this would be nice for the dax. Because of the Margin. It´s the half of Dow. Anyone tried?

Mmm thought it was a bit too good to be true! Just a bit though! 🙂

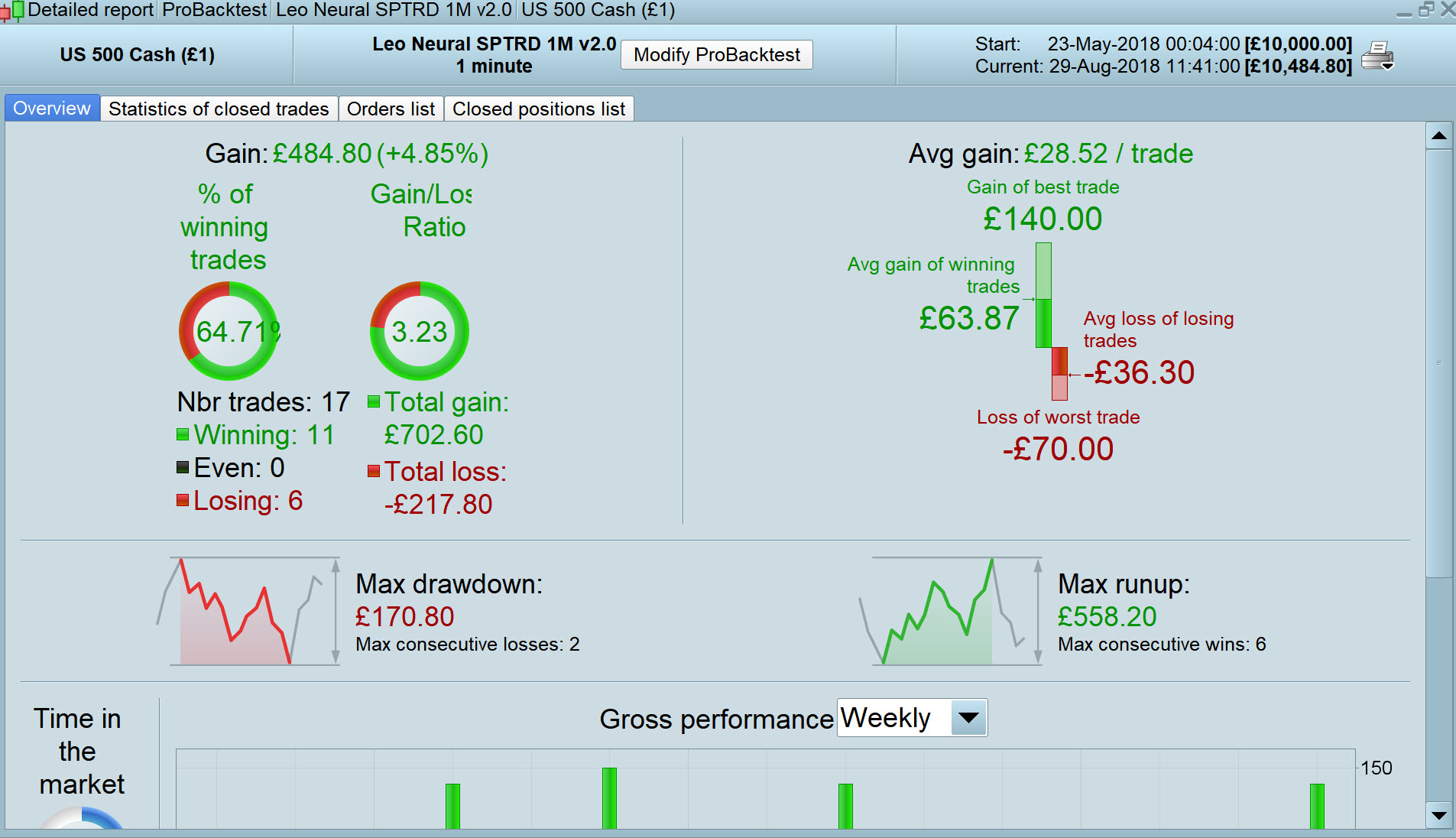

I have done a pessimistic calculation / check of results and £300 – £400 of profit is due to the spike we have had to endure at 21:15 on the Dow for the last 5 nights or so.

4 trades have been affected at 21:15, 1 lost around 350 due to the spike and 3 gained 200 due to the spike!

The 4 spiked tradess may have gone on to be gainers anyway if the spike hadn’t triggered the SL and TP. I guess I could work this out, but the coffee hasn’t worked through yet! 🙂

Results are still good though as v1.0 is currently trading at a genuine around £600 profit over 6 days (950 – 350 due to IG spikes! ).

I will put a time filter on the strategy when I get chance.

Vonasi proposed so here it is … SPTRD on 1 Min TF 100k bars, spread = 4

DEFPARAM CUMULATEORDERS = False

//Variables:

candlesback=5

ProfitRiskRatio=2

spread=1.5

myATR=average[20](range)+std[20](range)

ExtraStopLoss=MyATR

//ExtraStopLoss=3*spread*pipsize

//for long trades

classifierlong=0

FOR scanL=1 to candlesback DO

IF classifierlong[scanL]=1 then

BREAK

ENDIF

LongTradeLength=ProfitRiskRatio*(close[scanL]-(low[scanL]-ExtraStopLoss[scanL]))

IF close[scanL]+LongTradeLength < high-spread*pipsize then

IF lowest[scanL+1](low) > low[scanL]-ExtraStopLoss[scanL]+spread*pipsize then

classifierlong=1

//candleentrylong=barindex-scanL

BREAK

ENDIF

ENDIF

NEXT

IF classifierlong=1 and Close > Average[120](close)then

//DRAWSEGMENT(candleentrylong,close[barindex-candleentrylong],barindex,close[barindex-candleentrylong]+LongTradeLength) COLOURED(0,150,0)

//DRAWELLIPSE(candleentrylong-1,low[barindex-candleentrylong]-ExtraStopLoss,barindex+1,high+ExtraStopLoss) COLOURED(0,150,0)

Buy 2 Contract at Market

ENDIF

//for short trades

classifiershort=0

FOR scanS=1 to candlesback DO

IF classifiershort[scanS]=1 then

BREAK

ENDIF

ShortTradeLength=ProfitRiskRatio*((high[scanS]-close[scanS])+ExtraStopLoss[scanS])

IF close[scanS]-ShortTradeLength > low+spread*pipsize then

IF highest[scanS+1](high) < high[scanS]+ExtraStopLoss[scanS]-spread*pipsize then

classifiershort=1

//candleentryshort=barindex-scanS

BREAK

ENDIF

ENDIF

NEXT

IF classifiershort=1 and Close < Average[120](close) then

//DRAWSEGMENT(candleentryshort,close[barindex-candleentryshort],barindex,close[barindex-candleentryshort]-ShortTradeLength) COLOURED(150,0,0)

//DRAWELLIPSE(candleentryshort-1,high[barindex-candleentryshort]+ExtraStopLoss,barindex+1,low-ExtraStopLoss) COLOURED(150,0,0)

SellShort 2 Contract at Market

ENDIF

SET TARGET PROFIT 70

SET STOP PLOSS 35

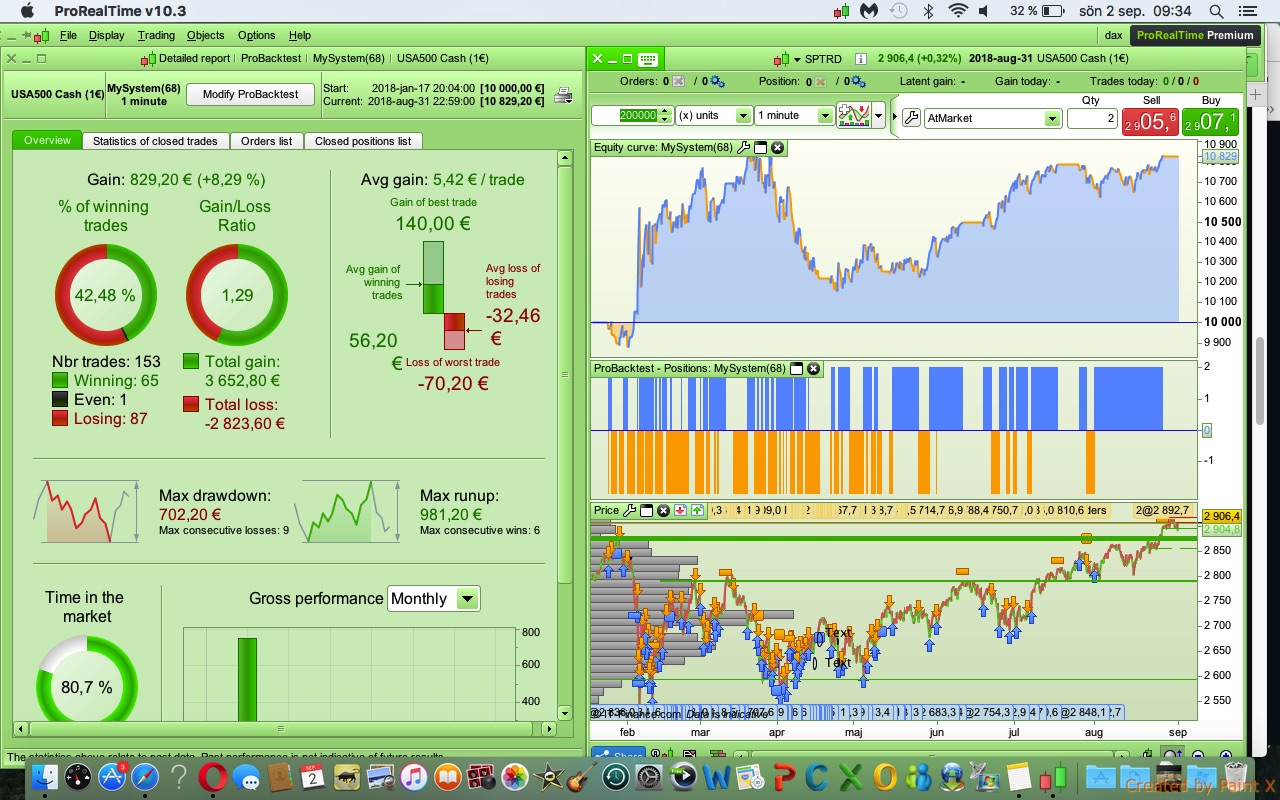

Vonasi proposed so here it is … SPTRD on 1 Min TF 100k bars, spread = 4

Why 4 pips? The SP500 spread is never that big.

Hey Everyone!!

Such a nice work!! Amazing results from the beginning, Congrats guys!!!

I would like my little idea to improve the results. Months ago I added an indicator to the library. I think this indicator can prevent fake entries, basiclly I added two more conditions to the original code:

AverageVolumeBuy > AverageVolumeSell and AverageVolumeBuy > 50

It is only a little bit improve, and please guys please to share your opinion. I hope you like.

Saludos!!

Why 4 pips? The SP500 spread is never that big.

I forgot, I forgot okay!? We all make mistakes!? 🙂

Also Lot size = 2 on my results above.

S&P500 is min Lot size 5, so more mistakes on my part! 🙁

I hope you like.

Yeah looks good, thanks! The more the merrier! 🙂

GraHal

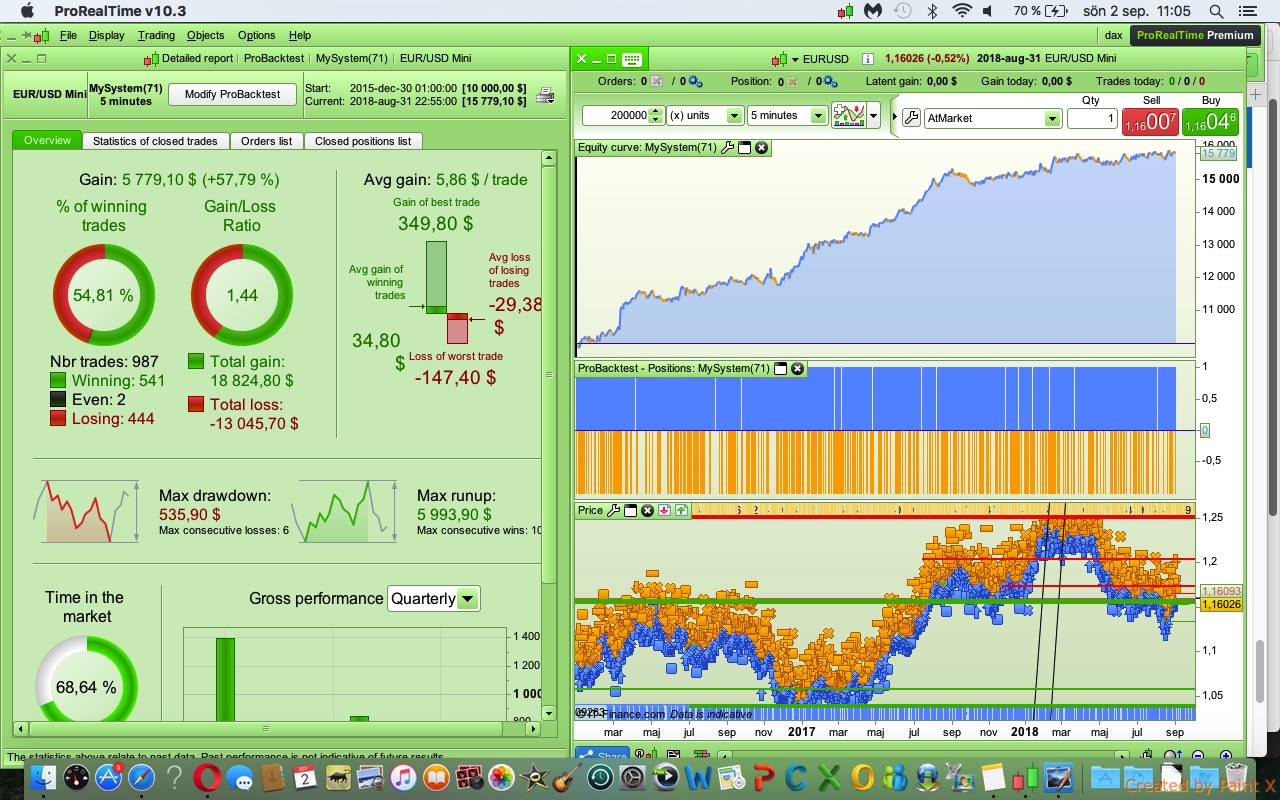

200k on your SP500 spread=2.

X

I did a 200k test on your code.

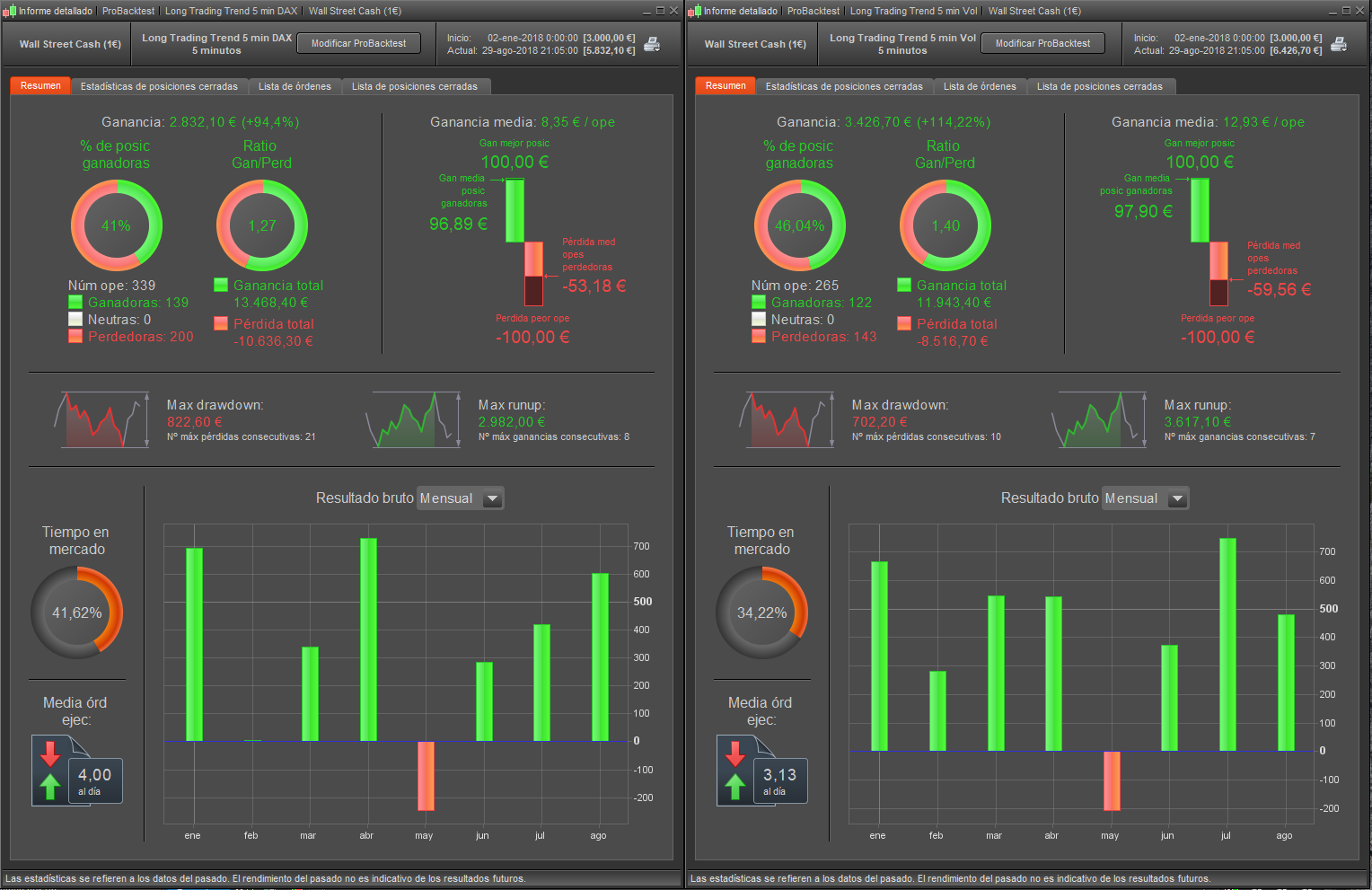

@Stefanb @Xusto @anybody … got any tweaks / fixes for that big drawdown shown on Stefanb screenshot over 200k bars above??

Please post your tweaked / fixed code on here with screen shot of equity curve and performance results.

Equity curve stagnation and lose come from ranging market. This seems normal for a strategy that detects market movements and bets on their continuity 🙂

Well we need code to keep out of the market when ranging?

X I did a 200k test on your code.

Above is for Xusto version with the volume tweak in post 79312.

( @stefanb in case you don’t know and for others … if you select part of the text of a post and THEN click on Quote on the right above the post then the selected text displays as a quote … very useful).

Here is a code that I will start live soon.

Have run it om demo for a while and it seems to be working ok.

Spread=1

Op 75%

DEFPARAM CumulateOrders = False

DEFPARAM PRELOADBARS = 200

indicator1 = SuperTrend[1,8]

c1 = (close <= indicator1)

indicator4 = SuperTrend[1,4]

c4 = (close <= indicator4)

c2 = DIplus[6](close) > DIminus[3](close)

HL = 14 // Hour of Long Entry

HLS = 12 // Hour of Long Exit

HS = 7 // Hour of Short Entry

HSS = 15 // Hour of Short Exit

LATR = 9// Number of ATRs for Stop Loss

PATR = 21 // Number of ATRs for Take Profit

ATR = 18 // ATR period

IF Hour=HL and c1 THEN

BUY 1 CONTRACTS AT MARKET

ENDIF

If LongOnMarket AND Hour=HLS THEN//

SELL AT MARKET

ENDIF

IF Hour=HS and c2 and c4 THEN

SELLSHORT 1 CONTRACTS AT MARKET

ENDIF

IF ShortOnMarket AND Hour=HSS THEN

EXITSHORT AT MARKET

ENDIF

SET STOP LOSS LATR*AverageTrueRange[ATR](close)

SET TARGET PROFIT PATR*AverageTrueRange[ATR](close)

IF Hour=HS and c2 and c4 THEN

SELLSHORT 1 CONTRACTS AT MARKET

ENDIF

IF ShortOnMarket AND Hour=HSS THEN

EXITSHORT AT MARKET

ENDIF

SET STOP LOSS LATR*AverageTrueRange[ATR](close)

SET TARGET PROFIT PATR*AverageTrueRange[ATR](close)

Lines 34-35 are duplicate and you may remove them.

Moreover, your SL & TP will change each new candle, while they should not while on market, I think you should use line 44 to write

If Not OnMarket then

and add line 47 with ENDIF

Lines 37 to 46 are all duplicated?

I guess maybe finger trouble with copy and paste??