hello i am fred and i am a beginner in ready programming. I am trying to use your XXXDJI-M1 program, but I have a message that says: edit the code. could you help me please ?

I am not an expert, but I can try. Is this a message you get when you try to backtest the code? could you send a screenshot?

hello Lucho0712 do you speak french ?

do you speak french ?

Even if you do then please do not do so in the English speaking forums. Start a fresh topic in the French forum if you wish to discuss things in French.

hello i am calling fred i am french and i am a beginner in ready programming. I am trying to use your XXXDJI-M1 program, but I have a message that says: edit the code. could you help me please

Wahrscheinlich meinte er diese Meldung siehe Anhang. Ich kann den Code auch nicht starte. Ich soll die Variablen einfügen. Aber weiß nicht wie.

He probably meant this message see attachment. I can’t start the code either. I should insert the variables. But don’t know how.

Maik2404 – You failed to attach any image plus….

There are some simple rules that everyone using the forums is expected to follow. Your post has broken one or more of these rules.

The forum rules are as follows. I have highlighted in bold the rule/rules that you have not followed:

Post your topic in the correct forum.

ProRealTime Platform Support only platform related issues.

ProOrder only strategy topics.

ProBuilder only indicator topics.

ProScreener only screener topics

General Discussion any other topics.

Welcome New Members for new forum members to introduce themselves.

Only post in the language of the forum that you are posting in. For example English only in the English speaking forums and French only in the French speaking forums.

Always use the ‘Insert PRT Code’ button when putting code in your posts to make it easier for others to read.

Do not double post. Ask your question only once and only in one forum. All double posts will be deleted anyway so posting the same question multiple times will just be wasting your own time and will not get you an answer any quicker. Double posting just creates confusion in the forums.

Be careful when quoting others in your posts. Only use the quote option when you need to highlight a particular bit of text that you are referring to or to highlight that you are replying to a particular member if there are several involved in a conversation. Do not include large amounts of code in your quotes. Just highlight the text you want to quote and then click on ‘Quote’.

Give your topic a meaningful title. Describe your question or your subject in your title. Do not use meaningless titles such as ‘Coding Help Needed’.

Do not include personal information such as email addresses or telephone numbers in your posts. If you would like to contact another forum member directly outside of the forums then contact the forums administrator via ‘Contact Us’ and they will pass your details on to the member that you wish to contact.

Always be polite and courteous to others.

Have fun.

I have edited your post where required. Please ensure that your future posts meet these few simple forum rules. 🙂

Maik Fred, as Yahootew mentions in the original post, try downloading XXXDJI-M1-TrendImpulsev1-1.itf

That version contains the variables. Maybe it solves your problem

Coding help required. I got the message that I should use variables, but I don’t know how to edit the code. Can someone help me?

Lucho0712: I can do the backtest but if I want to start the system then I should replace the variables with specific values. The variables are predefined but always from to. Do I have to assign fixed values? How can I do that?

Thanks a lot yahootex3000.

I was looking at the DLS conditions.

Things become a bit more complicated if we live in Europe, since we too have a DLS period… but not exactly on the same period as USA !

In Europe, DLS time begins on the last Sunday of March, and ends on the last Sunday of October.

As a consequence, during 2 short periods, in March (from the 2nd Sunday to the last Sunday) and in October/November (from the las Sunday of October to the 1st Sunday of November), the time difference is only 5 hrs, while it is 6 hrs during the other part of the year. I am trying to solve the equation !

In Europe, DLS time begins on the last Sunday of March, and ends on the last Sunday of October.

Indeed, I have a code for DLS conversion of ASIA->UK, but no UK (or EUR) -> USA. Anyway, I share also the UK version here, hope it can help a bit…

// --------- UK DAY LIGHT SAVINGS MONTHS ---------------- //

mar = month = 3 // MONTH START

oct = month = 10 // MONTH END

IF ( dayofweek >= 0 and mar AND 31-day<7 ) OR ( month > 3 AND month < 10 ) OR ( oct AND 31-day > 6 ) OR (dayofweek = 4 AND oct AND day<31) OR (dayofweek = 3 AND oct AND day+1<31) OR (dayofweek = 2 AND oct AND day+2<31) OR (dayofweek = 1 AND oct AND day+3<31) OR (dayofweek = 0 AND oct AND day+4<31) OR (dayofweek = 5 AND oct AND 31-day<7) THEN

UKDLS=1

ELSE

UKDLS=0

ENDIF

Hi All,

I integrated the ML + Trailing Stop and replace the trendimpulse with bollinger, result seems better. Also added ATR to filter out the huge volatility and cause big losses or big winners (especially March) to be more practical for live.

Take note I’m taking 90-10 WFA 5 iterations to optimize the startingvalue and startingvalue2.

Please see attached.

DEFPARAM CumulateOrders = false

DEFPARAM PRELOADBARS = 1000

// --------- US DAY LIGHT SAVINGS MONTHS ---------------- //

mar = month = 3 // MONTH START

nov = month = 11 // MONTH END

IF (month > 3 AND month < 11) OR (mar AND day>14) OR (mar AND day-dayofweek>7) OR (nov AND day<=dayofweek AND day<7) THEN

USDLS=010000

ELSE

USDLS=0

ENDIF

timeok = NOT(time >051500- USDLS AND time <053000 - USDLS) AND NOT(time >060000 - USDLS AND time <070000 - USDLS)

//startingvalue = 15 //5, 100, 10 boxsize

increment = 5 //5, 20, 10

maxincrement = 7 //5, 10 limit of no of increments either up or down

reps = 3 //1 number of trades to use for analysis //2

maxvalue = 70 //20, 300, 150 //maximum allowed value

minvalue = 50 //5, minimum allowed value

//startingvalue2 = 55 //5, 100, 50 stop loss

increment2 = 3 //5, 10

maxincrement2 = 7 //1, 30 limit of no of increments either up/down //4

reps2 = 3 //1, 2 nos of trades to use for analysis //3

maxvalue2 = 25 //20, 300, 200 maximum allowed value

minvalue2 = 5 //5, minimum allowed value

heuristicscyclelimit = 2

once heuristicscycle = 0

once heuristicsalgo1 = 1

once heuristicsalgo2 = 0

if heuristicscycle >= heuristicscyclelimit then

if heuristicsalgo1 = 1 then

heuristicsalgo2 = 1

heuristicsalgo1 = 0

elsif heuristicsalgo2 = 1 then

heuristicsalgo1 = 1

heuristicsalgo2 = 0

endif

heuristicscycle = 0

else

once valuex = startingvalue

once valuey = startingvalue2

endif

if heuristicsalgo1 = 1 then

//heuristics algorithm 1 start

if (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) then

optimise = optimise + 1

endif

once valuex = startingvalue

once pincpos = 1 //positive increment position

once nincpos = 1 //negative increment position

once optimise = 0 //initialize heuristicks engine counter (must be incremented at position start or exit)

once mode1 = 1 //switches between negative and positive increments

//once wincountb = 3 //initialize best win count

//graph wincountb coloured (0,0,0) as "wincountb"

//once stratavgb = 4353 //initialize best avg strategy profit

//graph stratavgb coloured (0,0,0) as "stratavgb"

if optimise = reps then

wincounta = 0 //initialize current win count

stratavga = 0 //initialize current avg strategy profit

heuristicscycle = heuristicscycle + 1

for i = 1 to reps do

if positionperf(i) > 0 then

wincounta = wincounta + 1 //increment current wincount

endif

stratavga = stratavga + (((positionperf(i)*countofposition[i]*close)*-1)*-1)

next

stratavga = stratavga/reps //calculate current avg strategy profit

//graph (positionperf(1)*countofposition[1]*100000)*-1 as "posperf1"

//graph (positionperf(2)*countofposition[2]*100000)*-1 as "posperf2"

//graph stratavga*-1 as "stratavga"

//once besta = 300

//graph besta coloured (0,0,0) as "besta"

if stratavga >= stratavgb then

stratavgb = stratavga //update best strategy profit

besta = valuex

endif

//once bestb = 300

//graph bestb coloured (0,0,0) as "bestb"

if wincounta >= wincountb then

wincountb = wincounta //update best win count

bestb = valuex

endif

if wincounta > wincountb and stratavga > stratavgb then

mode1 = 0

elsif wincounta < wincountb and stratavga < stratavgb and mode1 = 1 then

valuex = valuex - (increment*nincpos)

nincpos = nincpos + 1

mode1 = 2

elsif wincounta >= wincountb or stratavga >= stratavgb and mode1 = 1 then

valuex = valuex + (increment*pincpos)

pincpos = pincpos + 1

mode1 = 1

elsif wincounta < wincountb and stratavga < stratavgb and mode1 = 2 then

valuex = valuex + (increment*pincpos)

pincpos = pincpos + 1

mode1 = 1

elsif wincounta >= wincountb or stratavga >= stratavgb and mode1 = 2 then

valuex = valuex - (increment*nincpos)

nincpos = nincpos + 1

mode1 = 2

endif

if nincpos > maxincrement or pincpos > maxincrement then

if besta = bestb then

valuex = besta

else

if reps >= 10 then

weightedscore = 10

else

weightedscore = round((reps/100)*100)

endif

valuex = round(((besta*(20-weightedscore)) + (bestb*weightedscore))/20) //lower reps = less weight assigned to win%

endif

nincpos = 1

pincpos = 1

elsif valuex > maxvalue then

valuex = maxvalue

elsif valuex < minvalue then

valuex = minvalue

endif

optimise = 0

endif

// heuristics algorithm 1 end

elsif heuristicsalgo2 = 1 then

// heuristics algorithm 2 start

if (onmarket[1] = 1 and onmarket = 0) or (longonmarket[1] = 1 and longonmarket and countoflongshares < countoflongshares[1]) or (longonmarket[1] = 1 and longonmarket and countoflongshares > countoflongshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares < countofshortshares[1]) or (shortonmarket[1] = 1 and shortonmarket and countofshortshares > countofshortshares[1]) or (longonmarket[1] and shortonmarket) or (shortonmarket[1] and longonmarket) then

optimise2 = optimise2 + 1

endif

once valuey = startingvalue2

once pincpos2 = 1 //positive increment position

once nincpos2 = 1 //negative increment position

once optimise2 = 0 //initialize heuristicks engine counter (must be incremented at position start or exit)

once mode2 = 1 //switches between negative and positive increments

//once wincountb2 = 3 //initialize best win count

//graph wincountb2 coloured (0,0,0) as "wincountb2"

//once stratavgb2 = 4353 //initialize best avg strategy profit

//graph stratavgb2 coloured (0,0,0) as "stratavgb2"

if optimise2 = reps2 then

wincounta2 = 0 //initialize current win count

stratavga2 = 0 //initialize current avg strategy profit

heuristicscycle = heuristicscycle + 1

for i2 = 1 to reps2 do

if positionperf(i2) > 0 then

wincounta2 = wincounta2 + 1 //increment current wincount

endif

stratavga2 = stratavga2 + (((positionperf(i2)*countofposition[i2]*close)*-1)*-1)

next

stratavga2 = stratavga2/reps2 //calculate current avg strategy profit

//graph (positionperf(1)*countofposition[1]*100000)*-1 as "posperf1-2"

//graph (positionperf(2)*countofposition[2]*100000)*-1 as "posperf2-2"

//graph stratavga2*-1 as "stratavga2"

//once besta2 = 300

//graph besta2 coloured (0,0,0) as "besta2"

if stratavga2 >= stratavgb2 then

stratavgb2 = stratavga2 //update best strategy profit

besta2 = valuey

endif

//once bestb2 = 300

//graph bestb2 coloured (0,0,0) as "bestb2"

if wincounta2 >= wincountb2 then

wincountb2 = wincounta2 //update best win count

bestb2 = valuey

endif

if wincounta2 > wincountb2 and stratavga2 > stratavgb2 then

mode2 = 0

elsif wincounta2 < wincountb2 and stratavga2 < stratavgb2 and mode2 = 1 then

valuey = valuey - (increment2*nincpos2)

nincpos2 = nincpos2 + 1

mode2 = 2

elsif wincounta2 >= wincountb2 or stratavga2 >= stratavgb2 and mode2 = 1 then

valuey = valuey + (increment2*pincpos2)

pincpos2 = pincpos2 + 1

mode2 = 1

elsif wincounta2 < wincountb2 and stratavga2 < stratavgb2 and mode2 = 2 then

valuey = valuey + (increment2*pincpos2)

pincpos2 = pincpos2 + 1

mode2 = 1

elsif wincounta2 >= wincountb2 or stratavga2 >= stratavgb2 and mode2 = 2 then

valuey = valuey - (increment2*nincpos2)

nincpos2 = nincpos2 + 1

mode2 = 2

endif

if nincpos2 > maxincrement2 or pincpos2 > maxincrement2 then

if besta2 = bestb2 then

valuey = besta2

else

if reps2 >= 10 then

weightedscore2 = 10

else

weightedscore2 = round((reps2/100)*100)

endif

valuey = round(((besta2*(20-weightedscore2)) + (bestb2*weightedscore2))/20) //lower reps = less weight assigned to win%

endif

nincpos2 = 1

pincpos2 = 1

elsif valuey > maxvalue2 then

valuey = maxvalue2

elsif valuey < minvalue2 then

valuey = minvalue2

endif

optimise2 = 0

endif

// heuristics algorithm 2 end

endif

//GRAPH valuex

//GRAPH valuey

timeframe(1 day)

volindic = (averagetruerange[5](close)/close)*100

timeframe(5 minute)

thigh1 = Highest[valuex](high)+ SlowPipDisplace*pointsize

tlow1 = Lowest[valuex](low)- SlowPipDisplace*pointsize

thigh2 = Highest[valuey](high)+ FastPipDisplace*pointsize

tlow2 = Lowest[valuey](low)- FastPipDisplace*pointsize

if barindex>2 then

if Close>line1[1] then

line1 = tlow1

else

line1 = thigh1

endif

if Close>line2[1] then

line2 = tlow2

else

line2 = thigh2

endif

endif

if (Close[0]<line1[0] and Close[0]<line2[0]) then

trend = 1

endif

if (Close[0]>line1[0] and Close[0]>line2[0]) then

trend = -1

endif

if (line1[0]>line2[0] or trend[0] = 1) then

trena = 1

endif

if (line1[0]<line2[0] or trend[0] = -1) then

trena = -1

endif

if trena<>trena[1] then

if trena=1 then

//bear

prefecttrend = 2

else

//bull

prefecttrend = 1

endif

endif

timeframe(default)

bollMA = average[length, 1](close)//50,1

STDDEV = STD[length]

bollUP = bollMA + 2 * STDDEV

bollDOWN = bollMA - 2 * STDDEV

bollPercent = 100 * (close - bollDOWN) / (bollUP - bollDOWN)

//====== Enter market - start =====

// LONG side

C1 = bollPercent > 60 AND prefecttrend[1] = 2 AND prefecttrend = 1

IF timeok AND Not OnMarket AND C1 AND volindic < 3.5 THEN

BUY 1 CONTRACT AT MARKET

SET STOP pLOSS SL

ENDIF

// SHORT side

C2 = bollPercent < 40 AND prefecttrend[1] = 1 AND prefecttrend = 2

IF timeok AND Not OnMarket AND C2 AND volindic < 3.5 THEN

SELLSHORT 1 CONTRACT AT MARKET

SET STOP pLOSS SL

ENDIF

//====== Enter market - end =====

//====== Exit market - start =====

X1 = prefecttrend[1] = 1 AND prefecttrend = 2

IF LONGONMARKET AND X1 THEN

SELL AT MARKET

ENDIF

X2 = prefecttrend[1] = 2 AND prefecttrend = 1

IF SHORTONMARKET AND X2 THEN

EXITSHORT AT MARKET

ENDIF

// Avoid losing trade not caught by training

tradegain = POSITIONPERF * 100

rangelevel = 100* (range)/close

gainenough = summation[barindex - tradeindex](tradegain > 0.2) > 1

closefast = gainenough AND rangelevel < 0.5 AND POSITIONPERF * 100 <= 0.1

IF closefast THEN

EXITSHORT AT MARKET

SELL AT MARKET

ENDIF

//====== Exit market - end =====

//====== Trailing Stop mechanism - start =====

trailingstart = (0.5 * SL ) / pointsize

trailingstep = (0.25 * SL ) / pointsize

//resetting variables when no trades are on market

if not onmarket then

priceexit = 0

endif

//case LONG order

if longonmarket then

//first move (breakeven)

IF priceexit=0 AND close-tradeprice(1) >= trailingstart*pointsize THEN

priceexit = tradeprice(1) + trailingstep*pointsize

ENDIF

//next moves

IF priceexit>0 THEN

P2 = close-priceexit >= trailingstart*pointsize

IF P2 THEN

priceexit = priceexit + trailingstep*pointsize

ENDIF

ENDIF

endif

//case SHORT order

if shortonmarket then

//first move (breakeven)

IF priceexit=0 AND tradeprice(1)-close >= trailingstart*pointsize THEN

priceexit = tradeprice(1) - trailingstep*pointsize

ENDIF

//next moves

IF priceexit>0 THEN

P2 = priceexit-close >= trailingstart*pointsize

IF P2 THEN

priceexit = priceexit - trailingstep*pointsize

ENDIF

ENDIF

endif

//exit on trailing stop price levels

if onmarket and priceexit>0 then

EXITSHORT AT priceexit STOP

SELL AT priceexit STOP

endif

//====== Trailing Stop mechanism - end =====

Hi yahootew3000

Thank you very interesting strategy. I worked a lot on your previews version. I think some entry point missed because of the closure of a previous position.

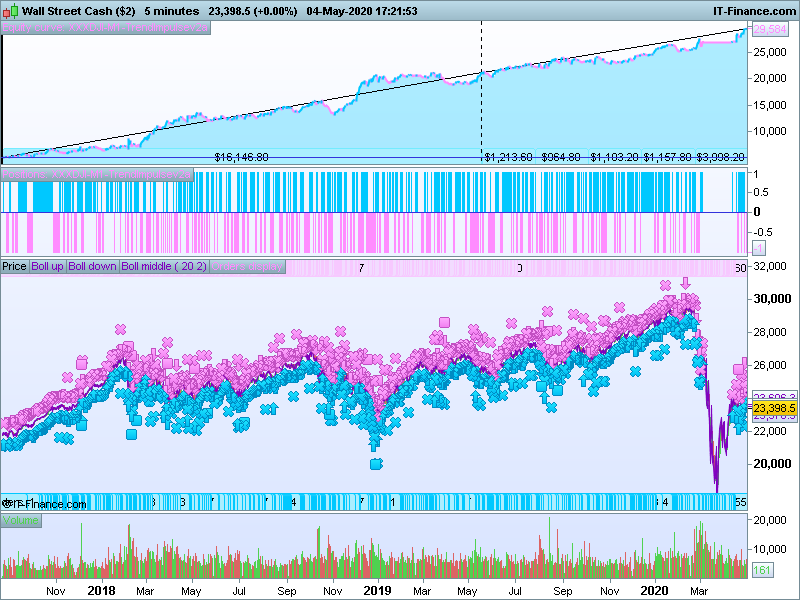

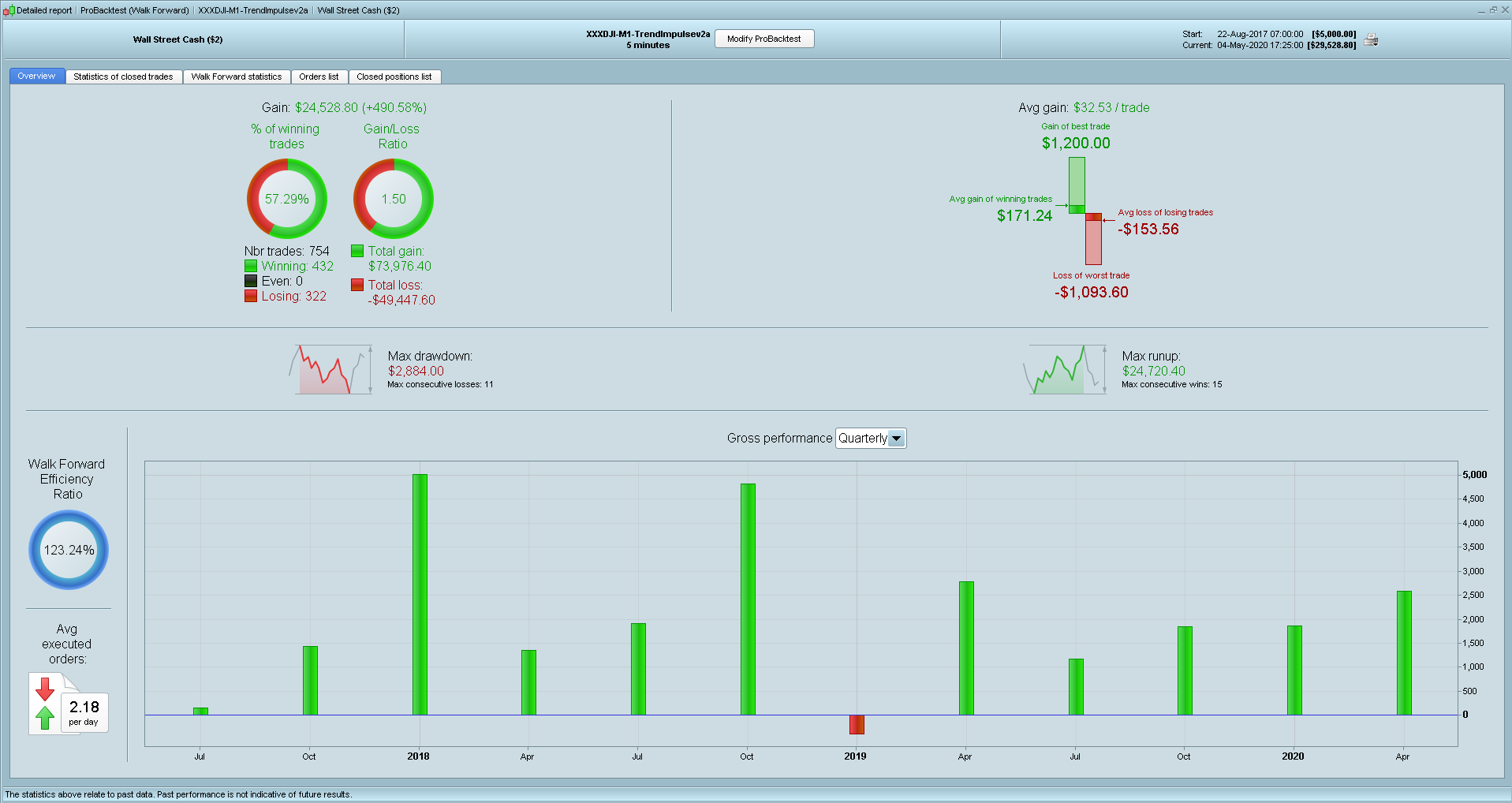

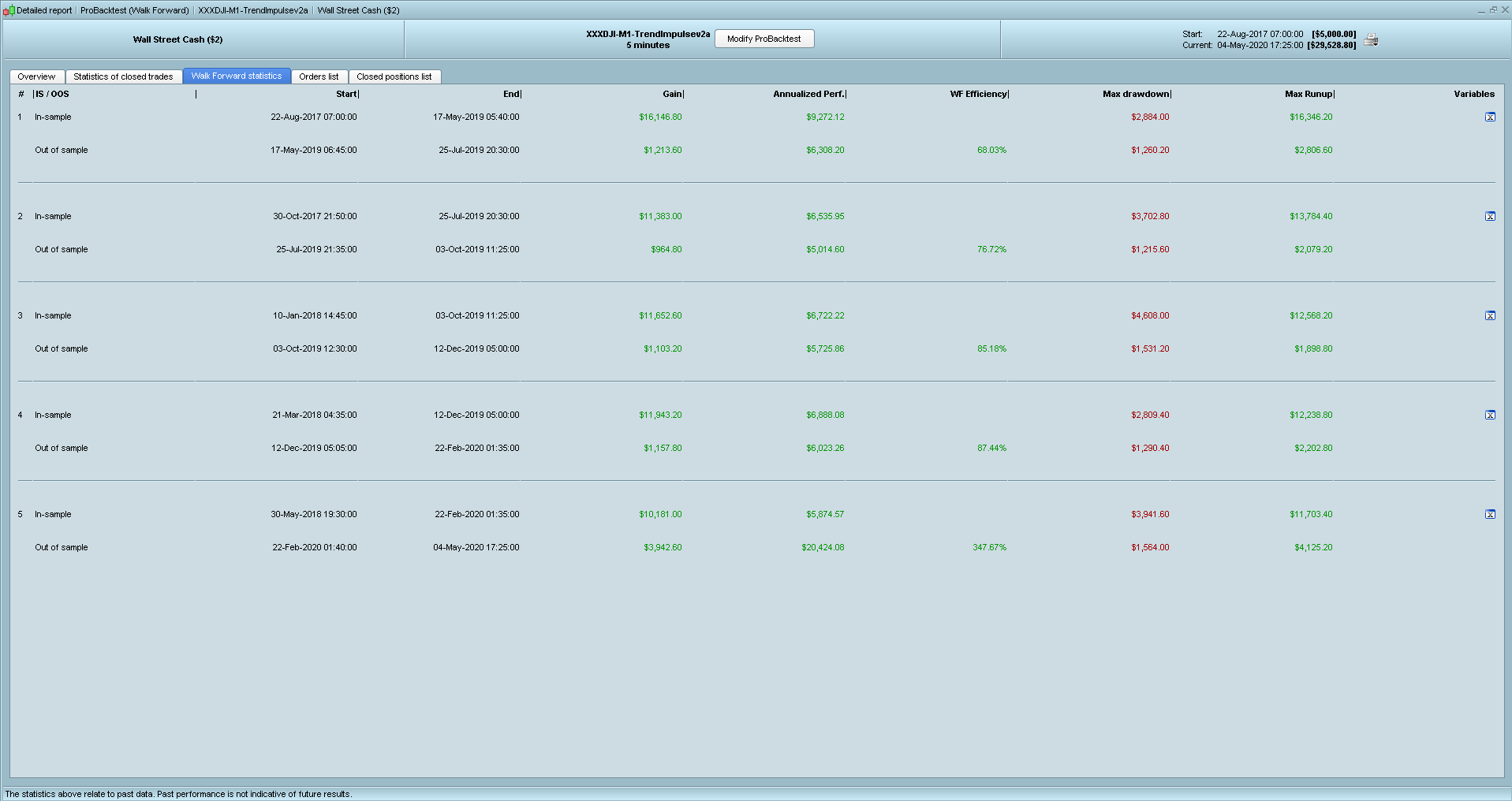

I’m going to look at your new one. Boll are interesting indeed. On you result screen below which variable did you use? Even with optimization tool starting date 2019, I can find out the same result. Maybe i’m wrong on something, is there variable to modify in the code text directly?

Many thanks for the work.