Ciao a tutti, ho messo su una strategia molto semplice, va a comprare quando la candela chiude sotto la banda inferioer di bollinger, e va a vendere quando chiude sopra.

La strategia si dimostra pero’ profittevole solo con le operazioni long, e per questo ho inserito nel codice la possibilità di disabilitarla.

Ho preso poi la gestione delle operazioni dal sistema Pathfinder per la chiusura dopo tot candele non in profit.

Chiedo a chi vuole ed ha tempo qualche consiglio o idea per eliminare il problema dei loss sulle operazioni short, o suggerimenti per gestire meglio le operazioni in loss ed in profit.

Grazie!

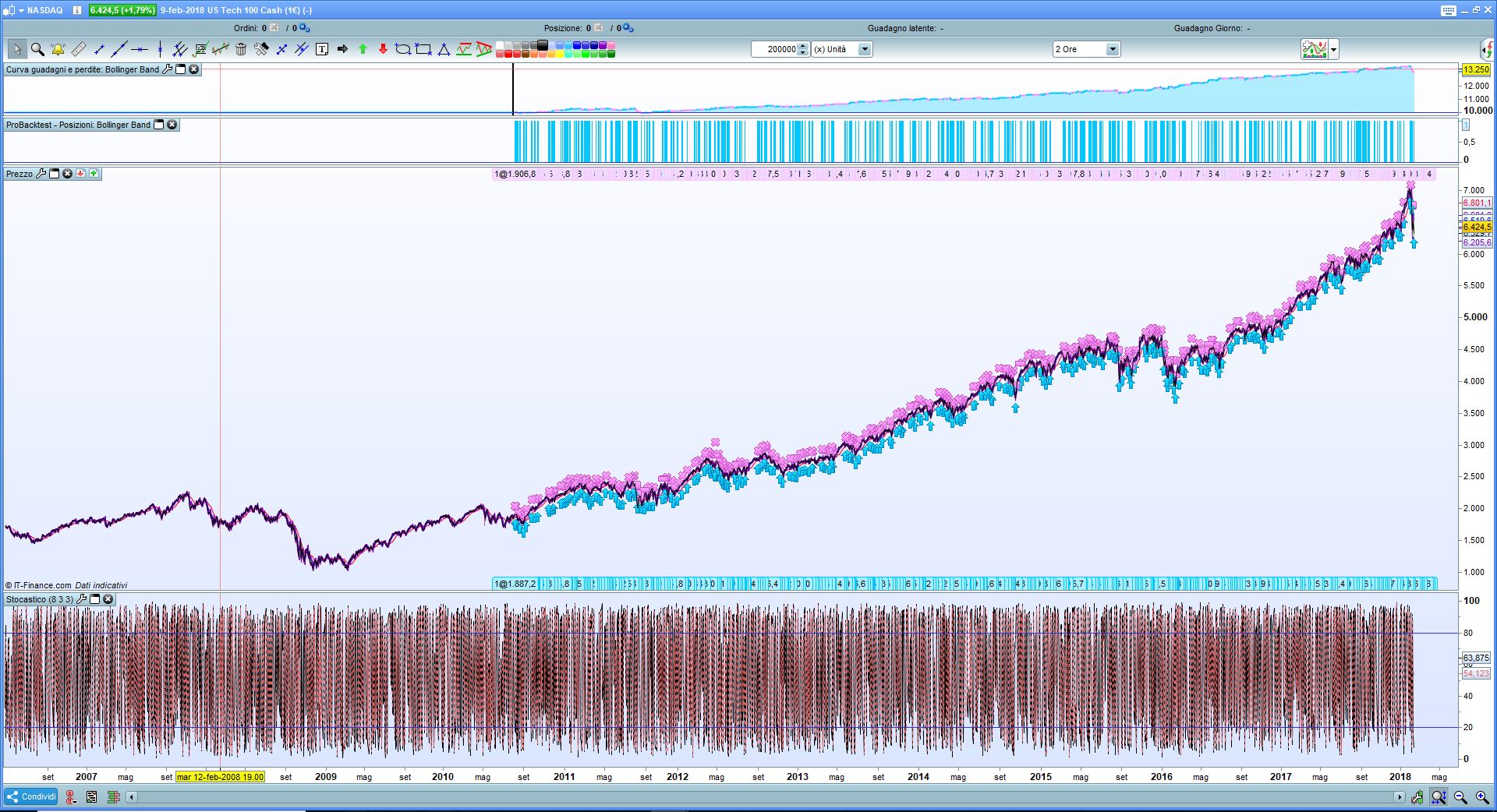

ps. negli screen la strategia è settata sul nasdaq, penso possa essere configurata agilmente anche su altri mercati.

Che ne pensate?

// Definizione dei parametri del codice

DEFPARAM CumulateOrders = false // Posizioni cumulate disattivate

ONCE startTime = 90000 // start time of trading window

ONCE endTime = 210000 // end time of trading window

///PARAMETRI

ONCE OKLONG = 1 // 1 LONG ON 0 LONG OFF

ONCE OKSHORT = 0 // 1 SHORT ON 0 SHORT OFF

ONCE stopLossLong = 5.2 // in %

ONCE stopLossShort = 0.8 // in %

ONCE takeProfitLong = 2.2 // in %

ONCE takeProfitShort = 0.4 // in %

ONCE maxCandlesLongWithProfit = 10 //takelong profit latest after x

ONCE maxCandlesShortWithProfit = 2 // take short profit latest after

ONCE maxCandlesLongWithoutProfit = 38 // limit long loss latest after x

ONCE maxCandlesShortWithoutProfit = 9 // limit short loss latest after

ONCE trailingStartLong = 2 // in % * changed from 1.25

ONCE trailingStartShort = 2 // in %

ONCE trailingStepLong = 0.1 // in %

ONCE trailingStepShort = 0.1 // in % * changed from 0.6

//Indicatori

boldo = BollingerDown[20](close)

bolu = bollingerup[20](close)

stoc = Stochastic[8,3](close)

//mm20 = average[20]

test1 = stoc < 44

test2 = stoc > 44

// Condizioni per entrare su posizioni long

c1 = (close[1] < boldo[1])

//esci = (close crosses under mm20)

// Condizioni per entrare su posizioni short

c2 = (close[1] > bolu[1])

//////////trade

IF Time >= startTime AND Time <= endTime THEN

IF OKLONG > 0 THEN

IF c1 and test1 THEN

BUY 1 CONTRACT AT MARKET

stopLoss = stopLossLONG

takeProfit = takeProfitLONG

ENDIF

ENDIF

IF OKSHORT > 0 THEN

IF c2 and test2 THEN

SELLSHORT 1 CONTRACT AT MARKET

stopLoss = stopLossShort

takeProfit = takeProfitShort

ENDIF

endif

ENDIF

//if longonmarket then

//if esci then

//sell at market

//endif

//endif

// stop and profit management

posProfit = (((close - positionprice) * pointvalue) * countofposition) / pipsize

numberCandles = (BarIndex - TradeIndex)

m1 = posProfit > 0 AND numberCandles >= maxCandlesLongWithProfit

m2 = posProfit > 0 AND numberCandles >= maxCandlesShortWithProfit

m3 = posProfit < 0 AND numberCandles >= maxCandlesLongWithoutProfit

m4 = posProfit < 0 AND numberCandles >= maxCandlesShortWithoutProfit

// take profit after max candles

IF LONGONMARKET AND (m1 OR m3) THEN

SELL AT MARKET

ENDIF

IF SHORTONMARKET AND (m2 OR m4) THEN

EXITSHORT AT MARKET

ENDIF

// trailing stop function (convert % to pips)

trailingStartLongInPoints = tradeprice(1) * trailingStartLong / 100

trailingStartShortInPoints = tradeprice(1) * trailingStartShort / 100

trailingStepLongInPoints = tradeprice(1) * trailingStepLong / 100

trailingStepShortInPoints = tradeprice(1) * trailingStepShort / 100

// reset the stoploss value

IF NOT ONMARKET THEN

newSL = 0

ENDIF

// manage long positions

IF LONGONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND close - tradeprice(1) >= trailingStartLongInPoints * pipsize THEN

newSL = tradeprice(1) + trailingStepLongInPoints * pipsize

//stopLoss = stopLossLong * 0.1

//takeProfit = takeProfitLong * 2

ENDIF

// next moves

IF newSL > 0 AND close - newSL >= trailingStepLongInPoints * pipsize THEN

newSL = newSL + trailingStepLongInPoints * pipsize

ENDIF

ENDIF

// manage short positions

IF SHORTONMARKET THEN

// first move (breakeven)

IF newSL = 0 AND tradeprice(1) - close >= trailingStartShortInPoints * pipsize THEN

newSL = tradeprice(1) - trailingStepShortInPoints * pipsize

ENDIF

// next moves

IF newSL > 0 AND newSL - close >= trailingStepShortInPoints * pipsize THEN

newSL = newSL - trailingStepShortInPoints * pipsize

ENDIF

ENDIF

// stop order to exit the positions

IF newSL > 0 THEN

IF LONGONMARKET THEN

SELL AT newSL STOP

ENDIF

IF SHORTONMARKET THEN

EXITSHORT AT newSL STOP

ENDIF

ENDIF

// Stop e target

SET STOP %LOSS stopLoss

SET TARGET %PROFIT takeProfit

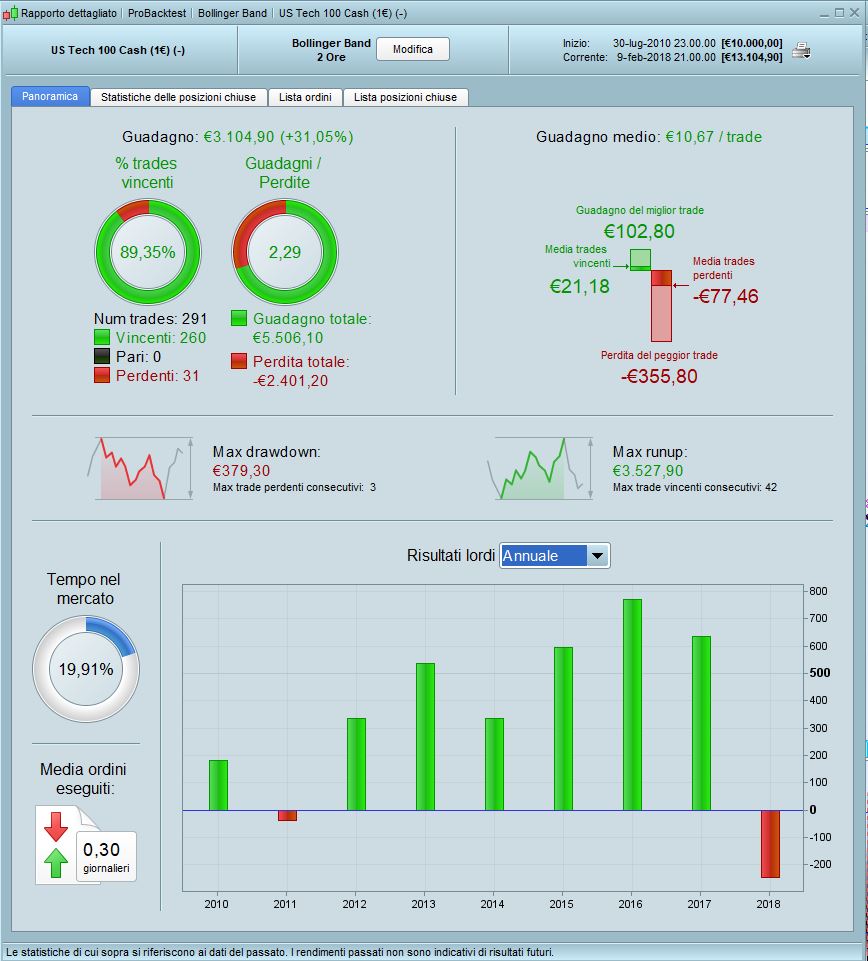

Un altro problema che ha questa strategia è che i gain sono tanti ma piccoli, mentre i loss quando ci sono sono corposi, c’e’ il rischio che a lanciarla in rial si prendano 2/3 loss che ti azzerano il conto.

ALE

ALEModerator

Master

1 time frame basso piuttosto erratico

2 usa una media lunga per filtrare le posizioni long / short

3 usa un oscillatore per filtrare Le entrare

ALEModerator

Master

Comunque non è male…

puoi anche considerare di utilizzarla solo long

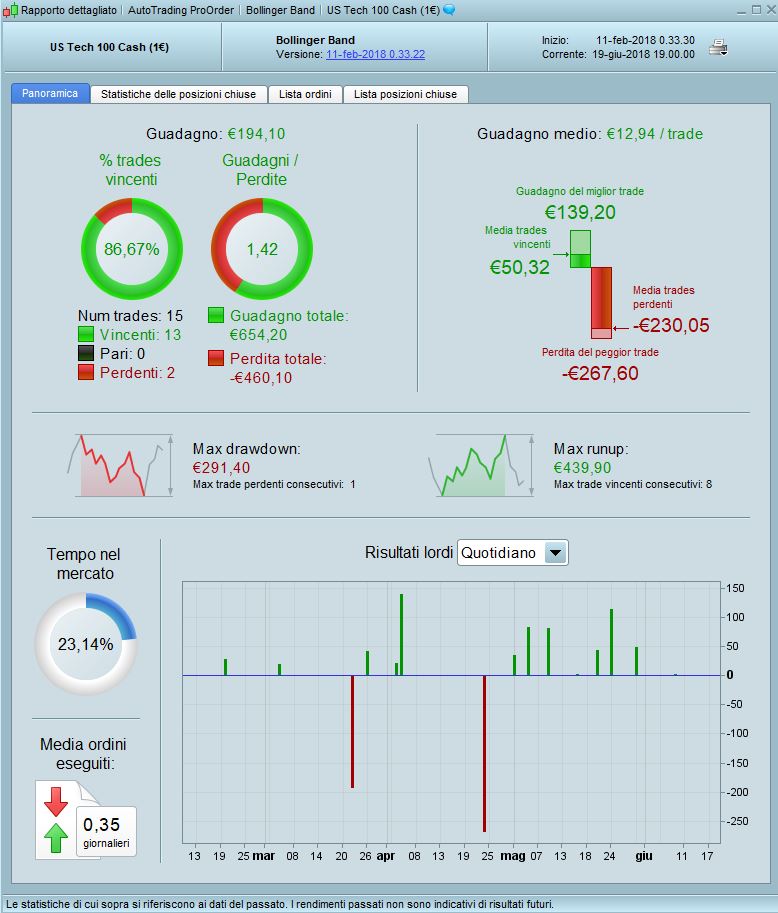

Ciao, ecco un piccolo aggiornamento dell’andamento del TS in Demo. 1 Contratto per trade.

[attachment file=”Andamento Demo Bollinger.JPG”]

Buon lavoro, si spera che il mercato continuerà a salire 🙂

Grazie per dare notizie sulla demo / live trading della tua strategia, dimostra che le cose semplici possono funzionare.

Quindi presumo che tu abbia ottimizzato le variabili? Come fai ad adattarli per periodi futuri? Hai provato a utilizzare l’analisi Walk Forward?

Buon lavoro, si spera che il mercato continuerà a salire

Grazie per dare notizie sulla demo / live trading della tua strategia, dimostra che le cose semplici possono funzionare.

Quindi presumo che tu abbia ottimizzato le variabili? Come fai ad adattarli per periodi futuri? Hai provato a utilizzare l’analisi Walk Forward?

La strategia quando è nata ottimizzata (profit e loss e il numero di barre) senza particolare attenzione alle ottimizzazioni, ma senza il walkforward, sto usando questi sei mesi come walkforward 🙂

Per quanto riguarda i mercati in salita che salgano o no alla strategia in se non importa, anzi forse per come è nata è meglio che scendano, visto che va a comprare gli ipervenduti segnalati dalle bande, certo il loss peggiore è avvenuto proprio in concomitanza con il crollo di febbraio/marzo, ma ha continuato a lavorare abbastanza bene.

ok, grazie per averlo condiviso qui comunque!

wella…avevi apportato altre modifiche a questo codice.?

era stato migliorato ? somiglia ad una strategià che ho già.