Hi Grahal,

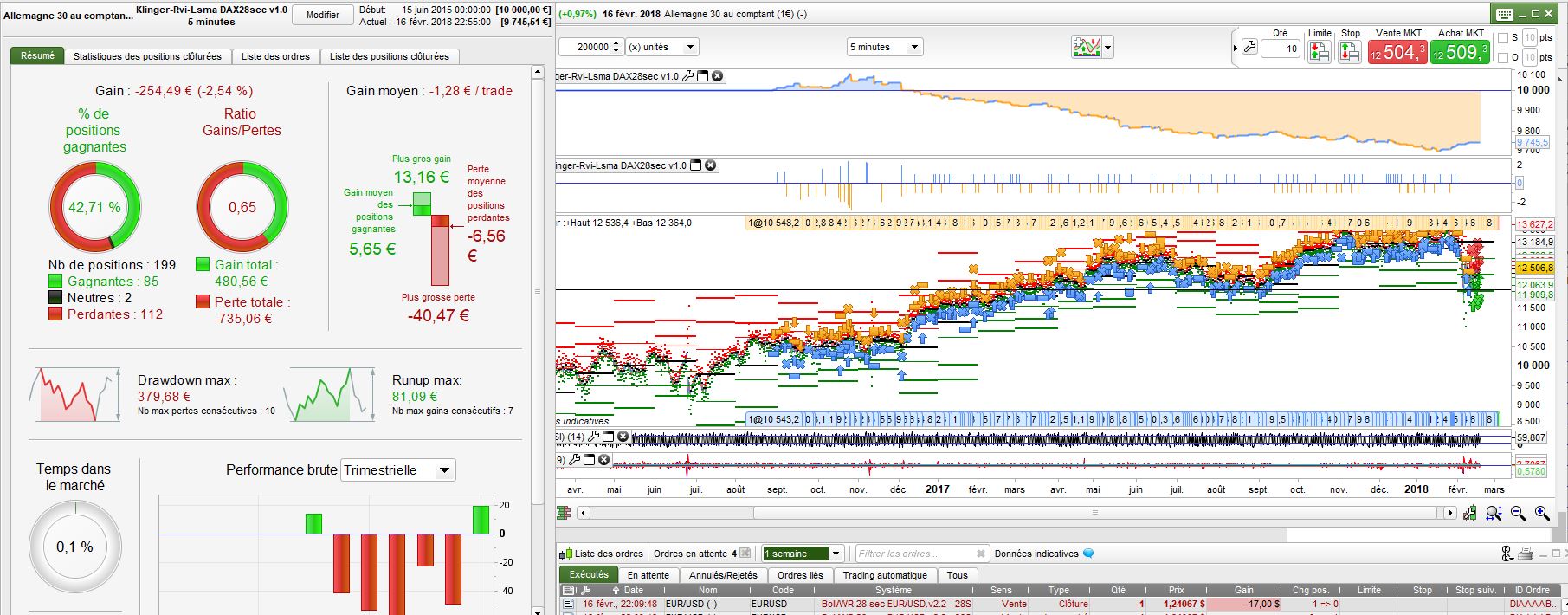

I’m just searching for a winning strategy in live! and for the moment I found nothing… So here is the backtest in 5mn TF with your proposition of TP 5 and SL 15. I’ve tried an optimisation with lots of other variables but no configuration brings gain. I will test other possibilities and post here if i find something good. But I am very careful, because all the promising backtests I’ve seen have lead to losses in demo or real.

Hi Aloysius the TP 5 and SL 15 I proposed were relevant only for the period I displayed / optimised over … 10,000 bars (and maybe going forward for weeks / months until there is an observed deviation from % winning trades and Gain to Loss ratio etc following optimisation)

Also if you backtested Gertrade version then you have backtested a 28 Sec TF version over 200,00 bars @ 5 Min TF?

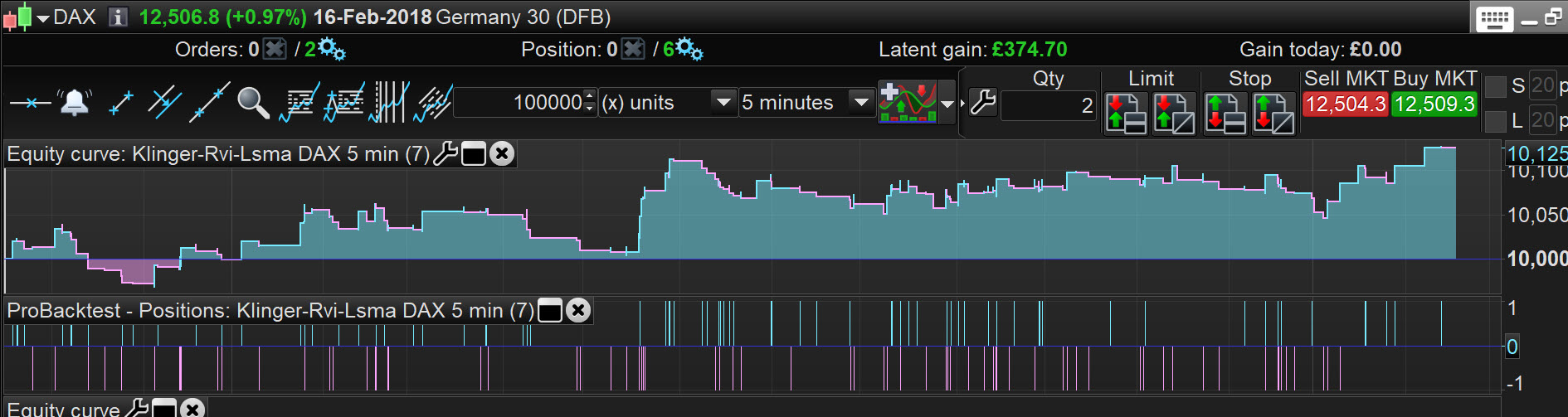

Attached results of original Roberto 5 Min version over 100,000 bars @ £1 per point. I have only optimised TP, SL and the Trailing Stop Variables as below.

I am considering that Algos on this Thread may need optimising every 3 months / 5000 bars.

Cheers

GraHal

//-------------------------------------------------------------------------

// Klinger-Rvi-Lsma DAX 5 min

//-------------------------------------------------------------------------

DEFPARAM CumulateOrders = False

DEFPARAM FlatBefore = 090000 //no trades before 09:00:00

DEFPARAM FlatAfter = 213000 //no trades after 21:30:00

ONCE nLots = 1 //number of LOTs traded

ONCE TP = 20 //23 pips Take Profit

ONCE SL = 16 //16 pips Stop Loss

RviVal, RviSignal = CALL "RVI by John Ehlers"[7] //7

KlingerVal, KlingerTrigger = CALL "Klinger oscillator"[25,44,55,1] //25,44,55,1 (ema)

LeastSquareEMA = CALL "ELSMA - Least Square EMA"[11,4] //11,4

//***************************************************************************************

IF LongOnMarket THEN

IF close < LeastSquareEMA THEN

SELL AT MARKET //Exit LONGs when MACD reverses southwards

ENDIF

ENDIF

IF ShortOnMarket THEN

IF close > LeastSquareEMA THEN

EXITSHORT AT MARKET //Exit SHORTs when MACD reverses northwards

ENDIF

ENDIF

//***************************************************************************************

trailingstart = 20//10 trailing will start @trailinstart points profit

trailingstep = 2 //13 trailing step to move the "stoploss"

//reset the stoploss value

IF NOT ONMARKET THEN

newSL=0

ENDIF

//manage long positions

IF LONGONMARKET THEN

//first move (breakeven)

IF newSL=0 AND close-tradeprice(1)>=trailingstart*pipsize THEN

newSL = tradeprice(1)+trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND close-newSL>=trailingstep*pipsize THEN

newSL = newSL+trailingstep*pipsize

ENDIF

ENDIF

//manage short positions

IF SHORTONMARKET THEN

//first move (breakeven)

IF newSL=0 AND tradeprice(1)-close>=trailingstart*pipsize THEN

newSL = tradeprice(1)-trailingstep*pipsize

ENDIF

//next moves

IF newSL>0 AND newSL-close>=trailingstep*pipsize THEN

newSL = newSL-trailingstep*pipsize

ENDIF

ENDIF

//stop order to exit the positions

IF newSL>0 THEN

SELL AT newSL STOP

EXITSHORT AT newSL STOP

ENDIF

//***************************************************************************************

// LONG trades

//***************************************************************************************

a1 = close > open //BULLish bar

a2 = KlingerTrigger CROSSES OVER KlingerVal //Klinger trigger is going north

a3 = RviSignal CROSSES OVER RviVal //RVI long signal occurred

IF a1 AND a2 AND a3 THEN

BUY nLots CONTRACT AT MARKET

ENDIF

//***************************************************************************************

// SHORT trades

//***************************************************************************************

b1 = close < open //BEARish bar

b2 = KlingerTrigger CROSSES UNDER KlingerVal //Klinger trigger is going south

b3 = RviSignal CROSSES UNDER RviVal //RVI short signal occurred

IF b1 AND b2 AND b3 THEN

SELLSHORT nLots CONTRACT AT MARKET

ENDIF

//

SET TARGET PPROFIT TP

SET STOP PLOSS SL

@ Grahal,

I realized the importance of history, I recognize that 20,000 units of history on the TF below the minute, it seems to me insufficient to validate a strategy. Right now, I’m doing tests on a TF 1 min, but I’m facing a major problem, how is it possible to make optimizations of variables of a complete strategy on 100,000 units? My PC is not powerful enough for that.

I Grahal,

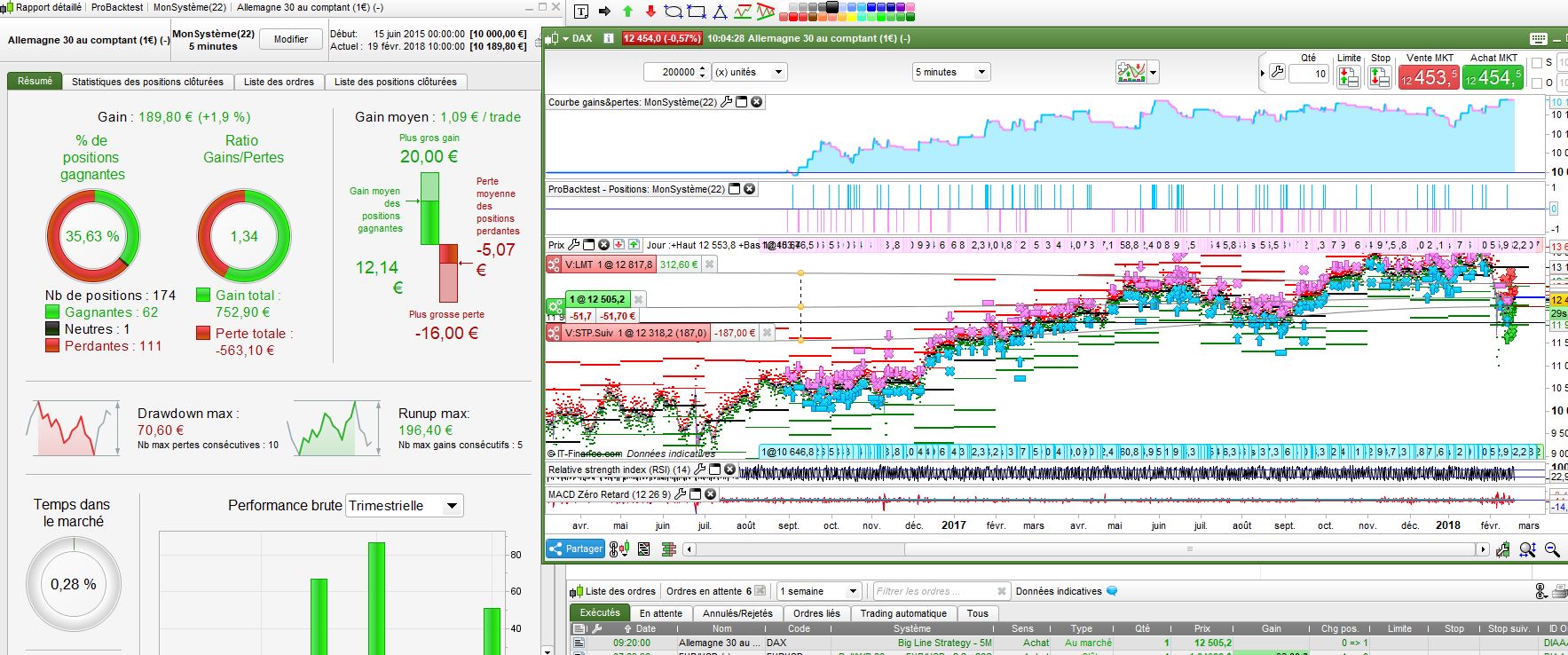

Yes I backtested Gertrade version for 28s, in 5mn TF, because you announced good results in this configuration. But your answer shows we have not the same approach of backtests: when a backtest is good for a little period it has been optimised for, and loosing at other periods, I don’t trust it and don’t think it will be good for some weeks. Anyway, here is the 200 000 bars backtest for Roberto code in 5mn, in the version you just posted: it looks promising, thank you.

@Gertrade you say … how is it possible to make optimizations of variables of a complete strategy on 100,000 units? My PC is not powerful enough for that … is your PC seeming to do nothing for ages then a quick spurt of results in the optimisation table then nothing then spurt … etc? If Yes then we all have that issue not matter how powerful our PCs … its due to optimise processing happening on the remote PRT Server.

If No to above, then what symptoms are you getting that makes you think you PC is not powerful enough?

GraHal

PS @Aloysius I do think same as you re not trusting if loose over longer Out of Sample / OOS period. Thank you for posting the 200,000 bar results.

@gertrade having said above re a spurt then a few results show in the Table then wait then another spurt etc … I have just backtested / optimised another Algo over 100,000 bars @ 5 Min TF and it completes in around 30 seconds with a lot less wait and a lot faster spurts.

So speed of optimising / backtest does depend on how complex the code is and if there any ‘ Indicator Calls’ (the code I’m checking doesn’t have any Calls).

GraHal