We’ve had 0 / zero real trades up to now so it’s still early days.

There’s been problems related to the variable minimum distance stop settings used by IG!

Hello, Why not use a virtual stop

Go on … tell us what a virtual stop is? 🙂

Paul

PaulParticipant

Master

@fifi743 you got me curious too!

@GraHal maybe we should do more testing, meaning more different barnumbers for entry1 to 4 so we can pick a entry-type which is reliable regardless of the bar-number and results.

so we can pick a entry-type which is reliable regardless of the bar-number and results.

Yeah but as backtest does not perform same as Live (which is a nonsense in itself!?) then how can we prove what is reliable other than Live Forward Test … which would take for ever as so few trades?

I guess if we don’t use stop entry then backtest results should be closer to Live results and so more reliable?

If I recall correctly, my 5 min version is an at market entry … hopefully there should be would be no Issues re minimum distance

// ================trailing atr stop VIRTUAL==================

if enabletsvir then

//

once stepsvir=0

once minatrdistvir=0

once atrtrailingperiodvir = 2 // atr parameter

once minstopvir = 10 // minimum distance

if barindex=tradeindex then

trailingstoplongvir = 5 // trailing stop atr distance

trailingstopshortvir = 5 // trailing stop atr distance

else

if longonmarket then

if newslvir>0 then

if trailingstoplongvir>minatrdistvir then

if newslvir>newslvir[1] then

trailingstoplongvir=trailingstoplongvir

else

trailingstoplongvir=trailingstoplongvir-stepsvir

endif

else

trailingstoplongvir=minatrdistvir

endif

endif

endif

if shortonmarket then

if newslvir>0 then

if trailingstopshortvir>minatrdistvir then

if newslvir<newslvir[1] then

trailingstopshortvir=trailingstopshortvir

else

trailingstopshortvir=trailingstopshortvir-stepsvir

endif

else

trailingstopshortvir=minatrdistvir

endif

endif

endif

endif

//

atrtrailvir=averagetruerange[atrtrailingperiodvir]((close/10)*pipsize)/1000

trailingstartlvir=round(atrtrailvir*trailingstoplongvir)

trailingstartsvir=round(atrtrailvir*trailingstopshortvir)

tglvir=trailingstartlvir

tgsvir=trailingstartsvir

//

if not onmarket or ((longonmarket and shortonmarket[1]) or (longonmarket[1] and shortonmarket)) then

maxpricevir=0

minpricevir=close

newslvir=0

endif

//

if longonmarket then

maxpricevir=max(maxpricevir,close)

if maxpricevir-tradeprice(1)>=tglvir*pointsize then

if maxpricevir-tradeprice(1)>=minstopvir then

newslvir=maxpricevir-tglvir*pointsize

else

newslvir=maxpricevir-minstopvir*pointsize

endif

endif

endif

//

if shortonmarket then

minpricevir=min(minpricevir,close)

if tradeprice(1)-minpricevir>=tgsvir*pointsize then

if tradeprice(1)-minpricevir>=minstopvir then

newslvir=minpricevir+tgsvir*pointsize

else

newslvir=minpricevir+minstopvir*pointsize

endif

endif

endif

//

if longonmarket and close <newslvir and newslvir>0 then

sell at market

endif

if shortonmarket and close>newslvir and newslvir>0 then

exitshort at market

endif

I have two trailing stops Whoever moves the stop And the other if it is closed is above or below the newslvir

Above added as Log 196 here …

Snippet Link Library

PaulParticipant

Master

Thanks fifi! The virtual stop is implemented as I thought. The original ts still running with atrtrailingperiod=14 and the virtual with value 2. Also the test de nombre de bar negative ajouter makes a difference. Total results is a bit the same, but the equitycurve has a nicer shape!

I’am working on something to drop the stop for entry. But it’s not there yet.

PaulParticipant

Master

@fifi, with importing I noticed tick by tick wasn’t enabled, so I did the test again and with target profit disabled.

your average loss dropped quite a bit. Will test to to see what difference it brings to the market version.

Unfortunately I don’t understand the benefit of the virtual trailing stop and see very little difference. Maybe it shows more with live trading.

Good-morning Paul,

To avoid errors of stops too close.

The value remains in the variable

There may be more difference in lower time frame.

Hello,

Entry type = 1 I reduced the hour to 21

I have placed two different stops depending on the trading hours.

To be checked so as not to have an error

Today I’m at 271 points for Stop

PaulParticipant

Master

Hi Fifi43

Thanks I will look into this. I found irregularities when using barindex numbers. Because when there is no data, everything shifts a bar! Doesn’t happen too much on 1 hour timeframe, but it could be more often on lower timeframes and I want it to be universal.

So I’m testing a way too quickly and efficiently optimise time using hour & any minutes. Also looking in your nicely coded FILTRE_Prise_Position if it could be of use for profittaking.

@Grahal

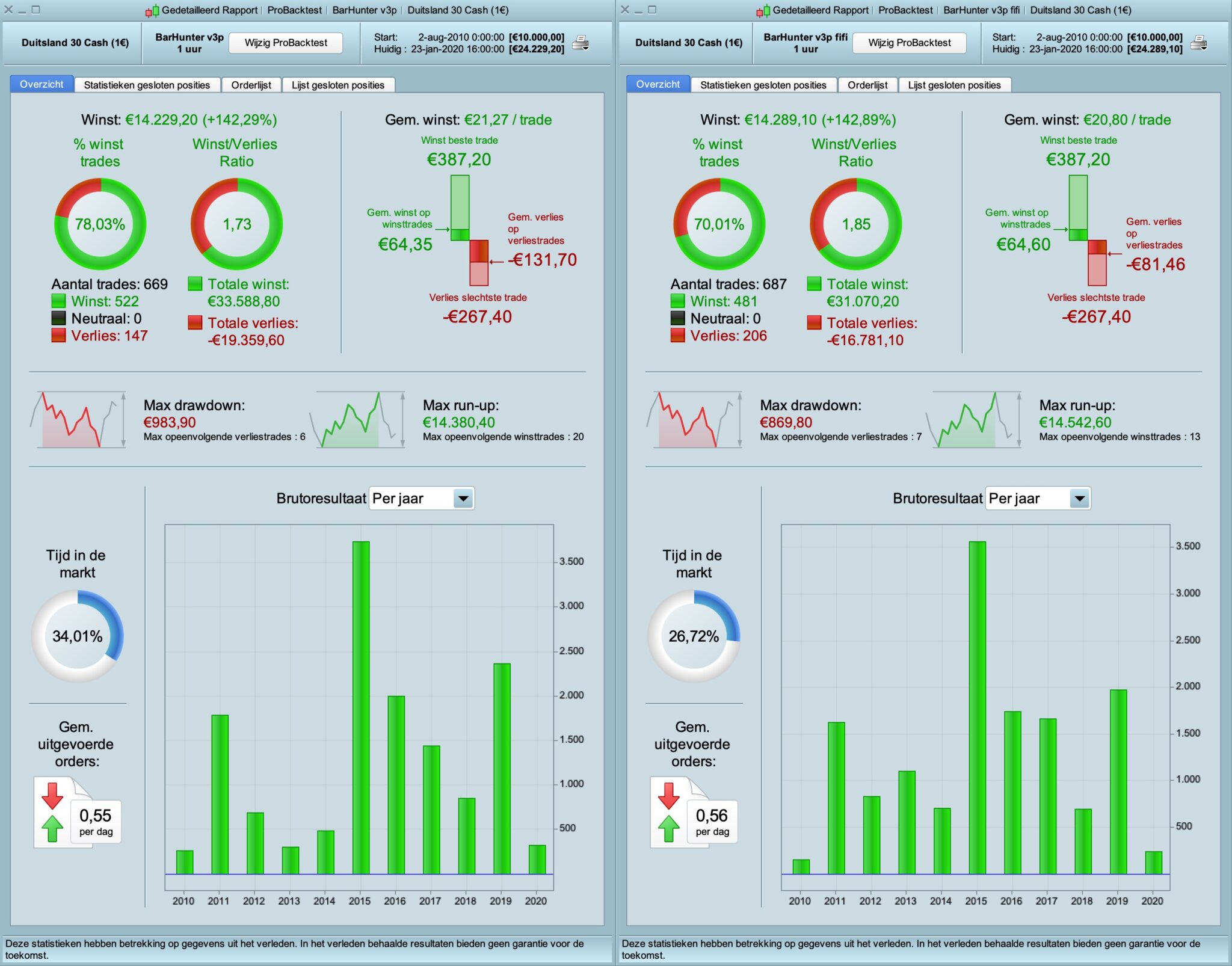

Did you figure out the exact reason of the difference ? As I am also getting a different equity curve and number of trades. I believe it is the timezone. I only 100 K bars to test, so I can’t compare exactly to the latest from fifi. But if I change the timezone to be inline with the others, I get exactly the same drawdown (869.80) and similar profit profile per month.

Optimizing barnumber might not give you the same result.

@Grahal : Disregard my previous comment. It will give you exactly the same result.