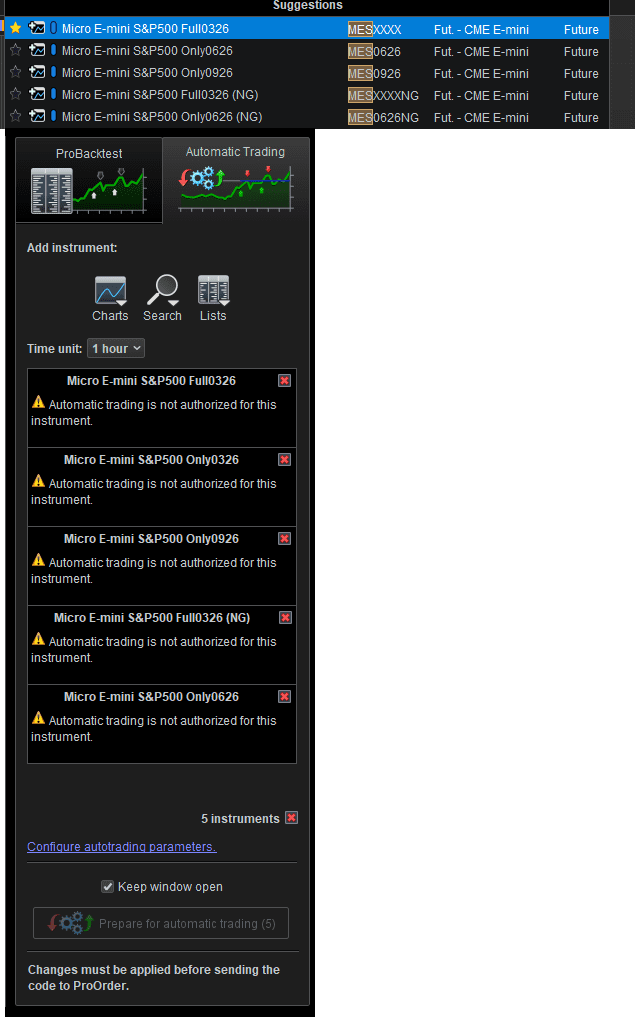

i cant seem to algotrade on any of the MES or ES or any other instrument i try? What am i doing wrong here? Something wrong with my account or whats the deal..

Okay i was approved for PRT to trade futures but not in IBKR, i am now approved but still same error pops up but im guessing its going to take a day or smthn before the data has been updated with prorealtime.. lets see if im able to do hit “start trading” tomorrow haha…

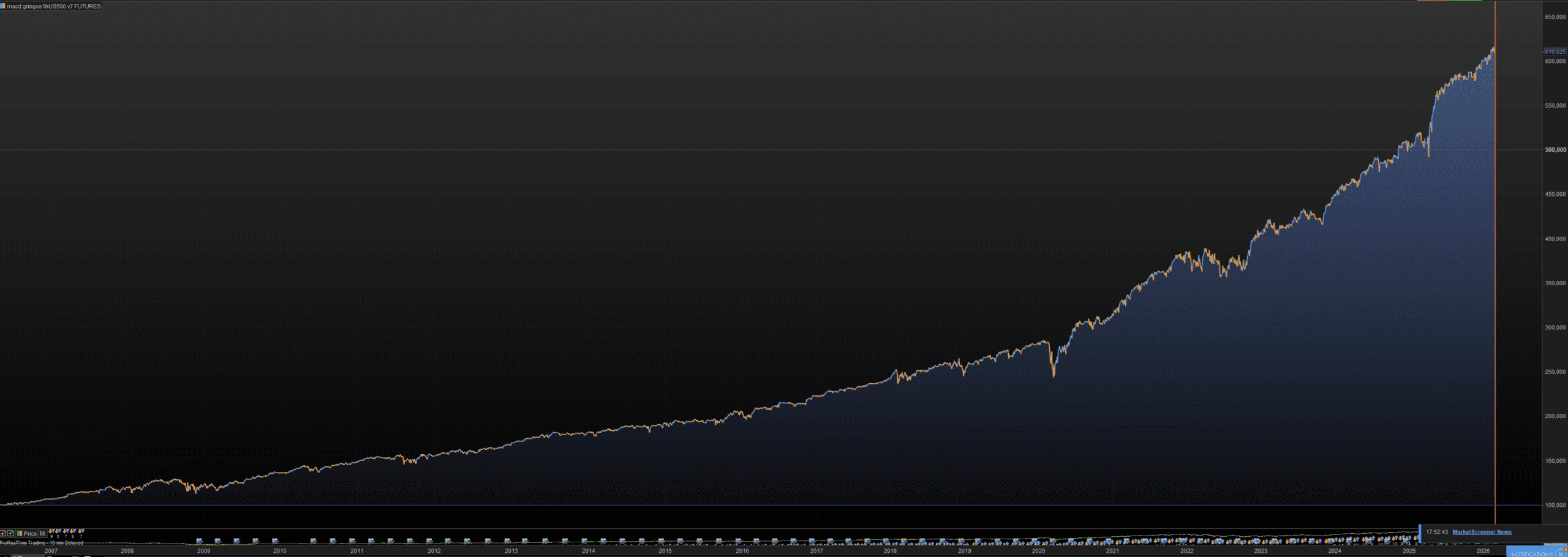

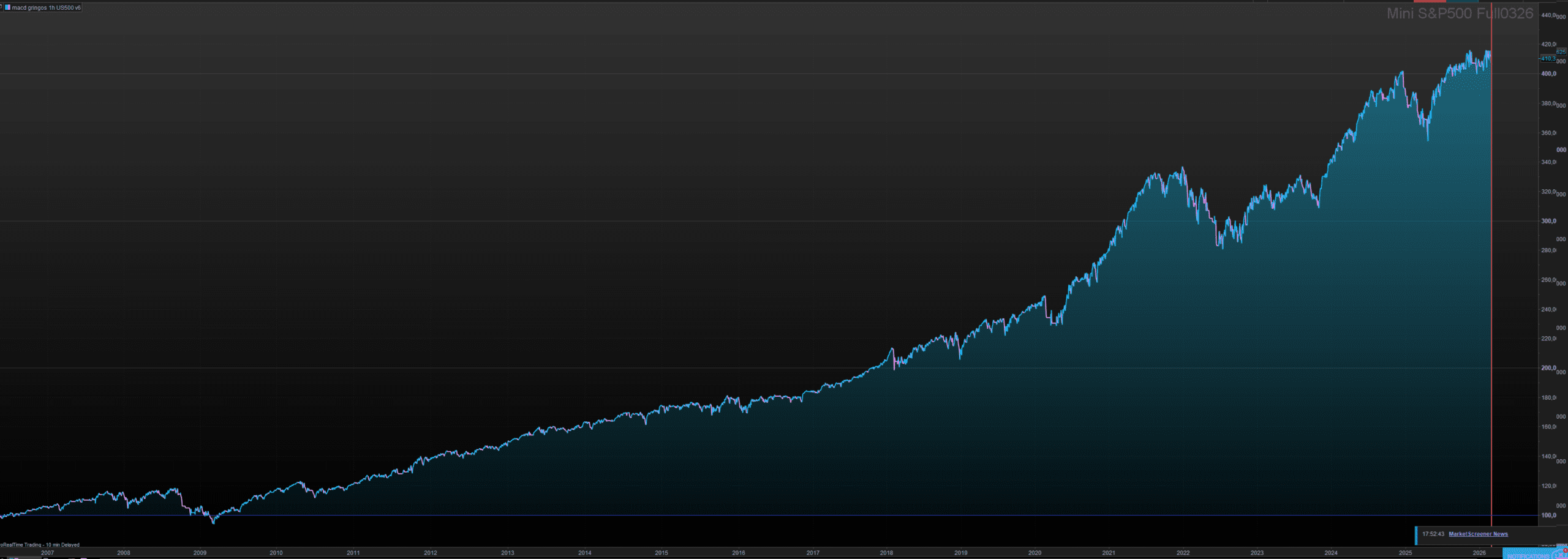

i have now optimized my algo for futuresmarked, had to readjust some of my variables, i dont like doing it because the “OG” code has been running for many years now on CFD, but ive changed the variables just slightly and its now looking pretty decent for futures marked also

Thats the Before (light blue) and after (dark blue)

Fingers crossed i havnt completly overfit and facked myself going forward ……

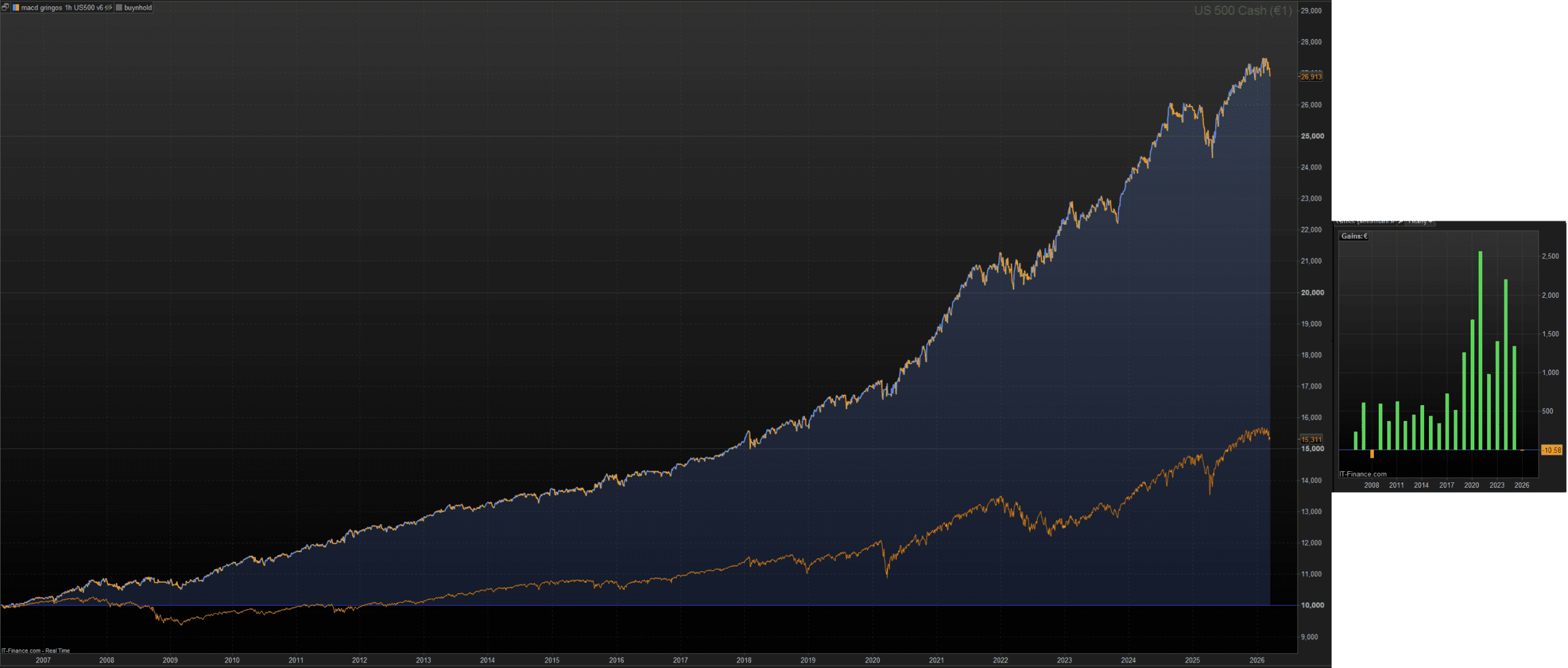

It seems like a buy-and-hold strategy… it’s not suitable for CFDs or futures at all. What you need is monthly investments in QQQ or SPY.

Its not buy and hold and it beats buy and hold by far when comparing max drawdown vs profits.. Not sure how even looking at the graph you can say “Its buy and hold”

Its around 50% winrate and 2.2 in profit/loss ratio for 1h US500

jebus89 wrote: Its not buy and hold and it beats buy and hold by far when comparing max drawdown vs profits.. Not sure how even looking at the graph you can say “Its buy and hold” Its around 50% winrate and 2.2 in profit/loss ratio for 1h US500

Whats the time in market?

60% in market

picture is 2 contract vs buy and hold.

max drawdown 2 contracts: 1700$~

max drawdown buy n hold: 1300$~

outperforms buy n hold by 3x with a minimal increase in max $ drawdown

however that is without any cost calculated, and with 3 days AVERAGE holding time this strategy dosnt look that good comparing real life vs backtest. which is why i think comission and spread in futures will reduce cost by ALOT.. no funding cost here is gonna be nice

When you compare your Algo with buy and hold, you have to do it with the same number of contracts… Otherwise, you can apply your algo with 20 contracts and say my algo outperforms buy n hold by 30x

LucasBest wrote: When you compare your Algo with buy and hold, you have to do it with the same number of contracts… Otherwise, you can apply your algo with 20 contracts and say my algo outperforms buy n hold by 30x

i compare my algo against by and hold adjusted by risk. You can take my numbers and divide by 2 if u wanna calculate my algo vs buy and hold, so my max drawdown would then be 850 vs 1300 max drawdown for buy and hold, and my algo would still outperform buy and hold.

Just wanted to add on my thought here on how i look at buy n hold compared to my algo. Lets in theory say you got a really nice strat. Lets just say it has 80% winrate and 1.5 gain/loss ratio, however it dosnt do too many trades so if you compare 1 contract with 1 contract buy n hold, it dosnt outperform the market, however buy n hold sees a max drawdown of -50% or say -5000 points (out of 10.000 wallet to start with) but your algo sees max drawdown og -10% or say -1000 (our of same 10.000 wallet to start with) it would be wrong in my eyes to say that your algo does not outperform the market, because if you can sit through a -50%/-5000 drawdown, then in my eyes you should up the contracts of your algo to match that same max drawdown of -5000, meaning your algo can have 5 contracts and would probably by then outperform buy and hold.

If this is flawed then let me know, until then ignorance is bliss i guess haha but thats my view on comparing algo with buy and hold.

BUT would also like to say that this is not on topic of this thread anyways hehe