JASS

JASSParticipant

Junior

That is exactly my experience! So either there is a problem in the code or there is a problem between IG and PRT. And then we are back to the “needle-in-a-haystack”. Can you spot anything else in the code that might cause this?

I might be speaking too soon, but I changed so SP = 2 and it has not been Rejected (yet!).

SP = 1 // Stochastic Period

I might be speaking too soon

Still no Rejection after 16 mins so SP = 1 looks like the problem?

I’ll keep monitoring and report back.

Rejected again but it took nearly 1 hour this time!

Well weird??

I’ll like to help but I do not see anything in the code that would suggest this behavior. But please test these, in the same order:

- restrain the whole code to a time condition: if time>=010000 and time<073000 then …. YOUR CODE …. endif

- use a period of more than just 1 period for the calculation of the stochastic (variable SP)

- Did you try on a 5-minutes timeframe? (I know it is not the desired TF, but ..)

SP = 2 on 1 min TF stopped again but it took about 3 hours this time (1 hour last time).

SP = 1 on 5 min TF got stopped, but it took about 3 hours.

SP =10 on 1 min TF is still running after 3 hours.

JASSParticipant

Junior

Thanks GraHal for your big effort here, I really appreciate it!

I have replaced the stochastic with one line of code, since I only need an intrabar view on the close vs. high and low. The code now looks like this:

K = ((close-low)/(high-low))*100

Very close to stochastic, but now I don’t have to worry about the highest/lowest in relation to one bar only.

The strategy still stops though.

Then I have followed suggestion from Nicolas and “wrapped” all code in an “if time>=010000 and time<073000 then” statement, though after the defparam lines, since they need to come before anything else in any code as far as I remember. I suppose I will have to wait and see till tomorrow morning if this has an influence.

I will revert.

I’ve incorporated the changes you mention above and set that version going so we can compare!

Sleep Well! 🙂

All versions stopped except SP = 10.

In backtest SP = 10 makes zero / 0 Profit (due to zero Trades over 100k bars).

Why is the SP = 10 System the only System (out of our trials) that does not get stopped??

No entries for any stoppages under Rejected / Cancelled in the Orders List.

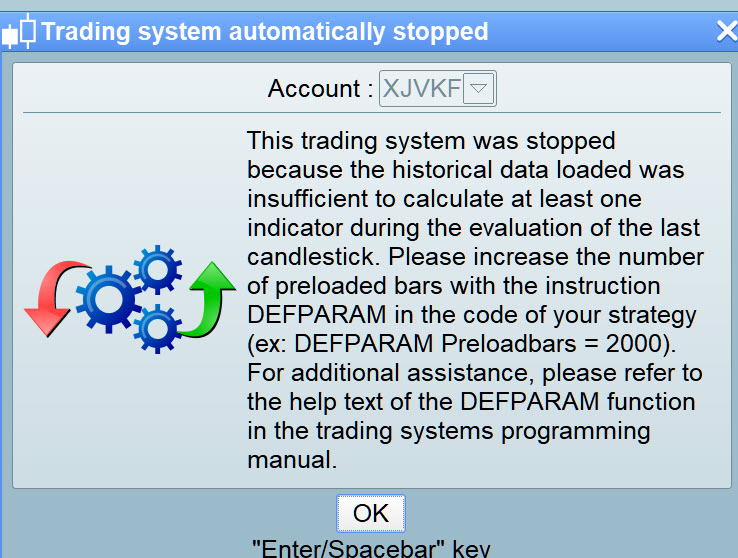

Stopped error message is attached. All my versions stopped have DEFPARAM PreLoadbars = 10000.

Point to Note:

Stoppages occur outside of trading hours (see numerous evidence in comments above) so it is not when a System tries to execute a trade that the System is stopped.

JASS and I have tried numerous versions, so for reference … below is the only code version that has NOT been stopped.

The version below has been running since 14:37 yesterday 6 Jan 20.

//-------------------------------------------------------------------------

// Main code : A107 Pullback Rev JPN 1M v04

//-------------------------------------------------------------------------

//https://www.prorealcode.com/topic/trading-system-automatically-stopped/#post-115990

//**********************************************************************************

// Title: A107 Pullback Rev JPN 1M v04

// Chart: JAPAN225 / NIKKEI 1M

// Note: Exploiting one bar pullbacks in steep trending market

//**********************************************************************************

DEFPARAM CumulateOrders = True

DEFPARAM PreLoadBars = 10000

DEFPARAM FLATBEFORE = 000000

DEFPARAM FLATAFTER = 063000

//**********************************************************************************

// Variables

//**********************************************************************************

PositionSize = 1

tp = 138 // Target profit

sl = 28 // Stop loss

EMAp1 = 34

EMAp2 = 29

EMAp4 = 41

SMAp2 = 40

SP = 10 // Stochastic Period

v10 = 10 // Stochastic lower line

v90 = 94 // Stochastic upper line

emadiff = 1.95 // EMA difference to ensure steep trend

MOMp = 51 // Momentum period

MOMLv = 40 // Momentum long value

MOMSv = -100 // Momentum short value

PBLp = 25 // Power bar long period

PBSp = 25 // Power bar short period

PBLv = 12 // Power bar long value

PBSv = 33 // Power bar short value

LBL = 20 // Large bar long

LBS = 15 // Large bar short

COSH = 4 // Count of shares

//**********************************************************************************

// Indicators and Math

//**********************************************************************************

// Stochastic

C = Close

HH = Highest[SP](high)

LL = Lowest[SP](low)

K = ((C-LL)/(HH-LL))*100

// EMA

c01 = exponentialaverage[EMAp1](close)

// Momentum

c03 = momentum[MOMp](close)

// SMA

c04 = average[SMAp2](close)

// Power bar long - no powerbar for the last PBLp number of periods before entry

PBL = close - open

IF highest[PBLp](PBL) < PBLv THEN

c13 = 1

else

c13 = 0

ENDIF

// Power bar short - no powerbar for the last PBSp number of periods before entry

PBS = open - close

IF highest[PBSp](PBS) < PBSv THEN

c33 = 1

else

c33 = 0

ENDIF

c05 = abs(c01[0]-c01[1]) > emadiff

c06 = exponentialaverage[EMAp2](((2*close)+open)/3)

c07 = exponentialaverage[EMAp4](((2*close)+open)/3)

//**********************************************************************************

// Entry/exit conditions

//**********************************************************************************

// Enter long conditions

c10 = c01[1] > c01[2]

c11 = countoflongshares < COSH

c12 = c03 > MOMLv

c14 = K[0] < v10

// Exit long conditions

c20 = c04[0] < c04[1]

c21 = close[0]-open[0] > LBL

c22 = c06[0] < c06[1]

// Enter short conditions

c30 = c01[1] < c01[2]

c31 = countofshortshares < COSH

c32 = c03 < MOMSv

c34 = K[0] > v90

// Exit short conditions

c40 = c04[0] > c04[1]

c41 = open[0]-close[0] > LBS

c42 = c07[0] > c07[1]

//**********************************************************************************

// Enter Long

//**********************************************************************************

if c05 and c10 and c11 and c12 and c13 = 1 and c14 then

buy PositionSize contract at market

endif

//**********************************************************************************

// Exit Long

//**********************************************************************************

if longonmarket and (c20 or c21 or c22) then

sell at market

endif

//**********************************************************************************

// Enter Short

//**********************************************************************************

if c05 and c30 and c31 and c32 and c33 = 1 and c34 then

sellshort PositionSize contract at market

endif

//**********************************************************************************

// Exit Short

//**********************************************************************************

if shortonmarket and (c40 or c41 or c42) then

exitshort at market

endif

//**********************************************************************************

// Stops and Targets

//**********************************************************************************

set stop ploss sl

set target pprofit tp

//GRAPH ((C-LL)/(HH-LL))*100

Ok, so my conclusion goes for the stochastic period, that must be superior to 1. If there is no bar (or “phantom bar”), the 1 period calculation leads to a division by zero at line 50.

You could also try this version of the calculation, it should also work with a 1-period:

K = ((C-LL)/max(pointsize,(HH-LL)))*100

JASS got rid of the stochastic and it was still stopped, but maybe he still ended up with a divide by zero error (if no bar or phantom bar) with his amended code. See his post here …

https://www.prorealcode.com/topic/trading-system-automatically-stopped/page/2/#post-116086

I will try your code Nicolas thank you.

Over 2.5 hours … so far so good using Nicolas code!

The no bar / phantom bar causing a divide by zero error would account for the Rejection / Stop being random … due to a no bar occurrence being random!

JASSParticipant

Junior

just returned home after a long day, will answer tomorrow

I moved the topic into the ProOrder section, it is now more related to automated trading coding than a platform issue.