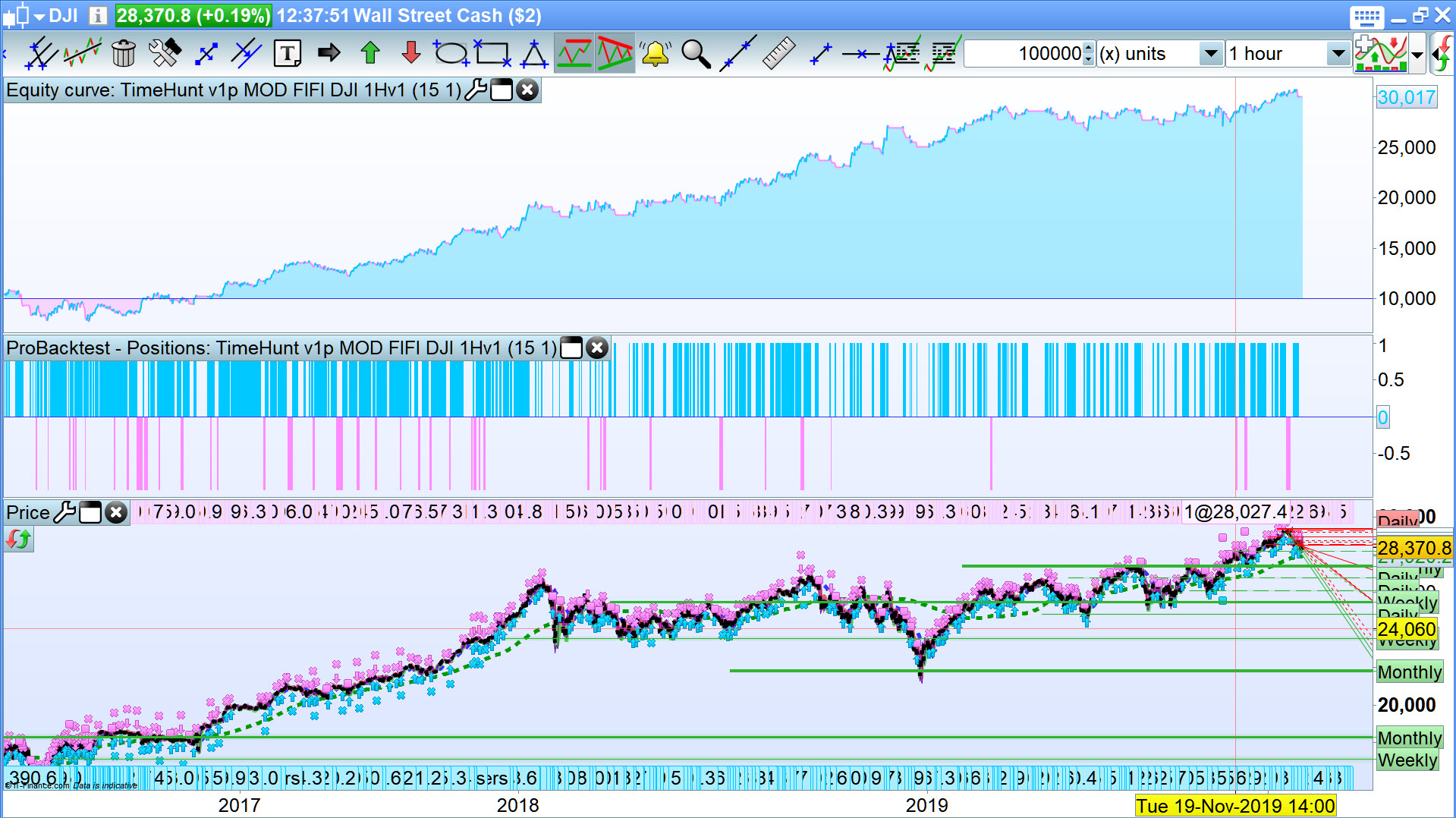

TimeHunter v1p MOD FIFI

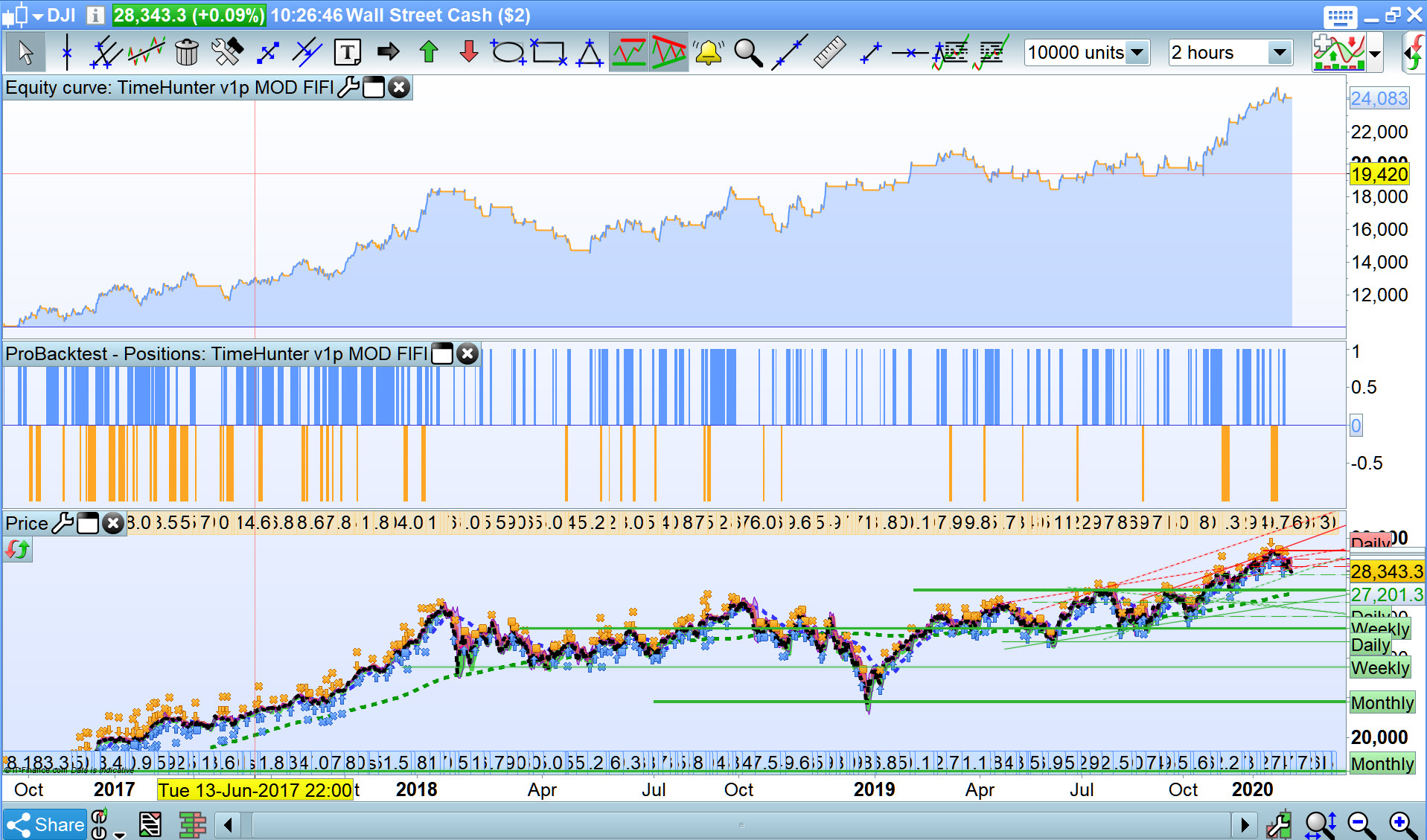

Hey interesting … with no optimisation or even adjustment of Time (yet) for UK Timezone see attached on DJI @ H2 TF.

Well done Paul and Fifi!

Hello,

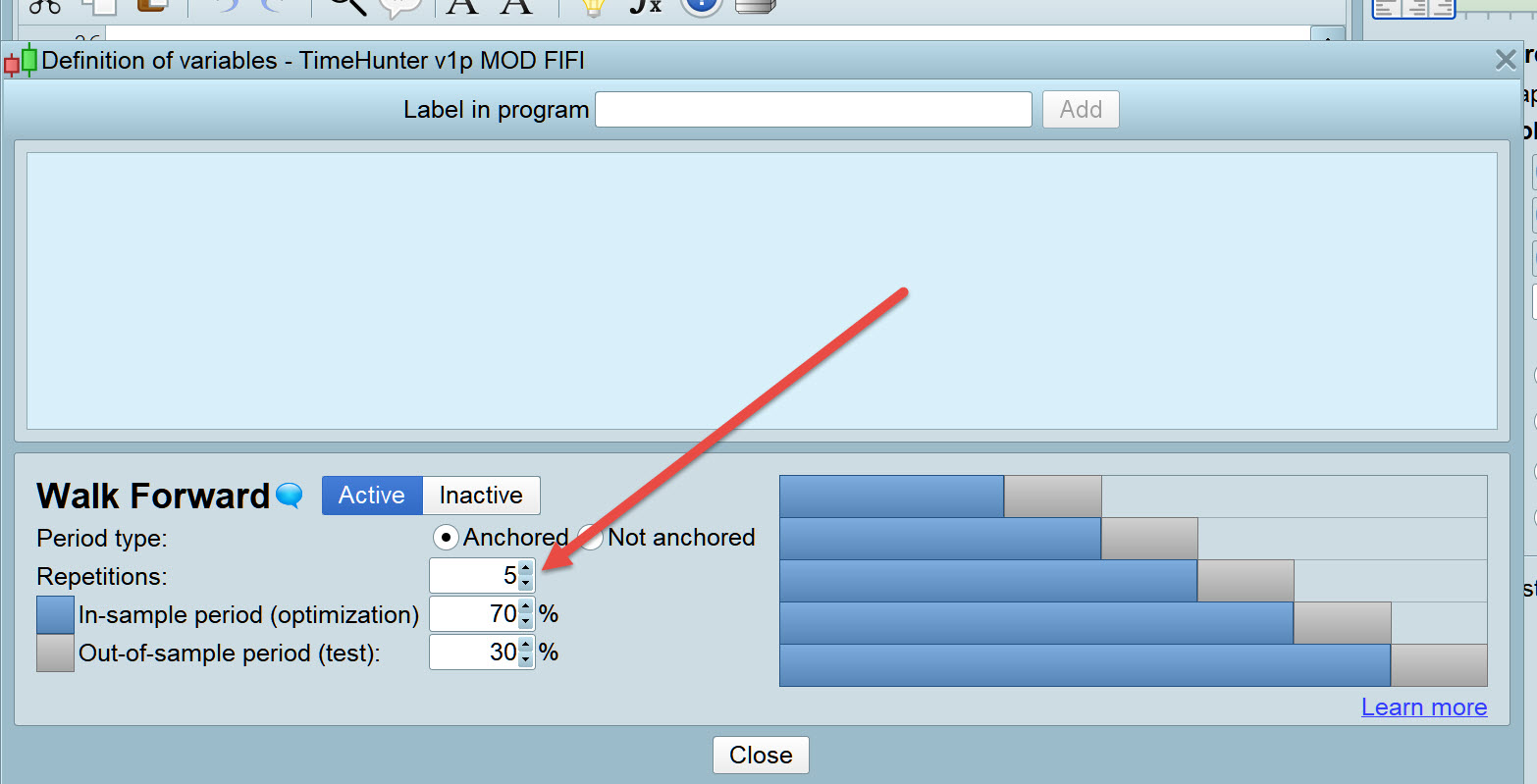

Cannot add backtest “TIMEHUNTER V1P MODFIFI” PRT wants me to edit the variables.

But the variables are already in the code I don’t understand where is the problem?

wants me to edit the variables.

Change the 7 to 5 at the red arrowhead

see attached on DJI @ H2 TF.

Even better on DJI H1 with EntryHour = 15 at Line 42.

Hour 15 being 15:00 to 16:00 UK time is logical as the DJI opens at 14:30 so after half an hour to settle down?

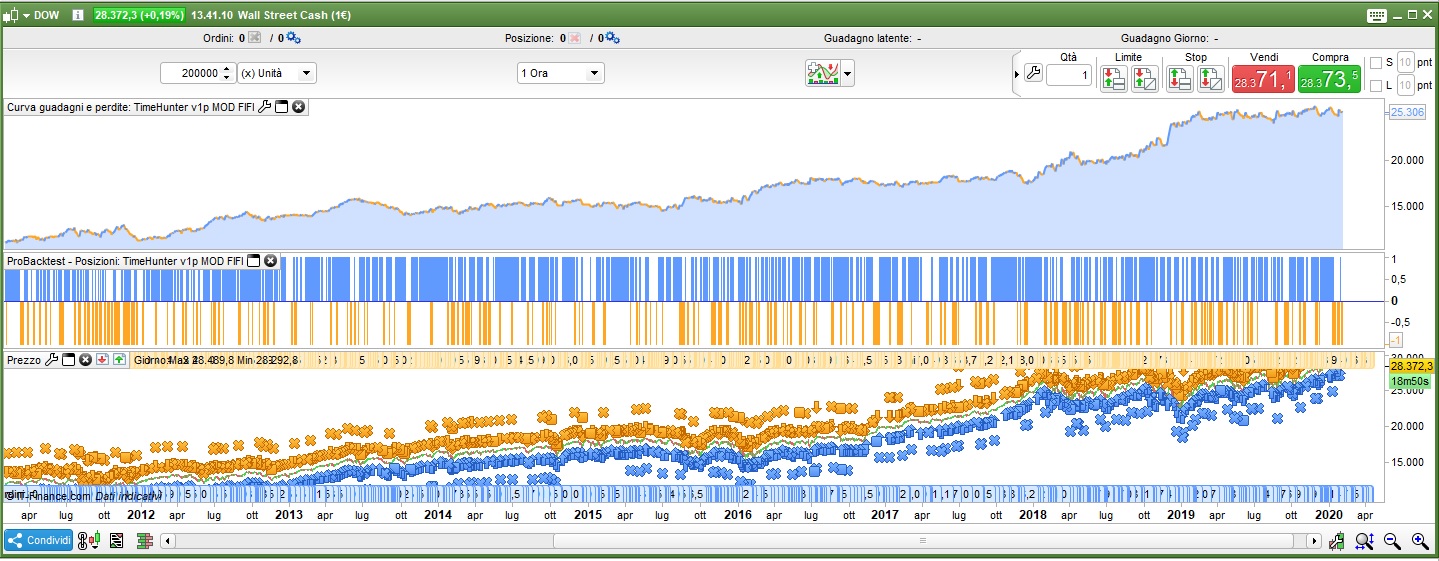

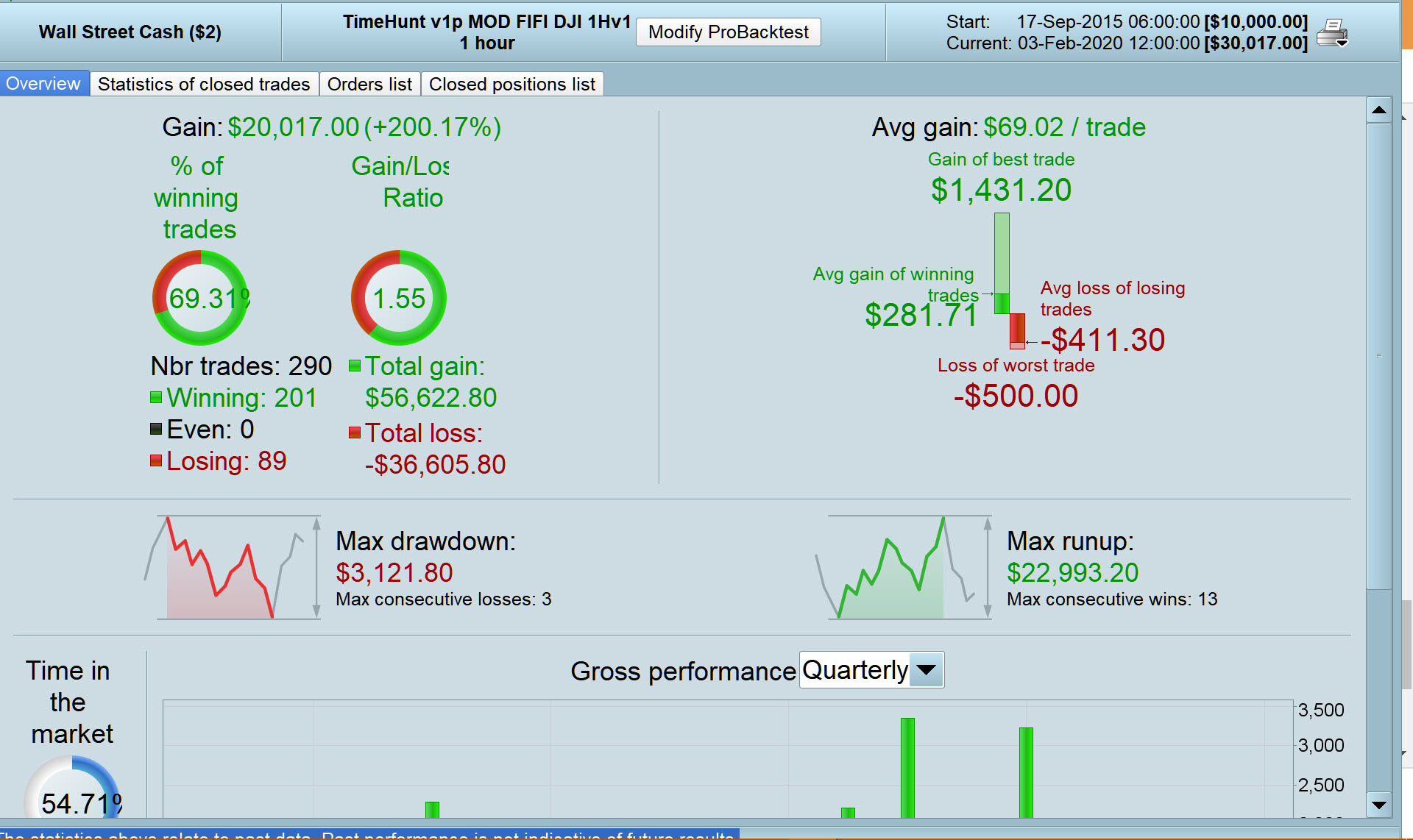

0.2 size

You are showing Size = 1 on your results?

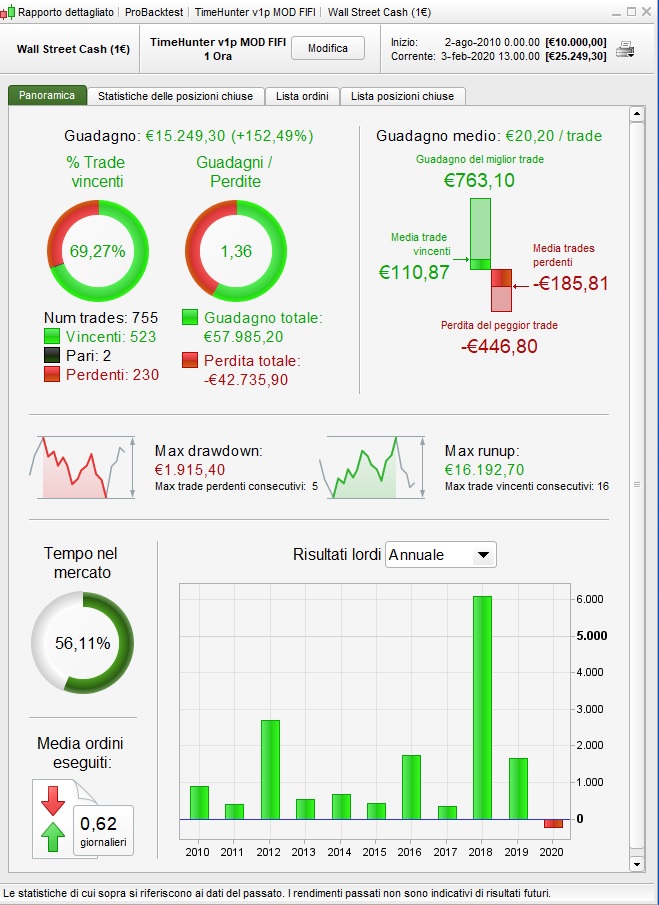

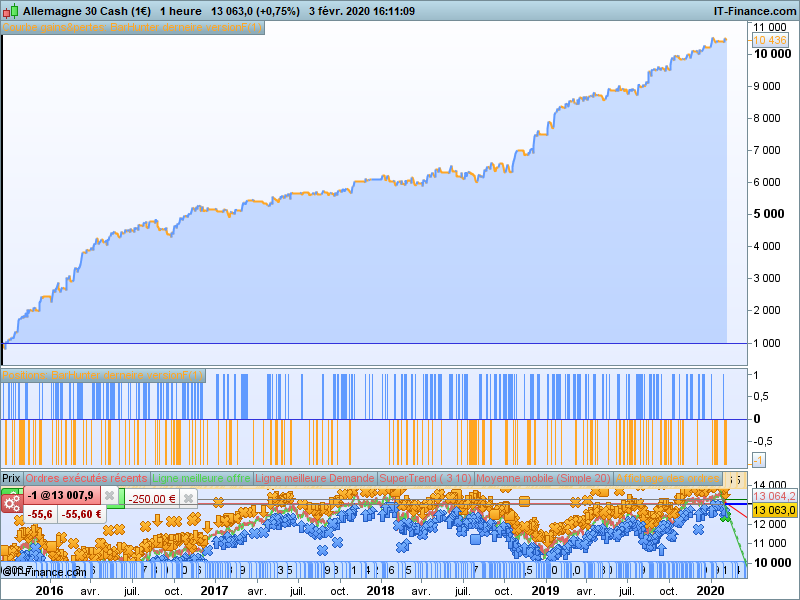

I haven’t yet got decent results on DAX 1 Hour … have you Francesco?

Maybe they were okay. but I was so impressed with the DJI results!? I’ll go back and have a look now I have got the DJI running in Forward Test on Demo.

All hail Paul and Fifi ! 🙂

Yes it’s size 1, I was wrong to write, that’s why I also edited the post

that’s why I also edited the post

We are too quick for each other! 🙂

I have added to my previous with a question for you anyway.

Yes we are 🙂

Anyway, I was not even able to get close to the results of the DAX.

It is probably due to the nature of the asset which is much more versatile for strategies in terms of volatility and trend.

Could someone help in pointing out where I can adjust this?

Change mindist in the code to 15.

But you may still get Rejected as IG ‘Flash widen’ (for several seconds) the spread often.

//-------------------------------------------------------------------------

// Hoofd code : BarHunter v3p

//-------------------------------------------------------------------------

//Germany //24 uur

//01.15-08.00 = 4

//08.00-09.00 = 2

//09.00-17.30 = 1

//17.30-22.00 = 2

//22.00-01.15 = 5

//South Africa 40 //24 uur ZAR50 ZAR10

//07.30-16.30 8

//Alle andere tijden 30

//Wall Street 24 uur $10 / $2

//09.00-15.30 2,4

//15.30-22.00 1,6

//22.15-22.30 9,8

//23.00-00.00 9,8

//Alle andere tijden 3,8

defparam cumulateorders = FALSE

defparam preloadbars = 1000

once enablets = 1 // trailing stop

once enabletsvir = 1 // trailing stop virtual

once displayts = 0 // trailing stop

once holiday = 1

once closebeforeweekend = 0

once closebeforeweekendinloss =0

once securebeforeweekendprofit=0

once entrytype= 1

//entrytype=1 first version with error minimum distance stop

//entrytype=2 entry modified with stop

//entrytype=3 entry modified with market

//entrytype=4 stop distance defnined first entry as entrytype 1

tds= 4// trend detection system off when optimising barnumbers

// separate long/short or go both

once longtrading =1

once shorttrading=1

// select which intradaybar should be analysed (depends on timeframe settings)

once barnumberlong = 3 //long (timezone dependent)

once barnumbershort= 3 //short (timezone dependent)

// select the number of points above/below the breakvaluelong/short

breakpoint=5

//=========

once limitSLbroker=0

if time >210000 and time<070000 and CurrentDayOfWeek>=0 then

limitSLbroker=12

elsif time>070000 and time<210000 and CurrentDayOfWeek>=0 then

limitSLbroker =10

elsif time>210000 and CurrentDayOfWeek>5 then

limitSLbroker=271

endif

//fixed value 10 for dax (the minimum distance the stop can be place to the current close)

if breakpoint <= limitSLbroker then

if (15-breakpoint)>=0 and (15-breakpoint)<=15 then

once minstopdistance=(15-breakpoint)

else

once minstopdistance = 15

endif

else

once minstopdistance = 0

endif

// main criteria

if intradaybarindex=0 then

tradecounter=0

breakvaluelong=99999

breakvalueshort=0

tradeday=1

endif

// holiday

if holiday then

if (Month = 5 AND Day = 1) OR (Month = 12 AND Day >=15) then

tradeday=0

else

tradeday=1

endif

endif

tradecount = tradecounter < 1 //perhaps 2 if using seperate bars for long & short

//

if entrytype>=1 and entrytype<4 then

if longtrading or (longtrading and shorttrading) then

if intradaybarindex=barnumberlong then

breakvaluelong=high

endif

endif

if shorttrading or (longtrading and shorttrading) then

if intradaybarindex=barnumbershort then

breakvalueshort=low

endif

endif

elsif entrytype=4 then

if longtrading or (longtrading and shorttrading) then

if intradaybarindex=barnumberlong then

breakvaluelong=high

if high-close<minstopdistance then

breakvaluelong=close+minstopdistance

else

breakvaluelong=breakvaluelong

endif

endif

endif

if shorttrading or (longtrading and shorttrading) then

if intradaybarindex=barnumbershort then

breakvalueshort=low

if close-low<minstopdistance then

breakvalueshort=close-minstopdistance

else

breakvalueshort=breakvalueshort

endif

endif

endif

endif

// trend detection

if tds=0 then

trendup=1

trenddown=1

else

if tds=1 then

trendup=(Average[10](close)>Average[10](close)[1])

trenddown=(Average[10](close)<Average[10](close)[1])

else

if tds=2 then

bbup=BollingerUp[20](close)

bbdn=BollingerDown[20](close)

bbav=(bbup+bbdn)/2

trendup=bbav>bbav[1]

trenddown=bbav<bbav[1]

else

if tds=3 then

Period= 3

inner = 2*weightedaverage[round( Period/2)](typicalprice)-weightedaverage[Period](typicalprice)

HULL = weightedaverage[round(sqrt(Period))](inner)

trendup = HULL > HULL[1]

trenddown = HULL < HULL[1]

else

if tds=4 then

Period= 2

inner = 2*weightedaverage[round( Period/2)](totalprice)-weightedaverage[Period](totalprice)

HULL = weightedaverage[round(sqrt(Period))](inner)

trendup = HULL > HULL[1]

trenddown = HULL < HULL[1]

endif

endif

endif

endif

endif

// POINT PIVOT HEBDOMADAIRE

IF dayofweek < dayofweek[1] THEN

weeklyhigh = prevweekhigh

weeklylow = prevweeklow

weeklyclose = prevweekclose

prevweekhigh = high

prevweeklow = low

weeklyPivot = (weeklyHigh + weeklyLow + weeklyclose) / 3

ENDIF

prevweekhigh = max(prevweekhigh, high)

prevweeklow = min(prevweeklow, low)

prevweekclose = close

// POINT PIVOT JOURNALIER

IF dayofweek = 1 THEN

dayhigh = DHigh(2)

daylow = DLow(2)

dayclose = DClose(2)

ENDIF

IF dayofweek >=2 and dayofweek < 6 THEN

dayhigh = DHigh(1)

daylow = DLow(1)

dayclose = DClose(1)

ENDIF

Pivot = (dayhigh + daylow + dayclose) / 3

S3 = daylow - 2 * (dayhigh- Pivot)

R3 = dayhigh + 2* (Pivot - daylow)

ecart=4

ecartWP=5

EC= HIGH-low/pointsize

//SP=call"filtre_barhunter"

// entry criteria

if entrytype=1 and tradeday=1 then

// entry criteria

if hour<=21 then

if longtrading then

if intradaybarindex >= barnumberlong then

if trendup and tradecount and (close>pivot or (close <pivot and (pivot-close)/pointsize >ecart)) and (close>weeklypivot or (close <weeklypivot and (weeklypivot-close)/pointsize >ecartWP))and ec>3.9 then

buy 1 contract at breakvaluelong+breakpoint stop

ppf=0

tradecounter=tradecounter+1

endif

endif

endif

if shorttrading then

if intradaybarindex >= barnumbershort then

if trenddown and tradecount and (close<pivot or (close>pivot and (close-pivot)/pointsize >ecart))and (close<weeklypivot or (close>weeklypivot and (close-weeklypivot)/pointsize >ecartWP)) and ec>3.1 then

sellshort 1 contract at breakvalueshort-breakpoint stop

ppf=0

tradecounter=tradecounter+1

endif

endif

endif

endif

elsif entrytype=2 then

if hour<=23 then

if longtrading then

if intradaybarindex >= barnumberlong then

if trendup and tradecount then

if ((breakvaluelong+breakpoint)-close)>=minstopdistance then

buy 1 contract at breakvaluelong+breakpoint stop

tradecounter=tradecounter+1

else

buy 1 contract at close+(minstopdistance+breakpoint) stop

tradecounter=tradecounter+1

endif

endif

endif

endif

if shorttrading then

if intradaybarindex >= barnumbershort then

if trenddown and tradecount then

if (close-(breakvalueshort-breakpoint))>=minstopdistance then

sellshort 1 contract at breakvalueshort-breakpoint stop

tradecounter=tradecounter+1

else

sellshort 1 contract at close-(minstopdistance-breakpoint) stop

tradecounter=tradecounter+1

endif

endif

endif

endif

endif

elsif entrytype=3 then

if hour<=23 then

if longtrading then

if intradaybarindex >= barnumberlong then

if trendup and tradecount then

if high crosses over (breakvaluelong+breakpoint) then

buy 1 contract at market

endif

endif

endif

endif

if shorttrading then

if intradaybarindex >= barnumbershort then

if trenddown and tradecount then

if low crosses under (breakvalueshort-breakpoint) then

sellshort 1 contract at market

tradecounter=tradecounter+1

endif

endif

endif

endif

endif

elsif entrytype=4 then

if hour<=23 then

if longtrading then

if intradaybarindex >= barnumberlong then

if trendup and tradecount then

buy 1 contract at breakvaluelong+breakpoint stop

tradecounter=tradecounter+1

endif

endif

endif

if shorttrading then

if intradaybarindex >= barnumbershort then

if trenddown and tradecount then

sellshort 1 contract at breakvalueshort-breakpoint stop

tradecounter=tradecounter+1

endif

endif

endif

endif

endif

// trailing atr stop

if enablets then

//

once steps=0.05

once minatrdist=3

once atrtrailingperiod = 14 // atr parameter

once minstop = 15 // minimum distance

if barindex=tradeindex then

trailingstoplong = 5 // trailing stop atr distance

trailingstopshort = 5 // trailing stop atr distance

else

if longonmarket then

if newsl>0 then

if trailingstoplong>minatrdist then

if newsl>newsl[1] then

trailingstoplong=trailingstoplong

else

trailingstoplong=trailingstoplong-steps

endif

else

trailingstoplong=minatrdist

endif

endif

endif

if shortonmarket then

if newsl>0 then

if trailingstopshort>minatrdist then

if newsl<newsl[1] then

trailingstopshort=trailingstopshort

else

trailingstopshort=trailingstopshort-steps

endif

else

trailingstopshort=minatrdist

endif

endif

endif

endif

//

atrtrail=averagetruerange[atrtrailingperiod]((close/10)*pipsize)/1000

trailingstartl=round(atrtrail*trailingstoplong)

trailingstarts=round(atrtrail*trailingstopshort)

tgl=trailingstartl

tgs=trailingstarts

//

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

maxprice=0

minprice=close

newsl=0

endif

//

if longonmarket then

maxprice=max(maxprice,close)

if maxprice-tradeprice(1)>=tgl*pointsize then

if maxprice-tradeprice(1)>=minstop then

newsl=maxprice-tgl*pointsize

else

newsl=maxprice-minstop*pointsize

endif

endif

endif

//

if shortonmarket then

minprice=min(minprice,close)

if tradeprice(1)-minprice>=tgs*pointsize then

if tradeprice(1)-minprice>=minstop then

newsl=minprice+tgs*pointsize

else

newsl=minprice+minstop*pointsize

endif

endif

endif

//

if longonmarket then

if newsl>0 then

sell at newsl stop

endif

endif

if shortonmarket then

if newsl>0 then

exitshort at newsl stop

endif

endif

if displayts then

//graphonprice newsl coloured(0,0,255,255) as "trailingstop atr"

endif

endif

// ================trailing atr stop VIRTUAL==================

if enabletsvir then

//

once stepsvir=0

once minatrdistvir=0

once atrtrailingperiodvir = 2 // atr parameter

once minstopvir = 10 // minimum distance

if barindex=tradeindex then

trailingstoplongvir = 5 // trailing stop atr distance

trailingstopshortvir = 5 // trailing stop atr distance

else

if longonmarket then

if newslvir>0 then

if trailingstoplongvir>minatrdistvir then

if newslvir>newslvir[1] then

trailingstoplongvir=trailingstoplongvir

else

trailingstoplongvir=trailingstoplongvir-stepsvir

endif

else

trailingstoplongvir=minatrdistvir

endif

endif

endif

if shortonmarket then

if newslvir>0 then

if trailingstopshortvir>minatrdistvir then

if newslvir<newslvir[1] then

trailingstopshortvir=trailingstopshortvir

else

trailingstopshortvir=trailingstopshortvir-stepsvir

endif

else

trailingstopshortvir=minatrdistvir

endif

endif

endif

endif

//

atrtrailvir=averagetruerange[atrtrailingperiodvir]((close/10)*pipsize)/1000

trailingstartlvir=round(atrtrailvir*trailingstoplongvir)

trailingstartsvir=round(atrtrailvir*trailingstopshortvir)

tglvir=trailingstartlvir

tgsvir=trailingstartsvir

//

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

maxpricevir=0

minpricevir=close

newslvir=0

endif

//

if longonmarket then

maxpricevir=max(maxpricevir,close)

if maxpricevir-tradeprice(1)>=tglvir*pointsize then

if maxpricevir-tradeprice(1)>=minstopvir then

newslvir=maxpricevir-tglvir*pointsize

else

newslvir=maxpricevir-minstopvir*pointsize

endif

endif

endif

//

if shortonmarket then

minpricevir=min(minpricevir,close)

if tradeprice(1)-minpricevir>=tgsvir*pointsize then

if tradeprice(1)-minpricevir>=minstopvir then

newslvir=minpricevir+tgsvir*pointsize

else

newslvir=minpricevir+minstopvir*pointsize

endif

endif

endif

//

if longonmarket and close <newslvir and newslvir>0 then

sell at market

endif

if shortonmarket and close>newslvir and newslvir>0 then

exitshort at market

endif

if displayts then

//graphonprice newsl coloured(0,0,255,255) as "trailingstop atr"

endif

endif

//======================AJOUTER PAR FIFI

PP=positionperf(0)*100

if pp>ppf then

ppf=pp

endif

filtre=call"Forme_bougie"

spread=abs(OPEN-CLOSE)

coeff=spread/highest[200](spread)*100

//=================

// coefficient de la bougie

if longonmarket and barindex-tradeindex>1 AND ppf>0.5 and pp<ppF and coeff<4 and close<positionprice then

sell at market

endif

if longonmarket AND coeff[1]<3 and coeff>80 and close>positionprice then

sell at market

endif

//===============SHORT

if shortonmarket and barindex-tradeindex<3 and pp<ppF and coeff>55 and close>positionprice then

exitshort at market

endif

if shortonmarket and barindex-tradeindex>6 AND ppf>0.1 and pp<ppF and coeff<3 and close>positionprice then

exitshort at market

endif

if shortonmarket AND coeff[1]<6 and coeff>70 and close<positionprice then

exitshort at market

endif

//===================FORME DE BOUGIE

if filtre[1]=-1 and barindex-tradeindex<4 and pp<ppF and longonmarket and close>positionprice then

sell at market

endif

if filtre[1]=-1 and pp>0.7 and pp<ppF and longonmarket and close>positionprice then

sell at market

endif

if filtre=1 and pp>2.5 and pp<PPF and shortonmarket and close<positionprice then

exitshort at market

endif

if filtre[1]=1 and barindex-tradeindex<7 and pp<PPF and shortonmarket and close<positionprice then

exitshort at market

endif

//=====================CROSS POINT DE PIVOT

If longonmarket and close[1] < R3 and high[1]>R3 and open>close and pp>ppF-pp and close>positionprice then

sell at market

endif

if shortonmarket and close[1]>S3 and low[1]<S3 and open<close and pp>ppF-pp and close<positionprice then

exitshort at market

endif

//=======================================

if longonmarket and pp>ppF-pp and close>positionprice and open>close and( (high-open>18)or(open=high and open-close>9)or(open[1]<close[1] and close[1]=high[1] and open[1]>close)) then

sell at market

endif

if shortonmarket and pp>ppF-pp and close<positionprice and open<close and open[1]>close[1] and close[1]=LOW[1] and open[1]<close then

exitshort at market

endif

// test de nombre de bar negative ajouter fifi743

if longonmarket and barindex-tradeindex>138 and close<positionprice then

sell at market

endif

if shortonmarket and barindex-tradeindex>11 and close>positionprice then

exitshort at market

endif

//===============AJOUTER FERMETURE DES POSITIONS RSI ET barindex-tradeindex =====

Myrsi=RSI[15](close)

//34

if Myrsi<47 and barindex-tradeindex>3 and longonmarket and close>positionprice then

sell at market

endif

if Myrsi>69 and barindex-tradeindex>1 and shortonmarket and close<positionprice then

exitshort at market

endif

//=========================NB bar

for i=0 to 3

if longonmarket and barindex-tradeindex<4 AND COEFF[i]>60 AND COEFF<10 and coeff[i]>coeff and ppf=0 then

sell at market

break

endif

if shortonmarket and barindex-tradeindex<5 AND COEFF[i]>60 AND COEFF<10 and coeff[i]>coeff and ppf=0 then

exitshort at market

endif

next

// =================== FORME DE BOUGIE DOJI ====================

if longonmarket and abs(open-close)<1 and high-close>18 and high[1]<high and close>positionprice then

sell at market

endif

if shortonmarket and abs(open-close)<1 and low[1]<low and close<positionprice then

exitshort at market

endif

//====================PAUL

if closebeforeweekend then

if onmarket then

if (dayofweek=5 and hour>=22) then

sell at market

exitshort at market

endif

endif

endif

if securebeforeweekendprofit then

if (dayofweek=5 and hour>=18) then

if longonmarket then

if close>positionprice+15 then

sell at tradeprice(1)+10 stop

//else

//if hour>=22 then

//sell at market

//endif

endif

endif

if shortonmarket then

if close<positionprice-15 then

exitshort at tradeprice(1)-10 stop

else

if hour>=22 then

exitshort at market

endif

endif

endif

endif

endif

if closebeforeweekendinloss then

if (dayofweek=5 and hour>=22) then

if longonmarket then

if close<positionprice then

sell at market

endif

endif

if shortonmarket then

if close>positionprice then

exitshort at market

endif

endif

endif

endif

//==============================

if CurrentDayOfWeek=1 and time>060000 and time<180000 then

SL=160

elsif CurrentDayOfWeek=2 and time>060000 and time<180000 then

SL=160

elsif CurrentDayOfWeek=3 and time>060000 and time<180000 then

SL=170

elsif CurrentDayOfWeek=4 and time>060000 and time<180000 then

SL=130

elsif CurrentDayOfWeek=5 and time>060000 and time<180000 then

SL=150

elsif time>180000 and time<060000 then

sl=270

endif

SET STOP PLOSS sl

//set stop %loss 2

//set target %profit 3

Florian Legeard – I removed your ‘bad’ code and replaced it with the second code that you posted. I also removed the French part of your post.

Paul

PaulParticipant

Master

here’s an early strategy I based on barhunter. It had to be very simple and it isn’t perfect by any stretch but it shows that there’s some predictable behaviour at certain times in the market. Uses market orders, based on 15 minutes, dax.

PaulParticipant

Master

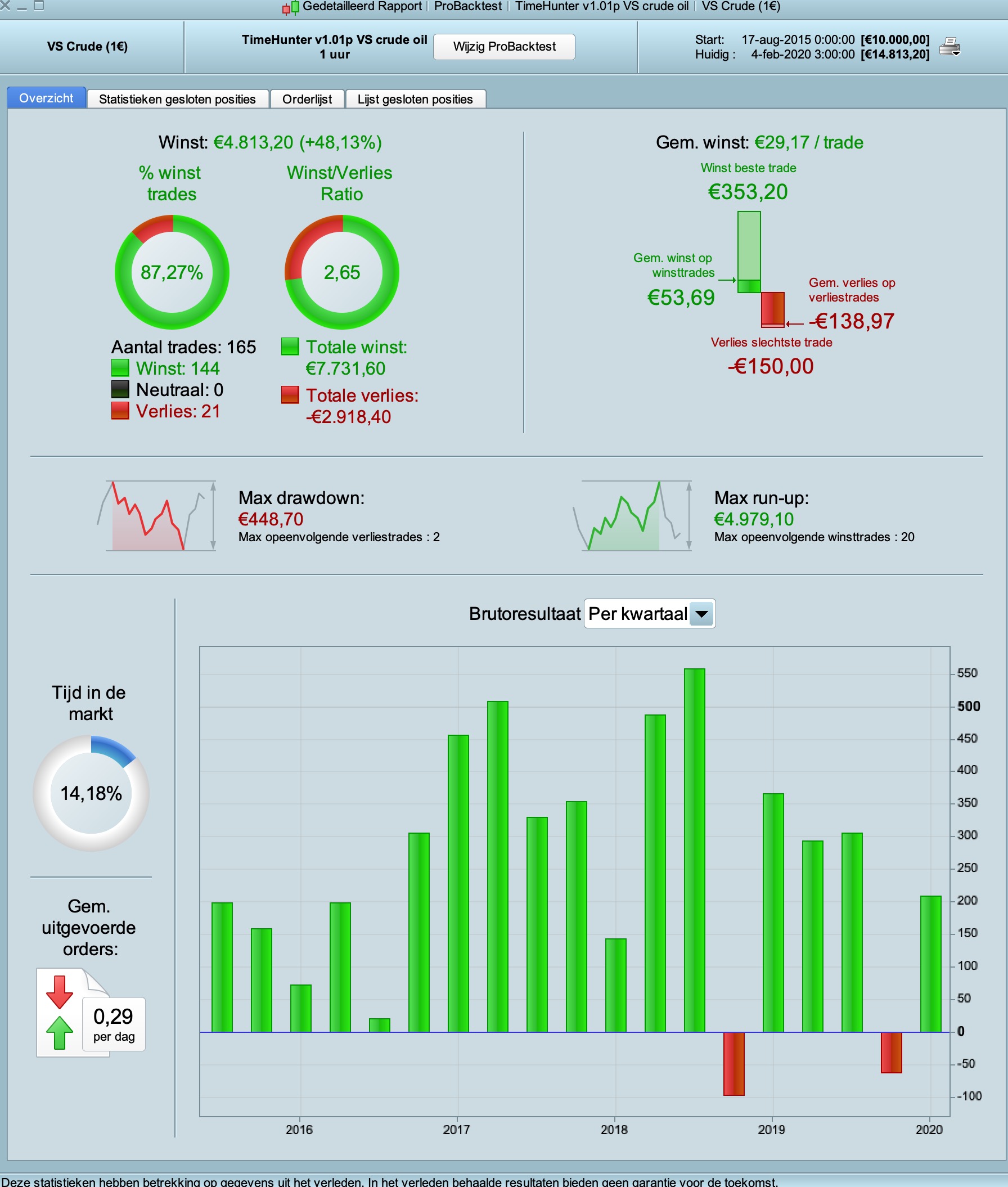

and here’s TimeHunter v1.01p VS crude oil

take into account, when going back in time and a index is half the value, a stoploss using points or percentage matters.

Same goes using points for a break or percentage. Using percentage can lower the equity curve.

Change mindist in the code to 15. But you may still get Rejected as IG ‘Flash widen’ (for several seconds) the spread often.

Have you been rejected at mindist = 15 Florian?

Try below (for mindist = 30) just so you can understand what goes on and hopefully you may get a trade triggered.

Below relates to Lines 51 to 71 in the code you posted.

Only try on Demo (Not Real Live).

breakpoint=5

//=========

once limitSLbroker=0

if time >210000 and time<070000 and CurrentDayOfWeek>=0 then

limitSLbroker=30

elsif time>070000 and time<210000 and CurrentDayOfWeek>=0 then

limitSLbroker =10

elsif time>210000 and CurrentDayOfWeek>5 then

limitSLbroker=271

endif

//fixed value 10 for dax (the minimum distance the stop can be place to the current close)

if breakpoint <= limitSLbroker then

if (30-breakpoint)>=0 and (30-breakpoint)<=25 then

once minstopdistance=(30-breakpoint)

else

once minstopdistance = 30

endif

else

once minstopdistance = 0

endif