Good morning and a Happy New Year!

I am trying to create a trading system based on the indicator posted by Nicolas, One More Average MACD, but I fail. I tried to tweak the different parameters but without any results. Any ideas why?

Thanks!!

//-------------------------------------------------------------------------

defparam cumulateorders=false

Defparam preloadbars=10000

amount = 10 //quantity of shares/contracts to open for each new order

//--------------------------------------------------------------------------------//

//Indicators

//Indicator: PRC_OneMoreAverage MACD

//Release date: 23.11.2016

//Web: https://www.prorealcode.com/prorealtime-indicators/one-more-average-macd/

//Coded by: Nicolas @ www.prorealcode.com

//--parameters

//>OMA parameters

Sensibility = 1

Adaptive = 1

//>MACD periods

FLength = 24

SLength = 52

//>signal line

SigLength = 9

Sigma = 4

Offset = 0.85

//--------

Speed = Sensibility

Speed = Max(Speed,-1.5)

price = average[1](customclose)

tconst=Speed

//--Fast moving average

FLength = Max(FLength,1)

//adaptive period

averagePeriod = FLength

if adaptive=1 and averagePeriod > 1 then

minPeriod = averagePeriod/2.0

maxPeriod = minPeriod*5.0

endPeriod = round(maxPeriod)

signal = Abs((price-stored[endPeriod]))

noise = 0.00000000001

for k=1 to endPeriod do

noise=noise+Abs(price-stored[k])

averagePeriod = round(((signal/noise)*(maxPeriod-minPeriod))+minPeriod)

next

endif

alpha = (2.0+tconst)/(1.0+tconst+averagePeriod)

e1 = e1 + alpha*(price-e1)

e2 = e2 + alpha*(e1-e2)

v1 = 1.5 * e1 - 0.5 * e2

e3 = e3 + alpha*(v1 -e3)

e4 = e4 + alpha*(e3-e4)

v2 = 1.5 * e3 - 0.5 * e4

e5 = e5 + alpha*(v2 -e5)

e6 = e6 + alpha*(e5-e6)

Fast = 1.5 * e5 - 0.5 * e6

//------------------------------------

//--Slow moving average

SLength = Max(SLength,1)

//adaptive period

averagePeriod = SLength

if adaptive=1 and averagePeriod > 1 then

minPeriod = averagePeriod/2.0

maxPeriod = minPeriod*5.0

endPeriod = round(maxPeriod)

signal = Abs((price-stored[endPeriod]))

noise = 0.00000000001

for k=1 to endPeriod do

noise=noise+Abs(price-stored[k])

averagePeriod = round(((signal/noise)*(maxPeriod-minPeriod))+minPeriod)

next

endif

alpha = (2.0+tconst)/(1.0+tconst+averagePeriod)

e1 = e1 + alpha*(price-e1)

e2 = e2 + alpha*(e1-e2)

v1 = 1.5 * e1 - 0.5 * e2

e3 = e3 + alpha*(v1 -e3)

e4 = e4 + alpha*(e3-e4)

v2 = 1.5 * e3 - 0.5 * e4

e5 = e5 + alpha*(v2 -e5)

e6 = e6 + alpha*(e5-e6)

Slow = 1.5 * e5 - 0.5 * e6

//------------------------------------

//--Signal moving average

OMAMACD = Slow-Fast

SigLength = Max(SigLength,1)

//---Signal MA

n = (Offset * (SigLength - 1))

t = SigLength/Sigma

SWtdSum = 0

SCumWt = 0

for k = 0 to SigLength - 1 do

SWtd = Exp(-((k-n)*(k-n))/(2*t*t))

SWtdSum = SWtdSum + SWtd * OMAMACD[SigLength - 1 - k]

SCumWt = SCumWt + SWtd

next

SIGMACD = SWtdSum / SCumWt

//------------------------------------

stored=price

//------------------------------------

BullSMA=(SIGMACD<OMAMACD)

BearSMA=(SIGMACD>OMAMACD)

//--------------------------------------------------------------------------------//

//Conditions when to act

if (not longonmarket and BullSMA)then

buy amount shares at market

endif

if (longonmarket and BearSMA and positionperf>0) then

sell at market

endif

Vous utilisez le même nom pour 2 variables différentes.

Il faut un nom différent pour chaque nouvelle variable.

You use the same name for 2 different variables.

Each new variable needs a different name.

Merci pour votre réponse rapide! Cependant, je ne comprends pas ce que vous voulez dire. OMAMACD et SIGMACD sont des variables différentes, ou voulez-vous dire quelques autres? Merci de votre patience!

Thanks for your quick answer! However, I do not understand what you mean. OMAMACD and SIGMACD are different variables, or do you mean some others? Thanks for your patience!

Like for example “averagePeriod” in the “Fast moving average”.

“AveragePeriod” in the “Slow moving average” must be renamed differently as “SaveragePeriod” and so on for all the variables written in black color.

You need to ensure that there are enough bars before starting the calculations. With the standard settings it seems a minimum of 129 bars are required.

//-------------------------------------------------------------------------

defparam cumulateorders=false

Defparam preloadbars=10000

amount = 1 //quantity of shares/contracts to open for each new order

///PRC_OneMoreAverage MACD | indicator

//23.11.2016

//Nicolas @ www.prorealcode.com

//Sharing ProRealTime knowledge

//--parameters

//>OMA parameters

Sensibility = 1

Adaptive = 1

//>MACD periods

FLength = 24

SLength = 52

//>signal line

SigLength = 9

Sigma = 4

Offset = 0.85

//--------

if barindex > 129 then

Speed = Sensibility

Speed = Max(Speed,-1.5)

price = average[1](customclose)

tconst=Speed

//--Fast moving average

FLength = Max(FLength,1)

//adaptive period

averagePeriod = FLength

if adaptive=1 and averagePeriod > 1 then

minPeriod = averagePeriod/2.0

maxPeriod = minPeriod*5.0

endPeriod = round(maxPeriod)

signal = Abs((price-stored[endPeriod]))

noise = 0.00000000001

for k=1 to endPeriod do

noise=noise+Abs(price-stored[k])

averagePeriod = round(((signal/noise)*(maxPeriod-minPeriod))+minPeriod)

next

endif

alpha = (2.0+tconst)/(1.0+tconst+averagePeriod)

e1 = e1 + alpha*(price-e1)

e2 = e2 + alpha*(e1-e2)

v1 = 1.5 * e1 - 0.5 * e2

e3 = e3 + alpha*(v1 -e3)

e4 = e4 + alpha*(e3-e4)

v2 = 1.5 * e3 - 0.5 * e4

e5 = e5 + alpha*(v2 -e5)

e6 = e6 + alpha*(e5-e6)

Fast = 1.5 * e5 - 0.5 * e6

//------------------------------------

//--Slow moving average

SLength = Max(SLength,1)

//adaptive period

averagePeriod = SLength

if adaptive=1 and averagePeriod > 1 then

minPeriod = averagePeriod/2.0

maxPeriod = minPeriod*5.0

endPeriod = round(maxPeriod)

signal = Abs((price-stored[endPeriod]))

noise = 0.00000000001

for k=1 to endPeriod do

noise=noise+Abs(price-stored[k])

averagePeriod = round(((signal/noise)*(maxPeriod-minPeriod))+minPeriod)

next

endif

alpha = (2.0+tconst)/(1.0+tconst+averagePeriod)

e1 = e1 + alpha*(price-e1)

e2 = e2 + alpha*(e1-e2)

v1 = 1.5 * e1 - 0.5 * e2

e3 = e3 + alpha*(v1 -e3)

e4 = e4 + alpha*(e3-e4)

v2 = 1.5 * e3 - 0.5 * e4

e5 = e5 + alpha*(v2 -e5)

e6 = e6 + alpha*(e5-e6)

Slow = 1.5 * e5 - 0.5 * e6

//------------------------------------

//--Signal moving average

OMAMACD = Slow-Fast

SigLength = Max(SigLength,1)

//---Signal MA

n = (Offset * (SigLength - 1))

t = SigLength/Sigma

SWtdSum = 0

SCumWt = 0

for k = 0 to SigLength - 1 do

SWtd = Exp(-((k-n)*(k-n))/(2*t*t))

SWtdSum = SWtdSum + SWtd * OMAMACD[SigLength - 1 - k]

SCumWt = SCumWt + SWtd

next

SIGMACD = SWtdSum / SCumWt

//------------------------------------

stored=price

//Conditions when to act

BullSMA=(SIGMACD<OMAMACD)

BearSMA=(SIGMACD>OMAMACD)

if (not longonmarket and BullSMA)then

buy amount shares at market

endif

if (longonmarket and BearSMA and positionperf>0) then

sell at market

endif

endif

graph sigmacd

graph omamacd

Matriciel – Please only use English in the English speaking forums. Using two languages just bloats the topics.

In the code it is OK to use the same variable name several times in different calculations as its new value for it is calculated prior to its use each time. Its previous value is not part of the calculation so that is fine.

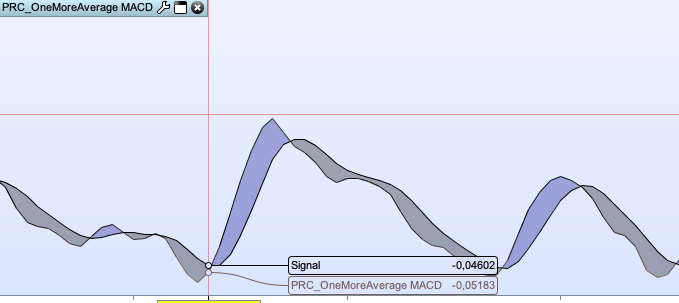

I just checked my code from my last post and it seems that the values of SIGMACD and OMAMACD are not calculated the same as the indicator returned values. Not sure why – might need to spend a little more time on this!

Thank you both! I tried to implement both your suggestions, but I still fail, now with an error… Thanks for your time!

//-------------------------------------------------------------------------

defparam cumulateorders=false

Defparam preloadbars=10000

amount = 10 //quantity of shares/contracts to open for each new order

//--------------------------------------------------------------------------------//

//Indicators

//Indicator: PRC_OneMoreAverage MACD

//Release date: 23.11.2016

//Web: https://www.prorealcode.com/prorealtime-indicators/one-more-average-macd/

//Code translator: Nicolas @ www.prorealcode.com

//--parameters

//>OMA parameters

Sensibility = 1

Adaptive = 1

//>MACD periods

FLength = 24

SLength = 52

//>signal line

SigLength = 9

Sigma = 4

Offset = 0.85

//--------

if barindex > 129 then

Speed = Sensibility

Speed = Max(Speed,-1.5)

price = average[1](customclose)

tconst=Speed

//--Fast moving average

FLength = Max(FLength,1)

//adaptive period

averagePeriod = FLength

if adaptive=1 and averagePeriod > 1 then

minPeriod = averagePeriod/2.0

maxPeriod = minPeriod*5.0

endPeriod = round(maxPeriod)

signal = Abs((price-stored[endPeriod]))

noise = 0.00000000001

for k=1 to endPeriod do

noise=noise+Abs(price-stored[k])

averagePeriod = round(((signal/noise)*(maxPeriod-minPeriod))+minPeriod)

next

endif

alpha = (2.0+tconst)/(1.0+tconst+averagePeriod)

e1 = e1 + alpha*(price-e1)

e2 = e2 + alpha*(e1-e2)

v1 = 1.5 * e1 - 0.5 * e2

e3 = e3 + alpha*(v1 -e3)

e4 = e4 + alpha*(e3-e4)

v2 = 1.5 * e3 - 0.5 * e4

e5 = e5 + alpha*(v2 -e5)

e6 = e6 + alpha*(e5-e6)

Fast = 1.5 * e5 - 0.5 * e6

//------------------------------------

//--Slow moving average

SLength = Max(SLength,1)

//adaptive period

SaveragePeriod = SLength

if adaptive=1 and SaveragePeriod > 1 then

SminPeriod = SaveragePeriod/2.0

SmaxPeriod = SminPeriod*5.0

SendPeriod = round(maxPeriod)

Ssignal = Abs((price-stored[SendPeriod]))

Snoise = 0.00000000001

for k=1 to SendPeriod do

Snoise=Snoise+Abs(price-stored[k])

SaveragePeriod = round(((Ssignal/Snoise)*(SmaxPeriod-SminPeriod))+SminPeriod)

next

endif

Salpha = (2.0+tconst)/(1.0+tconst+SaveragePeriod)

Se1 = Se1 + Salpha*(price-Se1)

Se2 = Se2 + Salpha*(Se1-Se2)

Sv1 = 1.5 * Se1 - 0.5 * Se2

Se3 = Se3 + Salpha*(Sv1 -Se3)

Se4 = Se4 + Salpha*(Se3-Se4)

Sv2 = 1.5 * Se3 - 0.5 * Se4

Se5 = Se5 + Salpha*(Sv2 -Se5)

Se6 = Se6 + Salpha*(Se5-Se6)

Slow = 1.5 * Se5 - 0.5 * Se6

//------------------------------------

//--Signal moving average

OMAMACD = Slow-Fast

SigLength = Max(SigLength,1)

//---Signal MA

n = (Offset * (SigLength - 1))

t = SigLength/Sigma

SWtdSum = 0

SCumWt = 0

for k = 0 to SigLength - 1 do

SWtd = Exp(-((k-n)*(k-n))/(2*t*t))

SWtdSum = SWtdSum + SWtd * OMAMACD[SigLength - 1 - k]

SCumWt = SCumWt + SWtd

next

SIGMACD = SWtdSum / SCumWt

//------------------------------------

stored=price

//------------------------------------

BullSMA=(SIGMACD<OMAMACD)

BearSMA=(SIGMACD>OMAMACD)

//--------------------------------------------------------------------------------//

//Conditions when to act

if (not longonmarket and BullSMA)then

buy amount shares at market

endif

if (longonmarket and BearSMA and positionperf>0) then

sell at market

endif

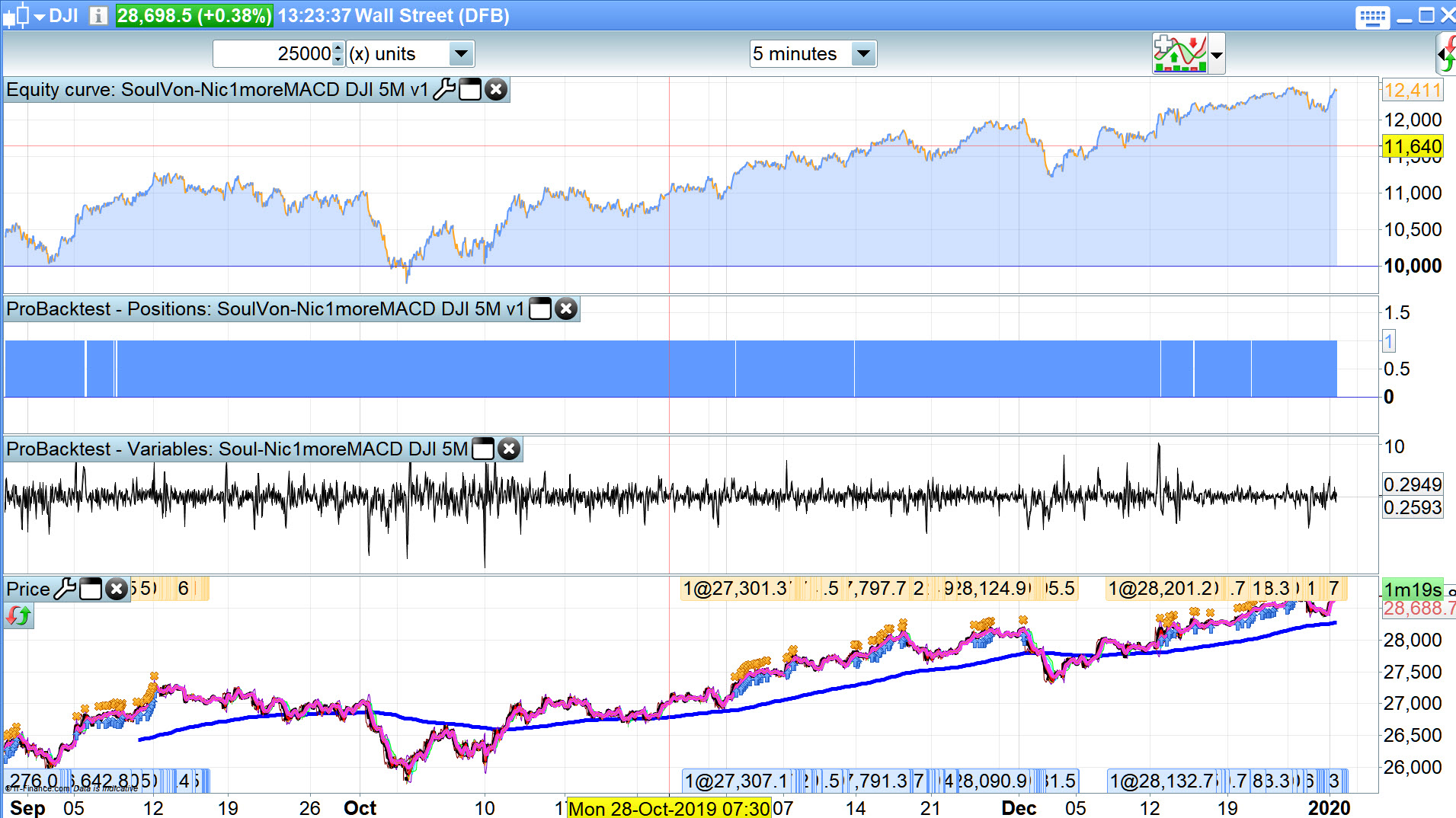

I used Vonasi version and got attached … no error messages.

Ain’t never seen a Gain to Loss ratio as high as attached!!

but I still fail, now with an error

Your version just needs an extra endif adding at line 131

for me in Soulintact to plot an other endif a the end

but Grahal what do you use as code because for me no result

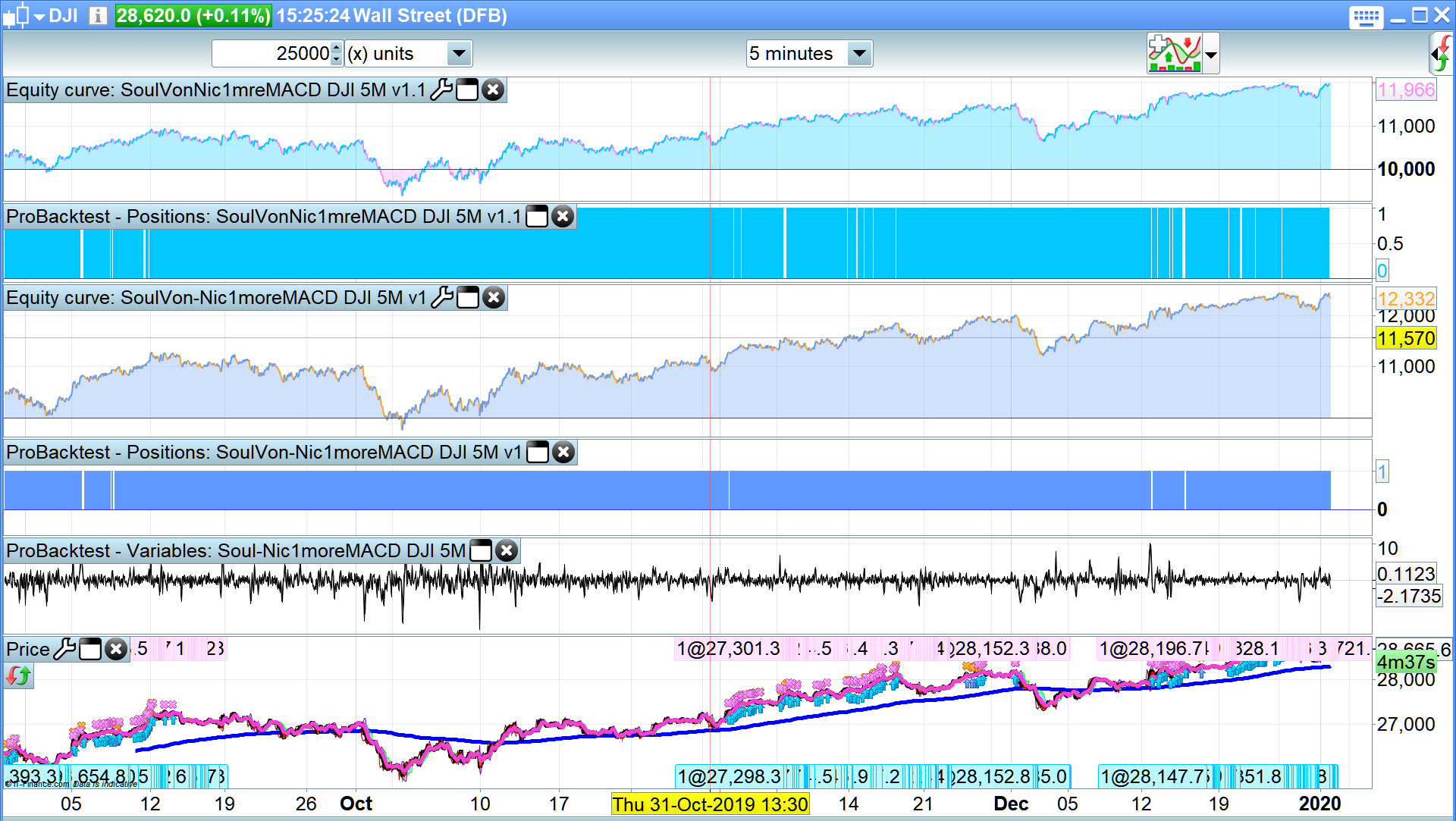

@Madrosat here you are … attached is Soulintact v1.1 as the top image.

All I did was add endif as the last line to Soulintact v1.1 version

Attached is the code

Ain’t never seen a Gain to Loss ratio as high as attached!!

That’s what happens if you never close any losing positions! The strategy does not exit unless it is profit. At some point you will find drawdown to be as impressive as gain/loss ratio!

Thank you for all your help. Truly appreciated! Take care and have a great start of 2020!

You too soulintact … keep on doing more of the same!!

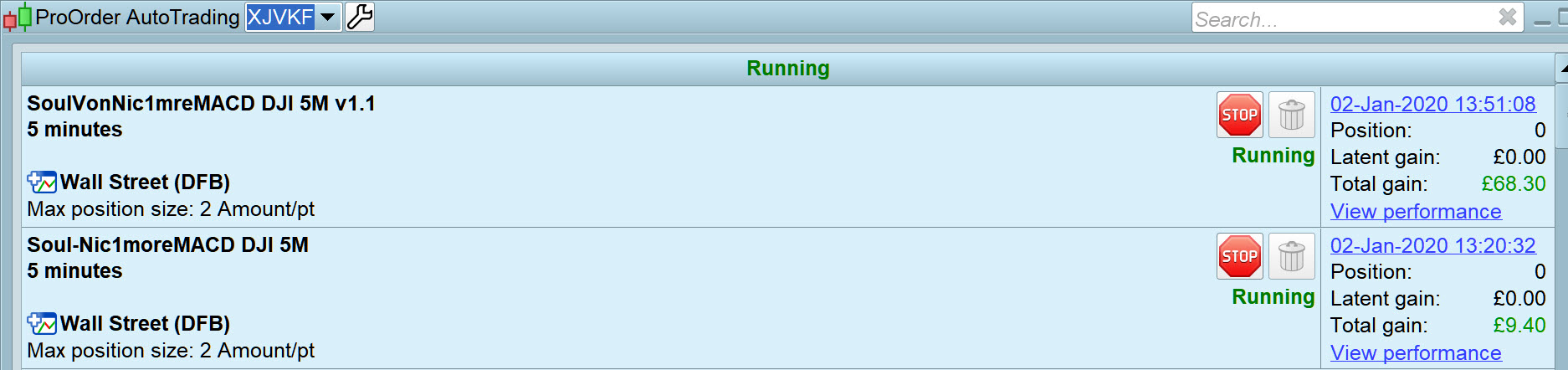

I wish I had put both versions Live … they’ve made nearly £80 over 3 trades in the last 3 hours!!!! hahahahaha