@Despair remember that the purpose was to create a strategy that can be adapted to any market by only optimizing the timeframe within which it is allowed to open trades.

As per my original description “Note that this strategy was not meant to be a jaw dropper in terms of performance but rather a proof of concept that a single strategy can be applied to different markets with positive results”

By doing so I could make it work on all the indexes and FX pairs I tested. Obviously, the results weren’t very good on a lot of them but almost always it managed to end in the positive given a decent enough time period.

No other strategy I have ever tested in its raw form was able to achieve this.

Remember I placed a challenge for all members of this community to contribute to this concept, albeit none participated.

Profitable strategy that work on any market

Yes, I understood all this and you did a great job. I was just curious if you managed to get little outstanding results for any asset. I also tested it on quite some assets and most were positive but not really that you could make it work in the long run. The EURUSD version stands out in this aspect. There the results are pretty nice and consistent.

I only found results that were also promising for AUDJPY.

It is of no surprise to me the lack of mechanical thus back testable strategies.

Hello

a strategy that is supposed to be applicable on any market and without any optimisation is triangle breakout.

https://www.prorealcode.com/topic/pseudo-triangle-trading-system-5-min-using-volume-and-volatity/

Eric

EricParticipant

Master

It is of no surprise to me the lack of successful mechanical systems with positive backtest results.

would you share for free a system that makes a lot of $?

Leo

LeoParticipant

Veteran

It is of no surprise to me the lack of successful mechanical systems with positive backtest results.

would you share for free a system that makes a lot of $?

Hi Eric, can you tell me why would you not share your code and why yes?

I am developing a modular code which means you can add/delete any paragraph and it still works so it can easily be developed further over time.

In the code, there are multiple conditions and each condition can be either zero or will be given a value based on how important that condition is. If the total value of all conditions is higher than Criteria (Can be determined by PRT) then Buy. The code is only to buy and will only sell if trailing stop is triggered. I put the code a new post as this post is getting too long.

https://www.prorealcode.com/topic/modular-code/

Hi, found this message on the internet after searching for this number serie

“Goichi Hosada spent 4.5years studying both eastern and western number theories and the core numbers he got out of his studies were 9, 17, and 26. When one really understands the entire ichimoku number system, the rest really come out of these numbers, but perhaps I’ll talk about this further in the future.

I’ll be writing an article on my website soon, but the main ichimoku numbers have a certain vibration that hosada had discovered, and that is why I always recommend keeping the original ichimoku numbers regardless of time frame.

Hope this helps

Kind Regards,

Chris Capre

Founder

2ndSkiesForex”

Hi Juanji,

DId you work in live trading with the strategy in post numb. #42371 , IT’s seems good also on 200k ?

REgards

Paul

PaulParticipant

Master

What about a strategy that trades big lines only?

The idea is that there is more support or resistance, which is applicable in any market I guess. So the right position has then a higher chance of success.

Here a quick strategy for the dax 5min timeframe with stop loss and trailing stop at 1% and spread set to 1

Would be nice though if biglines were automatically defined based on close.

//-------------------------------------------------------------------------

// Main code : template_test

//-------------------------------------------------------------------------

// common rules

DEFPARAM CUMULATEORDERS = false

DEFPARAM PRELOADBARS = 10000

//DEFPARAM FLATBEFORE = 100000

//DEFPARAM FLATAFTER = 200000

// time rules

ONCE entertime = 090000

ONCE lasttime = 183000

ONCE closetime = 240000

ONCE closetimefriday=210000

tt1 = time >= entertime

tt2 = time <= lasttime

tradetime = tt1 and tt2

// positionsize and stops

positionsize=1

sl=1

ts=1

// setup number of trades intraday

if IntradayBarIndex = 0 then

longtradecounter = 0

Shorttradecounter = 0

endif

// trade criteria

lc = tradetime and countoflongshares < 1 and longtradecounter < 2

sc = tradetime and countofshortshares < 1 and shorttradecounter < 0

// indicator

// --- settings

l1= close crosses over 13100 or close crosses over 12100 or close crosses over 11100 or close crosses over 10100 or close crosses over 9100

l2= close crosses over 13200 or close crosses over 12200 or close crosses over 11200 or close crosses over 10200 or close crosses over 9200

l3= close crosses over 13300 or close crosses over 12300 or close crosses over 11300 or close crosses over 10300 or close crosses over 9300

l4= close crosses over 13400 or close crosses over 12400 or close crosses over 11400 or close crosses over 10400 or close crosses over 9400

l5= close crosses over 13500 or close crosses over 12500 or close crosses over 11500 or close crosses over 10500 or close crosses over 9500

l6= close crosses over 13600 or close crosses over 12600 or close crosses over 11600 or close crosses over 10600 or close crosses over 9600

l7= close crosses over 13700 or close crosses over 12700 or close crosses over 11700 or close crosses over 10700 or close crosses over 9700

l8= close crosses over 13800 or close crosses over 12800 or close crosses over 11800 or close crosses over 10800 or close crosses over 9800

l9= close crosses over 13900 or close crosses over 12900 or close crosses over 11900 or close crosses over 10900 or close crosses over 9900

l10=close crosses over 14000 or close crosses over 13000 or close crosses over 12000 or close crosses over 11100 or close crosses over 10000

s1= close crosses under 13100 or close crosses under 12100 or close crosses under 11100 or close crosses under 10100 or close crosses under 9100

s2= close crosses under 13200 or close crosses under 12200 or close crosses under 11200 or close crosses under 10200 or close crosses under 9200

s3= close crosses under 13300 or close crosses under 12300 or close crosses under 11300 or close crosses under 10300 or close crosses under 9300

s4= close crosses under 13400 or close crosses under 12400 or close crosses under 11400 or close crosses under 10400 or close crosses under 9400

s5= close crosses under 13500 or close crosses under 12500 or close crosses under 11500 or close crosses under 10500 or close crosses under 9500

s6= close crosses under 13600 or close crosses under 12600 or close crosses under 11600 or close crosses under 10600 or close crosses under 9600

s7= close crosses under 13700 or close crosses under 12700 or close crosses under 11700 or close crosses under 10700 or close crosses under 9700

s8= close crosses under 13800 or close crosses under 12800 or close crosses under 11800 or close crosses under 10800 or close crosses under 9800

s9= close crosses under 13900 or close crosses under 12900 or close crosses under 11900 or close crosses under 10900 or close crosses under 9900

s10= close crosses under 14000 or close crosses under 13000 or close crosses under 12000 or close crosses under 11000 or close crosses under 10000

If lc and (l1 or l2 or l3 or l4 or l5 or l6 or l7 or l8 or l9 or l10) and high < dhigh(1) then

buy positionsize contract at market

longtradecounter=longtradecounter + 1

endif

if sc and (s1 or s2 or s3 or s4 or s5 or s6 or s7 or s8 or s9 or s10) and low > dlow(1) then

sellshort positionsize contract at market

shorttradecounter=shorttradecounter + 1

endif

// exit all

If onmarket then

if time >= closetime then

sell at market

exitshort at market

elsif (CurrentDayOfWeek=5 and time>=closetimefriday) then

sell at market

exitshort at market

endif

endif

SET STOP %LOSS sl %TRAILING ts

//GRAPH 0 coloured(300,0,0) AS "zeroline"

//GRAPH (positionperf*100)coloured(0,0,0,255) AS "PositionPerformance"

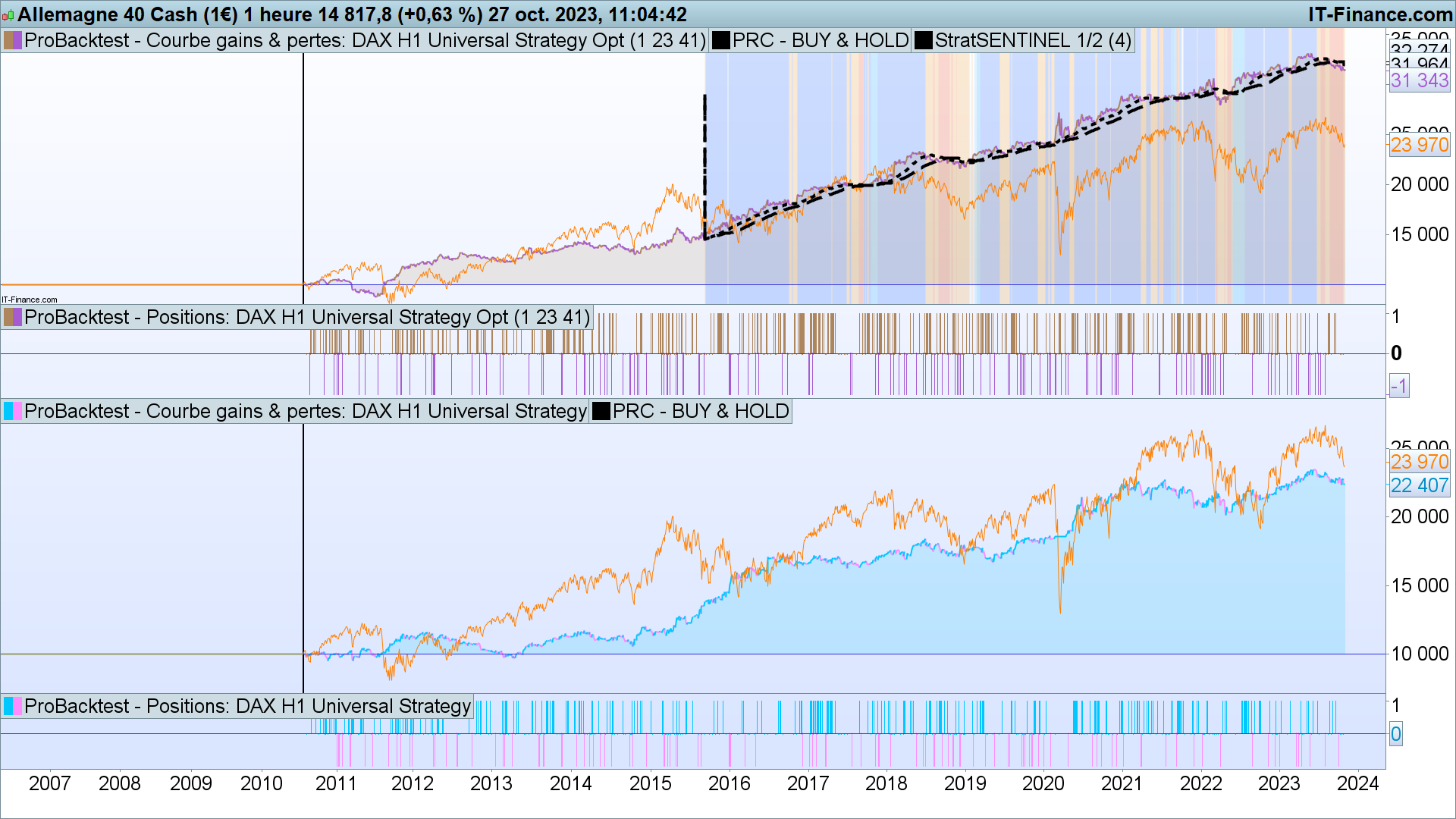

Hi Paul, interesting idea. I tested it over 200k bars and it doesn’t do so well before 2017. I think the idea or a variation of it could be made to work, maybe restrict the crosses to the 50 and 100 levels. The Dow seems particularly sensitive to those big number levels.

Hi,

Here is an optimised version of this strategy for the DAX H1;

Has anyone run this strat live?

Can anyone optimise maybe other markets?

Let’s synergize ;-))

//Stategy: Universal Bollinger Breakout/Reversal

//Author: Juan Jacobs

//Market: Neutral

//Timeframe: 1Hr but not timeframe dependant

//https://www.prorealcode.com/topic/profitable-strategy-that-work-on-any-market/

//https://www.prorealcode.com/prorealtime-trading-strategies/universal-strategy/

DEFPARAM CumulateOrders = False // Cumulating positions deactivated

//OpenH, ClosingH and VarPeriod have to be placed as variables to be optimised

// DAX: 1, 23, 41 are the optimised variable for this index

If hour > OpenH and hour < ClosingH then //(CAC: 0-18, ZA: 0-18, ,OMX: 8-11, US: 8-16, FTSE: 15-22, DOW: 8-22, EUR/USD: 9-23, AUD/USD: 3-17, GBP/USD: 10-23, EUR/GBP: 0-13, USCrude: 17-21, BrentCrude: 16-22, Gold: <2 or >22)

possize = 1

Else

possize = 0

EndIf

If dayofweek >= 5 and hour > 22 Then

If longonmarket Then

Sell at market

ElsIf shortonmarket Then

Exitshort at market

EndIf

EndIf

// Conditions to enter long positions

Periods = VarPeriod //42

Deviations = 1.618

PriceStrat = LOG(customclose)

alpha = 2/(PERIODS+1)

if barindex < PERIODS then

EWMA = AVERAGE[3](PriceStrat)

else

EWMA = alpha * PriceStrat + (1-alpha)*EWMA

endif

error = PriceStrat - EWMA

dev = SQUARE(error)

if barindex < PERIODS+1 then

var = dev

else

var = alpha * dev + (1-alpha) * var

endif

ESD = SQRT(var)

BollU = EXP(EWMA + (DEVIATIONS*ESD))

BollL = EXP(EWMA - (DEVIATIONS*ESD))

LongMA = Average[100](close)

RS2 = RSI[2](close)

ATR = AverageTrueRange[2](close)

If close > LongMA and RS2 > 70 and close[1] > BollU and close > BollU and open > open[2] Then

Buy possize contract at market

ElsIf close > LongMA and RS2 < 50 and close[1] > BollU and close < BollU Then

Sellshort possize contract at market

EndIf

If close < LongMA and RS2 < 40 and close[1] < BollL and close < BollL and open < open[2] Then

Sellshort possize contract at market

ElsIf close < LongMA and RS2 > 50 and close[1] < BollL and close > BollL Then

Buy possize contract at market

EndIf

If longonmarket and ((close < close[1] - ATR and RS2 < 5)) Then

Sell at market

ElsIf shortonmarket and ((close > close[1] + ATR and RS2 > 95)) Then

Exitshort at market

EndIf

Well, the only thing that i see is that all those strats does not really do better than buy and hold…

If you had invest in DAX in 2010/2011, you would have done x3, whil the stratgy do only little more thn x2.

So for me they do not worth being used.

I suppose we have all searched for, or at least though about the idea of a strategy that could be applied to any market (regardless of the spread) and be profitable.

So I want to put a challenge out here to create such a strategy:

I have myself been trying to develop such a strategy for quite some time and think I might of finally found one. And I will be sharing it here, but first I want some participation.

My criteria for such a strategy is simple:

- The strategy must remain completely un-optimized (i.e. other than the spread all code must be static) – average spread have to be taken into account.

- The strategy does not have to outperform buy and hold or have exceptional returns but it has to be in the blue regardless whether the market ends in the blue or not.

- The strategy must work on any market (Forex pairs, Indexes, etc.)

Some pointers from my experience:

…

What I was able to achieve so far is a market neutral strategy that could remain profitable in all of the major FX pairs as well as the US500 and other major indexes.

A “strategy that could be applied to any market” and that must “remain completely un-optimized” would work the same for any market and any time, and for eternity!

I would add to make the challenge even more fun : it has to work in any time frame!

If it’s doable, there is only one way to do this, to my point of view :

1 – The stratrgy have to identify first the type of the market (trending up or down ot ranging market)

2 – Use only Price action rules (No indicators at all or maybe only moving average ?!)

Even RSI with 2 periods is a bad idea, because RSI levels are sensible to time frame (extreme readings of rsi are not the same on 4h time frame and 5 min time frame…)