET THEN

EXITSHORT AT MARKET

ENDIF

BUY numberContracts CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossLong

takeProfit = takeProfitLong

ENDIF

// short entry with order cumulation

IF ( (s1 AND f3) OR (s2 AND f1) OR (s3 AND f3) ) AND NOT alreadyReducedShortPosition THEN

// check saisonal booster setup and max position size

IF saisonalPatternMultiplier < 0 THEN

numberContracts = MAX(1, MIN(maxPositionSizePerTrade, positionSize * ABS(saisonalPatternMultiplier)) * scaleFactor)

IF (ABS(COUNTOFPOSITION) + numberContracts) <= maxPositionSizeShort * scaleFactor THEN

IF LONGONMARKET THEN

SELL AT MARKET

ENDIF

SELLSHORT numberContracts CONTRACT AT MARKET

ENDIF

ELSIF saisonalPatternMultiplier <> 0 THEN

numberContracts = MAX(1, MIN(maxPositionSizePerTrade, positionSize) * scaleFactor)

IF (ABS(COUNTOFPOSITION) + numberContracts) <= maxPositionSizeShort * scaleFactor THEN

IF LONGONMARKET THEN

SELL AT MARKET

ENDIF

SELLSHORT numberContracts CONTRACT AT MARKET

ENDIF

ENDIF

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

// superordinate stop and take profit

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

numberCandles = (BarIndex - TradeIndex)

m1 = posProfit > 0 AND numberCandles >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND numberCandles >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND numberCandles >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND numberCandles >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

// trailing stop function (convert % to pips)

trailingStartLongInPoints = tradeprice(1) * trailingStartLong / 100

trailingStartShortInPoints = tradeprice(1) * trailingStartShort / 100

trailingStepLongInPoints = tradeprice(1) * trailingStepLong / 100

trailingStepShortInPoints = tradeprice(1) * trailingStepShort / 100

// reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

// manage long positions

IF LONGONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartLongInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepLongInPoints * pipsize

stopLoss = stopLossLong * 0.1

takeProfit = takeProfitLong * 2

ENDIF

// next moves

IF newSL > 0 AND close - newSL >= trailingStepLongInPoints * pipsize THEN

newSL = newSL + trailingStepLongInPoints * pipsize

ENDIF

ENDIF

// manage short positions

IF SHORTONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartShortInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepShortInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND newSL - close >= trailingStepShortInPoints * pipsize THEN

newSL = newSL - trailingStepShortInPoints * pipsize

ENDIF

ENDIF

// stop order to exit the positions

IF newSL > 0 THEN

IF LONGONMARKET THEN

SELL AT newSL STOP

ENDIF

IF SHORTONMARKET THEN

EXITSHORT AT newSL STOP

ENDIF

ENDIF

ENDIF

Gianluca it’s the other way round… all TF’s must be multiple of the main one, which is the lowest one from where the strategy is launched and which must be the current TF on the chart. In your case your default TF CANNOT be 4h! Your code has nothing to do with this issue.

You cannot launch or backtest your MTF strategy from a 4-hour TF if you are using lower TF’s.

If you want to use 4h and 1h, or even 1min, you must launch your strategy from the lowest one!

And you cannot use 4h, 1h and 7mins together, because 4h (240 mins) and 1h (60 mins) are not multiple of 7 minutes! You should use 245/238mins, 63/56mins and 7mins.

ou cannot launch or backtest your MTF strategy from a 4-hour TF if you are using lower TF’s.

If you want to use 4h and 1h, or even 1min, you must launch your strategy from the lowest one!

i have live 5 strategies in this way so how you explain it?