Paul

PaulParticipant

Master

Hi,

It’s about the dax 30 cash €1,- at a 1 minute timeframe and the Big Line Strategy Code.

To this code I’ve made small modifications compared to the one published in the library.

The code of the Big Line Strategy, it works using a market order.

But if you use a limit order then it works correctly in a live trading environment, but not in a back test.

Tick mode on or off don’t show a difference.

So why does the back test with a limit order not work correctly?

More specific, i.e. why does the back test skip a trade at 5 September 2018 at 11.24, but the same code in a live trading environment gets correctly activated?

Maybe I missed something and hope for some feedback.

//-------------------------------------------------------------------------

// Main code : Big Line Strategy

//-------------------------------------------------------------------------

// common rules

DEFPARAM CUMULATEORDERS = false

DEFPARAM PRELOADBARS = 10000

// optional

BreakEvenStop = 0 // BreakEvenStop and BreakEvenStop Minimum Gain

MFETrailing = 1 // MFETrailing

// time rules

ONCE entertime = 090000 //

ONCE lasttime = 133000

ONCE closetime = 240000 // greater then 23.59 means it continues position overnight

ONCE closetimeFriday=173000

tt1 = time >= entertime

tt2 = time <= lasttime

tradetime = tt1 and tt2

DayForbidden = 5 // no new entry on Friday

df = dayofweek <> dayforbidden

// positionsize and stops

positionsize = 1

sl = 1.00 // % Stoploss

pt = 1.50 // % Profit Target

ts = 1.20 // % MFETrailing

bs = 1.00 // % BreakEvenStop

bsm= 0.00 // % BreakEvenStop Minimum Gain

// setup number of trades intraday

if IntradayBarIndex = 0 then

longtradecounter = 0

Shorttradecounter = 0

endif

// general criteria

GeneralCriteria = tradetime and df and (barindex > tradeindex+1)

// trade criteria

tcLong = countoflongshares < 1 and longtradecounter < 1

tcShort = countofshortshares < 1 and shorttradecounter < 1

// line criteria

CurrentPrice = round(dclose(1))

MPmod = 100

Factor = 100 // defines lines

AboveLevel0 = CurrentPrice mod MPmod

StartLevel = CurrentPrice - AboveLevel0

Level00Up = Startlevel

Level10Up = StartLevel + (1*Factor)

Level20Up = StartLevel + (2*Factor)

Level30Up = StartLevel + (3*Factor)

Level40Up = StartLevel + (4*Factor)

Level50Up = StartLevel + (5*Factor)

Level60Up = StartLevel + (6*Factor)

Level70Up = StartLevel + (7*Factor)

Level80Up = StartLevel + (8*Factor)

Level90Up = StartLevel + (9*Factor)

Level00Down = Startlevel

Levell0Down = StartLevel - (1*Factor)

Level20Down = StartLevel - (2*Factor)

Level30Down = StartLevel - (3*Factor)

Level40Down = StartLevel - (4*Factor)

Level50Down = StartLevel - (5*Factor)

Level60Down = StartLevel - (6*Factor)

Level70Down = StartLevel - (7*Factor)

Level80Down = StartLevel - (8*Factor)

Level90Down = StartLevel - (9*Factor)

l0 = close crosses over Level00Up or close crosses over Level00Down

l1 = close crosses over Level10Up or close crosses over Levell0Down

l2 = close crosses over Level20Up or close crosses over Level20Down

l3 = close crosses over Level30Up or close crosses over Level30Down

l4 = close crosses over Level40Up or close crosses over Level40Down

l5 = close crosses over Level50Up or close crosses over Level50Down

l6 = close crosses over Level60Up or close crosses over Level60Down

l7 = close crosses over Level70Up or close crosses over Level70Down

l8 = close crosses over Level80Up or close crosses over Level80Down

l9 = close crosses over Level90Up or close crosses over Level90Down

s0 = close crosses under Level00Down or close crosses under Level00Up

s1 = close crosses under Levell0Down or close crosses under Level10Up

s2 = close crosses under Level20Down or close crosses under Level20Up

s3 = close crosses under Level30Down or close crosses under Level30Up

s4 = close crosses under Level40Down or close crosses under Level40Up

s5 = close crosses under Level50Down or close crosses under Level50Up

s6 = close crosses under Level60Down or close crosses under Level60Up

s7 = close crosses under Level70Down or close crosses under Level70Up

s8 = close crosses under Level80Down or close crosses under Level80Up

s9 = close crosses under Level90Down or close crosses under Level90Up

// trade criteria extra

min1 = MIN(dhigh(0),dhigh(1))

min2 = MIN(dhigh(1),dhigh(2))

max1 = MAX(dlow(0),dlow(1))

max2 = MAX(dlow(1),dlow(2))

tcxLong = high < MIN(min1,min2)

tcxShort = low > MAX(max1,max2)

// long entry

If GeneralCriteria then

If tcLong and tcxLong then

if (l0 or l1 or l2 or l3 or l4 or l5 or l6 or l7 or l8 or l9) then

longtradecounter=longtradecounter + 1

buy positionsize contract at high[1] limit

endif

endif

endif

// short entry

If GeneralCriteria then

if tcShort and tcxShort then

if (s0 or s1 or s2 or s3 or s4 or s5 or s6 or s7 or s8 or s9) then

shorttradecounter=shorttradecounter + 1

sellshort positionsize contract at low[1] limit

endif

endif

endif

// BreakEvenStop

If BreakEvenStop then

if not onmarket then

newSL=0

endif

If longonmarket and close-tradeprice(1)>=((tradeprice/100)*bs)*pipsize then

newSL = tradeprice(1)+((tradeprice/100)*bsm)*pipsize

endif

If shortonmarket and tradeprice(1)-close>=((tradeprice/100)*bs)*pipsize then

newSL = tradeprice(1)-((tradeprice/100)*bsm)*pipsize

endif

If newSL>0 then

sell at newSL Stop

exitshort at newSL Stop

endif

endif

// MFETrailing

If MFETrailing then

trailingstop = (tradeprice/100)*ts

if not onmarket then

MAXPRICE = 0

MINPRICE = close

priceexit = 0

endif

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=trailingstop*pipsize then

priceexit = MAXPRICE-trailingstop*pipsize

endif

endif

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=trailingstop*pipsize then

priceexit = MINPRICE+trailingstop*pipsize

endif

endif

If onmarket and priceexit>0 then

sell at market

exitshort at market

endif

endif

// exit at closetime

If onmarket then

if time >= closetime then

sell at market

exitshort at market

endif

endif

// exit friday at set closetime

if onmarket then

if (CurrentDayOfWeek=5 and time>=closetimefriday) then

sell at market

exitshort at market

endif

endif

// build-in exit

if BreakEvenStop=0 then

SET STOP %LOSS sl

elsif BreakEvenStop=1 then

SET STOP %LOSS bsm

endif

SET TARGET %PROFIT pt

//GRAPH 0 coloured(300,0,0) AS "zeroline"

//GRAPH (positionperf*100)coloured(0,0,0,255) AS "PositionPerformance"

What fixed spread did you have set on backtest?

Maybe try 0.6 spread and run bt again (see if it makes any difference as that is what DAX usually is at 11:24 AM)?

Makes no difference, but I have got a trade opening on 5 Sep 18 10:24 (you are 1 hour ahead of me) but at 30 sec TF.

This may be a red herring, but thought I’d post it anyway as I have spent time on it.

Makes no difference, but I have got a trade opening on 5 Sep 18 10:24 (you’re timezone is 1 hour ahead of me / UK) but at 30 sec TF.

This may be a red herring, but thought I’d post it anyway as I have spent time on it.

Also I have got a trade opening on 5 Sep 18 10:24 (you are 1 hour ahead of me) but at 5 min TF.

Are you comparing live account backtest with demo account one? Or real live trading?

Mmm good point Nicolas!

My tests were on Demo Backtest.

I asked Paul this question because of the 2 different version of the backtest engine that exist in demo and live account with IG.

PaulParticipant

Master

Thanks for the help guys.

@Nicolas

I ‘am running version v10.3 – 1.8.0_45 on a Mac (last update 30 july 2018)

That’s the version which does the backtest and the live trading.

The code has 1 point spread and tickmode is activated.

@GraHal

For 30 sec TF, I got the same as you, it entered a trade.

Also on 5 minutes it entered a trade at 11.25 my time on 5 sept.

But how’ is the 1 minute 10.24 your time zone?

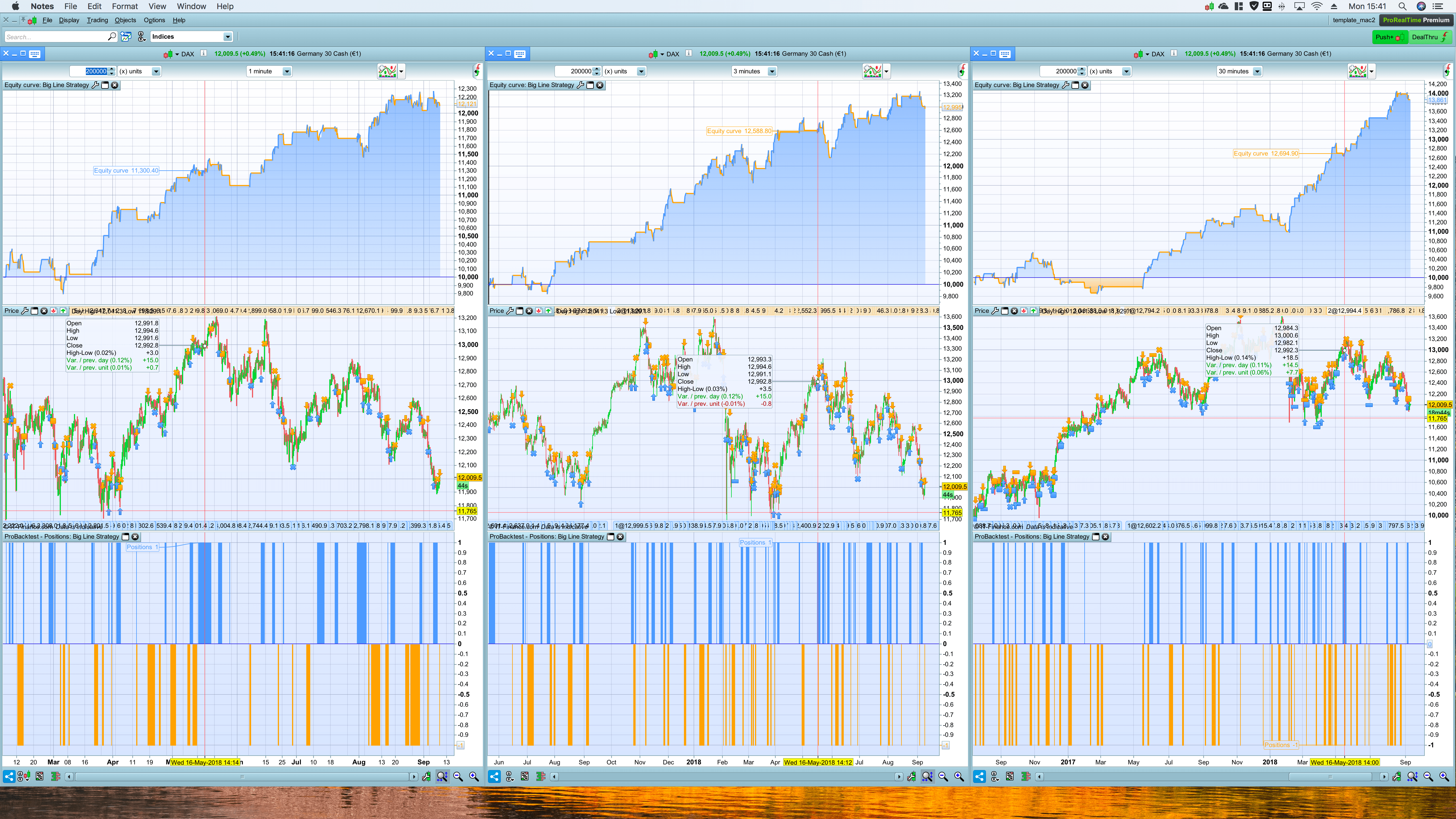

Of this code interesting timeframes are 1, 3 and 30 minutes with 200k backtest. I attached the screenshot. The 30min is a bit zoomed in.

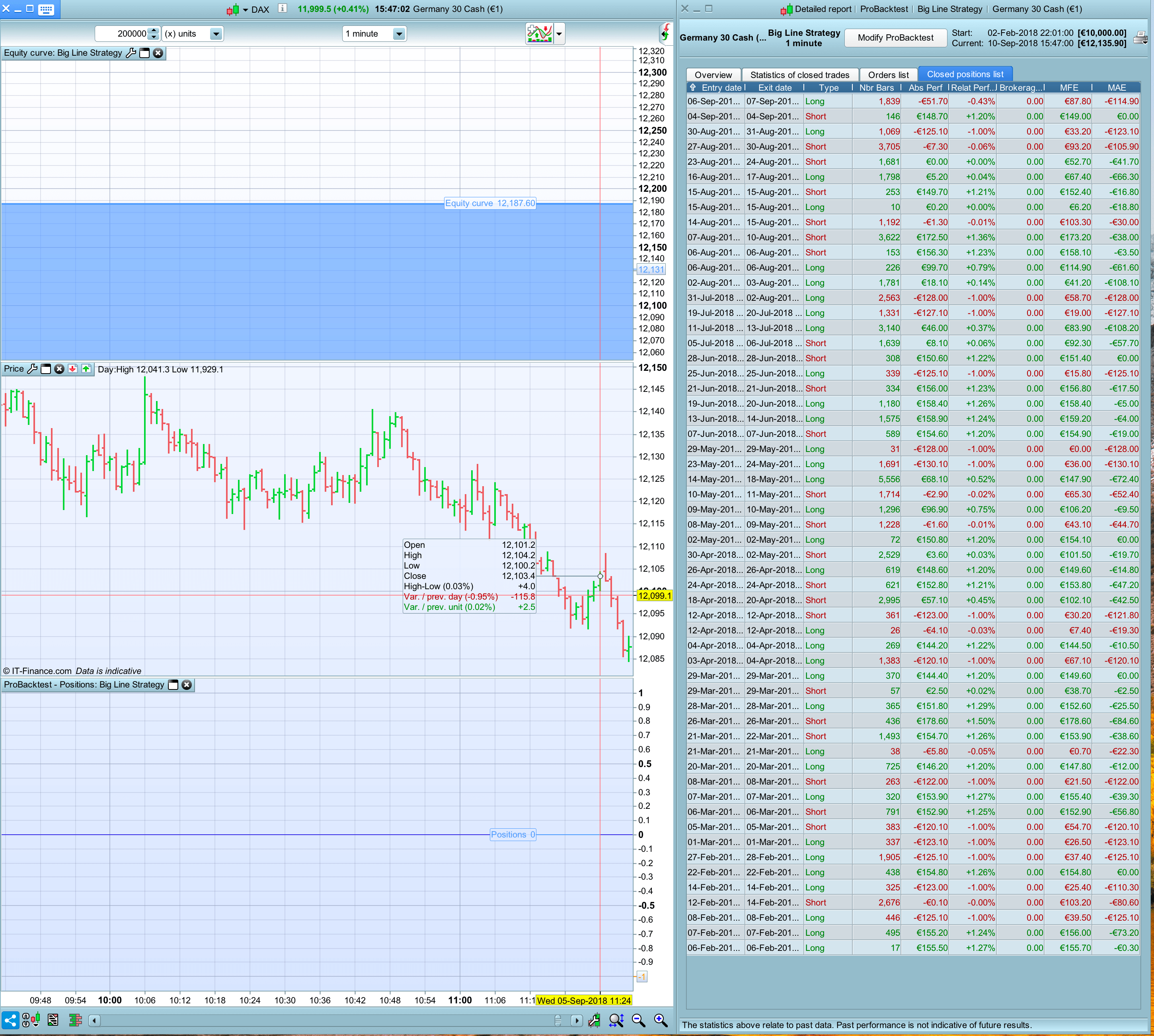

Also attached a screenshot of the 1 minute bar which is has my focus in this case.

I need to understand why the trade got skipped in backtest and get’s activated correctly live. It renders the back-test useless otherwise.

ok so the order is not triggered only in the 1 minute TF, right?

PaulParticipant

Master

Correct

The order in a back test does not get triggered only on the 1-minute TF when it’s a limit order. (5 September 2018 11:24:00)

details;

Close crosses the big line at 11.23 and meets all criteria

The limit order refers to high[1] which at 11.22 is 12.100,2.

The low at 11.24 is 12.100,2

A limit high[1] means buy at 12.100,2 or lower at the 11.24 bar, which traded 12.100.2

The spread on the DAX (DFB) is normally 1.0 at the time of the trade so this is the most likely reason that the trade did not open. The prices shown on the chart are mid prices (i.e halfway between the buy and sell prices). The mid price would need to have reached 12099.7 for a buy trade to have opened at 12100.2

What about a backtest without spread?

What about a backtest without spread?

Sorry – too early and not enough coffee yet. I just re-read the posts and now see that the problem is ‘the trade got skipped in backtest and get’s activated correctly live’ and that the OP tested with a 1.0 pip spread. A back test without spread should open the trade and so would be a nice test to try.

Correct … at 0 / zero spread, I get a trade opening on Demo Backtest at 1 min at 10:24 (I am UK so 1 hour behind the OP).