This is not my code but I have modified it a bit.

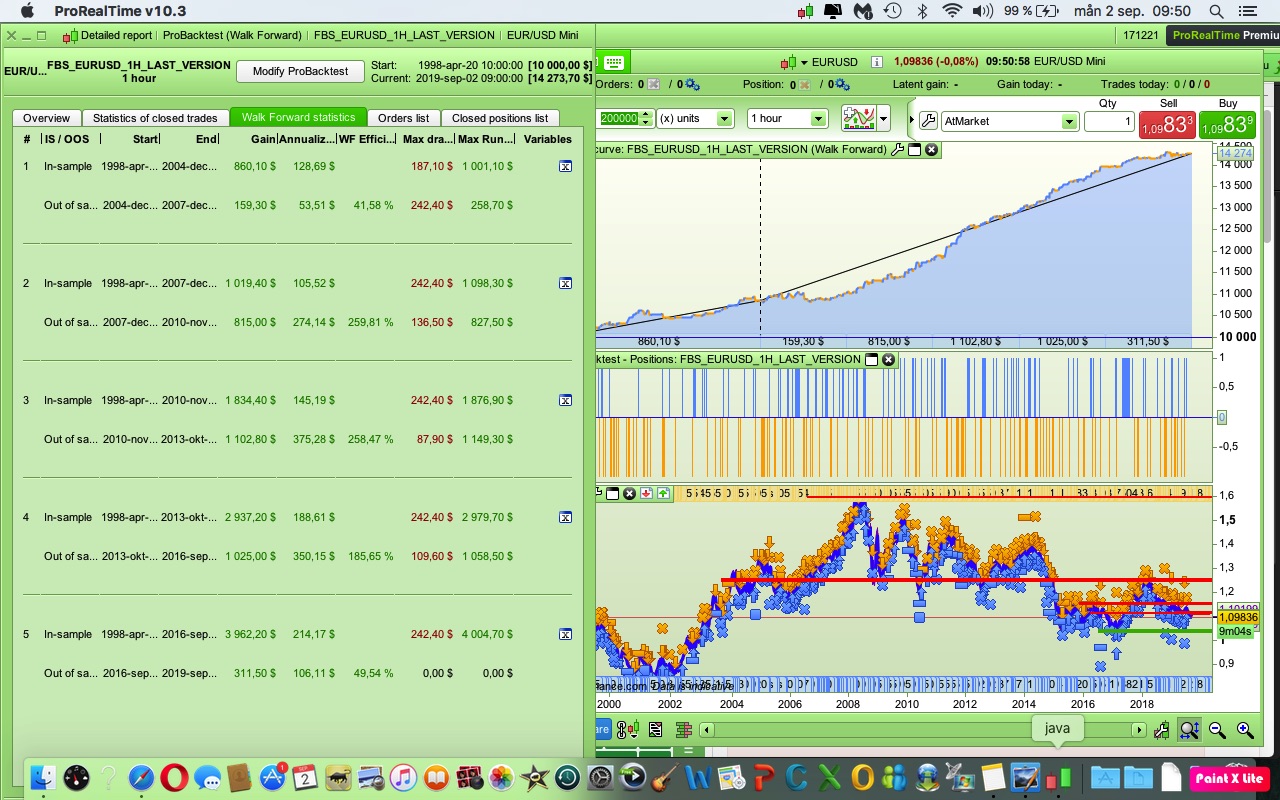

Optimized it with a regular back test. (100%)

Then I did a WF with 5 periods with 70% IS.

The result looks pretty good according to what I learned the last few days about WF.

DEFPARAM CumulateOrders = FALSE// Posizioni cumulate disattivate

ONCE trailingStopType = 1 // 0 NONE, 1 TRAILING

ONCE percprofit = 0.5 // 0.5

ONCE percloss = 1 // 1

ONCE barlong = 15 //15

ONCE barshort = 15 //15

ONCE atrtrailingperiod = 200 //200

ONCE minstop = 5 //5 Pipsize - least distance of the stop for IG

ONCE trailingstoplong = 15 //15 Trailing stop start and distance

ONCE trailingstopshort = 15 // 15

// FRACTAL

ONCE CP = 120 // 120

// MOVING AVERAGE

ONCE avgLongPeriod = 80 // 80

// CUMMRSI

ONCE CumRsiPer = 2 // 2

ONCE cumrsiEnterLongThreshold = 160 // 160

ONCE cumrsiEnterShortThreshold = 60 // 60

// TRAILINGSTOP

//----------------------------------------------

atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pointsize)

//atrtrail = AverageTrueRange[atrtrailingperiod]((close/10)*pointsize)/1000 // for indices divided for 1000

trailingstartl = round(atrtrail*trailingstoplong) //trailing stop start and distance

trailingstartS = round(atrtrail*trailingstopshort)

if trailingStopType = 1 THEN

TGL =trailingstartl

TGS=trailingstarts

if not onmarket then

MAXPRICE = 0

MINPRICE = close

PREZZOUSCITA = 0

ENDIF

if longonmarket then

MAXPRICE = MAX(MAXPRICE,close)

if MAXPRICE-tradeprice(1)>=TGL*pointsize then

if MAXPRICE-tradeprice(1)>=MINSTOP then

PREZZOUSCITA = MAXPRICE-TGL*pointsize

ELSE

PREZZOUSCITA = MAXPRICE - MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if shortonmarket then

MINPRICE = MIN(MINPRICE,close)

if tradeprice(1)-MINPRICE>=TGS*pointsize then

if tradeprice(1)-MINPRICE>=MINSTOP then

PREZZOUSCITA = MINPRICE+TGS*pointsize

ELSE

PREZZOUSCITA = MINPRICE + MINSTOP*pointsize

ENDIF

ENDIF

ENDIF

if onmarket and PREZZOUSCITA>0 then

EXITSHORT AT PREZZOUSCITA STOP

SELL AT PREZZOUSCITA STOP

ENDIF

ENDIF

// FILTER SETTING

///BILL WILLIAM FRACTAL INDICATOR

//CP=PERIOD

if Close[cp] >= highest[2*cp+1](Close) then

LH = 1

else

LH = 0

endif

if Close[cp] <= lowest[2*cp+1](Close) then

LL = -1

else

LL = 0

endif

if LH = 1 then

HIL = Close[cp]

endif

if LL = -1 then

LOL = Close[cp]

endif

PTN01 = (close CROSSES OVER HIL)

PTN02 = (close CROSSES UNDER LOL)

// CUMRSI

CUMRSI = SUMMATION[CUMRSIPER](RSI[CUMRSIPER](close))

// ENTRY

cumrsiFilterEnterLong = (cumrsi > cumrsiEnterLongThreshold)

cumrsiFilterEnterShort = (cumrsi < cumrsiEnterShortThreshold)

//MOVING AVERAGE

longAvg = Average[avgLongPeriod] (close)

//Enter

avgFilterEnterLong = (close>longAvg)

avgFilterEnterShort = (close<longAvg)

//--------------------------------------------------------------------------------------------------

// STRATEGY

//--------------------------------------------------------------------------------------------------

if (time >=100000 and time < 230000) then

IF NOT LongOnMarket AND avgFilterEnterLong AND PTN01 AND cumrsiFilterEnterLong THEN

BUY 1 CONTRACT AT MARKET

ENDIF

IF NOT ShortOnMarket AND avgFilterEnterShort AND PTN02 AND cumrsiFilterEnterShort THEN

SELLSHORT 1 CONTRACT AT MARKET

ENDIF

ENDIF

// Condizioni per uscire da posizioni long

IF POSITIONPERF<0 THEN

IF LongOnMarket AND BARINDEX-TRADEINDEX(1)>= barLong THEN

SELL AT MARKET

ENDIF

ENDIF

IF POSITIONPERF<0 THEN

IF shortOnMarket AND BARINDEX-TRADEINDEX(1)>= barshort THEN

EXITSHORT AT MARKET

ENDIF

ENDIF

SET STOP %LOSS percloss

SET TARGET %PROFIT percprofit

graph tgl

graph tgs

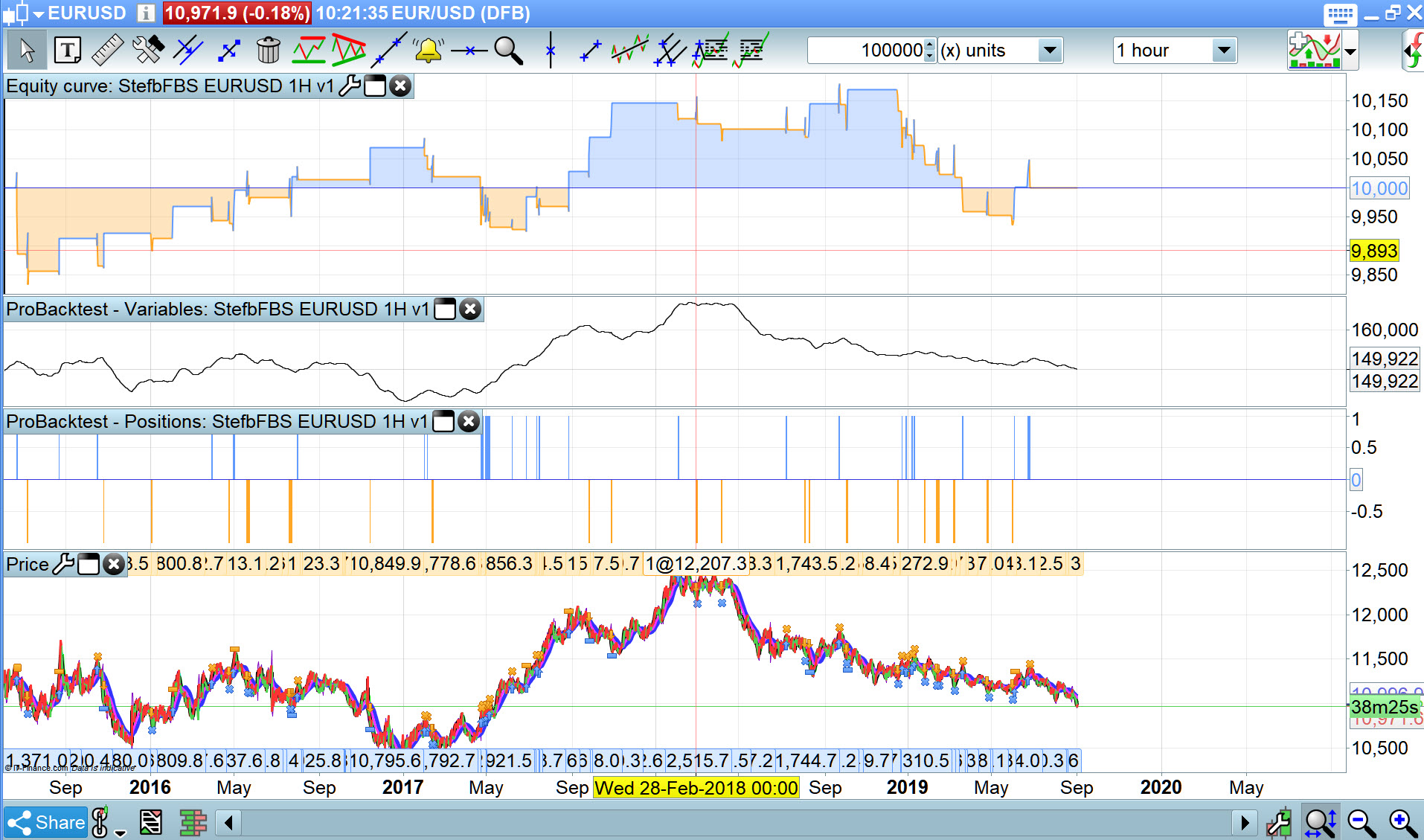

Strange I get better looking equity curve on DAX and DJI than I do on EURUSD over 100k bars, Spread = 2 in all images attached.

My results auger well for the strategy being robust (good on 2 Markets, maybe more? )

Why are my results on eurusd not good over 100k bars (3rd image attached). If I look at half of your equity curve over 200k bars on eurusd then yours increases steadily, mine does not!

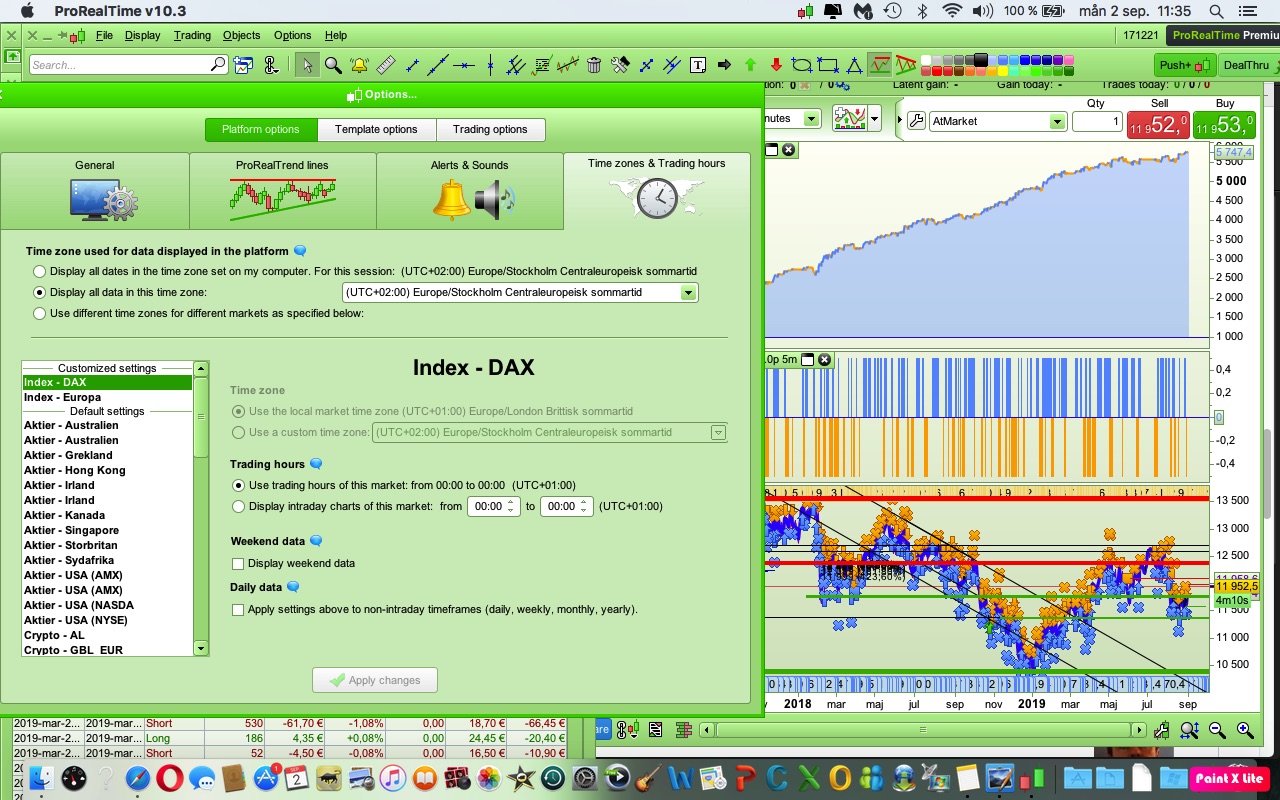

Ill go check timezones in the code and amend to match yours in Sweden.

Thanks anyway for sharing.

I have set it going on Demo DAX 1H for now.

Ill go check timezones

Yeah that was it … Times at Line 104 … knocked 1 hour off (to get same as Sweden) better equity curves on all 3 Markets now!

Nice one Stefan! 🙂

This is my time settings.

Must test DAX and DJ.

I use spread 1 on EURUSD.

knocked 1 hour off (to get same as Sweden)

I meant I set your 100000 (Sweden UTC +2) to 090000 (UTC+1 in UK)