Wisper Breakout Strategy SAF40

April 4, 2018, 9:48 AM

Strategies

6 Comments

{kind=link}

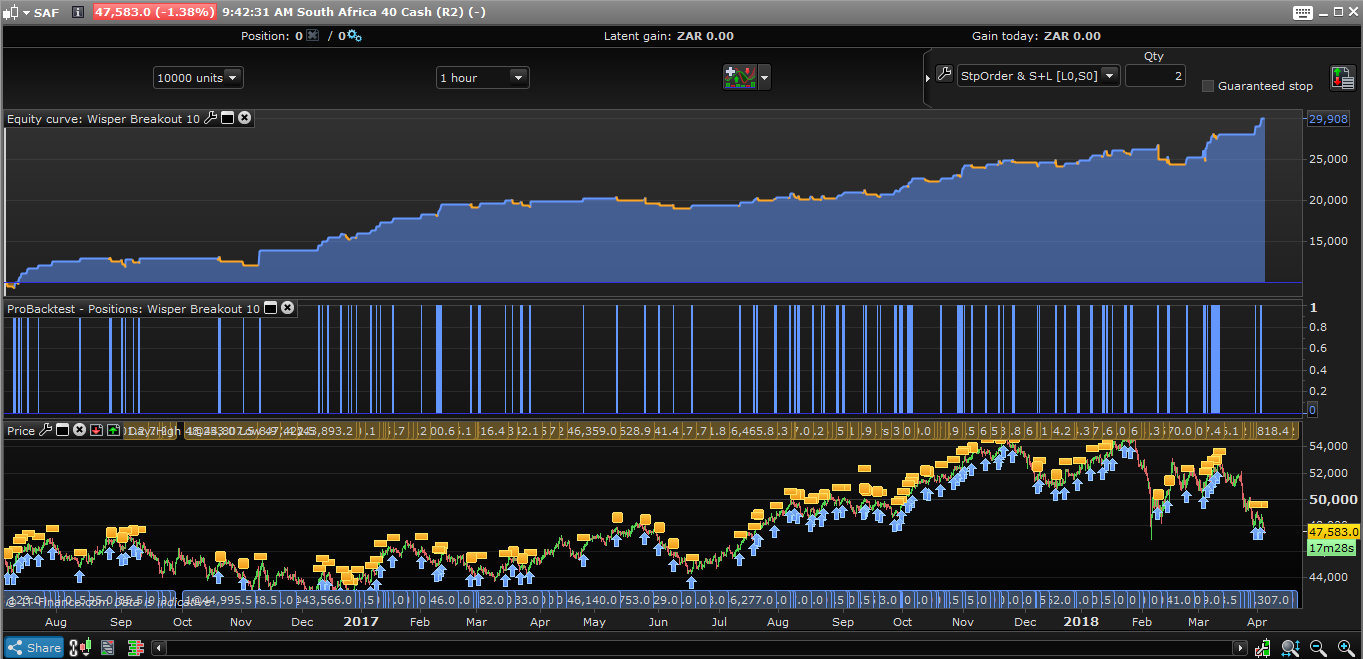

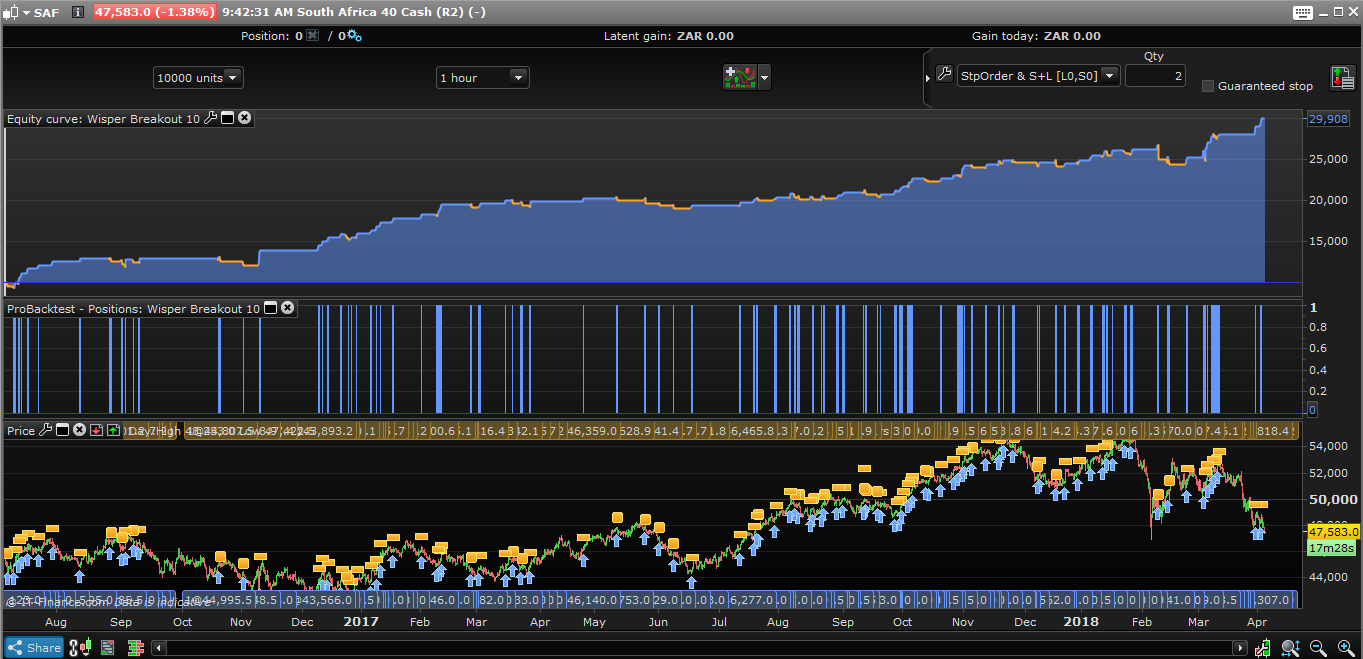

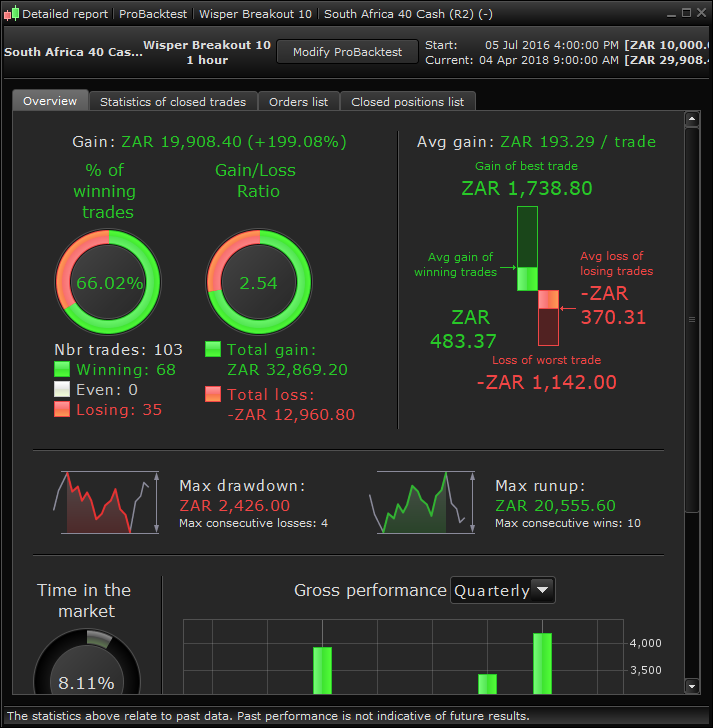

This strategy is one which takes advantage of only long opportunities in the SA Top 40 (SAF40) Index also known as the ALSI.

The code is testing if price is making new highs and lows before setting a new long order at market.

Target and loss levels are based upon the size of a factorized ATR 14 periods. Take profit size is larger than the stop loss one.

//-------------------------------------------------------------------------

// Main code : Wisper Breakout

//-------------------------------------------------------------------------

// Definition of code parameters

DEFPARAM CumulateOrders = false // Cumulating positions deactivated

daysForbiddenEntry = OpenDayOfWeek = 1 OR OpenDayOfWeek = 0

// Conditions to enter long positions

c1 = (close[3] <= high[4])

c2 = (close[3] >= low[4])

c3 = (close[2] <= high[3])

c4 = (close[2] >= low[3])

c5 = (close[1] <= high[2])

c6 = (close[1] >= low[2])

if high[4] > high[3] then

ath = high[4]

else

ath = high[3]

endif

if high[2] > ath then

ath = high[2]

else

ath = ath

endif

if high[1] > ath then

ath = high[1]

else

ath = ath

endif

c7 = (close > ath)

IF c1 AND c2 AND c3 AND c4 AND c5 AND c6 AND c7 AND not daysForbiddenEntry THEN

BUY 1 CONTRACT AT MARKET

ENDIF

// Stops and targets

atr = AverageTrueRange[14](close)

SET STOP pLOSS atr * 2

SET TARGET pPROFIT atr * 2.5

Download

Filename:

Wisper-Breakout-10H.itf

Downloads:

376

Download

{kind=link}

Filename:

wisper2.png

Downloads:

111

Download

{kind=link}

Filename:

wisper.png

Downloads:

218

New

Developer by day, aspiring writer by night. Still compiling my bio... Error 404: presentation not found.

Author’s Profile

Loading...