BC

BCParticipant

Master

I found this strategy from below website, made some minor modification, and add a MA filter, 240 per unit to simulate a daily MA.

https://www.babypips.com/trading/system-short-term-bollinger-reversion-180426

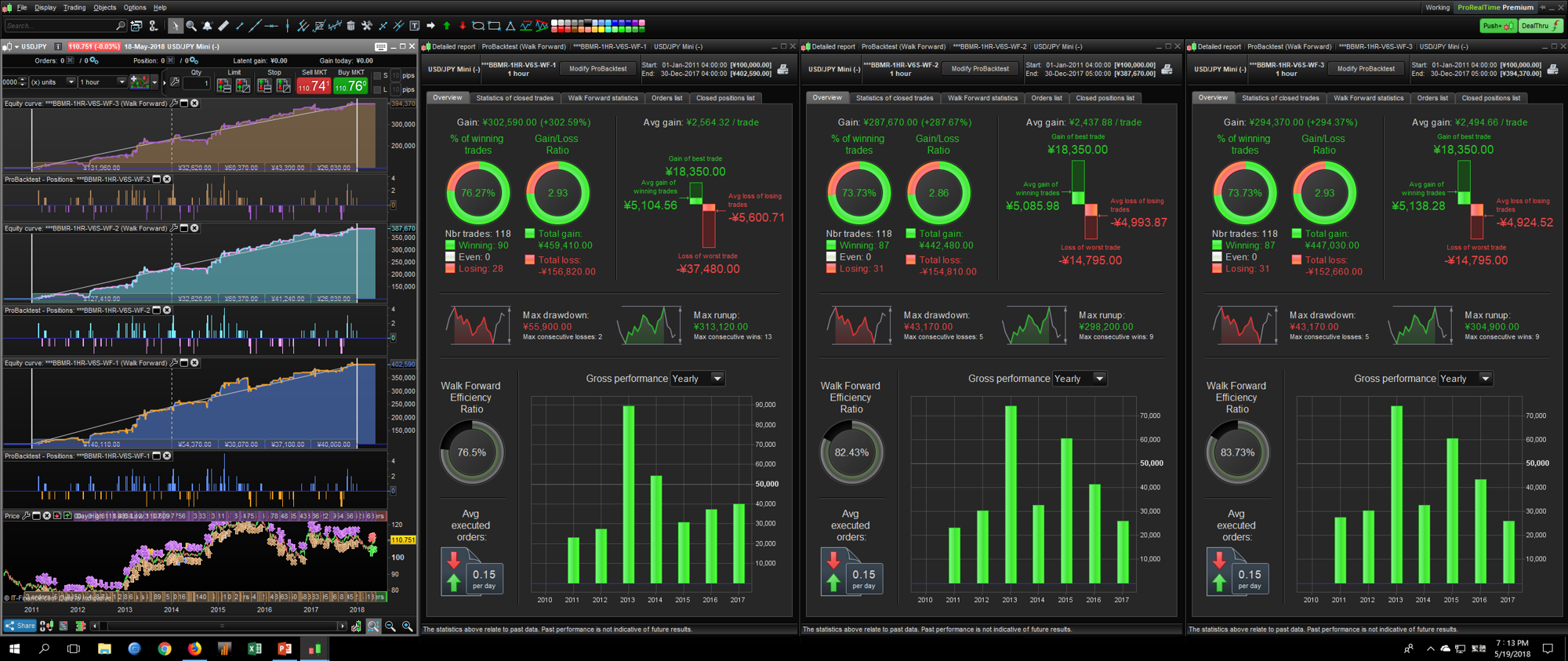

Walk forward by MA filter, stop loss and target profit screen capture attached.

Please enjoy and comment.

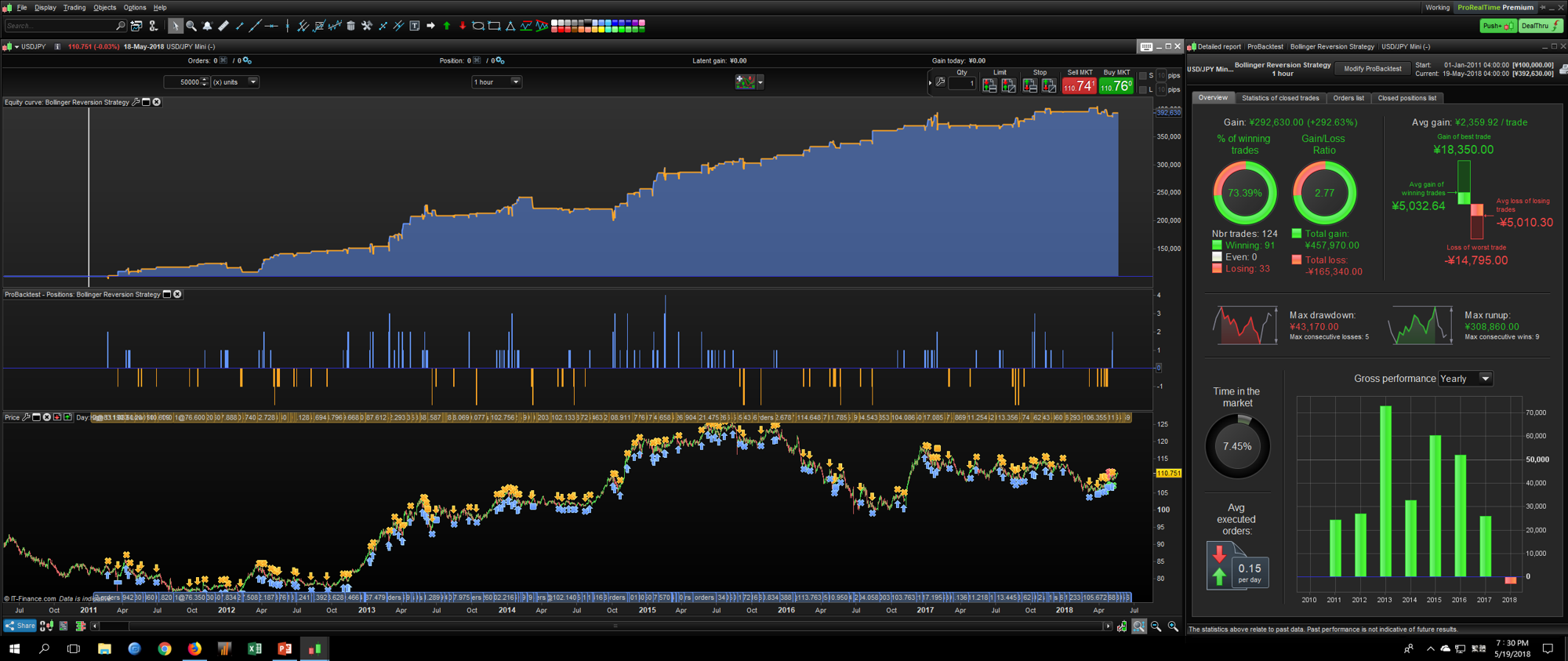

// Bollinger Reversion Strategy

// Market: USD-JPY

// Time Frame: 1 Hour

// Time Zone: Any

// Spread: 2

// Original Idea from below website

// https://www.babypips.com/trading/system-short-term-bollinger-reversion-180426

defparam preloadbars = 5000

defparam cumulateorders = True

// no MM Position Size

Once noMMPositionSizeLong = 1

Once noMMPositionSizeShort = 1

// Optional Function ( 1 = Enable 0 = Disable )

BollingerMiddleExit = 1

BollingerUpDownExit = 0

MAFilter = 1

MaxStopLoss = 1

MaxTargetProfit = 1

MoneyManagement = 0

// Main Indicators Parameters Setup

Once BollingerMAPeriods = 50 // Not Optimize

Once RSIPeriods = 9 // Not Optimize

// Optional Function Parameters Setup

// MA Filter

If MAFilter then

Once MAFilterPeriods = 1680 // Variables Optimized, Range: 240-2400 Step: 240

TrendMA = Average[MAFilterPeriods](close)

LongMAFilter = Close > TrendMA

ShortMAFilter = Close < TrendMA

Endif

// 1) MaxStopLoss Setting

If MaxStopLoss then

//Long

ONCE stopLossLong = 1.4 // by %, Variables Optimized

//Short

ONCE stopLossShort = 1 // by %, Variables Optimized

Endif

//2) Target Profit Setting

If MaxTargetProfit then

//Long

ONCE takeProfitLong = 1.2 // by %, Variables Optimized

//Short

ONCE takeProfitShort = 1 // by %, Variables Optimized

Endif

// Money Management

If MoneyManagement then

Once StartPositionSize = 1

Once Size = StartPositionSize

Once InitialCapital = (100000*Size)

Once LastBalance = 0

Equity = InitialCapital + LastBalance + StrategyProfit

Once MaxPosition = 100

Once StepX = InitialCapital * 1

For TimesX = 1 to MaxPosition Do

If Equity >= StepX * TimesX then

PositionSize = Size * TimesX

ElsIf Equity <= InitialCapital then

PositionSize = StartPositionSize

endif

Next

PositionSizeLong = PositionSize

PositionSizeShort = PositionSize

// Fuse System

Once CloseBalanceMaxDrop = 50

If equity<QuickLevel then

Quit

Endif

RecordHighest = MAX(RecordHighest,Equity)

QuickLevel = RecordHighest*((100-CloseBalanceMaxDrop)/100)

Endif

//Core Indicator

MyBollingerUpBand = BollingerUp[BollingerMAPeriods](close)

MyBollingerLowBand = BollingerDown[BollingerMAPeriods](close)

MyBollingerMidBand = Average[BollingerMAPeriods](close)

MyRSILong = RSI[RSIPeriods](close)

MyRSIShort = RSI[RSIPeriods](close)

//Long Setup

LongCondition1 = Close < Open

LongCondition2 = Low < MyBollingerLowBand

LongCondition3 = Close > MyBollingerLowBand

LongCondition4 = High < MyBollingerMidBand

LongCondition5 = MyRSILong < 30 // Not Optimize

LongSignal = LongCondition1 and LongCondition2 and LongCondition3 and LongCondition4 and LongCondition5

//Short Setup

ShortCondition1 = Open > Close

ShortCondition2 = High > MyBollingerUpBand

ShortCondition3 = Close < MyBollingerUpBand

ShortCondition4 = Low > MyBollingerMidBand

ShortCondition5 = MyRSIShort > 70 // Not Optimize

ShortSignal = ShortCondition1 and ShortCondition2 and ShortCondition3 and ShortCondition4 and ShortCondition5

//Trading Action

GoLong = LongSignal

GoShort = ShortSignal

If MAFilter then

GoLong = LongSignal and LongMAFilter

GoShort = ShortSignal and ShortMAFilter

Endif

//Long Entry

If GoLong then

If MoneyManagement then

Buy PositionSizeLong Contract at Market

Else

Buy noMMPositionSizeLong Contract at Market

Endif

If MaxStopLoss then

StopLoss = StopLossLong

Endif

If MaxTargetProfit then

TakeProfit = TakeProfitLong

Endif

Endif

//Short entry

If GoShort then

If MoneyManagement then

SellShort PositionSizeShort Contract at Market

Else

SellShort noMMPositionSizeShort Contract at Market

Endif

If MaxStopLoss then

StopLoss = StopLossShort

Endif

If MaxTargetProfit then

TakeProfit = TakeProfitShort

Endif

Endif

// Bollinger Middle Exit

If BollingerMiddleExit then

If LongonMarket and Close > MyBollingerMidBand then

Sell at Market

Endif

If ShortonMarket and Close < MyBollingerMidBand then

ExitShort at Market

Endif

Endif

// Bollinger Up Down Exit

If BollingerUpDownExit then

If LongonMarket and Close > MyBollingerUpBand then

Sell at Market

Endif

If ShortonMarket and Close < MyBollingerLowBand then

ExitShort at Market

Endif

Endif

// Stop Loss

If MaxStopLoss then

Set Stop %Loss StopLoss

Endif

// Target Profit

If MaxTargetProfit then

Set Target %Profit TakeProfit

Endif

, please enjoy and comment.

BCParticipant

Master

Another version with different SL, TP method and exit module.

good strategy , only consideration is few trade

only consideration is few trade

Unfortunately this is quite often the way. Some of the best strategies place very few trades – but good trades, unfortunately the lack of trades makes them tough to test for robustness. A portfolio of many strategies that place few trades but good trades is a desirable thing to have but achieving this can be difficult due to the time required to prove robustness on this type of strategy. Also lots of strategies means the potential of lots of positions open at the same time so a big bank is needed to avoid ruin in this scenario.

Sometimes it just seems easier to buy an ETF and open a beer and just get on with life!

BCParticipant

Master

Hi Vonsai

😩😩😩😩I wish someday I can meet u and beer togeher

Hi Bin

Thanks for sharing I like this strategy much! This one is pretty similar as my trading habit as I always look for the opportunities of BB reversal.

Apart from RSI, Stochastic is one of my favorite indicator combining with BB for determining a reversal e.g. <20 go long, >80 go short. Could be a good filter maybe : P

Best

Hang

COngrats for this work

COuld you test the strategy also for other FOREX ?

Thanks