There is the strategy, based on https://www.babypips.com/trading/so_youve_finished_the_school_o, I changed:

- 10-minute TF instead of 15

- SL and TP are fixed numbers, instead of being set at a swing price or the like

- added a sort of trailing stop to lock some profits

It seems to perform nicely (june 1st through today), even though I did not go through Walk Forward.

edit: this code is missing TIMEFRAME(default) after line 37, see the correct version (code and ITF file) at

https://www.prorealcode.com/topic/cowabunga-on-dax-with-multiple-time-frames/page/2/#post-147088

//************************************************************************

// Cowabunga DAX

//

// https://www.babypips.com/trading/so_youve_finished_the_school_o

//************************************************************************

//

DEFPARAM CumulateOrders = False //Do not cumulate orders

DEFPARAM FlatBefore = 090000 //No Trades before 09:00

DEFPARAM FlatAfter = 200000 //No Trades after 21:00

DEFPARAM PreLoadBars = 2000

////////////////////////////////////////////////////////////////////////

TIMEFRAME (10 minutes, updateonclose) //10 minutes instead of 15

ONCE nLots = 1

ONCE TP = 65 //65

ONCE SL = 50 //50

ONCE AvgType = 1 //1 = ema

ONCE FastMA = 5 //5

ONCE SlowMA = 10 //10

FastMA15m = Average[FastMA,AvgType](close)

SlowMA15m = Average[SlowMA,AvgType](close)

ONCE StocOS = 25 //25 - 75 OverSold/OverBought tresholds

ONCE StocOB = 100 - StocOS

StocK15m = Stochastic[10,3](close) //10, 3

StocD15m = Average[3](StocK15m) //3

ONCE RsiMiddle = 50 //50

ONCE RsiP = 9 //9

Rsi15m = Rsi[RsiP](close)

Macd15m = MACD[12,26,9](close) //12,26,9

////////////////////////////////////////////////////////////////////////

TIMEFRAME (4 hours, updateonclose) //4 hours (240 minutes)

FastMA4h = Average[FastMA,AvgType](close)

SlowMA4h = Average[SlowMA,AvgType](close)

StocK4h = Stochastic[10,3](close) //10, 3

StocD4h = Average[3](StocK4h) //3

Rsi4h = Rsi[RsiP](close)

//************************************************************************

// LONG trades

//************************************************************************

a0 = FastMA4h > SlowMA4h //FastMA > SlowMA on higher TF

a1 = FastMA15m CROSSES OVER SlowMA15m //FastMA crosses over SlowMA on lower TF

a2 = Rsi4h > RsiMiddle //Rsi > Middle line on higher TF

a3 = Rsi15m > RsiMiddle //Rsi > Middle line on lower TF

a4 = StocD4h > StocOS //D > OS on higher TF

a5 = StocK4h > StocD4h //K > D on higher TF

a6 = StocD15m > StocOS //D > OS on lower TF

a7 = StocK15m > StocD15m //K > D on lower TF

a8 = StocK4h < StocOB //K < OB on higher TF

a9 = Macd15m > Macd15m[1] //Macd increasing on lower TF

ax = a0 AND a1 AND a2 AND a3 AND a4 AND a5 AND a6 AND a7 AND a8 AND a9

IF ax AND Not OnMarket THEN

SET TARGET pPROFIT TP

SET STOP pLOSS SL

BUY nLots CONTRACT AT MARKET

ENDIF

//************************************************************************

// SHORT trades

//************************************************************************

b0 = FastMA4h < SlowMA4h //FastMA < SlowMA on higher TF

b1 = FastMA15m CROSSES UNDER SlowMA15m //FastMA crosses under SlowMA on lower TF

b2 = Rsi4h < RsiMiddle //Rsi < Middle line on higher TF

b3 = Rsi15m < RsiMiddle //Rsi < Middle line on lower TF

b4 = StocD4h < StocOB //D < OB on higher TF

b5 = StocK4h < StocD4h //K < D on higher TF

b6 = StocD15m < StocOB //D < OB on lower TF

b7 = StocK15m < StocD15m //K < D on lower TF

b8 = StocK4h > StocOS //K > OS on higher TF

b9 = Macd15m < Macd15m[1] //Macd decreasing on lower TF

bx = b0 AND b1 AND b2 AND b3 AND b4 AND b5 AND b6 AND b7 AND b8 AND b9

IF bx AND Not Onmarket THEN

SET TARGET pPROFIT TP

SET STOP pLOSS SL

SELLSHORT nLots CONTRACT AT MARKET

ENDIF

//////////////////////////////////////////////////////////////////////////////////////////////////////////

TIMEFRAME (default) //code to lock some profits

//////////////////////////////////////////////////////////////////////////////////////////////////////////

ONCE TrailStart = 15 //15 Start trailing profits from this point

ONCE ProfitPerCent = 0.400 //40.0% Profit to keep

IF Not OnMarket THEN

y1 = 0

y2 = 0

ELSIF LongOnMarket AND close > (TradePrice + (y1 * pipsize)) THEN //LONG

x1 = (close - tradeprice) / pipsize //convert price to pips

IF x1 >= TrailStart THEN //go ahead only if N+ pips

y1 = max(x1 * ProfitPerCent, y1) //y = % of max profit

ENDIF

IF y1 THEN //Place pending STOP order when y>0

SELL AT Tradeprice + (y1 * pipsize) STOP //convert pips to price

ENDIF

ELSIF ShortOnMarket AND close < (TradePrice - (y2 * pipsize)) THEN //SHORT

x2 = (tradeprice - close) / pipsize //convert price to pips

IF x2 >= TrailStart THEN //go ahead only if N+ pips

y2 = max(x2 * ProfitPerCent, y2) //y = % of max profit

ENDIF

IF y2 THEN //Place pending STOP order when y>0

EXITSHORT AT Tradeprice - (y2 * pipsize) STOP //convert pips to price

ENDIF

ENDIF

tryin to make an MoneyManagement-System for it 😀

Just had this System stopped with the message below.

No entry in the Orders List under Cancelled / Rejected.

Never had this message before, anybody had it or know what it means? Wished I’d taken a screen shot.

Strategy Forced Stop

Never had this message before, anybody had it or know what it means?

Nope – but I would send a report especially as it is an MTF strategy and any issues need to be reported so we can get MFT on live sooner rather than later fully tested.

Done! Tech Report sent!

Thanks for the prompt! 🙂

Any answer GraHal?

Usual problem … even if I had an acknowledgement from PRT for the Tech Report they rarely quote any information from the Tech Report (or didn’t used to) and so I have no copy of what I sent as the Tech Report.

I just spent 15 mins doing an e-search of my email account linked to my Platform (and 3 other email accounts) and I cannot find anything relating to the Issue / error message – “

Strategy Forced Stop” and also “forced stop”.

So I am sorry, but I have no reply / information to share.

Why anyway … have you had the same error message recently??

I never happened to see that message!

I’ve changed Timeframes (only) and set it going on Demo Forward Test on Dax.

I’ll report back if System gets rejected

Cowabunga System has executed 3 trades this morning with no rejections!

Hopefully that rejection reason / error I experienced over 12 months ago is gone for good!?

I think so, last June/July Nicolas reported that many issues between PRT and IG had been resolved, hopefully!

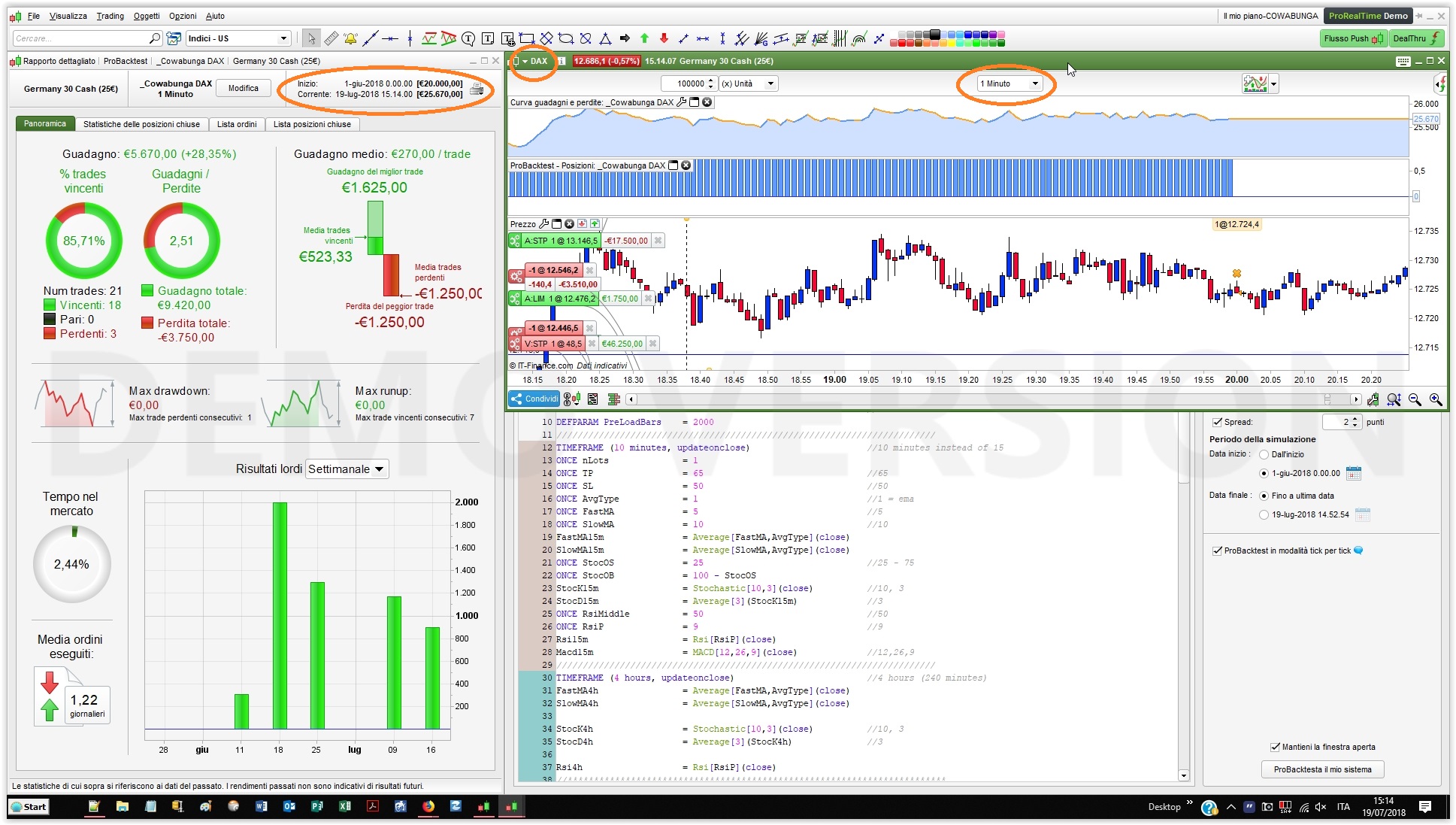

whenn i backtest it on dax1€ / 10 minutes, i have these results…Not really the same ratio Robertgozzi gave. I did an error somewhere?

No results on 1 min..

Mine was just over 40 days, yours is much longer.

Any strategy’s settings should be updated regularly. Once a month, I’d recommend.

If you plan to use settings so that it runs smoothly over one o more years then you’ll average down your profits, but you won’t spend much effort on it. If, instead, you aim to larger profits then you’ll have to update settings often, backtesting for shorter periods. This will imply more efforts, though.